Blackrock Securities Lending

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Assessing Securities Lending Risk-Return Performance in a Portfolio Context

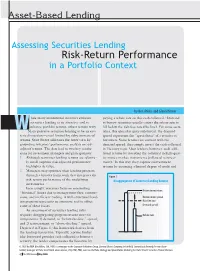

Asset-Based Lending Assessing Securities Lending Risk-Return Performance in a Portfolio Context by Ben Atkins and Glenn Horner hile many institutional investors embrace paying a rebate rate on this cash collateral.1 Demand securities lending as an attractive tool to to borrow securities usually causes the rebate rate to enhance portfolio returns, others remain wary. fall below the risk-free rate (the line). For some secu- WMany perceive securities lending to be an eso- rities, this spread is quite substantial; the demand teric distraction—a tool limited by risky, immaterial spread represents the “specialness” of a security to returns. State Street addresses the latter view by borrowers. Some lenders are content with the grounding investors’ performance analysis on risk- demand spread; they simply invest the cash collateral adjusted returns. The data lead to two key conclu- in Treasury repo. Most lenders, however, seek addi- sions for investment managers and plan sponsors: tional returns by investing the collateral in high-qual- 1. Although securities lending returns are relative- ity money market instruments (collateral reinvest- ly small, superior risk-adjusted performance ment).2 In this way, they capture reinvestment highlights its value. returns by assuming a limited degree of credit and 2. Managers may optimize their lending program through a broader framework that integrates the Figure 1 risk-return performance of the underlying Disaggregation of Securities Lending Returns investments. Increasingly, investors focus on minimizing Reinvestment return “frictional” losses due to management fees, commis- sions, and inefficient trading. A well-structured lend- Reinvestment spread ing program represents an attractive tool to offset Risk-free rate some of these losses. -

Understanding and Managing Risk in Public Investing

CDIAC/CMTA Advanced Public Funds Investing Workshop Session Three: Understanding and Managing Risk in Public Investing Presented by: Sarah Meacham, Managing Director January 15, 2020 PFM Asset 601 S. Figueroa Street, Suite 4500 Management LLC Los Angeles, CA 90017 www.pfm.com 213.489.4075 © PFM 1 TYPES OF FIXED INCOME INVESTMENT RISK Inflation Interest rate Topics Liquidity Reinvestment Credit HOW TO MANAGE AND MITIGATE RISK Investment policy development Diversification Discipline to long-term strategy Performance measurement © PFM 2 “Risk is inherent throughout the investment process. There is investment risk associated with any investment activity and opportunity risk related to inactivity.” ~Local Agency Investment Guidelines, CDIAC January 1, 2019 © PFM 3 Types of Fixed Income Investment Risk © PFM 4 Types of Fixed Income Investment Risk Inflation Risk Liquidity Risk Credit Risk Loss of purchasing Inability to sell portfolio Risk of default or power over time as a holdings at a competitive decline in security value result of inflation price due to issuer’s financial strength Reinvestment Risk Interest Rate Risk The risk that a security’s Variability of return/price cash flow will be related to changes in reinvested at a lower interest rates rate of return © PFM 5 Inflation Risk © PFM 6 Inflation (Purchasing Power) Risk Loss of purchasing power over time as a result of inflation Real interest rate is after inflation; nominal is before inflation • Real = nominal – inflation • Nominal = real + inflation • Inflation = nominal -

Transcript of Securities Lending and Short Sale Roundtable

210 1 UNITED STATES SECURITIES AND EXCHANGE COMMISSION 2 3 4 SECURITIES LENDING AND 5 SHORT SALE ROUNDTABLE 6 7 8 PAGES: 210 through 330 9 PLACE: U.S. Securities and Exchange Commission 10 100 F Street, N.E. 11 Washington, D.C. 12 DATE: Wednesday, September 30, 2009 13 14 15 16 The above-entitled matter came on for hearing, 17 pursuant to notice, at 9:33 a.m. 18 19 20 21 22 23 24 Diversified Reporting Services, Inc. 25 (202) 467-9200 211 1 P R O C E E D I N G S 2 CHAIRMAN SCHAPIRO: Good morning. Welcome today to 3 day two of the Securities and Exchange Commission's 4 Securities Lending and Short Sale Roundtable, which will 5 focus on short sale issues. 6 First, on behalf of the Commission, let me thank 7 all of you who've agreed to participate today. Our 8 consideration of these important short selling issues will be 9 enhanced by what I expect will be informative and interesting 10 comments, insights, and recommendations by our panelists. 11 During my tenure as Chairman, the issue of short 12 selling has been the subject of numerous inquiries, 13 suggestions and expressions of concern to the Commission. We 14 know that the practice of short selling evokes strong 15 opinions from both its supporters and detractors. I have 16 made it a priority to evaluate the issue of short selling 17 regulation and ensure that any future policies in this area 18 are the result of a deliberate and thoughtful process, which 19 is why we're here today. -

