WAREHOUSE MARKET REPORT Moscow

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Moscow, Russia

Moscow, Russia INGKA Centres The bridge 370 STORES 38,6 MLN to millions of customers VISITORS ANNUALLY From families to fashionistas, there’s something for everyone meeting place where people connect, socialise, get inspired, at MEGA Belaya Dacha that connects people with inspirational experience new things, shop, eat and naturally feel attracted lifestyle experiences. Supported by IKEA, with more than to spend time. 370 stores, family entertainment and on-trend leisure and dining Our meeting places will meet people's needs & desires, build clusters — it’s no wonder millions of visitors keep coming back. trust and make a positive difference for local communities, Together with our partners and guests we are creating a great the planet and the many people. y w h e Mytischi o k v s la Khimki s o r a Y e oss e sh sko kov hel D RING RO c IR AD h ov Hwy TH S ziast ntu MOSCOW E Reutov The Kremlin Ryazansky Avenue Zheleznodorozhny Volgogradskiy Prospect Lyubertsy Kuzminki y Lyublino Kotelniki w H e o Malakhovka k s v a Dzerzhinsky h s r Zhukovskiy a Teply Stan V Catchment Areas People Distance Kashirskoe Hwy Lytkarino Novoryazanskoe Hwy ● Primary 1,600,000 < 20 km ● Secondary 1,600,000 20–35 km ● Tertiary 3,800,000 35–47 km Gorki Total area: <47 km: 7,000,000 Leninskiye Volodarskogo 55% 25 3 METRO 34 MIN CUSTOMERS BUS ROUTES STATIONS AVERAGE COME BY CAR NEAR BY COMMUTE TIME A region with Loyal customers MEGA Belaya Dacha is located at the heart of the very dynamic population development in strong potential the South-East of Moscow and attracts shoppers from all over Moscow and surrounding areas. -

MEGA Belaya Dacha Le N in G R Y a D W S H V K Olo O E K E O O Mytischi Lam H K Sk W S O Y Av E

MEGA Belaya Dacha Le n in g r y a d w s h V k olo o e k e o o Mytischi lam h k sk w s o y av e . sl o h r w a y Y M K Tver A Market overview D region Balashikha Dmitrov Krasnogorsk y Welcome v hw Sergiev-Posad hw uziasto oe y nt Klin Catchment Peoplesk Distance E Vladimir region izh or Reutov ov to MEGA N Mytischi Pushkin areas Schelkovo Belaya Dacha Moscow Zheleznodorozhny Primary 1,589,000 < 20 km Smolensk region Odintsovo N Naro-Fominsk o Podolsk v o ry a Klimovsk wy z Secondary 1,558,800 h 20–35 km a oe n k sk ins o Obninsk Kolomna M e y h hw w oe y Serpukhov Tertiary 3,787,300 35–47vsk km ALONG WITH LONDON’S WESTFIELD Kaluga region Kie AND ISTANBUL’S FORUM, MEGA BELAYA y y w Tula region h w h DACHA IS ONE OF EUROPE’S LARGEST e ko e Total area: 6,965,200 s o z h k RETAIL COMPLEXES. s lu Troitsk a v K a h s r a Domodedovo V It has more than 350 tenants and the centre Moscow has the highest density of retailers façade runs for four km. Major brands such of all Russian cities with tenants occupying as Auchan, Inditex brands, TopShop, H&M, 4.5 million square metres, according to fig- Uniqlo, T.G.I. Fridays, Debenhams, MAC, ures for 2013. Many world-famous retailers IKEA, OBI, MediaMarkt, Kinostar, Cosmic, have outlets here and the city is the first M.Video, Detsky Mir, Deti and Decathlon to show new trends. -

Moscow United Electric Grid Company” As of July 13, 2007 (Minutes No.46 As of July 17, 2007)

