Securities Lending Best Practices

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

UBS News for Banks and Financial Institutions March 03, 2011

UBS News for Banks and Financial Institutions March 03, 2011 Priority: Urgent – Market: Poland Poland: Change of Custodian UBS Zurich is changing its custodian in the Polish market from SIX SIS AG / Bank Handlowy W Warszawie, Warsaw to Bank PeKAO (UniCredit Group), Warsaw as of trade date March 24, 2011. New settlement instructions Trades with settlement date (SD) until and including March 28, 2011 will be settled with UBS' current sub-custodian Bank Handlowy W Warszawie, Warsaw. Trades with settlement date as from March 29, 2011 need to be submitted with the instruction details of UBS' new custodian Bank PeKAO (UniCredit Group), Warsaw (see below). Settlement instructions (as from SD March 29, 2011) Custodian (NEW) Bank PeKAO, Warsaw SWIFT BIC (NEW) PKOPPLPWCUS SWIFT BIC UBS UBSWCHZH80A Account No. Individual account for each client New cut-off times – client deadlines Equities / Fixed Income DFP/RFP SD; 4 p.m. T-Bills DFP/RFP SD; 1 p.m. Equities / Fixed Income DVP/RVP SD; 8 a.m. T-Bills DVP/RVP SD; 8 a.m. Impact Clients and counterparties are requested to instruct with the new custodian details as from settlement date March 29, 2011. To see full market details, please access the Market Guide Poland. Should you have any questions, please contact your UBS – Source: UBS AG Relationship Manager or Account Manager. UBS AG Securities Services P.O. Box CH-8098 Zurich Switzerland Phone: +41-44-236 61 36 Email: [email protected] While the facts in this publication have been carefully researched, UBS cannot be held responsible for their accuracy. -

UBS (CH) Investment Fund B

Unit Accoun- Reference Initial Launch Minimum Smallest Annual Form of Approp- class¹ ting currency subscrip- period/date* subscription tradeable fee custody riation of currency tion price lot income I-A110 USD USD 1 000 Not yet n/a 0.001 0.21%2 Registered7 Accumulating known (0.17%) I-A210 USD USD 1 000 Not yet 10 000 00011 0.001 0.18%2 Registered7 Accumulating known (0.14%) I-A310 USD USD 1 000 Not yet 30 000 00012 0.001 0.15%2 Registered7 Accumulating known (0.12%) I-B8 USD USD 1 000 Not yet n/a 0.001 0.035%5 Registered7 Accumulating known I-X8 USD USD 1 000 04.11.2014 n/a 0.001 0.00%6 Registered7 Accumulating U-X USD USD 100 000 Not yet n/a 0.001 0.00%6 Registered7 Accumulating known UBS (CH) Investment Fund B. UBS (CH) Investment Fund – Bonds CHF Ausland Medium Term Passive Investment fund under Swiss law with multiple sub-funds Unit Accoun- Reference Initial Launch Minimum Smallest Annual Form of Approp- (umbrella fund) class¹ ting currency subscrip- period/date* subscription tradeable fee custody riation of (Category Other Funds for Traditional Investments) currency tion price lot income W CHF CHF 100 Not yet n/a 0.001 0.18%3 Bearer Accumulating known (0.14%) Prospectus with integrated fund contract February 2017 F9 CHF CHF 100 Not yet n/a 0.001 0.14%4 Registered7 Accumulating known (0.11%) I-A110 CHF CHF 1 000 Not yet n/a 0.001 0.18%2 Registered7 Accumulating known (0.14%) I-A210 CHF CHF 1 000 Not yet 10 000 00011 0.001 0.18%2 Registered7 Accumulating known (0.14%) I-A310 CHF CHF 1 000 Not yet 30 000 00012 0.001 0.14%2 Registered7 Accumulating known (0.11%) I-B8 CHF CHF 1 000 Not yet n/a 0.001 0.045%5 Registered7 Accumulating known I-X8 CHF CHF 1 000 04.11.2014 n/a 0.001 0.00%6 Registered7 Accumulating U-X CHF CHF 100 000 Not yet n/a 0.001 0.00%6 Registered7 Accumulating known Part I Prospectus C. -

