Asset Securitisation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Analysis of Securitized Asset Liquidity June 2017 an He and Bruce Mizrach1

Analysis of Securitized Asset Liquidity June 2017 An He and Bruce Mizrach1 1. Introduction This research note extends our prior analysis2 of corporate bond liquidity to the structured products markets. We analyze data from the TRACE3 system, which began collecting secondary market trading activity on structured products in 2011. We explore two general categories of structured products: (1) real estate securities, including mortgage-backed securities in residential housing (MBS) and commercial building (CMBS), collateralized mortgage products (CMO) and to-be-announced forward mortgages (TBA); and (2) asset-backed securities (ABS) in credit cards, autos, student loans and other miscellaneous categories. Consistent with others,4 we find that the new issue market for securitized assets decreased sharply after the financial crisis and has not yet rebounded to pre-crisis levels. Issuance is below 2007 levels in CMBS, CMOs and ABS. MBS issuance had recovered by 2012 but has declined over the last four years. By contrast, 2016 issuance in the corporate bond market was at a record high for the fifth consecutive year, exceeding $1.5 trillion. Consistent with the new issue volume decline, the median age of securities being traded in non-agency CMO are more than ten years old. In student loans, the average security is over seven years old. Over the last four years, secondary market trading volumes in CMOs and TBA are down from 14 to 27%. Overall ABS volumes are down 16%. Student loan and other miscellaneous ABS declines balance increases in automobiles and credit cards. By contrast, daily trading volume in the most active corporate bonds is up nearly 28%. -

Asset Securitization

L-Sec Comptroller of the Currency Administrator of National Banks Asset Securitization Comptroller’s Handbook November 1997 L Liquidity and Funds Management Asset Securitization Table of Contents Introduction 1 Background 1 Definition 2 A Brief History 2 Market Evolution 3 Benefits of Securitization 4 Securitization Process 6 Basic Structures of Asset-Backed Securities 6 Parties to the Transaction 7 Structuring the Transaction 12 Segregating the Assets 13 Creating Securitization Vehicles 15 Providing Credit Enhancement 19 Issuing Interests in the Asset Pool 23 The Mechanics of Cash Flow 25 Cash Flow Allocations 25 Risk Management 30 Impact of Securitization on Bank Issuers 30 Process Management 30 Risks and Controls 33 Reputation Risk 34 Strategic Risk 35 Credit Risk 37 Transaction Risk 43 Liquidity Risk 47 Compliance Risk 49 Other Issues 49 Risk-Based Capital 56 Comptroller’s Handbook i Asset Securitization Examination Objectives 61 Examination Procedures 62 Overview 62 Management Oversight 64 Risk Management 68 Management Information Systems 71 Accounting and Risk-Based Capital 73 Functions 77 Originations 77 Servicing 80 Other Roles 83 Overall Conclusions 86 References 89 ii Asset Securitization Introduction Background Asset securitization is helping to shape the future of traditional commercial banking. By using the securities markets to fund portions of the loan portfolio, banks can allocate capital more efficiently, access diverse and cost- effective funding sources, and better manage business risks. But securitization markets offer challenges as well as opportunity. Indeed, the successes of nonbank securitizers are forcing banks to adopt some of their practices. Competition from commercial paper underwriters and captive finance companies has taken a toll on banks’ market share and profitability in the prime credit and consumer loan businesses. -

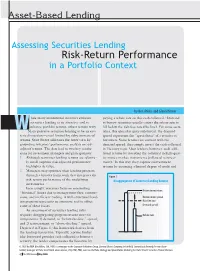

Assessing Securities Lending Risk-Return Performance in a Portfolio Context

Asset-Based Lending Assessing Securities Lending Risk-Return Performance in a Portfolio Context by Ben Atkins and Glenn Horner hile many institutional investors embrace paying a rebate rate on this cash collateral.1 Demand securities lending as an attractive tool to to borrow securities usually causes the rebate rate to enhance portfolio returns, others remain wary. fall below the risk-free rate (the line). For some secu- WMany perceive securities lending to be an eso- rities, this spread is quite substantial; the demand teric distraction—a tool limited by risky, immaterial spread represents the “specialness” of a security to returns. State Street addresses the latter view by borrowers. Some lenders are content with the grounding investors’ performance analysis on risk- demand spread; they simply invest the cash collateral adjusted returns. The data lead to two key conclu- in Treasury repo. Most lenders, however, seek addi- sions for investment managers and plan sponsors: tional returns by investing the collateral in high-qual- 1. Although securities lending returns are relative- ity money market instruments (collateral reinvest- ly small, superior risk-adjusted performance ment).2 In this way, they capture reinvestment highlights its value. returns by assuming a limited degree of credit and 2. Managers may optimize their lending program through a broader framework that integrates the Figure 1 risk-return performance of the underlying Disaggregation of Securities Lending Returns investments. Increasingly, investors focus on minimizing Reinvestment return “frictional” losses due to management fees, commis- sions, and inefficient trading. A well-structured lend- Reinvestment spread ing program represents an attractive tool to offset Risk-free rate some of these losses. -

