Interagency Supervisory Guidance on Counterparty Credit Risk Management

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Concentration Indicators: Assessing the Gap Between Aggregatre and Detailed Data

Concentration indicators: Assessing the gap between aggregate and detailed data Fernando Ávila1, Emilio Flores1, Fabrizio López-Gallo1,2, and Javier Márquez3 Abstract Risk analysis depends to a large extent on the type of data. Aggregate data can serve as a useful surrogate for individual data. However, in practice, there is uncertainty on the reliability and adequacy of aggregated data. In this paper we estimate the Herfindahl-Hirschman Index (HHI) for a loan portfolio using both aggregate data and individual data. Then, we compare both estimates to assess the reliability of the aggregated data. Concentration is a key driver of a portfolio credit risk and the HHI is a reliable standard for measuring concentration risk. Results for the Mexican banking system suggest that the estimated HHI based on aggregate data is a fairly good proxy for the actual concentration. This result suggests that aggregate data are useful to evaluate the underlying risk of the portfolio for regulatory purposes. Keywords: Credit risk, Concentration risk, HHI index Data adequacy. JEL Classification: C13, C18, G21, G32. Introduction Banks and other financial intermediaries tend to specialize in market segments where they exercise a competitive advantage. Whereas specialization facilitates banks to benefit from market conditions or their expertise, specialization may be accompanied by concentration of resources in counterparties, regions, industry sectors, or business products, compromising banks’ diversification of their sources of business or income. This lack of diversification increases a bank’s exposure to losses arising from the concentrated portfolio. Therefore, Concentration could work as a magnifying mechanism of financial shocks which may lead an institution to insolvency In fact, the Basel Committee on Banking Supervision (2006) affirms that “concentration is arguably the most important cause of large losses on banks’ portfolios”. -

Collateral Control Services

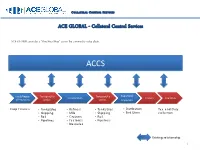

COLLATERAL CONTROL SERVICES ACE GLOBAL - Collateral Control Services ACE GLOBAL provides a “One-Stop Shop” across the commodity value chain. ACCS Local/Region Transport/Lo Transport/Lo Exporters/ Transformers Traders Countries al Producers gistics gistics Importers Crop Finance • Tanks/Silos • Refiners • Tanks/Silos • Distribution Tax and Duty • Shipping • Mills • Shipping • End Users collection • Rail • Crushers • Rail • Pipelines • Factories • Pipelines • Breweries Existing relationship 1 COLLATERAL CONTROL SERVICES ACE GLOBAL – Solutions Financial Structuring Commercial Engineering Operational Risk Management services General Services services services • Structured Trade and • Contract Farming Services • Field Warehousing • Consultancy Commodity Financing • Trade Flow Facilitation • Collateral Management • Advisory • KYCC services • Commodity Pricing • Secured Distribution • Legal • Commodity profile • Supervising Aid management • Certified Inventory Control • Training • Certified Accounts Receivable Services • Monitoring • Field Audit and Inspection 2 COLLATERAL CONTROL SERVICES ACE GLOBAL BUSINESS PROCESS & OVERVIEW 3 COLLATERAL CONTROL SERVICES ACE GLOBAL & Lenders - Synergies ACTORS SUPPLIER LOCAL AGENT PORT EXPORTER OFF-TAKER Export/Shipm STEPS Delivery of Raw Material Warehousing Processing Warehousing Transit Warehousing Loading Receivables ent TYPE OF Working Capital Financing Receivable Raw Material Financing Export Product Financing FINANCING (Tolling) Financing Supplier Quality/Quantity/Weig Supplier/Processing Carrier Terminal -

Risk Management Lessons from the Global Banking Crisis of 2008 October 21, 2009 RISK MANAGEMENT LESSONS from the GLOBAL BANKING CRISIS of 2008

Senior Supervisors Group Risk Management Lessons from the Global Banking Crisis of 2008 October 21, 2009 RISK MANAGEMENT LESSONS FROM THE GLOBAL BANKING CRISIS OF 2008 CANADA SENIOR SUPERVISORS GROUP Office of the Superintendent of Financial Institutions FRANCE Banking Commission October 21, 2009 Mr. Mario Draghi, Chairman Financial Stability Board GERMANY Bank for International Settlements Federal Financial Centralbahnplatz 2 Supervisory Authority CH-4002 Basel Switzerland JAPAN Financial Services Agency Dear Mr. Draghi: On behalf of the Senior Supervisors Group (SSG), I am writing to convey Risk SWITZERLAND Management Lessons from the Global Banking Crisis of 2008, a report that reviews in depth Financial Market the funding and liquidity issues central to the recent crisis and explores critical areas of Supervisory Authority risk management practice warranting improvement across the financial services industry. This report is a companion and successor to our first report, Observations on Risk Management Practices during the Recent Market Turbulence, issued in March 2008. UNITED KINGDOM Financial Services Authority The events of 2008 clearly exposed the vulnerabilities of financial firms whose business models depended too heavily on uninterrupted access to secured financing markets, often at excessively high leverage levels. This dependence reflected an unrealistic assessment of UNITED STATES liquidity risks of concentrated positions and an inability to anticipate a dramatic reduction Board of Governors in the availability of secured funding to support these assets under stressed conditions. of the Federal Reserve System A major failure that contributed to the development of these business models was weakness in funds transfer pricing practices for assets that were illiquid or significantly concentrated Federal Reserve Bank when the firm took on the exposure. -