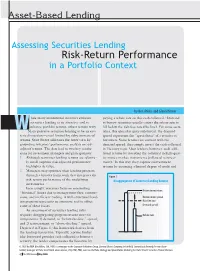

Assessing Securities Lending Risk-Return Performance in a Portfolio Context

Asset-Based Lending Assessing Securities Lending Risk-Return Performance in a Portfolio Context by Ben Atkins and Glenn Horner hile many institutional investors embrace paying a rebate rate on this cash collateral.1 Demand securities lending as an attractive tool to to borrow securities usually causes the rebate rate to enhance portfolio returns, others remain wary. fall below the risk-free rate (the line). For some secu- WMany perceive securities lending to be an eso- rities, this spread is quite substantial; the demand teric distraction—a tool limited by risky, immaterial spread represents the “specialness” of a security to returns. State Street addresses the latter view by borrowers. Some lenders are content with the grounding investors’ performance analysis on risk- demand spread; they simply invest the cash collateral adjusted returns. The data lead to two key conclu- in Treasury repo. Most lenders, however, seek addi- sions for investment managers and plan sponsors: tional returns by investing the collateral in high-qual- 1. Although securities lending returns are relative- ity money market instruments (collateral reinvest- ly small, superior risk-adjusted performance ment).2 In this way, they capture reinvestment highlights its value. returns by assuming a limited degree of credit and 2. Managers may optimize their lending program through a broader framework that integrates the Figure 1 risk-return performance of the underlying Disaggregation of Securities Lending Returns investments. Increasingly, investors focus on minimizing Reinvestment return “frictional” losses due to management fees, commis- sions, and inefficient trading. A well-structured lend- Reinvestment spread ing program represents an attractive tool to offset Risk-free rate some of these losses. -

Understanding Private Equity in the Healthcare Market June 2019 Table of Contents

UNDERSTANDING PRIVATE EQUITY IN THE HEALTHCARE MARKET JUNE 2019 TABLE OF CONTENTS SECTION PAGE I. BCA Introduction 1 II. Healthcare Market Dynamics 8 III. What is Private Equity? 13 IV. What is a Recapitalization? 17 V. Appendix 20 I. BCA INTRODUCTION BCA IS ONE OF THE LARGEST HEALTHCARE BOUTIQUE INVESTMENT BANKS KEY FACTS 19 $6.4 billion 1 PARTNER-OWNED Total Investment Bankers Total Transaction Value 90% 10.9x 2 RELATIONSHIP-DRIVEN Closure Rate Avg. EBITDA Mult. For Healthcare Services Deals Closed in 2018 3 HEALTHCARE-FOCUSED 100 $85 million Total Transactions Closed Average Transaction Size 4 RESULTS-ORIENTED RELEVANT HEALTHCARE SERVICES TRANSACTIONS Recapitalization Sell-Side Recapitalization Recapitalization Recapitalization RecapitalizationSell-Side Recapitalization Recapitalization Recapitalization Recapitalization Recapitalization Recapitalization Recapitalization Recapitalization Led By Led By Led By Sell-Side Advisory Recapitalization Recapitalization Sell-Side Advisory Led by Led by Led by Led By to Led by Led By to UnitrancheRecapitalization Debt RecapitalizationGrowth Equity RecapitalizationSell-Side Buy Side Recapitalization Sell-Side Recapitalization Recapitalization Recapitalization Recapitalization Acquired Recapitalization Debt-Private placement Equity Investment Sell-Side Advisory Recapitalization Led By Led By Led By Sell-Side Advisory Led by Led by Led By to Led by to $113,000,000 1 OUR HEALTHCARE INVESTMENT BANKING TEAM EXTENSIVE INDUSTRY KNOWLEDGE & EXPERIENCED INVESTMENT BANKERS 2 3 DEEP BENCH 1 TRANSACTION EXPERIENCE -

Understanding and Managing Risk in Public Investing

CDIAC/CMTA Advanced Public Funds Investing Workshop Session Three: Understanding and Managing Risk in Public Investing Presented by: Sarah Meacham, Managing Director January 15, 2020 PFM Asset 601 S. Figueroa Street, Suite 4500 Management LLC Los Angeles, CA 90017 www.pfm.com 213.489.4075 © PFM 1 TYPES OF FIXED INCOME INVESTMENT RISK Inflation Interest rate Topics Liquidity Reinvestment Credit HOW TO MANAGE AND MITIGATE RISK Investment policy development Diversification Discipline to long-term strategy Performance measurement © PFM 2 “Risk is inherent throughout the investment process. There is investment risk associated with any investment activity and opportunity risk related to inactivity.” ~Local Agency Investment Guidelines, CDIAC January 1, 2019 © PFM 3 Types of Fixed Income Investment Risk © PFM 4 Types of Fixed Income Investment Risk Inflation Risk Liquidity Risk Credit Risk Loss of purchasing Inability to sell portfolio Risk of default or power over time as a holdings at a competitive decline in security value result of inflation price due to issuer’s financial strength Reinvestment Risk Interest Rate Risk The risk that a security’s Variability of return/price cash flow will be related to changes in reinvested at a lower interest rates rate of return © PFM 5 Inflation Risk © PFM 6 Inflation (Purchasing Power) Risk Loss of purchasing power over time as a result of inflation Real interest rate is after inflation; nominal is before inflation • Real = nominal – inflation • Nominal = real + inflation • Inflation = nominal -