Property/Liability Insurance Risk Management and Securitization

PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Biography Trent R. Vaughn, FCAS, MAAA, is Vice President of Actuarial/Pricing at GRE Insurance Group in Keene, NH. Mr. Vaughn is a 1990 graduate of Central College in Pella, Iowa. He is also the author of a recent Proceedings paper and has been a member of the CAS Examination Committee since 1996. Acknowledgments The author would like to thank an anonymous reviewer from the CAS Continuing Education Committee for his or her helpful comments. PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Abstract This paper presents a comprehensive framework for property/liability insurance risk management and securitization. Section 2 presents a rationale for P/L insurance risk management. Sections 3 through 6 describe and evaluate the four categories of P/L insurance risk management techniques: (1) maintaining internal capital within the organization, (2) managing asset risk, (3) managing underwriting risk, and (4) managing the covariance between asset and liability returns. Securitization is specifically discussed as a potential method of managing underwriting risk. Lastly, Section 7 outlines four key guidelines for cost- effective risk management. 1. INTRODUCTION In recent years, the property-liability insurance industry has witnessed intense competition from alternative risk management techniques, such as large deductibles and retentions, risk retention groups, and captive insurance companies. Moreover, the next decade promises to bring additional competition from new players in the P/L insurance industry, including commercial banks and securities firms. In order to survive in this competitive new landscape, P/L insurers must manage total risk in a cost-efficient manner. This paper provides a rationale for P/L insurance risk management, then describes four categories of risk management techniques utilized by insurers. -

Diversification and Discussion of Risk

Diversification and Discussion of Risk Conference of the County Investment Academy San Antonio June 2019 PFIA 2256.008c Requires Training in: • Investment Diversification 2 Capital Market Theory 12.0% 10.0% 8.0% E( r) 6.0% P* * 4.0% 2.0% 0.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% Std. Dev. 3 Capital Market Theory • Points along the upper half of the curve represent the best risk/return diversified portfolios of risky assets • The straight line represents portfolios obtained by investing in the “optimal risky portfolio” (P*) and either lending or leveraging at the “risk‐free” rate. • Points on the line below the curve represent “lending” and points above represent “leveraging” (note increased “risk” as measured by standard deviation of returns!) 4 So in theory….. Key result? An undiversified portfolio yields inferior return for the level of risk! The same, or higher, return could be attained at a lower level of risk with a diversified portfolio. If you are not diversified, you are taking more risk than you can expect to be compensated for! 5 Diversification and Correlation of Returns Correlation, which measures the degree of “co‐ movement”, ranges from ‐1 to +1. When the correlation between returns is less than 1 there are diversification benefits—the risk of portfolio is less than the average of the risks of the individual assets. Which pair of stock returns is more correlated? Chevron, Exxon Chevron, Delta Airlines 6 International Diversification Correlations vs S&P 500: China 0.62 Korea 0.53 Japan 0.73 Germany 0.74 UK 0.73 Brazil 0.29 Chile 0.38 Monthly returns vs corresponding MSCI indexes (US dollar returns) 5 years ended April 2019 Source: FactSet 7 Global Market Capitalization Latin Canada 1% UK 3% Other 5% 1% Japan 8% Asia ex Japan 13% U.S. -

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk, and Incentive Issues Frank M. Keane Securities loans collateralized by cash are by far the most popular form of securities-lending transaction. But when the www.newyorkfed.org/research/current_issues F cash collateral associated with these transactions is actively reinvested by a lender’s agent, potential risks emerge. This 2013 F study argues that the standard compensation scheme for securities-lending agents, which typically provides for agents to share in gains but not losses, creates incentives for them to take excessive risk. It also highlights the need for greater scrutiny and understanding of cash reinvestment practices— especially in light of the AIG experience, which showed that Volume 19, Number 3 Volume risks related to cash reinvestment, by even a single participant, could have destabilizing effects. lthough less researched than the money markets, the collateral markets IN ECONOMICS AND FINANCE are critical to the efficiency of the asset markets—including the markets for ATreasury, agency, and agency mortgage-backed securities. Well-functioning collateral markets allow dealers and investors in the asset markets to finance short positions for the purposes of hedging, market making, settlement, and arbitrage. Two important mechanisms for accessing the U.S. money and collateral markets are repurchase agreements (repos) and securities-lending transactions. In a money market transaction, when cash and securities are exchanged, the securities act as collateral and mitigate the risks associated with a borrower’s failure to repay the cash. In a collateral market transaction, however, the cash serves as collateral and mitigates the risk associated with replacing the security if the borrower fails to return it. -