Approved by the Board of Directors decision of Open Joint-Stock Company “Moscow United Electric Grid Company” as of July 13, 2007 (Minutes No.46 as of July 17, 2007) Amendments No. 1 to the Charter Open Joint-Stock Company “Moscow United Electric Grid Company” To introduce the following amendments in the Charter of Open Joint-Stock Company “Moscow United Electric Grid Company”: To state the Company List of Branches (Appendix No. 1 to the Charter) as follows: List of Branches OJSC “Moscow United Electric Grid Company” No. Name Address 1. Central Electric Networks 115201, Moscow city, Kashirskoye highway, 18 2. Southern Electric Networks 115201, Moscow city, Kashirskoye highway, 18 3. Eastern Electric Networks 107140, Moscow city, Nizhnyaya Krasnoselskaya street, 6, bld. 1 4. Oktyabrskie Electric Netwowrks 127254, Moscow city, Rustaveli street, 2 5. Northern Electric Networks 141070, Moscow region, Korolev city, Gagarina street, 4 6. Noginsk Electric Networks 142400, Moscow region, Noginsk city, Radchenko street, 13 7. Podolsk Electric Networks 142117, Moscow region, Podolsk city, Kirova street, 65 8. Kolomna Electric Networks 140408, Moscow region, Kolomna city, Oktyabrskoy Revolyutsii street, 381а 9. Shatura Electric Networks 140700, Moscow region, Shatura city, Sportivnaya street, 12 10. Western Electric Networks 121170, Moscow city, 1812 Goda street, estate 15 11. Kashira Electric Networks 142900, Moscow region, Kashira city, Klubnaya street, 4 12. Mozhaisk Electric Networks 143200, Moscow region, Mozhaisk city, Mira street, 107 13. Dmitrov Electric Networks 141800, Moscow region, Dmitrov city, Kosmonavtov street, 46 14. Volokolamsk Electric Networks 143600, Moscow region, Volokolamsk city, Novosoldatskaya street, 58 15. Moskabelenergoremont (MKER) 115569, Moscow city, Shipilovskaya street, 13, bld. -

Glass in Ancient and Medieval Eastern Europe As Evidence of International Contacts

Archeologia Polski 61 (2016), pp. 191-212 Archeologia Polski, LXI: 2016 PL ISSN 0003-8180 Ekaterina STOLYAROVA GLASS IN ANCIENT AND MEDIEVAL EASTERN EUROPE AS EVIDENCE OF INTERNATIONAL CONTACTS Abstract: This paper deals with glass artifacts as markers of interregional economic, religious and cultural links, trade routes, and social stratification. It is focused on finds from Eastern Europe from the Bronze Age to the 17th–18th centuries A.D. Keywords: glass beads, glass vessels, Eastern Europe, international links. Introduction Glass is one of the most ancient artificial materials possessing unique properties from which a variety of artifacts can be made. Among these are luxury artifacts and objects of applied art, tesserae for figured mosaics and stained glass, glass icons and ritual vessels, window-panes and tableware as well as small ornaments, i.e., arm rings, beads, fingerings, buttons and pendants. These artifacts were used in daily life, sold, donated, used to decorate clothes, interiors and architectural structures. They were symbols of their owner’s social and economic position. The value of glass as a historical source stems from its extensive application. Glass objects provide information on the formation and spread of glassmaking and on the place of glass in scientific concepts and the production of a given epoch. Chemical properties of glass and means of its production are of technological interest. Glass artifacts are important for the study of culture and daily life of a given epoch, e.g. the history of costume. Excavated glass objects are examined from the angle of their functions, peculiarities of their form and decoration, the spread and evolution of different type. -

MEGA Khimki Tver Region Market Overview Welcome

MEGA Khimki Tver region Market overview Welcome Dmitrov L e y n Sergiev-Posad Catchment areas People Distance i w y n h to MEGA Khimki Klin g w r a e h V Vladimir d o ol s e o k ko k o region la o s k m e v s Pushkin s Mytischi ko h o av e w r sl t Schelkovo y i o h . r a w m y Y Primary 398,200 < 17 km D Zheleznodorozhny M K A Smolensk Moscow D Balashikha region Podolsk Naro-Fominsk Secondary 1,424,200 17–40 km Krasnogorsk y Klimovsk v hw hw uziasto oe y nt RUSSIA’S FIRST IKEA WAS OPENED IN sk E Obninsk izh Kolomna or Reutov Tertiary 3,150,656 40–140 km ov KHIMKI IN 2000. MEGA KHIMKI SOON N Serpukhov FOLLOWED IN 2004 AND BECAME THE Kaluga region LARGEST RETAIL COMPLEX IN RUSSIA Tula region Total area: 4,973,000 AT THE TIME. Odintsovo N o v o ry y a hw z e a ko n s sk Min o e wy h h w oe y vsk Kie Despite several new retail centres opening their doors along the Leningradskoe Shosse, y y w w h MEGA Khimki remains one of the district’s h e oe o sk k most popular shopping destinations, largely s h Troitsk z Scherbinka v u a al due to its location, well-designed layout and K h s r retail mix. a V Domodedovo New tenants and constant improvements to the centre have significantly increased customer numbers. -