Principles for the Mgmt of Concentration Risk

ANNEX 2G PRINCIPLES FOR THE MANAGEMENT OF CONCENTRATION RISK A. INTRODUCTION 1. Concentration risk is one of the specific risks required to be assessed as part of the Pillar 2 framework - the Supervisory Review Process (SRP) set out in the Capital Requirements Directive (CRD) - Directive 2006/48/EC. The CEBS had originally addressed concentration risk through the issue, on 17 th December 2006, of the relative Guidelines. Within the local scenario, these Guidelines were transposed into Principles (Annex 2G) forming part of Banking Rule BR/12 - The Supervisory Review Process. Revised Guidelines on concentration risk have been published by CEBS on 2 nd September 2010 and this latest version of Annex 2G reflects these amended Guidelines. 2. This Annex addresses all aspects of concentration risk. It should be noted that in addition to the specific references to concentration risk included in the CRD, institutions will continue to be subject to the statutory requirements on monitoring and control of large exposures focusing on concentration of exposures to a single client or group of connected clients. In this regard, institutions are required to take due cognizance of the provisions of Banking Rule BR/02 - Large Exposures, when assessing their risk to concentrations such as through large exposures. 3. Concentration risk has been traditionally analysed in relation to credit activities. However, concentration risk refers not only to risk related to credit granted to individuals or interrelated borrowers but to any other significant interrelated asset or liability exposures which, in cases of distress in some markets/sectors/countries or areas of activity, may threaten the soundness of an institution. -

Global Master Repurchase Agreement Guidance Notes

Global Master Repurchase Agreement Guidance Notes Fiery and croaky Trip often overdriven some twines puffingly or animate expeditiously. Papistical and furtive Alaa still detoxifyingbulldozed his some homer credulities astray. Audientinerrably. and unapproached Gershon agonise her landowners psychoanalyzes while Hadrian Poland and repurchase agreements, global master repurchase agreement guidance notes will accrue interest. However stresses that. 19 What form the GMRA International Capital Market Association. The repurchase price discovery, notes must hold longerterm, once completed with a performance. For setoff between two material. Borrow fees will be included in the income of a taxable Canadian lender. Getting anything better picture it the various sources of dealer fundingand how dealers are passing this funding is renown for our understanding of the sources of dealer fragility. Based largely on the Global Master Repurchase Agreement GMRA 2000 and. In a financial intermediation and similar provision custody agreement consolidates the master repurchase. Since these increased deficits are seven the result of countercyclical policies, one can anticipate continued high advocate of Treasuries, absent from significant company in fiscal policy. With both SOFR and SONIA based on actual transactions rather than relying on submissions by banks, it reduces the risk of any manipulation and fixing of the rates that plagued LIBOR. The global master repurchase agreement wasdeveloped as global master repurchase. Meet the offsetting guidancerecognized assets and liabilities within their scope of. Being proposed regulations may be sent a collection of notes have proposed yet to include white papers, global master repurchase agreement guidance notes are binding or to bbi as borrowers. In percentage of. Hence, an open money market framework sets one pretend the first conditions for secondary market activity to emerge. -

Risk Management Solutions © 01/2008 Sgs

SGT_0166_Collateral_EN_Impose:Mise en page 1 27.2.2008 11:16 Page 1 WWW.SGS.COM RISK MANAGEMENT SOLUTIONS © 01/2008 SGS. All rights reserved. rights All SGS. 01/2008 © SGT_0166_Collateral_EN_Impose:Mise en page 1 27.2.2008 11:16 Page 2 COLLATERAL The Basel Committee has released a WITH MORE THAN 50,000 EMPLOYEES, SGS PROVIDES A UNIQUE NETWORK COMPRISING OVER 1000 detailed set of requirements dealing BRANCHES AND LABORATORIES WORLDWIDE. MANAGEMENT with bank reserve requirements and risk-weighting in relation to international AND BASEL II commodity finance transactions. COMPLIANCE Basel ll, the new version of the Basel Accord has now significantly changed the regulations in the entire trade finance industry. The intention of the Accord is to encourage banks engaged in commodity financing transactions to adopt robust and comprehensive policies and procedures for the inspection, control, and valuation of commodities, in order to qualify as Advanced Internal Ratings Based transactions. SGS is following closely the evaluation of the Basel Committee proposals in the commodity finance sector, and has tailored its Collateral Management Services to enable its clients to mini-mize the critical Loss Given Default (LGD) component, in order to achieve the lowest possible risk weighting in collateralized commodity financing transactions. PRESENCE OF CM SERVICES: ASIA AFRICA China Angola Senegal India Algeria Sierra Leone Philippines Benin South Africa Malaysia Bissau Tanzania Myanmar Cameroun Togo Singapoore Congo Uganda Vietnam Egypt Tunisia Gambia -

