Download The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Proquest Dissertations

OPPOSITION TO CONSCRIPTION IN ONTARIO 1917 A thesis submitted to the Department of History of the University of Ottawa in partial fulfillment of the requirements for the Degree of Master of Arts. % L,., A: 6- ''t, '-'rSily O* John R. Witham 1970 UMI Number: EC55241 INFORMATION TO USERS The quality of this reproduction is dependent upon the quality of the copy submitted. Broken or indistinct print, colored or poor quality illustrations and photographs, print bleed-through, substandard margins, and improper alignment can adversely affect reproduction. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if unauthorized copyright material had to be removed, a note will indicate the deletion. UMI UMI Microform EC55241 Copyright 2011 by ProQuest LLC All rights reserved. This microform edition is protected against unauthorized copying under Title 17, United States Code. ProQuest LLC 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106-1346 TABLE OF CONTENTS PAGE INTRODUCTION 1 CHAPTER ONE:IDEOLOGICAL OPPOSITION 8 CHAPTER TWO:THE TRADE UNIONS 33 CHAPTER THREE:THE FARMERS 63 CHAPTER FOUR:THE LIBERAL PARTI 93 CONCLUSION 127 APPENDIX A# Ontario Liberals Sitting in the House of Commons, May and December, 1917 • 131 APPENDIX B. "The Fiery Cross is now uplifted throughout Canada." 132 KEY TO ABBREVIATIONS 135 BIBLIOGRAPHY 136 11 INTRODUCTION The Introduction of conscription in 1917 evoked a deter mined, occasionally violent opposition from French Canadians. Their protests were so loud and so persistent that they have tended to obscure the fact that English Canada did not unanimous ly support compulsory military service. -

Lesson Plan with Activities: Political

LESSON PLAN POLITICAL PARTIES Recommended for Grade 10 Duration: Approximately 60 minutes BACKGROUND INFORMATION Parliamentary Roles: www.ola.org/en/visit-learn/about-ontarios-parliament/ parliamentary-roles LEARNING GOALS This lesson plan is designed to engage students in the political process through participatory activities and a discussion about the various political parties. Students will learn the differences between the major parties of Ontario and how they connect with voters, and gain an understanding of the important elements of partisan politics. INTRODUCTORY DISCUSSION (10 minutes) Canada is a constitutional monarchy and a parliamentary democracy, founded on the rule of law and respect for rights and freedoms. Ask students which country our system of government is based on. Canada’s parliamentary system stems from the British, or “Westminster,” tradition. Since Canada is a federal state, responsibility for lawmaking is shared among one federal, ten provincial and three territorial governments. Canada shares the same parliamentary system and similar roles as other parliaments in the Commonwealth – countries with historic links to Britain. In our parliament, the Chamber is where our laws are debated and created. There are some important figures who help with this process. Some are partisan and some are non-partisan. What does it mean to be partisan/non-partisan? Who would be voicing their opinions in the Chamber? A helpful analogy is to imagine the Chamber as a game of hockey, where the political parties are the teams playing and the non-partisan roles as the people who make sure the game can happen (ex. referees, announcers, score keepers, etc.) LEGISLATIVE ASSEMBLY OF ONTARIO POLITICAL PARTIES 01 EXPLANATION (5 minutes) Political Parties: • A political party is a group of people who share the same political beliefs. -