Asset Pricing with Liquidity Risk∗

Asset Pricing with Liquidity Risk∗ Viral V. Acharyay and Lasse Heje Pedersenz First Version: July 10, 2000 Current Version: September 24, 2004 Abstract This paper solves explicitly an equilibrium asset pricing model with liq- uidity risk — the risk arising from unpredictable changes in liquidity over time. In our liquidity-adjusted capital asset pricing model, a security's re- quired return depends on its expected liquidity as well as on the covariances of its own return and liquidity with market return and market liquidity. In addition, the model shows how a negative shock to a security's liquidity, if it is persistent, results in low contemporaneous returns and high predicted future returns. The model provides a simple, unified framework for under- standing the various channels through which liquidity risk may affect asset prices. Our empirical results shed light on the total and relative economic significance of these channels. ∗We are grateful for conversations with Andrew Ang, Joseph Chen, Sergei Davydenko, Fran- cisco Gomes, Joel Hasbrouck, Andrew Jackson, Tim Johnson, Martin Lettau, Anthony Lynch, Stefan Nagel, Lubos Pastor, Tano Santos, Dimitri Vayanos, Luis Viceira, Jeff Wurgler, and semi- nar participants at London Business School, London School of Economics, New York University, the National Bureau of Economic Research (NBER) Summer Institute 2002, the Five Star Confer- ence 2002, Western Finance Association Meetings 2003, and the Texas Finance Festival 2004. We are especially indebted to Yakov Amihud and to an anonymous referee for help and many valuable suggestions. All errors remain our own. yAcharya is at London Business School and is a Research Affiliate of the Centre for Eco- nomic Policy Research (CEPR). -

Understanding and Managing Risk in Public Investing

CDIAC/CMTA Advanced Public Funds Investing Workshop Session Three: Understanding and Managing Risk in Public Investing Presented by: Sarah Meacham, Managing Director January 15, 2020 PFM Asset 601 S. Figueroa Street, Suite 4500 Management LLC Los Angeles, CA 90017 www.pfm.com 213.489.4075 © PFM 1 TYPES OF FIXED INCOME INVESTMENT RISK Inflation Interest rate Topics Liquidity Reinvestment Credit HOW TO MANAGE AND MITIGATE RISK Investment policy development Diversification Discipline to long-term strategy Performance measurement © PFM 2 “Risk is inherent throughout the investment process. There is investment risk associated with any investment activity and opportunity risk related to inactivity.” ~Local Agency Investment Guidelines, CDIAC January 1, 2019 © PFM 3 Types of Fixed Income Investment Risk © PFM 4 Types of Fixed Income Investment Risk Inflation Risk Liquidity Risk Credit Risk Loss of purchasing Inability to sell portfolio Risk of default or power over time as a holdings at a competitive decline in security value result of inflation price due to issuer’s financial strength Reinvestment Risk Interest Rate Risk The risk that a security’s Variability of return/price cash flow will be related to changes in reinvested at a lower interest rates rate of return © PFM 5 Inflation Risk © PFM 6 Inflation (Purchasing Power) Risk Loss of purchasing power over time as a result of inflation Real interest rate is after inflation; nominal is before inflation • Real = nominal – inflation • Nominal = real + inflation • Inflation = nominal -

Liquidity Risk Management

BASEL III FRAMEWORK Liquidity Risk Management Rules and Guidelines November 2018 Table of Contents TABLE OF CONTENTS ...................................................................................................................................... 2 LIST OF ACRONYMS ......................................................................................................................................... 4 PART I – LIQUIDITY RISK MANAGEMENT FRAMEWORK ............................................................... 5 1. BACKGROUND AND OVERVIEW ............................................................................................................................ 5 2. SCOPE OF APPLICATION ...................................................................................................................................... 5 3. STATEMENT OF OBJECTIVES ................................................................................................................................ 5 4. ONGOING LIQUIDITY MANAGEMENT ................................................................................................................... 5 5. MEASURING AND MONITORING LIQUIDITY REQUIREMENTS ............................................................................. 7 6. MANAGING MARKET ACCESS .............................................................................................................................. 9 7. CONTINGENCY PLANNING ................................................................................................................................... -

