Spring 2011 Advanced Portfolio Management Solutions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Assessing Securities Lending Risk-Return Performance in a Portfolio Context

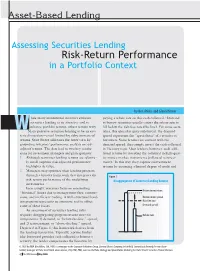

Asset-Based Lending Assessing Securities Lending Risk-Return Performance in a Portfolio Context by Ben Atkins and Glenn Horner hile many institutional investors embrace paying a rebate rate on this cash collateral.1 Demand securities lending as an attractive tool to to borrow securities usually causes the rebate rate to enhance portfolio returns, others remain wary. fall below the risk-free rate (the line). For some secu- WMany perceive securities lending to be an eso- rities, this spread is quite substantial; the demand teric distraction—a tool limited by risky, immaterial spread represents the “specialness” of a security to returns. State Street addresses the latter view by borrowers. Some lenders are content with the grounding investors’ performance analysis on risk- demand spread; they simply invest the cash collateral adjusted returns. The data lead to two key conclu- in Treasury repo. Most lenders, however, seek addi- sions for investment managers and plan sponsors: tional returns by investing the collateral in high-qual- 1. Although securities lending returns are relative- ity money market instruments (collateral reinvest- ly small, superior risk-adjusted performance ment).2 In this way, they capture reinvestment highlights its value. returns by assuming a limited degree of credit and 2. Managers may optimize their lending program through a broader framework that integrates the Figure 1 risk-return performance of the underlying Disaggregation of Securities Lending Returns investments. Increasingly, investors focus on minimizing Reinvestment return “frictional” losses due to management fees, commis- sions, and inefficient trading. A well-structured lend- Reinvestment spread ing program represents an attractive tool to offset Risk-free rate some of these losses. -

Understanding and Managing Risk in Public Investing

CDIAC/CMTA Advanced Public Funds Investing Workshop Session Three: Understanding and Managing Risk in Public Investing Presented by: Sarah Meacham, Managing Director January 15, 2020 PFM Asset 601 S. Figueroa Street, Suite 4500 Management LLC Los Angeles, CA 90017 www.pfm.com 213.489.4075 © PFM 1 TYPES OF FIXED INCOME INVESTMENT RISK Inflation Interest rate Topics Liquidity Reinvestment Credit HOW TO MANAGE AND MITIGATE RISK Investment policy development Diversification Discipline to long-term strategy Performance measurement © PFM 2 “Risk is inherent throughout the investment process. There is investment risk associated with any investment activity and opportunity risk related to inactivity.” ~Local Agency Investment Guidelines, CDIAC January 1, 2019 © PFM 3 Types of Fixed Income Investment Risk © PFM 4 Types of Fixed Income Investment Risk Inflation Risk Liquidity Risk Credit Risk Loss of purchasing Inability to sell portfolio Risk of default or power over time as a holdings at a competitive decline in security value result of inflation price due to issuer’s financial strength Reinvestment Risk Interest Rate Risk The risk that a security’s Variability of return/price cash flow will be related to changes in reinvested at a lower interest rates rate of return © PFM 5 Inflation Risk © PFM 6 Inflation (Purchasing Power) Risk Loss of purchasing power over time as a result of inflation Real interest rate is after inflation; nominal is before inflation • Real = nominal – inflation • Nominal = real + inflation • Inflation = nominal -

Property/Liability Insurance Risk Management and Securitization

PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Biography Trent R. Vaughn, FCAS, MAAA, is Vice President of Actuarial/Pricing at GRE Insurance Group in Keene, NH. Mr. Vaughn is a 1990 graduate of Central College in Pella, Iowa. He is also the author of a recent Proceedings paper and has been a member of the CAS Examination Committee since 1996. Acknowledgments The author would like to thank an anonymous reviewer from the CAS Continuing Education Committee for his or her helpful comments. PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Abstract This paper presents a comprehensive framework for property/liability insurance risk management and securitization. Section 2 presents a rationale for P/L insurance risk management. Sections 3 through 6 describe and evaluate the four categories of P/L insurance risk management techniques: (1) maintaining internal capital within the organization, (2) managing asset risk, (3) managing underwriting risk, and (4) managing the covariance between asset and liability returns. Securitization is specifically discussed as a potential method of managing underwriting risk. Lastly, Section 7 outlines four key guidelines for cost- effective risk management. 1. INTRODUCTION In recent years, the property-liability insurance industry has witnessed intense competition from alternative risk management techniques, such as large deductibles and retentions, risk retention groups, and captive insurance companies. Moreover, the next decade promises to bring additional competition from new players in the P/L insurance industry, including commercial banks and securities firms. In order to survive in this competitive new landscape, P/L insurers must manage total risk in a cost-efficient manner. This paper provides a rationale for P/L insurance risk management, then describes four categories of risk management techniques utilized by insurers. -

