Reviewing Systemic Risk Within the Insurance Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ISSA 6314 – Strategic Thought and Leadership

Course Syllabus and Policy Requirement Statement In order to access your course materials, you must agree to the following, by clicking the "Mark Reviewed" button at the bottom of this document. By checking the "Mark Reviewed" link below, you are indicating the following: • You have read, understood, and will comply with the policies and procedures listed in the class syllabus, and that you have acquired the required textbook(s). • You have read, understood, and will comply with class policies and procedures as specified in the online Student Handbook. • You have read, understood, and will comply with computer and software requirements as specified with Browser Test. • You have familiarize yourself with how to access course content in Blackboard using the Student Quick Reference Guide or CSS Student Orientation Course. ISSA 6314 – Strategic Thought and Leadership Course Description/Overview This course offers students an opportunity to explore how strategic leaders at the executive level of organizations think and influence actions. Students study leadership, ethics, decision-making, and strategy. The course emphasizes the relationship between intelligence and strategic decisions. Historical case studies highlight commonalities and habits of mind that form the nexus between strategic thought and leadership. Students will appreciate that a major aspect of thinking strategically and influencing others toward effective outcomes is well-analyzed intelligence appropriately tailored for the needs of policy makers. Strategic thought and leadership literature was once the purview of government policy makers and the military. As such, much material exists on grand strategy, operational strategy, and battlefield strategy or tactics. The same paradigm exists for decision-making, intelligence, and leading men and women. -

In Their Own Words: Voices of Jihad

THE ARTS This PDF document was made available from www.rand.org as CHILD POLICY a public service of the RAND Corporation. CIVIL JUSTICE EDUCATION Jump down to document ENERGY AND ENVIRONMENT 6 HEALTH AND HEALTH CARE INTERNATIONAL AFFAIRS The RAND Corporation is a nonprofit research NATIONAL SECURITY POPULATION AND AGING organization providing objective analysis and PUBLIC SAFETY effective solutions that address the challenges facing SCIENCE AND TECHNOLOGY the public and private sectors around the world. SUBSTANCE ABUSE TERRORISM AND HOMELAND SECURITY Support RAND TRANSPORTATION AND INFRASTRUCTURE Purchase this document WORKFORCE AND WORKPLACE Browse Books & Publications Make a charitable contribution For More Information Visit RAND at www.rand.org Learn more about the RAND Corporation View document details Limited Electronic Distribution Rights This document and trademark(s) contained herein are protected by law as indicated in a notice appearing later in this work. This electronic representation of RAND intellectual property is provided for non-commercial use only. Unauthorized posting of RAND PDFs to a non-RAND Web site is prohibited. RAND PDFs are protected under copyright law. Permission is required from RAND to reproduce, or reuse in another form, any of our research documents for commercial use. For information on reprint and linking permissions, please see RAND Permissions. This product is part of the RAND Corporation monograph series. RAND monographs present major research findings that address the challenges facing the public and private sectors. All RAND monographs undergo rigorous peer review to ensure high standards for research quality and objectivity. in their own words Voices of Jihad compilation and commentary David Aaron Approved for public release; distribution unlimited C O R P O R A T I O N This book results from the RAND Corporation's continuing program of self-initiated research. -