The Guide to Securities Lending

3&"$)#&:0/%&91&$5"5*0/4 An Introduction to Securities Lending First Canadian Edition An Introduction to $IPPTFTFDVSJUJFTMFOEJOHTFSWJDFTXJUIBO Securities Lending JOUFSOBUJPOBMSFBDIBOEBEFUBJMFEGPDVT Mark C. Faulkner, Managing Director, Spitalfields Advisors Spitalfields Managing Director, Mark C. Faulkner, First Canadian Edition 5SVTUFECZNPSFUIBOCPSSPXFSTXPSMEXJEFJOHMPCBMNBSLFUT QMVTUIF64 BOE$BOBEB $*#$.FMMPOJTDPNNJUUFEUPQSPWJEJOHVOSJWBMMFETFDVSJUJFTMFOEJOH TFSWJDFTUP$BOBEJBOJOTUJUVUJPOBMJOWFTUPST8FMFWFSBHFOFBSMZZFBSTPG EFBMFSBOEUSBEJOHFYQFSJFODFUPIFMQDMJFOUTBDIJFWFIJHIFSSFUVSOTXJUIPVU Mark C. Faulkner, Managing Director DPNQSPNJTJOHBTTFUTFDVSJUZ 0VSTUSBUFHZJTUPNBYJNJ[FSFUVSOTBOEDPOUSPMSJTLCZGPDVTJOHJOUFOUMZPOUIF Spitalfields Advisors TUSVDUVSFBOEEFUBJMTPGFBDIMPBO5IBUJTXIZXFPGGFSBMFOEJOHQSPHSBNUIBUJT USBOTQBSFOU SJTLDPOUSPMMFEBOEEPFTOPUJNQFEFZPVSGVOETUSBEJOHBOEWBMVBUJPO QSPDFTT4PZPVDBOFYDFFEFYQFDUBUJPOT ■ (MPCBM$VTUPEZ ■ 4FDVSJUJFT-FOEJOH ■ 0VUTPVSDJOH ■ 8PSLCFODI ■ #FOFmU1BZNFOUT ■ 'PSFJHO&YDIBOHF &OBCMJOH:PVUP 'PDVTPO:PVS8PSME XXXDJCDNFMMPODPN XXXXPSLCFODIDJCDNFMMPODPN $*#$.FMMPO(MPCBM4FDVSJUJFT4FSWJDFT$PNQBOZJTBMJDFOTFEVTFSPGUIF$*#$BOE.FMMPOUSBEFNBSLT ______________________________ An Introduction to Securities Lending First Canadian Edition Mark C. Faulkner Spitalfields Advisors Limited 155 Commercial Street London E1 6BJ United Kingdom Published in Canada First published, 2006 © Mark C. Faulkner, 2006 First Edition, 2006 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, -

Securities Lending, Market Liquidity and Retirement Savings: the Real World Impact November 2015 ______

Securities Lending, Market Liquidity and Retirement Savings: The Real World Impact November 2015 ______________________________________________________________________________________________________________________________________ Securities Lending, Market Liquidity and Retirement Savings: The Real World Impact November 2015 Josh Galper Managing Principal PO Box 560 Concord, MA 01742 USA Tel: 1-978-318-0920 http://www.Finadium.com © 2015 Finadium LLC. All rights reserved. Reproduction of this report by any means is strictly prohibited. Securities Lending, Market Liquidity and Retirement Savings: The Real World Impact November 2015 ______________________________________________________________________________________________________________________________________ Table of Contents Why Securities Lending Matters ........................................................................ 1 Sizing the Market ........................................................................................................ 2 The Uses of Securities Loans ..................................................................................... 4 Securities Lending, Market Efficiency and Economic Growth ........................ 6 Evidence on Equity Market Liquidity and Short Selling .............................................. 7 Efficient Markets and Economic Growth ................................................................... 10 How Much Do Investors Earn from Securities Lending? ............................... 12 Where Is the Risk in Securities Lending? -

The Naked Truth: Examining Prevailing Practices in Short Sales and the Resultant Voter Disenfranchisement