Diversification and Discussion of Risk

Diversification and Discussion of Risk Conference of the County Investment Academy San Antonio June 2019 PFIA 2256.008c Requires Training in: • Investment Diversification 2 Capital Market Theory 12.0% 10.0% 8.0% E( r) 6.0% P* * 4.0% 2.0% 0.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% Std. Dev. 3 Capital Market Theory • Points along the upper half of the curve represent the best risk/return diversified portfolios of risky assets • The straight line represents portfolios obtained by investing in the “optimal risky portfolio” (P*) and either lending or leveraging at the “risk‐free” rate. • Points on the line below the curve represent “lending” and points above represent “leveraging” (note increased “risk” as measured by standard deviation of returns!) 4 So in theory….. Key result? An undiversified portfolio yields inferior return for the level of risk! The same, or higher, return could be attained at a lower level of risk with a diversified portfolio. If you are not diversified, you are taking more risk than you can expect to be compensated for! 5 Diversification and Correlation of Returns Correlation, which measures the degree of “co‐ movement”, ranges from ‐1 to +1. When the correlation between returns is less than 1 there are diversification benefits—the risk of portfolio is less than the average of the risks of the individual assets. Which pair of stock returns is more correlated? Chevron, Exxon Chevron, Delta Airlines 6 International Diversification Correlations vs S&P 500: China 0.62 Korea 0.53 Japan 0.73 Germany 0.74 UK 0.73 Brazil 0.29 Chile 0.38 Monthly returns vs corresponding MSCI indexes (US dollar returns) 5 years ended April 2019 Source: FactSet 7 Global Market Capitalization Latin Canada 1% UK 3% Other 5% 1% Japan 8% Asia ex Japan 13% U.S. -

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk, and Incentive Issues Frank M. Keane Securities loans collateralized by cash are by far the most popular form of securities-lending transaction. But when the www.newyorkfed.org/research/current_issues F cash collateral associated with these transactions is actively reinvested by a lender’s agent, potential risks emerge. This 2013 F study argues that the standard compensation scheme for securities-lending agents, which typically provides for agents to share in gains but not losses, creates incentives for them to take excessive risk. It also highlights the need for greater scrutiny and understanding of cash reinvestment practices— especially in light of the AIG experience, which showed that Volume 19, Number 3 Volume risks related to cash reinvestment, by even a single participant, could have destabilizing effects. lthough less researched than the money markets, the collateral markets IN ECONOMICS AND FINANCE are critical to the efficiency of the asset markets—including the markets for ATreasury, agency, and agency mortgage-backed securities. Well-functioning collateral markets allow dealers and investors in the asset markets to finance short positions for the purposes of hedging, market making, settlement, and arbitrage. Two important mechanisms for accessing the U.S. money and collateral markets are repurchase agreements (repos) and securities-lending transactions. In a money market transaction, when cash and securities are exchanged, the securities act as collateral and mitigate the risks associated with a borrower’s failure to repay the cash. In a collateral market transaction, however, the cash serves as collateral and mitigates the risk associated with replacing the security if the borrower fails to return it. -

Interest Rate Risk • Interest Rate Risk Is the Risk Market Rates Will Change. O

MANAGING BOND PORTFOLIOS Interest Rate Risk Interest rate risk is the risk market rates will change. o Price risk—bond prices (values) move opposite interest rates; there exists an inverse relationship such that prices decrease when market rates increase, and vice versa. o Reinvestment risk—interest rate changes are positively related to the ability to reinvest at favorable rates; that is, when market rates increase, the coupon interest that is paid by a bond can be reinvested at higher rates, and vice versa. Interest rate sensitivity—the characteristics of bonds indicate how sensitive bond prices are to changes in interest rates. o Bond prices move opposite changes in interest rates (inversely related). When market yields increase, bond price decrease, and vice versa. A price decrease that results from an increase in the market rate will be less than a price increase that results from an equivalent decrease in the market rate. o Everything else equal, bond prices are more sensitive for bonds with: . Longer terms to maturity than bonds with shorter terms to maturity. The sensitivity of longer-term bonds increases at a decreasing rate, which means that a bond with 20 years to maturity is not twice as sensitive to changes in market rates than a bond with 10 years to maturity; e.g., the price of a 10-year bond might decrease by 6 percent when market rates increase, whereas the price of the 20- year bond would decrease by 9 percent for the same change in market rates. Bonds with lower coupon rates than bonds with higher coupon rates. -

