Property/Liability Insurance Risk Management and Securitization

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Best Practices for Lease Insurance Specifications

BEST PRACTICES FOR LEASE INSURANCE SPECIFICATIONS CHECKLIST VERSUS NARRATIVE FORMAT William H. Locke, Jr. Graves Dougherty Hearon & Moody Austin, Texas ACREL Annual Meeting Leasing and Insurance Committees Chicago October, 2012 1685471v2 TABLE OF CONTENTS I. INTRODUCTION .......................................................................................................................................................... 1 A. Contractual Risk Allocation .................................................................................................................................... 1 B. Risk of Casualty Loss and Injuries in Leased Premises .......................................................................................... 1 C. Heightened Risk Concern Arising During Periods of Financial Distress ................................................................ 2 D. Annotated Forms ..................................................................................................................................................... 2 II. FORMS ........................................................................................................................................................................... 3 A. Lease Provisions ...................................................................................................................................................... 3 1. Form A.1. - Insurance Specifications as Exhibit to Lease ............................................................................... 3 A. General -

Chapter 3: Escrow, Taxes, and Insurance

HB-2-3550 CHAPTER 3: ESCROW, TAXES, AND INSURANCE 3.1 INTRODUCTION To protect the Agency’s interest in the security property, the Servicing and Asset Management Office (Servicing Office) must ensure that real estate taxes and any other local assessments are paid and that the property remains adequately insured. To ensure that funds are available for these purposes, the Agency requires most borrowers who receive new loans to deposit funds to an escrow account. Borrowers who are not required to establish an escrow account may do so voluntarily. If an escrow account has been established, payments for insurance, taxes, and other assessments are made by the Agency. If an escrow account has not been established, the borrower is responsible for making timely payments. Section 1 of this chapter describes basic requirements for paying taxes and maintaining insurance coverage; Section 2 provides procedure for establishing and maintaining the escrow account; and Section 3 discusses procedures for addressing insured and uninsured losses to the security property. SECTION 1: TAX AND INSURANCE REQUIREMENTS [7 CFR 3550.60 and 3550.61] 3.2 TAXES AND OTHER LOCAL ASSESSMENTS The Agency contracts with a tax service to secure tax information for all borrowers. The tax service obtains tax bills due for payment, determines the optimal time to pay the taxes in order to take advantage of any discounts, and provides delinquent tax status on the portfolio. A. Tax Service Fee All borrowers are charged a tax service fee. Borrowers who obtain a subsequent loan are not required to pay a second tax service fee. -

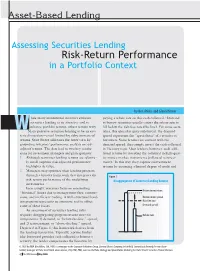

Assessing Securities Lending Risk-Return Performance in a Portfolio Context

Asset-Based Lending Assessing Securities Lending Risk-Return Performance in a Portfolio Context by Ben Atkins and Glenn Horner hile many institutional investors embrace paying a rebate rate on this cash collateral.1 Demand securities lending as an attractive tool to to borrow securities usually causes the rebate rate to enhance portfolio returns, others remain wary. fall below the risk-free rate (the line). For some secu- WMany perceive securities lending to be an eso- rities, this spread is quite substantial; the demand teric distraction—a tool limited by risky, immaterial spread represents the “specialness” of a security to returns. State Street addresses the latter view by borrowers. Some lenders are content with the grounding investors’ performance analysis on risk- demand spread; they simply invest the cash collateral adjusted returns. The data lead to two key conclu- in Treasury repo. Most lenders, however, seek addi- sions for investment managers and plan sponsors: tional returns by investing the collateral in high-qual- 1. Although securities lending returns are relative- ity money market instruments (collateral reinvest- ly small, superior risk-adjusted performance ment).2 In this way, they capture reinvestment highlights its value. returns by assuming a limited degree of credit and 2. Managers may optimize their lending program through a broader framework that integrates the Figure 1 risk-return performance of the underlying Disaggregation of Securities Lending Returns investments. Increasingly, investors focus on minimizing Reinvestment return “frictional” losses due to management fees, commis- sions, and inefficient trading. A well-structured lend- Reinvestment spread ing program represents an attractive tool to offset Risk-free rate some of these losses. -