Download Presentation

WAREHOUSE REAL ESTATE 7 % of the market of class A warehouse property of Russia --- Management company MLP --- 1.8 million sq.m - total area of class A warehouses ----------------------------------------------------------------------------------- 8 operating class A warehouse facilities ----------------------------------------------------------------------------- 1.5 million sq.m - 6 facilities - Moscow region ------------------------------------------------------------------------- 209.600 sq.m - 1 facility - the city of Saint-Petersburg ----------------------------------------------------------------------- 113.900 sq.m - 1 facility - Ukraine, the city of Kiev ---------------------------------------------------------------------- 49.5 ha - land bank --- FINANCIAL PARTNERS --- 2 1 9 % of the market of warehouse property of Moscow region ------------------------------- ----------------------------- Warehouse Complex Warehouse Complex Leningradskiy Terminal Nikolskoe ------------------------------- ----------------------------- ----------------------------- Warehouse Complex ----------------------------- Tomilino Warehouse Complex ----------------------------- Podolsk ----------------------------- ----------------------------- -------------------------------- Warehouse Complex Warehouse Complex Chekhov Severnoe Domodedovo ----------------------------- -------------------------------- 1.5 million sq.m (82% of the total storage space of MLP Management Company) are located in the Moscow region 2 Warehouse Complex Severnoe Domodedovo Facility -

Construction of Public Roads at the Meeting Point of Different Legislation Systems

Journal of Ecological Engineering Volume 18, Issue 6, Nov. 2017, pages 86–94 DOI: 10.12911/22998993/76217 Research Article CONSTRUCTION OF PUBLIC ROADS AT THE MEETING POINT OF DIFFERENT LEGISLATION SYSTEMS Maria Hełdak¹, Elena Bykowa² ¹ Wroclaw University of Environmental and Life Sciences, Department of Spatial Economy, ul. Grunwaldzka 55, 50-357 Wrocław, Poland, e-mail: [email protected] ² Saint-Petersburg Mining University, Department of Engineering Geodesy, Russia, e-mail: [email protected] Received: 2017.07.07 ABSTRACT Accepted: 2017.08.12 The study discusses the topic of transport accessibility in Poland and the Russian Published: 2017.11.01 Federation. The authors have analysed the principles of acquiring land for the con- struction of public roads, network development and problems that accompany the development of national roads. Since the political transformation at the beginning of the 1990’s, Poland and Russian Federation have been in the need of legislative changes that would facilitate the acquisition of land for road investments. The study presents the dynamic development of the national roads system in Poland, after the accession to the European Union, and improvement of the communication system in the Russian Federation. Keywords: road density, development of transportation networks, public roads, Russian Federation, Poland INTRODUCTION differences in transport accessibility. Since then, Poland has benefitted from the opportunity to Poland has been struggling with the problem use EU subsidies and funding. The use of means of transport accessibility for a long time. In spite of from the European budget for infrastructural de- numerous investments in this area, deficits in the velopment forced the Polish government to take system of road networks and international routes actions to provide legal regulations with respect are still visible. -

Invest in Moscow Region

INVEST IN MOSCOW REGION LOCATION GENERAL INFORMATION Dubna Sergiev Posad Mytishchy Population - 7.1 million Korolev Khimki Balashiha Urban population - 80% Odintsovo Lyubertsy More than 100 000 people live Zhukovsky in 20 cities of Moscow Region Podolsk Shatura Zaraysk DEVELOPED TRANSPORT INFRASTRUCTURE Road density km/1000 km2 3 international airports 232 Total passengers - 60 million people/year The total volume of cargo transportation in Russia (%) Moscow Central Federal Region District of Russia Density of railways 40 km/1000 km2 60 26 - Volume of cargo transportation in Moscow and Central Federal Moscow Region Moscow District of Russia Region QUALIFIED WORK FORCE Key Facts: 4.5 million people are 18-60 years old Salaries are 30% lower than in Moscow 71% of population has a higher education or vocational training CITIES OF MOSCOW REGION HAVE HISTORICALLY HIGH PERSONNEL POTENTIAL INNOVATIVE, HIGH-TECH HI-TECH BIOTECHNOLOGY DEVELOPMENT and SPACE ENGINEERING PHARMACEUTICALS Korolev, Podolsk, Dubna Podolsk, Kolomna, Klimovsk Pushchino, Chernogolovka, Obolensky Population Population Population 464 793 people 404 583 people 47 615 people THE LARGEST CONSUMER MARKET IN RUSSIA Tver region 30 million people live in the Moscow agglomeration or 20% of Russia's Smolensk region 300 km population Yaroslavl 1/3 of consumer spending in Russia Kaluga region region Tula region Ivanovo region Vladimir region Ryazan region ECONOMIC AND INVESTMENT INDICATORS Gross regional product of Regions of the Russian Federation (2012, billion USD) 352.57 -