IBOR to RFR Transition

Changing the world’s most important number IBOR to RFR transition March 2021 home.kpmg/in 2 Foreword For more than three decades, London Interbank all 35 LIBOR settings at once, giving firms a Offered Rate (‘LIBOR’) has been integrated in clear set of deadlines across all currencies and financial markets, serving as the benchmark tenors. FCA issued that all seven tenors for for borrowings, loans and derivative contracts. both euro and Swiss franc LIBOR, overnight, LIBOR has hence been called the ‘world’s one-week, two-month and 12-month sterling most important number’ as it is hardwired LIBOR, spot next, one-week, two-month and in all financial activities, such as treasury, 12-month yen LIBOR and one-week and two- risk management, accounting including month U.S. dollar LIBOR will permanently hedge accounting, valuation and commercial cease immediately after 31 December 2021. contracts. Following the global financial crisis, Overnight and 12-month U.S. dollar LIBOR regulators discovered that the banks entrusted settings publication will cease immediately after to set the rates underpinning hundreds of 30 June 2023. trillions of dollars of financial assets had been In response, the regulators and market manipulating them to their advantage, raising participants across the globe have been questions about the future sustainability of developing new benchmarks to replace Libor LIBOR. Regulators globally have signaled clearly by the end of 2021. With 31 December 2021, that institutions should transition away from in plain sight, and FCA announcement on the Interbank Offered Rate (IBOR) to alternative LIBOR cessation, preparation for the transition overnight risk-free rates (RFRs). -

Securitization, Monetary Policy and Bank Stability

Securitization, Monetary Policy and Bank Stability Mohamed Bakousha,1,∗, Tapas Mishraa,2, Simon Wolfea,3, aSouthampton Business School, University of Southampton, UK Abstract We provide new evidence about the effect of securitization activities on bank stability and systemic risk in the run-up to and following the global financial crisis by consid- ering the role of monetary policy interest rates. In so doing, we propose S{score as a new measure of the net effect of securitization activities on bank stability. Analyzing the dynamics of this measure at the individual bank level and the banking system level shows that securitization activities have a destabilizing effect on banks. We also find that securitization increases commonality of asset returns among banks leading to increased interconnectedness and systemic risk. We also find that low monetary policy interest rates in the aftermath of the global financial crisis have mitigated the destabilizing effect of securitization on banks. Keywords: Securitization, Bank Profitability, Bank Risk, Bank Stability, Systemic Risk; Monetary Policy JEL Classification: G21; G10 ∗Corresponding Author (Email: [email protected]). 1Mohamed Bakoush is an Assistant Professor in Banking and Finance, Southampton Business School, University of Southampton. (Email: [email protected]) 2Tapas Mishra is a Professor of Banking and Finance, Southampton Business School, University of Southampton. (Email: [email protected]) 3Simon Wolfe is a Professor of Banking and Finance, Southampton Business School, University of Southampton.(Email: [email protected]) Preprint submitted to Elsevier December 31, 2019 1. Introduction Securitization has fundamentally altered the way in which financial intermediation is organized as it has provided banks with an innovative way to improve efficiency and performance. -

COVID-19 Impact on Bank Liquidity Risk Management and Response

COVID-19 impact on bank liquidity risk management and response Overview As a result of COVID-19 and the actions In response to the recent adverse market the economy during adverse situations taken by governments and businesses activity, the Federal Reserve Board such as the impacts of COVID-19 and to to help mitigate the impact, financial (the Fed) has taken steps to stabilize the enable banks to continue lending. The Fed is institutions have been challenged in their financial markets through the purchase of encouraging banks to use their capital and ability to manage and report on their Treasuries and government guaranteed liquidity buffers as they make loans available liquidity positions and funding capabilities. mortgage-backed securities, reviving to households and businesses affected by Regulatory requirements put in place the Primary Dealer Credit Facility to offer the COVID-19 restrictions, assuming this after 2008 were designed to improve loans to securities firms, reestablishing lending is done in a safe and sound manner2. banks’ ability to meet funding obligations the Money Market Mutual Fund Facility, by establishing liquidity buffers, and to and substantially expanding its repo Industry challenges in liquidity implement contingency funding plans operations1 The Fed has also encouraged and funding risk management (CFPs) to guide banks during times of crisis. banks to start borrowing from its discount However, recent equity market volatility, window and regulators have extended the Although the Fed has taken steps to stabilize liquidity tightening, widening funding timeline for certain regulatory requirements the market and make funding available, spreads, operational fails, and (e.g. the Current Expected Credit Losses many banks have already activated their other challenges have put significant implementation) in an effort to reduce CFPs and are actively managing and pressure on bank liquidity some pressure on bank resources. -