S a M P L E D O C U M E N T Allstate Insurance Company Standard

Allstate Insurance Company S Standard HomeownersA PolicyM Policy: P Effective: Issued to: L E D O C U M Allstate Insurance Company The Company Named in the Policy Declarations A Stock Company----Home Office: Northbrook, Illinois 60062 E AP1 N T Table of Contents General Definitions Used In This Policy..................................2 Insurable Interest and Our Liability .........................11 InsuringSAgreement....................................................3 What You Must Do After A Loss.............................11 Agreements We Make With You...............................4 Our Settlement Options............................................12 Conformity To State Statutes ....................................4 How We Pay For A Loss...........................................12 Coverage Changes......................................................4 Our Settlement Of Loss ............................................14 Policy Transfer .A...........................................................4 Appraisal.....................................................................14 Continued Coverage After Your Death.....................4 Abandoned Property.................................................14 Cancellation .................................................................4 Permission Granted To You.....................................14 Concealment Or Fraud ..M.............................................5 Our Rights To Recover Payment.............................14 Our Rights To Obtain Salvage..................................14 -

Property Insurance Requirements TO

U.S. Department of Housing and OMB Approval No. 2502-0029 Property Insurance Urban Development (exp. 10/31/2012) Requirements Federal Housing Administration Public reporting burden for this collection of information is estimated to average .08 hours per response, including the time for reviewing instructions, searching existing data sources, gathering and maintaining the data needed, and completing and reviewing the collection of information. This is part of the basic application package for insured mortgages for construction of rental housing projects. This is a requirement under Section 207(b) of the National Housing Act (Public Law 479, 48 Stat. 1246, 12 U.S.C., 1701 et. seq.), authorizing the Secretary of HUD to insured mortgages. The information establishes property insurance requirements for a proposed multifamily project. The information is required to obtain benefits. Privacy Act Notice - The United States Department of Housing and Urban Development, Federal Housing Administration, is authorized to solicit the information requested in this form by virtue of Title 12, United States Code, Section 1701 et. seq., and regulations promulgated thereunder at Title 12, Code of Federal Regulations. While no assurances of confidentiality is pledged to respondents, HUD generally discloses this data only in response to a Freedom of Information request. This agency may not conduct or sponsor, and a person is not required to respond to, a collection of information unless that collection displays a valid OMB control number. _______________________________________________ -

Over Insurance Statutes by State State Statute Statutory Wording Alabama Alaska Over-Insurance Prohibited

Over Insurance Statutes by State State Statute Statutory Wording Alabama Alaska Over-Insurance Prohibited. (a) Over-insurance shall be considered to exist if property or an insurable interest in property is insured by one or more insurance contracts against the same hazard in an amount in excess of the fair value of the property or of the interest, as determined on the effective date of the insurance or the renewal of it. AS 21.60.010 (b) In this section the term "fair value" means the cost of replacement less depreciation that is properly applicable to the subject insured. (c) A person may not knowingly issue, place, procure, or accept an insurance contract that would result in over-insurance of the property or interest in the property proposed to be insured, except as provided in AS 21.60.020 . (d) Each violation of this section shall subject the violator to the penalties provided in AS 21.90.020 . Arizona 6-909 Prohibited Acts (Banking Law) P. A mortgage broker shall not require a person seeking a loan secured by real property to obtain property insurance coverage in an amount that exceeds the replacement cost of the improvements as established by the property insurer. 44-1208 44-1208. Loans secured by real estate; prohibited practices; insurance Except for consumer lender loans regulated pursuant to section 6-636, for any loan that is secured by real property, a person shall not require as a condition of the loan that the borrower obtain property insurance coverage in an amount that exceeds the replacement cost of the improvements as established by the property insurer. -

Understanding and Managing Risk in Public Investing

CDIAC/CMTA Advanced Public Funds Investing Workshop Session Three: Understanding and Managing Risk in Public Investing Presented by: Sarah Meacham, Managing Director January 15, 2020 PFM Asset 601 S. Figueroa Street, Suite 4500 Management LLC Los Angeles, CA 90017 www.pfm.com 213.489.4075 © PFM 1 TYPES OF FIXED INCOME INVESTMENT RISK Inflation Interest rate Topics Liquidity Reinvestment Credit HOW TO MANAGE AND MITIGATE RISK Investment policy development Diversification Discipline to long-term strategy Performance measurement © PFM 2 “Risk is inherent throughout the investment process. There is investment risk associated with any investment activity and opportunity risk related to inactivity.” ~Local Agency Investment Guidelines, CDIAC January 1, 2019 © PFM 3 Types of Fixed Income Investment Risk © PFM 4 Types of Fixed Income Investment Risk Inflation Risk Liquidity Risk Credit Risk Loss of purchasing Inability to sell portfolio Risk of default or power over time as a holdings at a competitive decline in security value result of inflation price due to issuer’s financial strength Reinvestment Risk Interest Rate Risk The risk that a security’s Variability of return/price cash flow will be related to changes in reinvested at a lower interest rates rate of return © PFM 5 Inflation Risk © PFM 6 Inflation (Purchasing Power) Risk Loss of purchasing power over time as a result of inflation Real interest rate is after inflation; nominal is before inflation • Real = nominal – inflation • Nominal = real + inflation • Inflation = nominal -