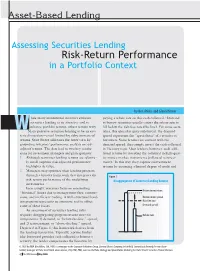

Assessing Securities Lending Risk-Return Performance in a Portfolio Context

Asset-Based Lending Assessing Securities Lending Risk-Return Performance in a Portfolio Context by Ben Atkins and Glenn Horner hile many institutional investors embrace paying a rebate rate on this cash collateral.1 Demand securities lending as an attractive tool to to borrow securities usually causes the rebate rate to enhance portfolio returns, others remain wary. fall below the risk-free rate (the line). For some secu- WMany perceive securities lending to be an eso- rities, this spread is quite substantial; the demand teric distraction—a tool limited by risky, immaterial spread represents the “specialness” of a security to returns. State Street addresses the latter view by borrowers. Some lenders are content with the grounding investors’ performance analysis on risk- demand spread; they simply invest the cash collateral adjusted returns. The data lead to two key conclu- in Treasury repo. Most lenders, however, seek addi- sions for investment managers and plan sponsors: tional returns by investing the collateral in high-qual- 1. Although securities lending returns are relative- ity money market instruments (collateral reinvest- ly small, superior risk-adjusted performance ment).2 In this way, they capture reinvestment highlights its value. returns by assuming a limited degree of credit and 2. Managers may optimize their lending program through a broader framework that integrates the Figure 1 risk-return performance of the underlying Disaggregation of Securities Lending Returns investments. Increasingly, investors focus on minimizing Reinvestment return “frictional” losses due to management fees, commis- sions, and inefficient trading. A well-structured lend- Reinvestment spread ing program represents an attractive tool to offset Risk-free rate some of these losses. -

Concentration Indicators: Assessing the Gap Between Aggregatre and Detailed Data

Concentration indicators: Assessing the gap between aggregate and detailed data Fernando Ávila1, Emilio Flores1, Fabrizio López-Gallo1,2, and Javier Márquez3 Abstract Risk analysis depends to a large extent on the type of data. Aggregate data can serve as a useful surrogate for individual data. However, in practice, there is uncertainty on the reliability and adequacy of aggregated data. In this paper we estimate the Herfindahl-Hirschman Index (HHI) for a loan portfolio using both aggregate data and individual data. Then, we compare both estimates to assess the reliability of the aggregated data. Concentration is a key driver of a portfolio credit risk and the HHI is a reliable standard for measuring concentration risk. Results for the Mexican banking system suggest that the estimated HHI based on aggregate data is a fairly good proxy for the actual concentration. This result suggests that aggregate data are useful to evaluate the underlying risk of the portfolio for regulatory purposes. Keywords: Credit risk, Concentration risk, HHI index Data adequacy. JEL Classification: C13, C18, G21, G32. Introduction Banks and other financial intermediaries tend to specialize in market segments where they exercise a competitive advantage. Whereas specialization facilitates banks to benefit from market conditions or their expertise, specialization may be accompanied by concentration of resources in counterparties, regions, industry sectors, or business products, compromising banks’ diversification of their sources of business or income. This lack of diversification increases a bank’s exposure to losses arising from the concentrated portfolio. Therefore, Concentration could work as a magnifying mechanism of financial shocks which may lead an institution to insolvency In fact, the Basel Committee on Banking Supervision (2006) affirms that “concentration is arguably the most important cause of large losses on banks’ portfolios”. -

North American Income Choice 10 Fixed Indexed Annuity

® NAC IncomeChoice 10 fixed index annuity The income you need, the potential you want 25432Z | REV 1-20 Go for a retirement paycheck big enough for your life For all the tough choices you’ve had to make in life, a few keep coming back around again. Life still costs money, and it seems the more adventures you pursue, the more expensive life gets. What if you didn’t have to sacrifice your adventures in retirement? What if you could meet your basic needs and get the growth potential you want to pursue your dreams? Look to the NAC IncomeChoice® 10 from North American 2 25432Z | REV 1-20 Know the lingo What sets NAC Key terms to help you understand how your annuity works IncomeChoice An annuity represents a simple promise. It’s an insurance contract. For your money and the time apart? you leave it with us, we promise to offer both growth potential and downside protection from market drops. This deferred, flexible-premium, fixed In explaining the fine details, though, you might see some terms that are new to you. Look for boxes index annuity is designed to provide you like this if you run into a word you’d like to better guaranteed lifetime income with growth understand. potential from index accounts linked to the stock market. Premium You can get started for a minimum of $20,000. Better The amount paid to the insurance company to fund rates are available for premium levels of $250,000 or an annuity. more. And because NAC IncomeChoice can grow $20,000 minimum (qualified and non-qualified) in multiple ways, we’re able to offer our highest potential income, helping you on your way to whatever Accumulation value adventures retirement has in store. -