Property/Liability Insurance Risk Management and Securitization

PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Biography Trent R. Vaughn, FCAS, MAAA, is Vice President of Actuarial/Pricing at GRE Insurance Group in Keene, NH. Mr. Vaughn is a 1990 graduate of Central College in Pella, Iowa. He is also the author of a recent Proceedings paper and has been a member of the CAS Examination Committee since 1996. Acknowledgments The author would like to thank an anonymous reviewer from the CAS Continuing Education Committee for his or her helpful comments. PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Abstract This paper presents a comprehensive framework for property/liability insurance risk management and securitization. Section 2 presents a rationale for P/L insurance risk management. Sections 3 through 6 describe and evaluate the four categories of P/L insurance risk management techniques: (1) maintaining internal capital within the organization, (2) managing asset risk, (3) managing underwriting risk, and (4) managing the covariance between asset and liability returns. Securitization is specifically discussed as a potential method of managing underwriting risk. Lastly, Section 7 outlines four key guidelines for cost- effective risk management. 1. INTRODUCTION In recent years, the property-liability insurance industry has witnessed intense competition from alternative risk management techniques, such as large deductibles and retentions, risk retention groups, and captive insurance companies. Moreover, the next decade promises to bring additional competition from new players in the P/L insurance industry, including commercial banks and securities firms. In order to survive in this competitive new landscape, P/L insurers must manage total risk in a cost-efficient manner. This paper provides a rationale for P/L insurance risk management, then describes four categories of risk management techniques utilized by insurers. -

Diversification and Discussion of Risk

Diversification and Discussion of Risk Conference of the County Investment Academy San Antonio June 2019 PFIA 2256.008c Requires Training in: • Investment Diversification 2 Capital Market Theory 12.0% 10.0% 8.0% E( r) 6.0% P* * 4.0% 2.0% 0.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% Std. Dev. 3 Capital Market Theory • Points along the upper half of the curve represent the best risk/return diversified portfolios of risky assets • The straight line represents portfolios obtained by investing in the “optimal risky portfolio” (P*) and either lending or leveraging at the “risk‐free” rate. • Points on the line below the curve represent “lending” and points above represent “leveraging” (note increased “risk” as measured by standard deviation of returns!) 4 So in theory….. Key result? An undiversified portfolio yields inferior return for the level of risk! The same, or higher, return could be attained at a lower level of risk with a diversified portfolio. If you are not diversified, you are taking more risk than you can expect to be compensated for! 5 Diversification and Correlation of Returns Correlation, which measures the degree of “co‐ movement”, ranges from ‐1 to +1. When the correlation between returns is less than 1 there are diversification benefits—the risk of portfolio is less than the average of the risks of the individual assets. Which pair of stock returns is more correlated? Chevron, Exxon Chevron, Delta Airlines 6 International Diversification Correlations vs S&P 500: China 0.62 Korea 0.53 Japan 0.73 Germany 0.74 UK 0.73 Brazil 0.29 Chile 0.38 Monthly returns vs corresponding MSCI indexes (US dollar returns) 5 years ended April 2019 Source: FactSet 7 Global Market Capitalization Latin Canada 1% UK 3% Other 5% 1% Japan 8% Asia ex Japan 13% U.S. -

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk, and Incentive Issues Frank M. Keane Securities loans collateralized by cash are by far the most popular form of securities-lending transaction. But when the www.newyorkfed.org/research/current_issues F cash collateral associated with these transactions is actively reinvested by a lender’s agent, potential risks emerge. This 2013 F study argues that the standard compensation scheme for securities-lending agents, which typically provides for agents to share in gains but not losses, creates incentives for them to take excessive risk. It also highlights the need for greater scrutiny and understanding of cash reinvestment practices— especially in light of the AIG experience, which showed that Volume 19, Number 3 Volume risks related to cash reinvestment, by even a single participant, could have destabilizing effects. lthough less researched than the money markets, the collateral markets IN ECONOMICS AND FINANCE are critical to the efficiency of the asset markets—including the markets for ATreasury, agency, and agency mortgage-backed securities. Well-functioning collateral markets allow dealers and investors in the asset markets to finance short positions for the purposes of hedging, market making, settlement, and arbitrage. Two important mechanisms for accessing the U.S. money and collateral markets are repurchase agreements (repos) and securities-lending transactions. In a money market transaction, when cash and securities are exchanged, the securities act as collateral and mitigate the risks associated with a borrower’s failure to repay the cash. In a collateral market transaction, however, the cash serves as collateral and mitigates the risk associated with replacing the security if the borrower fails to return it.