Homeowners Insurance Application

Homeowners Insurance Application Named Insured(s) and Mailing Address Insurance Company 650 Davis Street San Francisco, CA 94111 Primary Email: Insured Property Primary Phone #: Alternate Phone #: Bought through: NOTICE OF INSURANCE INFORMATION PRACTICES In some insurance transactions, we may not be able to get all the information we need directly from you. In that case, we may obtain information from outside sources at our own expense. We would also like to inform you that without prior authorization, we may as permitted by law, provide information about you contained in our records and files to certain persons or organizations. NOTICE: As part of Esurance's underwriting/qualification procedure and subject to applicable laws and regulations, we may obtain information regarding you and other individuals who may be covered by the insurance you are applying for, including: (i) driving record, based on state motor vehicle reports and loss information reports; (ii) your prior insurance record, if any, which will be obtained from your current or prior carrier(s); (iii) credit reports; and (iv) claim history, based on loss information reports. Policy Number Purchase Date and Time Effective Date Expiration Date Primary Applicant Information Name Date of Birth Gender Marital Status Education Level Existing Esurance Policy Drivers License Number DL State Currently Insured - Auto Length of Time with Current Auto Carrier Length of Time with Prior Auto Carrier Years with Prior Property Company Type of Current Property Policy Co -Applican t Information -

Mortgage Impairment / Mortgagee's Errors & Omissions Insurance

Mortgage Impairment / Mortgagee’s Errors & Omissions Insurance – Frequently Asked Questions What is Mortgage Impairment / Mortgagee’s Errors & Omissions insurance? Mortgage Impairment provides insurance coverage to a financial institution for a loss to its “mortgage interest” (defined as interest in real property as security for a loan) caused by the lack, or inadequacy, of insurance for Required Perils. Required Perils are the perils against which the mortgage agreement requires the borrower to insure the collateral property. These perils are fire, flood, and other similar direct physical damage perils. These Required Perils are typically covered by homeowner’s insurance, fire and extended coverage insurance, and flood insurance policies. Mortgagee’s Errors & Omissions provides liability insurance to a financial institution for negligent acts, errors, or omissions in procuring and/or failing to maintain insurance for Required Perils (as detailed above). What does this coverage do for me as a mortgage lender or mortgage servicer? Mortgage Impairment insurance covers loss Mortgagee’s Errors & Omissions insurance to the insured’s “mortgage interest” resulting covers the insured’s liability in: from physical damage to mortgaged property and: Failing to obtain or maintain required property insurance, Lack, or inadequacy, of insurance including flood insurance for Required Perils Flood zone determination Lack, or inadequacy, of insurance Failing to secure FHA/VA/PMI for Non-Required Perils (such as guarantees earthquake and flood insurance Failing to obtain or maintain life or Tax seizure disability insurance on the borrower Defective title (mortgagor) Failing to pay real estate taxes or special assessments What are some examples of claims that have been covered by this insurance? Mortgage Impairment A medium sized financial institution suffered a loss as a result of fire damage to a large residential property. -