Icommandant November 2009.Pdf

iCommandant: November 2009 Contact Us Site Map FAQs Phone Book ● Home ● Careers ● Units ● Missions ● Doing Business ● About Us RSS ● Leaders iCommandant ● Commandant's Corner Web Journal of Admiral Thad Allen ● All Hands Messages ● Biography Showing newest 30 of 38 posts from November 2009. Show older posts ● Official Photo Sunday, November 29, 2009 ● iCommandant Weekend Wrap Up ... We have a lot of customers! ● Podcasts Guardians, We returned to Washington this afternoon after a busy week in Europe. We participated in the 26th General Assembly of the International Maritime Organization and visited a number of United States, NATO, European Union, and coalition partners. There are several themes that emerge from the world of work that our Guardians perform this week and every week beyond our maritime borders. 1. The world is becoming more complex and the trend will continue. 2. The issues we face challenge existing governing structures that were created in different times to address different threats. 3. Asymmetrical threats such as piracy, illegal fishing, and illegal immigration are proliferating and challenge our governing structures and operational response models. 4. The value, relevance, and return of investment of Coast Guard resources has never been more appreciated. 4. Allocating our forces outside the western hemisphere has always been a challenge but the demand is likely to outstrip our capability for the foreseeable future. 5. These realities will require us to make tough choices in the near future as we reconcile supply and demand for our limited resources. I am more well informed and sensitive to the complex issues at play having made these visits. -

What Amounts to a Surrender by Operation of Law?

September 2010 Review Property @ction Welcome to the Fifth Edition of the Quarterly Review from Hammonds’ Property@ction Team. In this issue we will look at the following: (i) What amounts to a surrender by operation of law; (ii) Does it do what it says on the tin? - full repairing and insuring leases; (iii) Double trouble; (iv) Compulsory purchase orders; (v) Adverse possession; We welcome all contributions to this review and if you would like to discuss this further please contact any of the editorial team. What amounts to a surrender by operation of law? Where a landlord and tenant bring a lease to an end, they usually do so by completing a deed of surrender. However, sometimes, it may be implied that a surrender has occurred. The term commonly used for an implied surrender is a surrender “by operation of law”. In a recent case, QFS Scaffolding v Sable1 , the court considered some of the relevant principles for a surrender by operation of law to take place. Facts The landlord (Mr and Mrs Sable) granted a lease to a tenant company which eventually entered into administration. Prior to the administration, a new company (QFS) was formed with a view to taking over the tenant’s business. The Sables negotiated terms for a new lease with QFS who, in fact, went into occupation. However, the negotiations faltered and no new lease was entered into. Instead, QFS asked the administrator of the tenant to assign the lease to it and, as a result of this request, a deed of assignment was executed. -

UNOFFICIAL TRANSLATION Law No. 25/2008 of 5 June Establishing The

UNOFFICIAL TRANSLATION Law No. 25/2008 of 5 June Establishing the preventive and repressive measures for the combat against the laundering of benefits of illicit origin and terrorism financing, transposing into the domestic legal system Directive 2005/60/EC of the European Parliament and Council, of 26 October 2005, and Directive 2006/70/EC, of the Commission, of 01 August 2006, relating to the prevention of the use of the financial system and of the specially designated activities and professions for purposes of money laundering and terrorism financing, first amendment to Law No. 52/2003 of 22 August, and revoking Law No. 11/2004, of 27 March The Assembly of the Republic decrees, pursuant to Article 161 c) of the Constitution, the following: CHAPTER I General provisions SECTION I Subject matter and definitions Article 1 Subject matter 1- This Law establishes preventive and repressive measures to combat the laundering of unlawful proceeds and terrorism financing and transposes into Portuguese law Directive 2005/60/EC of the European Parliament and of the Council of 26th October 2005 and Commission Directive 2006/70/EC of 1st August 2006 on the prevention of the use of the financial system and designated non-financial businesses and professions for the purpose of money laundering and terrorism financing. 2- Money laundering and terrorism financing are prohibited and punishable in accordance with the procedures established by the applicable criminal law. Article 2 Definitions For the purposes of this Law the following shall mean: 1) «Entities -