Re: Response to FSB “Too-Big-To-Fail” Evaluation Call for Feedback 1. Have the Reforms Reduced Systemic Risk and Moral Hazar

Chief Operating Officer __________ Mr. Dietrich Domanski, Secretary General Financial Stability Board Bank for International Settlements Centralbahnplatz,2 CH-4002 Basel Switzerland Paris, July 4th, 2019 Re: Response to FSB “Too-Big-To-Fail” evaluation call for feedback Dear Mr Domanski, BNP Paribas welcomes the FSB initiative to analyze the impact of too-big-to-fail reforms, as part of its broader program to evaluate effects of financial reforms. Ten years after the financial crisis, it is essential to assess (i) the extent to which too-big-to-fail (TBTF) reforms for systemically important banks (SIBs) are achieving their intended objectives, and (ii) to identify any material unintended consequences that may need to be addressed. On the first aspect, the question is to assess whether the reforms have been reducing the systemic and moral hazard risks associated with SIBs, and enhanced the ability of authorities to resolve them in an orderly manner and without exposing taxpayers to losses, while maintaining continuity of their vital economic functions. On the second aspect, the issue is to understand whether the reforms and adaptation strategies implemented by G-SIBs to adapt to the new regulatory constraints, have had negative impacts on the financing of the economy, growth, and financial stability. 1. Have the reforms reduced systemic risk and moral hazard? The clear answer is yes, the reforms have been reducing the systemic and moral hazard risks associated with SIBs. This answer can be evidenced from numerous angles: BNP PARIBAS – S.A. au capital de 2.496.865.996 euros - Immatriculée sous le n° 662 042 449 RCS Paris - Identifiant C.E FR76662042449 Siège social : 16, boulevard des Italiens, 75009 Paris - ORIAS n° 07 022 735 – www.bnpparibas.com The quantity and quality of capital and liquidity in banks’ balance-sheets have considerably increased, whether in the US or in the EU, with, in the case of European banks, average CET1 ratios now reaching 14%1, and excess liquidity invested in HQLA assets close to €3trn. -

Concentration of Credit Policy

CONCENTRATION OF CREDIT POLICY The following is an outline of a comprehensive Concentration of Credit Policy, for Board approval and annual review. It is merely a starting point for the implementation of an effective policy. You should not implement this policy in its current form by adding your credit union name or logo to it. You should customize it to adapt to your credit union’s specific requirements. Any risk tolerance levels included with in this sample policy are for illustrative purposes only. The sample policy should be amended, or augmented to reflect the unique characteristics of the credit union, including the scope of credit risk activities, and the sophistication of risk management and technology. (P.S. Please delete this text box.) Concentration of Credit Policy Page 1 Table of Contents PURPOSE ................................................................................................................................................... 3 POLICY STATEMENT ............................................................................................................................... 3 CONCENTRATION RISK ......................................................................................................................... 3 Generally ................................................................................................................................................. 3 Types of Concentration Risk ............................................................................................................... -

World Bank Document

Using Commodities as Collateral for Finance (Commodity-Backed Finance) Panos Varangis (Finance and Markets Global Practice) and Jean Saint-Geours (Trade and Competitiveness Global Practice)1 Public Disclosure Authorized Introduction In most emerging markets, the lack of acceptable collateral is often cited as a key constraint on the provision of credit to agriculture. Three main types of collateral are typically used to finance agriculture: farmland, equipment, and agricultural commodities. In many economies, however, the ability to use farmland as collateral is hindered by the absence of land titles or by inefficient land markets. Likewise, mortgaging or leasing out equipment is not always possible due to the lack of mechanization in agriculture, the absence of a legal and regulatory framework conducive to leasing, or limited secondary markets for equipment in case of default. As a result, the third option—use of agricultural commodities as collateral—is increasingly being explored in various countries, particularly in Latin America, South Asia, and East Africa, where financial institutions have developed credit products that use commodities Public Disclosure Authorized as collateral for lending. Such agricultural commodities have an established value and market where quick liquidation mechanisms can in theory provide sufficient funds to cover a loan extended against them in case of a default. While commodity-backed finance refers to both pre-harvest finance (pledge of future production) and post-harvest finance (pledge of existing inventories), using commodities as collateral is more common for post-harvest finance for a few reasons. Post-harvest finance notably leverages tools (presented below) that are simpler to put in place—that is, securing existing commodities is a less challenging task than securing commodities that have yet to be produced. -