C,Anadä LIBERÄL PÄRÏY ORGAI{IZÂTIOII AI{D

N,flonalLtbrav Bibliothèque nationale l*l du Canada Acquisitions and Direction des acquisitions et Bibliog raphic Services Branch des services bibliograPhiques 395 Wellington Street 395, rue Wellington Ottawa, Ontario Ottawa (Ontario) K1A ON4 K.lA ON4 Yout l¡le Volre élérence Our lile Noue rclércnce The author has granted an L'auteur a accordé une licence irrevocable non-exclus¡ve licence irrévocable et non exclus¡ve allowing the National Library of permettant à la Bibliothèque Canada to reproduce, loan, nationale du Canada de distribute or sell cop¡es of reproduire, prêter, distribuer ou his/her thesis by any means and vendre des copies de sa thèse in any form or format, making de quelque manière et sous this thesis available to interested quelque forme que ce soit pour persons. mettre des exemplaires de cette thèse à Ia disposition des personnes intéressées. The author retains ownership of L'auteur conserve la propriété du the copyright in his/her thesis. droit d'auteur qu¡ protège sa Neither the thesis nor substantial thèse. Ni la thèse ni des extraits extracts from it may be printed or substantiels de celle-ci ne otherwise reproduced without doivent être imprimés ou his/her permission. autrement reproduits sans son autorisation. ISBN 0-612-13090_8 C,anadä LIBERÄL PÄRÏY ORGAI{IZÂTIOII AI{D }'ANITOBA'S 1995 PROVINCIAL ELECTION BY ROBERT ANDREIJ DRI'I'IMOITD A Thesis submitted to the Faculty of Graduate Studies of the University of Manitoba in partial fulfiilment of the requirements of the degree of }TASIER OF ARTS @ 1996 Permission has been granted to the LIBRARY OF THE LTNIVERSITY OF MANITOBA to lend or sell copies of this thesis, to the NATIONAL LIBRARY OF CANADA to microfilm this thesis and to lend or sell copies of the film, and LIBRARY MICROFILMS to publish an abstract of this thesis. -

In Crisis Or Decline? Selecting Women to Lead Provincial Parties in Government

University of Calgary PRISM: University of Calgary's Digital Repository Arts Arts Research & Publications 2018-06 In Crisis or Decline? Selecting Women to Lead Provincial Parties in Government Thomas, Melanee Cambridge University Press Thomas, M. (2018). In Crisis or Decline? Selecting Women to Lead Provincial Parties in Government. Canadian Journal of Political Science/Revue canadienne de science politique, 51(2), 379-403. http://hdl.handle.net/1880/107552 journal article Unless otherwise indicated, this material is protected by copyright and has been made available with authorization from the copyright owner. You may use this material in any way that is permitted by the Copyright Act or through licensing that has been assigned to the document. For uses that are not allowable under copyright legislation or licensing, you are required to seek permission. Downloaded from PRISM: https://prism.ucalgary.ca In Crisis or Decline? Selecting Women to Lead Provincial Parties in Government By Melanee Thomas Associate Professor Department of Political Science University of Calgary 2500 University Drive NW Calgary, AB T2N 1N4 Abstract: The majority of Canada’s women premiers were selected to that office while their parties held government. This is uncommon, both in the comparative literature and amongst premiers who are men. What explains this gendered selection pattern to Canada’s provincial premiers’ offices? This paper explores the most common explanation found in the comparative literature for women’s emergence as leaders of electorally competitive parties and as chief political executives: women are more likely to be selected when that party is in crisis or decline. Using the population of women provincial premiers in Canada as case studies, evidence suggests 3 of 8 women premiers were selected to lead parties in government that were in crisis or decline; a fourth was selected to lead a small, left-leaning party as predicted by the literature. -

2019 Federal Election: Result and Analysis

2019 Federal Election: Result and Analysis O C T O B E R 22, 2 0 1 9 NATIONAL ELECTION RESULTS 157 121 24 3 32 (-20) (+26) (-15) (+1) (+22) Comparison between results reflected based on party standings at dissolution of the 42nd parliament • The Liberal Party of Canada (LPC) won a second mandate, although was diminished to minority status. • The result of the 43rd Canadian election is one of the closest in recent memory, with both the Liberals and Conservatives separated by little more than one percentage point. Conservatives share of vote is slightly higher than the Liberals, making major gains in key areas for the party • Bloc Quebecois (BQ) is a winner in this election, moving up to official party status which will give the party added resources as well as significance in the House of Commons • The NDP managed to win enough seats to potentially play an important role in the House of Commons, but the party took a big hit in Quebec — where they were only able to hold one of the Layton era “Orange Wave” seats • Maxime Bernier, who started the People’s Party of Canada after narrowly losing the Conservative leadership contest in 2017, lost the seat he has held onto since 2006 • The former Treasury Board president Dr. Jane Philpott, who ran as an independent following her departure from the liberal caucus, lost her seat in Markham Stouffville to former Liberal MPP and Ontario Minister of Health, Dr. Helena Jaczek. Jody Wilson-Raybould won as an independent in Vancouver Granville NATIONAL ELECTION RESULTS 10 2 32 3 39 24 PARTY STANDINGS AT -