Risk Management Lessons from the Global Banking Crisis of 2008 October 21, 2009 RISK MANAGEMENT LESSONS from the GLOBAL BANKING CRISIS of 2008

Senior Supervisors Group Risk Management Lessons from the Global Banking Crisis of 2008 October 21, 2009 RISK MANAGEMENT LESSONS FROM THE GLOBAL BANKING CRISIS OF 2008 CANADA SENIOR SUPERVISORS GROUP Office of the Superintendent of Financial Institutions FRANCE Banking Commission October 21, 2009 Mr. Mario Draghi, Chairman Financial Stability Board GERMANY Bank for International Settlements Federal Financial Centralbahnplatz 2 Supervisory Authority CH-4002 Basel Switzerland JAPAN Financial Services Agency Dear Mr. Draghi: On behalf of the Senior Supervisors Group (SSG), I am writing to convey Risk SWITZERLAND Management Lessons from the Global Banking Crisis of 2008, a report that reviews in depth Financial Market the funding and liquidity issues central to the recent crisis and explores critical areas of Supervisory Authority risk management practice warranting improvement across the financial services industry. This report is a companion and successor to our first report, Observations on Risk Management Practices during the Recent Market Turbulence, issued in March 2008. UNITED KINGDOM Financial Services Authority The events of 2008 clearly exposed the vulnerabilities of financial firms whose business models depended too heavily on uninterrupted access to secured financing markets, often at excessively high leverage levels. This dependence reflected an unrealistic assessment of UNITED STATES liquidity risks of concentrated positions and an inability to anticipate a dramatic reduction Board of Governors in the availability of secured funding to support these assets under stressed conditions. of the Federal Reserve System A major failure that contributed to the development of these business models was weakness in funds transfer pricing practices for assets that were illiquid or significantly concentrated Federal Reserve Bank when the firm took on the exposure. -

Understanding and Managing Risk in Public Investing

CDIAC/CMTA Advanced Public Funds Investing Workshop Session Three: Understanding and Managing Risk in Public Investing Presented by: Sarah Meacham, Managing Director January 15, 2020 PFM Asset 601 S. Figueroa Street, Suite 4500 Management LLC Los Angeles, CA 90017 www.pfm.com 213.489.4075 © PFM 1 TYPES OF FIXED INCOME INVESTMENT RISK Inflation Interest rate Topics Liquidity Reinvestment Credit HOW TO MANAGE AND MITIGATE RISK Investment policy development Diversification Discipline to long-term strategy Performance measurement © PFM 2 “Risk is inherent throughout the investment process. There is investment risk associated with any investment activity and opportunity risk related to inactivity.” ~Local Agency Investment Guidelines, CDIAC January 1, 2019 © PFM 3 Types of Fixed Income Investment Risk © PFM 4 Types of Fixed Income Investment Risk Inflation Risk Liquidity Risk Credit Risk Loss of purchasing Inability to sell portfolio Risk of default or power over time as a holdings at a competitive decline in security value result of inflation price due to issuer’s financial strength Reinvestment Risk Interest Rate Risk The risk that a security’s Variability of return/price cash flow will be related to changes in reinvested at a lower interest rates rate of return © PFM 5 Inflation Risk © PFM 6 Inflation (Purchasing Power) Risk Loss of purchasing power over time as a result of inflation Real interest rate is after inflation; nominal is before inflation • Real = nominal – inflation • Nominal = real + inflation • Inflation = nominal -