Overview of Lender-Place Insurance Products, Markets and Issues Birny Birnbaum

Overview of Lender-Place Insurance Products, Markets and Issues Birny Birnbaum Lender-Placed Insurance Regulatory Working Group Outreach Session, June 13, 2013 © Birny Birnbaum Consulting, Inc. Birnbaum LPI Overview Page 1 June 13, 2013 Overview of Lender-Placed Insurnce Topics Covered 1. Ensuring Continuous Insurance Coverage 2. The LPI Policy 3. LPI Underwriting of Loan Portfolio 4. Blanket LPI vs. “Regular” LPI 5. Insurance Tracking 6. Other Features of LPI 7. Market Participants 8. Operation of Insurance Tracking and LPI 9. LPI Pricing 10. LPI Premium Charges Relative to Voluntary Property Insurance 11. LPI Flood 12. LPI Insurers 13. LPI by State 14. LPI Loss Ratios 15. Reverse Competition 16. Recent Regulatory Activity Involving LPI 17. Issues of Concern Birnbaum LPI Overview Page 2 June 13, 2013 1. Ensuring Continuous Insurance Coverage Mortgage loan agreements include a requirement that the borrower maintain insurance to protect the property serving as collateral for the loan and, if the borrower fails to maintain the required insurance or fails to provide required evidence of insurance, the lender, through the servicer, may place insurance on the property serving as collateral for the loan and charge the borrower for this insurance. When the mortgage owner hires a mortgage servicer to service the loan on behalf of the mortgage owner, the mortgage servicing agreement requires the servicer to maintain continuous insurance coverage on the properties serving as collateral for the mortgage loans. Lender-Placed Insurance (LPI) is an important tool for mortgage servicers to meet this requirement and for mortgage markets to operate smoothly. LPI is a master insurance policy issued to the mortgage servicer as the policyholder and insured. -

Diversification and Discussion of Risk

Diversification and Discussion of Risk Conference of the County Investment Academy San Antonio June 2019 PFIA 2256.008c Requires Training in: • Investment Diversification 2 Capital Market Theory 12.0% 10.0% 8.0% E( r) 6.0% P* * 4.0% 2.0% 0.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% Std. Dev. 3 Capital Market Theory • Points along the upper half of the curve represent the best risk/return diversified portfolios of risky assets • The straight line represents portfolios obtained by investing in the “optimal risky portfolio” (P*) and either lending or leveraging at the “risk‐free” rate. • Points on the line below the curve represent “lending” and points above represent “leveraging” (note increased “risk” as measured by standard deviation of returns!) 4 So in theory….. Key result? An undiversified portfolio yields inferior return for the level of risk! The same, or higher, return could be attained at a lower level of risk with a diversified portfolio. If you are not diversified, you are taking more risk than you can expect to be compensated for! 5 Diversification and Correlation of Returns Correlation, which measures the degree of “co‐ movement”, ranges from ‐1 to +1. When the correlation between returns is less than 1 there are diversification benefits—the risk of portfolio is less than the average of the risks of the individual assets. Which pair of stock returns is more correlated? Chevron, Exxon Chevron, Delta Airlines 6 International Diversification Correlations vs S&P 500: China 0.62 Korea 0.53 Japan 0.73 Germany 0.74 UK 0.73 Brazil 0.29 Chile 0.38 Monthly returns vs corresponding MSCI indexes (US dollar returns) 5 years ended April 2019 Source: FactSet 7 Global Market Capitalization Latin Canada 1% UK 3% Other 5% 1% Japan 8% Asia ex Japan 13% U.S. -

Model Insurance Requirements for a Commercial Mortgage Loan

Model Insurance Requirements For A Commercial Mortgage Loan James E. Branigan and Joshua Stein Commercial buildings make good collateral for a lender.They make even better collateral when properly insured against damage and destruction. ⅥⅥⅥ REAL ESTATE LOANS START FROM the A fire or other loss affecting the borrower’s fundamental assumption that the borrower’s building can undercut this very fundamental assumption and throw the loan into default building will continue to exist. As long as the rather quickly—unless the borrower has main- building exists, it can produce rental income so tained an appropriate package of insurance cov- the borrower can pay debt service. erage for the mortgaged property. James E. Branigan, President and Chief Executive Officer of Omega Risk Management LLC, has spoken extensively on insurance and risk management for bar associations and major law firms. His firm is a consultancy, which does not sell insurance. He can be reached at (631) 692-9866 or [email protected]. Joshua Stein, a partner in the New York office of Latham & Watkins LLP, is a member of the American College of Real Estate Lawyers, First Vice Chair of the New York State Bar Association Real Property Law Section, and author of New York Commercial Mortgage Transactions (Aspen 2002), A Practical Guide to Real Estate Practice (ALI-ABA 2001), and over 100 articles about commercial real estate law and prac- tice. He can be reached at (212) 906-1342 or [email protected]. An earlier version of this article appeared in The Real Estate Finance Journal 10 (Winter 2004) , and in Joshua Stein’s recent Mortgage Bankers Association book, Lender’s Guide to Structuring and Closing Commercial Mortgage Loans.