The Chronicle of Novgorod 1016-1471

- THE CHRONICLE OF NOVGOROD 1016-1471 TRANSLATED FROM THE RUSSIAN BY ROBERT ,MICHELL AND NEVILL FORBES, Ph.D. Reader in Russian in the University of Oxford WITH AN INTRODUCTION BY C. RAYMOND BEAZLEY, D.Litt. Professor of Modern History in the University of Birmingham AND AN ACCOUNT OF THE TEXT BY A. A. SHAKHMATOV Professor in the University of St. Petersburg CAMDEN’THIRD SERIES I VOL. xxv LONDON OFFICES OF THE SOCIETY 6 63 7 SOUTH SQUARE GRAY’S INN, W.C. 1914 _. -- . .-’ ._ . .e. ._ ‘- -v‘. TABLE OF CONTENTS PAGE General Introduction (and Notes to Introduction) . vii-xxxvi Account of the Text . xxx%-xli Lists of Titles, Technical terms, etc. xlii-xliii The Chronicle . I-zzo Appendix . 221 tJlxon the Bibliography . 223-4 . 225-37 GENERAL INTRODUCTION I. THE REPUBLIC OF NOVGOROD (‘ LORD NOVGOROD THE GREAT," Gospodin Velikii Novgorod, as it once called itself, is the starting-point of Russian history. It is also without a rival among the Russian city-states of the Middle Ages. Kiev and Moscow are greater in political importance, especially in the earliest and latest mediaeval times-before the Second Crusade and after the fall of Constantinople-but no Russian town of any age has the same individuality and self-sufficiency, the same sturdy republican independence, activity, and success. Who can stand against God and the Great Novgorod ?-Kto protiv Boga i Velikago Novgoroda .J-was the famous proverbial expression of this self-sufficiency and success. From the beginning of the Crusading Age to the fall of the Byzantine Empire Novgorod is unique among Russian cities, not only for its population, its commerce, and its citizen army (assuring it almost complete freedom from external domination even in the Mongol Age), but also as controlling an empire, or sphere of influence, extending over the far North from Lapland to the Urals and the Ob. -

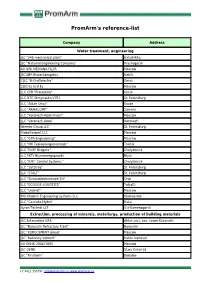

Promarm's Reference-List

PromArm's reference-list Company Address Water treatment, engineering JSC "345 mechanical plant" Balashikha JSC "National Engineering Company" Krasnogorsk AO NPK MEDIANA-FILTR Moscow JSC NPP Biotechprogress Kirishi CJSC "B-Graffelectro" Omsk CJSC Es End Ey Moscow LLC CPB "Protection" Omsk LLC NTC Stroynauka-VITU St. Petersburg LLC "Aidan Stroy" Kazan LLC "ARMACOMP" Samara LLC "Voronezh-Aqua Invest" Moscow LLC "Voronezh-Aqua" Voronezh Hermes Group LLC St. Petersburg Globaltexport LLC Moscow LLC "GPA Engineering" Moscow LLC "MK Teploenergomontazh" Troitsk LLC "NVK" Niagara " Chelyabinsk LLC PKTs Biyskenergoproekt Biysk LLC "RPK" Control Systems " Chelyabinsk LLC "SetStroy" St. Petersburg LLC "STALT" St. Petersburg LLC "Stroisantechservice-1N" Orsk LLC "ECOLINE-LOGISTICS" Tolyatti LLC "Unimet" Moscow PKK Modern Engineering Systems LLC Vladivostok LLC "Cascade-Hydro" Baku Ayron-Technik LLP Ust-Kamenogorsk Extraction, processing of minerals, metallurgy, production of building materials JSC Aldanzoloto GRK Aldan ulus, pos. Lower Kuranakh JSC "Borovichi Refractory Plant" Borovichi JSC "EUROCEMENT group" Moscow JSC "Katavsky cement" Katav-Ivanovsk AO OKHK URALCHEM Moscow JSC OEMK Stary Oskol-15 JSC "Firstborn" Bodaibo +7 8412 350797, [email protected], www.promarm.ru JSC "Aleksandrovsky Mine" Mogochinsky district of Davenda JSC RUSAL Ural Kamensk-Uralsky JSC "SUAL" Kamensk-Uralsky JSC "Khiagda" Bounty district, with. Bagdarin JSC "RUSAL Sayanogorsk" Sayanogorsk CJSC "Karabashmed" Karabash CJSC "Liskinsky gas silicate" Voronezh CJSC "Mansurovsky career management" Istra district, Alekseevka village Mineralintech CJSC Norilsk JSC "Oskolcement" Stary Oskol CJSC RCI Podolsk Refractories Shcherbinka Bonolit OJSC - Construction Solutions Old Kupavna LLC "AGMK" Amursk LLC "Borgazobeton" Boron Volga Cement LLC Nizhny Novgorod LLC "VOLMA-Absalyamovo" Yutazinsky district, with. Absalyamovo LLC "VOLMA-Orenburg" Belyaevsky district, pos. -