MSME) During COVID 19 Outbreak in South Sulawesi Province Indonesia

May – June 2020 ISSN: 0193-4120 Page No. 26707 - 26721 Factors Influencing Resilience of Micro Small and Medium Entrepreneur (MSME) during COVID 19 Outbreak in South Sulawesi Province Indonesia Muhammad Hidayat¹, Fitriani Latief², DaraAyu Nianty³ ShandraBahasoan⁴AndiWidiawati⁵ ¹²³⁴⁵STIE Nobel Indonesia Article Info Abstract: Volume 83 Aim: To find out factors influencing resilience of Micro Small and Medium Page Number: 26707 – 26721 Entrepreneur MSME entrepreneurs during the worlwide spread of COVID-19 Publication Issue: pandemic, this study aims at empirically examine the influence of entrepreneurial May - June 2020 personality in utilizing technology and government support for business resilience through crisis management as an intervening variable. Research design, data and method:This research is a quantitative study analyzing sample of 97 small and medium enterprisesactors in South Sulawesi, Indonesia, chosen by using purposive sampling. The main data in this study is results of questionnaires distributed to respondents which is analyzed by using Partial Least Square (PLS analysis). Results and Findings: This study proves a positive and significant relationship between entrepreneurship personlity and crisis management. Thereis no significant relationship between utilizing of technology toward crisis management. There is a Article History positive and significant relationship between government supporttoward crisis Article Received: 11 May 2020 management. This research also proves a positive and significant influence between Revised: 19 May 2020 crisis management on business resilience. Accepted: 29 May 2020 Publication: 12 June 2020 Keywords: Entrepreneurship Characteristic, Technology Utilization, Government Support , Business Resilience I. INTRODUCTION viruses that infect the respiratory system. This viral infection is called covid-19. The world has been being troubled by the Coronavirus causes common cold,amild to appearance of corona virus. -

GOLD Package Channel & VOD List

GOLD Package Channel & VOD List: incl Entertainment & Video Club (VOD), Music Club, Sports, Adult Note: This list is accurate up to 1st Aug 2018, but each week we add more new Movies & TV Series to our Video Club, and often add additional channels, so if there’s a channel missing you really wanted, please ask as it may already have been added. Note2: This list does NOT include our PLEX Club, which you get FREE with GOLD and PLATINUM Packages. PLEX Club adds another 500+ Movies & Box Sets, and you can ‘request’ something to be added to PLEX Club, and if we can source it, your wish will be granted. ♫: Music Choice ♫: Music Choice ♫: Music Choice ALTERNATIVE ♫: Music Choice ALTERNATIVE ♫: Music Choice DANCE EDM ♫: Music Choice DANCE EDM ♫: Music Choice Dance HD ♫: Music Choice Dance HD ♫: Music Choice HIP HOP R&B ♫: Music Choice HIP HOP R&B ♫: Music Choice Hip-Hop And R&B HD ♫: Music Choice Hip-Hop And R&B HD ♫: Music Choice Hit HD ♫: Music Choice Hit HD ♫: Music Choice HIT LIST ♫: Music Choice HIT LIST ♫: Music Choice LATINO POP ♫: Music Choice LATINO POP ♫: Music Choice MC PLAY ♫: Music Choice MC PLAY ♫: Music Choice MEXICANA ♫: Music Choice MEXICANA ♫: Music Choice Pop & Country HD ♫: Music Choice Pop & Country HD ♫: Music Choice Pop Hits HD ♫: Music Choice Pop Hits HD ♫: Music Choice Pop Latino HD ♫: Music Choice Pop Latino HD ♫: Music Choice R&B SOUL ♫: Music Choice R&B SOUL ♫: Music Choice RAP ♫: Music Choice RAP ♫: Music Choice Rap 2K HD ♫: Music Choice Rap 2K HD ♫: Music Choice Rock HD ♫: Music Choice