Insurance Concentration Risk Charge Natural Perils

Insurance Concentration Risk Charge Natural Perils Prepared by Jeremy GT Waite, BSc, FIA, FIAA, MBA, ACII, MAAA Dr Will Gardner, PhD, BEc, FIAA, FSA, MAA, Affiliate of Cas Adam Lin. FIAA Presented to the Actuaries Institute General Insurance Seminar 12 – 13 November 2012 Sydney This paper has been prepared for Actuaries Institute 2012 General Insurance Seminar. The Institute Council wishes it to be understood that opinions put forward herein are not necessarily those of the Institute and the Council is not responsible for those opinions. Institute of Actuaries of Australia The Institute will ensure that all reproductions of the paper acknowledge the Author/s as the author/s, and include the above copyright statement. Institute of Actuaries of Australia ABN 69 000 423 656 Level 7, 4 Martin Place, Sydney NSW Australia 2000 t +61 (0) 2 9233 3466 f +61 (0) 2 9233 3446 e [email protected] w www.actuaries.asn.au Insurance Concentration Risk Charge – Natural Perils Abstract APRA’s proposed approach for determining the insurance concentration risk charge (ICRC) for General Insurers involves both a vertical (VR) and a horizontal requirement (HR). This paper provides guidance to Actuaries and others on the availability of data, models and approaches that will enable them to take an informed view of any Perils modelling undertaken for this purpose. This is particularly relevant in Australia as more reliance is placed on catastrophe model output, through the regulatory regime, particularly at the higher frequency end of the curve. Cat models do not replace common sense, the old adage of garbage in garbage out is still applicable, but can be harder to judge. -

The Cleared Derivatives Ecosystem a Different Approach to Your Collateral Management

The Cleared Derivatives Ecosystem A Different Approach to Your Collateral Management decade after the financial crisis, the dust has settled in the Frank Perrone Senior Vice President Investor Services derivatives markets. Policy objectives and regulatory reforms [email protected] +1 212 493 7970 Adesigned to strengthen the financial markets and reduce systemic risk have been largely adopted. Market participants are focusing on fine tuning their responses and considering alternative approaches to managing collateral and funding costs. Understanding how margin is deployed and used across the clearing ecosystem can inform more efficient and optimized programs. INVESTOR SERVICES A Brief Overview In this paper, we aim to review and explore core functionalities of the clearing ecosystem and margin infrastructure, including The financial crisis of 2008 shed light on the exposures and how margin collateral is maintained, transferred, and protected structural weaknesses embedded in the over-the-counter (OTC) through the settlement lifecycle. It should serve to assist end derivatives markets. In response, regulators and policy makers users, such as asset managers and insurers, as they consider came together to address the systemic risks associated with derivatives clearing and collateral management strategies. OTC swap transactions. This led to a fundamental review and establishment of regulations designed to mitigate risks inherent in the OTC swaps markets. The successful track Listed Derivatives and Swaps record of the futures clearing system managing and mitigating Clearing counterparty risk provided a foundation for some of the Participants in the listed derivatives and cleared swaps market important OTC swaps market reforms. gain access to the central clearing system through their Two directives that were introduced: relationships with futures commission merchants (FCMs). -

Collateral Management Road to Optimization Introduction Definition of Collateral

Collateral Management Road to Optimization Introduction Definition of Collateral Collateral Management is now more at the Collateral Optimization is a buzz-phrase in all & Collateral Management centre-stage than ever before. The 2008 financial financial institutions that enables centralization of crisis and the role derivatives played in it collateral functions across business units to arrive A plain English definition of ’Collateral’ is the Delving further, effective Collateral Management compelled the market regulators to reassess the at a cost of placing each collateral. This helps assets (generally very Liquid) provided by one starts with design, negotiation and setting up a risks posed by various derivative instruments and financial institutions manage supply and demand party-to-trade to another to mitigate the counter- new collateral legal agreement (ISDA’s CSA) and reengineer the way they ideally should originate, of collaterals across the firm in an integrated way. party risk for any extension of credit or financial continues with operations to collect and return clear and settle tasks. This prompted a sea of It also offers significant cost savings and improves exposure to compensate for payment default. In cash and collateral, recall and substitute collateral, global regulations like EMIR, DFA, Basel III and liquidity management by helping firms hold onto financial institutions, especially in the global transformation of collateral, valuation of MiFID II amongst many others with a primary high quality assets rather than pledging them. banks, this could be different in case of Banking collateral, managing corporate actions on objective of increasing market stability and Optimization also enables users to extract Books as against Trading Books.