Blackrock Securities Lending

BlackRock Securities Lending Unlocking the potential of portfolios January 2021 | Securities Lending Introduction: In summary: Securities lending is a well-established practice whereby • While not without risk, securities lending seeks to U.S. registered funds, such as mutual funds, make loans benefit the fund. of securities to seek an incremental increase in returns for • BlackRock has focused on delivering competitive fund shareholders. returns while balancing return, risk and cost in its three This paper explains the basics of securities lending, decades of lending securities on behalf of outlines the benefits and risks for investors, and describes shareholders. BlackRock’s leading approach to securities lending. • Since 1981, BlackRock has delivered positive monthly lending income for every fund that has participated in Basics of Securities Lending securities lending, including mutual funds. In securities lending transactions, mutual funds lend stocks or bonds to generate additional returns for Benefits of Securities Lending the funds. Mutual fund investors can benefit from securities lending Here’s how it works: first, a large financial institution asks in the form of fund performance. How? The mutual fund to borrow a stock or bond from a mutual fund. In order to seeks to generate additional income through the rate that borrow the stock or bond, the financial institution will it charges for lending securities (if applicable), and/or income on the reinvestment of the collateral that the negotiate financial terms with the lending agent of the borrower provides in exchange for the loan. mutual fund and provide collateral. The mutual fund keeps the collateral to secure repayment in case the Securities lending returns typically vary by asset class and borrower fails to return the loaned stock or bond. -

Asset Securitisation

Superseded document Basel Committee on Banking Supervision Consultative Document Asset Securitisation Supporting Document to the New Basel Capital Accord Issued for comment by 31 May 2001 January 2001 Superseded document Superseded document Table of Contents OVERVIEW .............................................................................................................................................1 I. THE TREATMENT OF EXPLICIT RISKS ASSOCIATED WITH TRADITIONAL SECURITISATION........................................................................................................................1 A. THE STANDARDISED APPROACH .............................................................................................2 1. The treatment for originating banks..........................................................................2 (a) Minimum operational requirements for achieving a clean break.................................3 (b) Minimum capital requirements for credit enhancements ............................................3 (c) Minimum operational requirements for revolving securitisations with early amortisation features .............................................................................................................4 2. The treatment for investing banks ............................................................................6 (a) Minimum capital requirements for investments in ABS...............................................6 (b) Treatment of unrated securitisations ..........................................................................7 -

Chapter 4 Interest Rate Measurement and Behavior Chapter 5 the Risk and Term Structure of Interest Rates

Chapter 4 Interest Rate Measurement and Behavior Chapter 5 The Risk and Term Structure of Interest Rates LEVEL OF INTEREST RATES Fisher Effect (risk-free rate) Interest rate has 2 components: (1) real rate (2) inflation premium I = r+ IP STRUCTURE OF INTEREST RATES http://www.ratecurve.com/yc2.html Term Structure of Interest Rates - defines the relationship between maturity & annualized yield, holding other factors such as risk, taxes, etc., constant. Graphic presentation is the yield curve. Curve shifts and twists through time. Four Basic Shapes: Positive Yield Curve: upward sloping Negative Yield Curve: downward sloping Flat Yield Curve Humped Yield Curve Level of Interest Rates: Loanable Funds Theory -- market interest rate is determined by the factors that control the supply of and demand for loanable funds. Demand Factors Household: Y increases then installment debt increases R increases then installment debt falls Business: n CFt NPV = - I + å (1+i )t T =1 if i decrease _ NPV (?) Government: interest inelastic 1980: debt/GNP =25% 1987: debt/GNP=42% Foreign Foreign interest rates vs. U.S. rates Supply Households - largest suppliers Very steep slope for supply. Why? What happens if expect higher inflation? Savers - Liquidity Preference Theory - Market rate of interest is determined by demand/supply of money balances. Demand of Money + Transaction f(y) + Precautionary f(y) - Speculative f(r) Supply of Money Fed basically determines supply Few uncontrollable factors (1) banks lending (2) public's preference for cash Letting D=S then solve for interest rate: + + - _ r = f ( , , ) y m p e THEORIES ON SHAPE OF YIELD CURVE Unbiased Expectations - shape of yield curve is determined solely by current & expected future short-term interest rates. -