THE AMERICAN IMPRINT on ALBERTA POLITICS Nelson Wiseman University of Toronto

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Great Plains Quarterly Great Plains Studies, Center for Winter 2011 THE AMERICAN IMPRINT ON ALBERTA POLITICS Nelson Wiseman University of Toronto Follow this and additional works at: http://digitalcommons.unl.edu/greatplainsquarterly Part of the American Studies Commons, Cultural History Commons, and the United States History Commons Wiseman, Nelson, "THE AMERICAN IMPRINT ON ALBERTA POLITICS" (2011). Great Plains Quarterly. 2657. http://digitalcommons.unl.edu/greatplainsquarterly/2657 This Article is brought to you for free and open access by the Great Plains Studies, Center for at DigitalCommons@University of Nebraska - Lincoln. It has been accepted for inclusion in Great Plains Quarterly by an authorized administrator of DigitalCommons@University of Nebraska - Lincoln. THE AMERICAN IMPRINT ON ALBERTA POLITICS NELSON WISEMAN Characteristics assigned to America's clas the liberal society in Tocqueville's Democracy sical liberal ideology-rugged individualism, in America: high status was accorded the self market capitalism, egalitarianism in the sense made man, laissez-faire defined the economic of equality of opportunity, and fierce hostility order, and a multiplicity of religious sects com toward centralized federalism and socialism peted in the market for salvation.l Secondary are particularly appropriate for fathoming sources hint at this thesis in their reading of Alberta's political culture. In this article, I the papers of organizations such as the United contend that Alberta's early American settlers Farmers of Alberta (UFA) and Alberta's were pivotal in shaping Alberta's political cul Social Credit Party.2 This article teases out its ture and that Albertans have demonstrated a hypothesis from such secondary sources and particular affinity for American political ideas covers new ground in linking the influence and movements. -

'Turncoats, Opportunists, and Political Whores': Floor Crossers in Ontario

“‘Turncoats, Opportunists, and Political Whores’: Floor Crossers in Ontario Political History” By Patrick DeRochie 2011-12 Intern Ontario Legislature Internship Programme (OLIP) 1303A Whitney Block Queen’s Park Toronto, Ontario M7A 1A2 Phone: 416-325-0040 [email protected] www.olipinterns.ca www.facebook.com/olipinterns www.twitter.com/olipinterns Paper presented at the 2012 Annual meeting of the Canadian Political Science Association Edmonton, Alberta Friday, June 15th, 2012. Draft: DO NOT CITE 2 Acknowledgements I would like to thank the following people for their support, advice and openness in helping me complete this research paper: Gilles Bisson Sean Conway Steve Gilchrist Henry Jacek Sylvia Jones Rosario Marchese Lynn Morrison Graham Murray David Ramsay Greg Sorbara Lise St-Denis David Warner Graham White 3 INTRODUCTION When the October 2011 Ontario general election saw Premier Dalton McGuinty’s Liberals win a “major minority”, there was speculation at Queen’s Park that a Member of Provincial Parliament (MPP) from the Progressive Conservative (PC) Party or New Democratic Party (NDP) would be induced to cross the floor. The Liberals had captured fifty-three of 107 seats; the PCs and NDP, thirty-seven and seventeen, respectively. A Member of one of the opposition parties defecting to join the Liberals would have definitively changed the balance of power in the Legislature. Even with the Speaker coming from the Liberals’ ranks, a floor crossing would give the Liberals a de facto majority and sufficient seats to drive forward their legislative agenda without having to rely on at least one of the opposition parties. A January article in the Toronto Star revealed that the Liberals had quietly made overtures to at least four PC and NDP MPPs since the October election, 1 meaning that a floor crossing was a very real possibility. -