The Naked Truth: Examining Prevailing Practices in Short Sales and the Resultant Voter Disenfranchisement ROBE R T BR OOKS AND CLAY M. MOFFETT FORMAT ANY ROBE R T BR OOKS iterature on short-selling activity due to the costs associated with shorting is Wallace D. Malone, Jr. is a common topic for financial, stocks, thusIN leaving only optimistic investors Endowed Chair of Finan- economic, accounting, and legal and the resulting inflated asset prices; and cial Management in the Department of Finance, authors and has been since the very second, that there are a number of short sales Lfirst journals were established (De la Vega constraints that reduce or limit the number of University of Alabama in Tuscaloosa, AL. [1688]). Short sales occur when a shareholder short sellers. These constraints include: [email protected] sells a share of stock he does not own (by bor-ARTICLE rowing shares), and only later acquires them, • Borrowing costs. The shorter has to be CLAY M. MOFFETT which then closes out the transaction. In so able to borrow and provide securities to is an assistant professor in the Department of doing, there may be various borrowingTHIS costs the purchaser of shares. The proceeds Finance, University of associated with the transaction. The short are then retained by the broker serving North Carolina, seller profits from the transaction if the share as collateral for the securities lender. Wilmington, NC. price declines more than the all-in costs of The interest that is paid is theoreti- [email protected] the transaction by the time he closes out the cally paid to the lender, who then must transaction. -

Interest Rate Risk • Interest Rate Risk Is the Risk Market Rates Will Change. O

MANAGING BOND PORTFOLIOS Interest Rate Risk Interest rate risk is the risk market rates will change. o Price risk—bond prices (values) move opposite interest rates; there exists an inverse relationship such that prices decrease when market rates increase, and vice versa. o Reinvestment risk—interest rate changes are positively related to the ability to reinvest at favorable rates; that is, when market rates increase, the coupon interest that is paid by a bond can be reinvested at higher rates, and vice versa. Interest rate sensitivity—the characteristics of bonds indicate how sensitive bond prices are to changes in interest rates. o Bond prices move opposite changes in interest rates (inversely related). When market yields increase, bond price decrease, and vice versa. A price decrease that results from an increase in the market rate will be less than a price increase that results from an equivalent decrease in the market rate. o Everything else equal, bond prices are more sensitive for bonds with: . Longer terms to maturity than bonds with shorter terms to maturity. The sensitivity of longer-term bonds increases at a decreasing rate, which means that a bond with 20 years to maturity is not twice as sensitive to changes in market rates than a bond with 10 years to maturity; e.g., the price of a 10-year bond might decrease by 6 percent when market rates increase, whereas the price of the 20- year bond would decrease by 9 percent for the same change in market rates. Bonds with lower coupon rates than bonds with higher coupon rates. -

Asset Securitisation

Superseded document Basel Committee on Banking Supervision Consultative Document Asset Securitisation Supporting Document to the New Basel Capital Accord Issued for comment by 31 May 2001 January 2001 Superseded document Superseded document Table of Contents OVERVIEW .............................................................................................................................................1 I. THE TREATMENT OF EXPLICIT RISKS ASSOCIATED WITH TRADITIONAL SECURITISATION........................................................................................................................1 A. THE STANDARDISED APPROACH .............................................................................................2 1. The treatment for originating banks..........................................................................2 (a) Minimum operational requirements for achieving a clean break.................................3 (b) Minimum capital requirements for credit enhancements ............................................3 (c) Minimum operational requirements for revolving securitisations with early amortisation features .............................................................................................................4 2. The treatment for investing banks ............................................................................6 (a) Minimum capital requirements for investments in ABS...............................................6 (b) Treatment of unrated securitisations ..........................................................................7 -

Over-The-Counter Market Liquidity and Securities Lending by Nathan Foley-Fisher, Stefan Gissler and Stéphane Verani

BIS Working Papers No 768 Over-the-Counter Market Liquidity and Securities Lending by Nathan Foley-Fisher, Stefan Gissler and Stéphane Verani Monetary and Economic Department February 2019 JEL classification: G01, G12, G22, G23 Keywords: Over-the-counter markets, corporate bonds, market liquidity, securities lending, insurance companies, broker-dealers BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS. This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2019. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated. ISSN 1020-0959 (print) ISSN 1682-7678 (online) Over-the-Counter Market Liquidity and Securities Lending∗ Nathan Foley-Fisher Stefan Gissler Stéphane Verani y December 2018 Abstract This paper studies how over-the-counter market liquidity is affected by securities lending. We combine micro-data on corporate bond market trades with securities lending transactions and individual corporate bond holdings by U.S. insurance companies. Applying a difference-in-differences empirical strategy, we show that the shutdown of AIG’s securities lending program in 2008 caused a statistically and economically significant reduction in the market liquidity of corporate bonds predominantly held by AIG. We also show that an important mechanism behind the decrease in corporate bond liquidity was a shift towards relatively small trades among a greater number of dealers in the interdealer market.