Reviewing Systemic Risk Within the Insurance Industry

Reviewing Systemic Risk within the Insurance Industry February 2017 2 Reviewing Systemic Risk within the Insurance Industry SPONSOR Society of Actuaries AUTHOR Max J. Rudolph, FSA, CERA, CFA, MAAA Caveat and Disclaimer The opinions expressed and conclusions reached by the authors are their own and do not represent any official position or opinion of the Society of Actuaries or its members. The Society of Actuaries makes no representation or warranty to the accuracy of the information. Copyright ©2017 All rights reserved by the Society of Actuaries © 2017 Society of Actuaries 3 TABLE OF CONTENTS Executive Summary .................................................................................................................................................. 4 Systemic Risk ............................................................................................................................................................ 5 Systemic Risk Definition ............................................................................................................................................. 5 Definition Nuances ..................................................................................................................................................... 7 What are the Drivers of Systemic Risk? ................................................................................................................... 10 Size .............................................................................................................................................................. -

Interest Rate Risk # Reinvestment Risk: the Returns on Funds to Be Reinvested Will Fall Below the Cost of Funds

Interest Rate Risk # Reinvestment risk: the returns on funds to be reinvested will fall below the cost of funds. # Refinancing risk: the costs of rolling over funds or reborrowing funds will rise above the returns generated on investments. # Int rate risk is the risk incurred by an FI if it mismatches the maturities of it’s A & L. # Market value risk: Interest rate increase, the market value of assets and liabilities decrease Credit risk is é possibility that promised cash flows may not occur or may only partially occur. 2 types of credit risk: 1. Systematic credit risk affects all borrowers. 2. Firm-specific credit risk affects a particular company. NB:Firm-specific credit risk can be managed through diversification. (b) Which types of FIs are more susceptible to this type of risk? Why? Answer: FIs that lend money for long periods of time, whether as loans or by buying bonds, are more susceptible to this risk than those FIs that have short investment horizons. ‐ Maturity Model •MA–ML > 0: the FI is exposed to increasing interest rates. R asset decrease more •MA– ML < 0: the FI is exposed to decreasing interest rates. R liability decrease more •MA– ML = 0: the FI is ‘immunised’. For most FIs: MA– ML > 0. Maturity matching does not always eliminate interest rate risk exposure, because: a. The duration of A & L might be different, b. The maturity model does not consider the leverage of the FI ‐ Duration Model Duration and maturity: dD/dM>0 Duration and yield: dD/dR< 0 Duration and coupon interest rate: dD/dC< 0 Foreign Exchange Risk Foreign exchange risk: The risk that changes in exchange rates can affect the value of an FI’s Asset and/or Liabilities located abroad. -

Investment Risk: What Risks Are You Willing to Take? Compound Value Advisers by Jerry Matecun

Investment Risk: What Risks Are You Willing to Take? Compound Value Advisers by Jerry Matecun Stocks For the Long-Term….What About Your Term? The first reaction to the chart below is – a no-brainer – stocks compound at a much higher rate than bonds and inflation; therefore, put your money in stocks for the long-term! Yet we know that in the last 15 years we have seen two investment booms that went bust in a very short time period. Stocks declined over 50% in 18 months; there have been several longer term stock declines throughout history. Statistical certainty of future returns does not exist, and this presents a challenge to managing portfolio risk. Time horizon is a key element to consider. A younger person with a long time horizon can better handle this type of market risk. However, as you near retirement age, this kind of decline can cause very real anxiety. Understanding the relationship between the various risk and rates of return inherent in every asset class is fundamental to constructing an investment plan that can help you sleep at night. Ibbotson® SBBI® Stocks, Bonds, Bills, and Inflation 1926–2012 $18,365 $10,000 $3,533 Compound annual return 1,000 • Small stocks 11.9 % • Large stocks 9.8 • Government bonds 5.7 • Treasury bills 3.5 • Inflation 3.0 $123 100 $21 $13 10 1 0.10 1926 1936 1946 1956 1966 1976 1986 1996 2006 Past performance is no guarantee of future results. Hypothetical value of $1 invested at the beginning of 1926. Assumes reinvestment of income and no transaction costs or taxes.