Identity Politicking: New Candidacies and Representations in Contemporary Canadian Politics

Identity Politicking: New Candidacies and Representations in Contemporary Canadian Politics by Teresa-Elise Maiolino A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Department of Sociology University of Toronto © Copyright by Teresa-Elise Maiolino 2017 Identity Politicking: New Candidacies and Representations in Contemporary Canadian Politics Teresa-Elise Maiolino Doctor of Philosophy Department of Sociology University of Toronto 2017 Abstract This dissertation centres on the candidacies and leaderships of three politicians—Justin Trudeau, Olivia Chow, and Kathleen Wynne. It examines the ways in which gender, race, sexuality, and other salient aspects of politicians’ identities are strategically negotiated and mobilized by politicians, political actors, the media, and the grassroots. The cases herein question the extent to which identity matters in Canadian electoral politics at the municipal, provincial, and federal levels, bridging sociological understandings of power and authority with feminist analyses of identity. The project engages broadly with qualitative methods—discourse analysis, media analysis, participant observation, and interviewing. The research contributes to understandings of: (1) the durability of masculinity in Canadian electoral politics; (2) dispositional requirements for leaders; (3) the compensatory labour that minority politicians perform; (4) alignments and allegiances between politicians and grassroots movements. The first case of the dissertation examines media coverage of a charity-boxing match between Liberal Member of Parliament Justin Trudeau and Conservative Canadian Senator Patrick Brazeau. It offers the concept recuperative gender strategies to describe how political leaders work to restore their public gender identities. The second case is focused on the candidacy of visible minority Toronto mayoral candidate, Olivia Chow. -

The Rise and Decline of the Cooperative Commonwealth

THE RISE AND DECLINE OF THE COOPERATIVE COMMONWEALTH FEDERATION IN ONTARIO AND QUEBEC DURING WORLD WAR II, 1939 – 1945 By Charles A. Deshaies B. A. State University of New York at Potsdam, 1987 M. A. State University of New York at Empire State, 2005 A THESIS Submitted in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy (in History) The Graduate School The University of Maine December 2019 Advisory Committee: Scott W. See, Professor Emeritus of History, Co-advisor Jacques Ferland, Associate Professor of History, Co-advisor Nathan Godfried, Professor of History Stephen Miller, Professor of History Howard Cody, Professor Emeritus of Political Science Copyright 2019 Charles A. Deshaies All Rights Reserved ii THE RISE AND DECLINE OF THE COOPERATIVE COMMONWEALTH FEDERATION IN ONTARIO AND QUEBEC DURING WORLD WAR II, 1939 – 1945 By Charles A. Deshaies Dissertation Advisor: Dr. Scott See and Dr. Jacques Ferland An Abstract of the Thesis Presented In Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy (in History) December 2019 The Cooperative Commonwealth Federation (CCF) was one of the most influential political parties in Canadian history. Without doubt, from a social welfare perspective, the CCF helped build and develop an extensive social welfare system across Canada. It has been justly credited with being one of the major influences over Canadian social welfare policy during the critical years following the Great Depression. This was especially true of the period of the Second World War when the federal Liberal government of Mackenzie King adroitly borrowed CCF policy planks to remove the harsh edges of capitalism and put Canada on the path to a modern Welfare State. -

Um 1897, Testimony & Exhibits, 2/12/2018

BEFORE THE PUBLIC UTILITY COMMISSION OF OREGON UM 1897 In the Matter of ) ) HYDRO ONE LIMITED, ) ) Application for Authorization to Exercise ) Substantial Influence over Policies and ) Actions of AVISTA CORPORATION. ) ) REPLY TESTIMONY OF THE OREGON CITIZENS’ UTILITY BOARD February 12th, 2018 Table of Contents Introduction ....................................................................................................................................2 Background of Hydro One ...........................................................................................................4 Risks ..............................................................................................................................................7 Political Risk ................................................................................................................................7 North American Free Trade Agreement Risk ............................................................................14 Post-Transaction Corporate Structure ........................................................................................17 Double Leverage Holding Company ..........................................................................................19 Why Avista .................................................................................................................................24 Benefits ..........................................................................................................................................27 Exhibits -