CRR) of Moscow Region, Start-Up Complex № 4

THE CENTRAL RING ROAD OF MOSCOW REGION INFORMATION MEMORANDUM Financing, construction and toll operation of the Central Ring Road (CRR) of Moscow Region, start-up complex № 4 July 2014, Moscow Contents Introduction 3–4 Project goals and objectives 5–7 Relevance of building the Central Ring Road Timeline for CRR project implementation Technical characteristics Brief description 8–34 Design features Cultural legacy and environmental protection Key technical aspects Concession agreement General provisions 34–37 Obligations of the concessionaire Obligations of the grantor Project commercial structure 38–46 Finance. Investment stage Finance. Operation stage Risk distribution 47–48 Tender criteria 49 Preliminary project schedule 50 The given information memorandum is executed for the purpose of acquainting market players in good time with information about the given project and the key conditions for its implementation. Avtodor SC reserves the right to amend this memorandum. 2 Introduction The investment project for construction and subsequent toll operation of the Central Ring Road of the Moscow Region A-113 consists of five Start-up complexes to be implemented on a public-private partnership basis. Start-up complex No. 4 of the Central Ring Road (the Project or SC No.4 of the CRR) provides for construction of a section of the CRR in the south-east of the Moscow Region, stretching from the intersection with the M-7 Volga express highway currently under construction to the intersection with the M-4 public highway. Section SC No. 4 of the CRR was distinguished as a separate investment project because the given section is of major significance both for the Region and for the economy of the Russian Federation in general. -

As of June 30, 2018

LIST OF AFFILIATES Sberbank of Russia (full corporate name of the joint-stock company) Issuer code: 0 1 4 8 1 – В as 3 0 0 6 2 0 1 8 of (indicate the date on which the list of affiliates of the joint-stock company was compiled) Address of the issuer: 19, Vavilova St., Moscow 117997 (address of the issuer – the joint-stock company – indicated in the Unified State Register of Legal Entities where a body or a representative of the joint-stock company is located) Information contained in this list of affiliates is subject to disclosure pursuant to the laws of the Russian Federation on securities. Website: http://www.sberbank.com; http://www.e-disclosure.ru/portal/company.aspx?id=3043 (the website used by the issuer to disclose information) Deputy Chairperson of the Executive Board of Sberbank B. Zlatkis (position of the authorized individual of the joint-stock company) (signature) (initials, surname) L.S. “ 03 ” July 20 18 . Issuer codes INN (Taxpayer Identificat ion Number) 7707083893 OGRN (Primary State Registrati on Number) 1027700132195 I. Affiliates as of 3 0 0 6 2 0 1 8 Item Full company name (or name for a Address of a legal entity or place of Grounds for recognizing the entity Date on which Interest of the affiliate Percentage of ordinary No. nonprofit entity) or full name (if any) of residence of an individual (to be as an affiliate the grounds in the charter capital of shares of the joint- the affiliate indicated only with the consent of became valid the joint-stock stock company owned the individual) company, % by the affiliate, % 1 2 3 4 5 6 7 Entity may manage more than The Central Bank of the Russian 12, Neglinnaya St., Moscow 20% of the total number of votes 1 21.03.1991 50.000000004 52.316214 Federation 107016 attached to voting shares of the Bank 1.