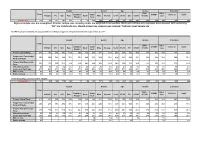

Regional Sample Sizes Are Unweighted. All Other Sample Sizes, Including Totals, Are Weighted to Census Data

Region Gender Age Income Education $50K- HS or Total Hamilton/ South $100K+ Coll/Tech Univ+ 416/905 416 905 East North Male Female 18-34 35-54 55+ <$50K <$100K less Niagara west Sample Size 807 341 157 184 152 74 50 190 392 415 233 307 267 231 261 162 332 242 233 Regional sample sizes are unweighted. All other sample sizes, including totals, are weighted to census data. Blank cells indicate zero responses were received. Cells containing "0%" are statistically zero, though at least one response was received. *Indicates small sample size Q1. Which party's candidate are you yourself most likely to support in the provincial election expected on June 7? Region Gender Age Income Education Total $50K- HS or Hamilton/ South $100K+ Coll/Tech Univ+ 416/905 416 905 East North Male Female 18-34 35-54 55+ <$50K <$100K less Niagara west Ontario Liberal Party 17% 18% 21% 15% 19% 15% 12% 15% 17% 16% 23% 13% 15% 18% 17% 18% 13% 17% 22% Progressive Conservative 35% 35% 30% 39% 39% 35% 29% 33% 38% 31% 21% 38% 43% 33% 36% 39% 38% 34% 31% Party of Ontario Ontario New Democratic 15% 13% 13% 13% 9% 16% 24% 18% 18% 11% 18% 15% 11% 16% 16% 13% 11% 17% 16% Party Other/Independent 2% 1% 1% 1% 2% 4% 2% 2% 2% 2% 2% 2% 2% 3% 1% 1% 1% 3% 2% Undecided /Can't Say 27% 28% 27% 30% 26% 27% 20% 25% 21% 32% 29% 27% 24% 22% 26% 26% 29% 24% 27% Will not vote 4% 4% 6% 2% 4% 2% 6% 4% 3% 4% 5% 4% 2% 6% 3% 3% 5% 4% 1% Rather not say 2% 2% 2% 1% 2% 1% 6% 1% 1% 3% 2% 1% 2% 2% 1% 3% 1% 1% Q1/Q2 [Including Leaners] Likely to support Sample Size 762 323 145 178 145 71 45 182 377 385 -

The Waffle, the New Democratic Party, and Canada's New Left During the Long Sixties

Western University Scholarship@Western Electronic Thesis and Dissertation Repository 8-13-2019 1:00 PM 'To Waffleo t the Left:' The Waffle, the New Democratic Party, and Canada's New Left during the Long Sixties David G. Blocker The University of Western Ontario Supervisor Fleming, Keith The University of Western Ontario Graduate Program in History A thesis submitted in partial fulfillment of the equirr ements for the degree in Doctor of Philosophy © David G. Blocker 2019 Follow this and additional works at: https://ir.lib.uwo.ca/etd Part of the Canadian History Commons Recommended Citation Blocker, David G., "'To Waffleo t the Left:' The Waffle, the New Democratic Party, and Canada's New Left during the Long Sixties" (2019). Electronic Thesis and Dissertation Repository. 6554. https://ir.lib.uwo.ca/etd/6554 This Dissertation/Thesis is brought to you for free and open access by Scholarship@Western. It has been accepted for inclusion in Electronic Thesis and Dissertation Repository by an authorized administrator of Scholarship@Western. For more information, please contact [email protected]. i Abstract The Sixties were time of conflict and change in Canada and beyond. Radical social movements and countercultures challenged the conservatism of the preceding decade, rejected traditional forms of politics, and demanded an alternative based on the principles of social justice, individual freedom and an end to oppression on all fronts. Yet in Canada a unique political movement emerged which embraced these principles but proposed that New Left social movements – the student and anti-war movements, the women’s liberation movement and Canadian nationalists – could bring about radical political change not only through street protests and sit-ins, but also through participation in electoral politics.