Transcript of Securities Lending and Short Sale Roundtable

210 1 UNITED STATES SECURITIES AND EXCHANGE COMMISSION 2 3 4 SECURITIES LENDING AND 5 SHORT SALE ROUNDTABLE 6 7 8 PAGES: 210 through 330 9 PLACE: U.S. Securities and Exchange Commission 10 100 F Street, N.E. 11 Washington, D.C. 12 DATE: Wednesday, September 30, 2009 13 14 15 16 The above-entitled matter came on for hearing, 17 pursuant to notice, at 9:33 a.m. 18 19 20 21 22 23 24 Diversified Reporting Services, Inc. 25 (202) 467-9200 211 1 P R O C E E D I N G S 2 CHAIRMAN SCHAPIRO: Good morning. Welcome today to 3 day two of the Securities and Exchange Commission's 4 Securities Lending and Short Sale Roundtable, which will 5 focus on short sale issues. 6 First, on behalf of the Commission, let me thank 7 all of you who've agreed to participate today. Our 8 consideration of these important short selling issues will be 9 enhanced by what I expect will be informative and interesting 10 comments, insights, and recommendations by our panelists. 11 During my tenure as Chairman, the issue of short 12 selling has been the subject of numerous inquiries, 13 suggestions and expressions of concern to the Commission. We 14 know that the practice of short selling evokes strong 15 opinions from both its supporters and detractors. I have 16 made it a priority to evaluate the issue of short selling 17 regulation and ensure that any future policies in this area 18 are the result of a deliberate and thoughtful process, which 19 is why we're here today. -

The Securities Custody Industry

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Chan, Diana; Fontan, Florence; Rosati, Simonetta; Russo, Daniela Research Report The securities custody industry ECB Occasional Paper, No. 68 Provided in Cooperation with: European Central Bank (ECB) Suggested Citation: Chan, Diana; Fontan, Florence; Rosati, Simonetta; Russo, Daniela (2007) : The securities custody industry, ECB Occasional Paper, No. 68, European Central Bank (ECB), Frankfurt a. M. This Version is available at: http://hdl.handle.net/10419/154521 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten -

Property/Liability Insurance Risk Management and Securitization

PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Biography Trent R. Vaughn, FCAS, MAAA, is Vice President of Actuarial/Pricing at GRE Insurance Group in Keene, NH. Mr. Vaughn is a 1990 graduate of Central College in Pella, Iowa. He is also the author of a recent Proceedings paper and has been a member of the CAS Examination Committee since 1996. Acknowledgments The author would like to thank an anonymous reviewer from the CAS Continuing Education Committee for his or her helpful comments. PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Abstract This paper presents a comprehensive framework for property/liability insurance risk management and securitization. Section 2 presents a rationale for P/L insurance risk management. Sections 3 through 6 describe and evaluate the four categories of P/L insurance risk management techniques: (1) maintaining internal capital within the organization, (2) managing asset risk, (3) managing underwriting risk, and (4) managing the covariance between asset and liability returns. Securitization is specifically discussed as a potential method of managing underwriting risk. Lastly, Section 7 outlines four key guidelines for cost- effective risk management. 1. INTRODUCTION In recent years, the property-liability insurance industry has witnessed intense competition from alternative risk management techniques, such as large deductibles and retentions, risk retention groups, and captive insurance companies. Moreover, the next decade promises to bring additional competition from new players in the P/L insurance industry, including commercial banks and securities firms. In order to survive in this competitive new landscape, P/L insurers must manage total risk in a cost-efficient manner. This paper provides a rationale for P/L insurance risk management, then describes four categories of risk management techniques utilized by insurers. -

Diversification and Discussion of Risk

Diversification and Discussion of Risk Conference of the County Investment Academy San Antonio June 2019 PFIA 2256.008c Requires Training in: • Investment Diversification 2 Capital Market Theory 12.0% 10.0% 8.0% E( r) 6.0% P* * 4.0% 2.0% 0.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% Std. Dev. 3 Capital Market Theory • Points along the upper half of the curve represent the best risk/return diversified portfolios of risky assets • The straight line represents portfolios obtained by investing in the “optimal risky portfolio” (P*) and either lending or leveraging at the “risk‐free” rate. • Points on the line below the curve represent “lending” and points above represent “leveraging” (note increased “risk” as measured by standard deviation of returns!) 4 So in theory….. Key result? An undiversified portfolio yields inferior return for the level of risk! The same, or higher, return could be attained at a lower level of risk with a diversified portfolio. If you are not diversified, you are taking more risk than you can expect to be compensated for! 5 Diversification and Correlation of Returns Correlation, which measures the degree of “co‐ movement”, ranges from ‐1 to +1. When the correlation between returns is less than 1 there are diversification benefits—the risk of portfolio is less than the average of the risks of the individual assets. Which pair of stock returns is more correlated? Chevron, Exxon Chevron, Delta Airlines 6 International Diversification Correlations vs S&P 500: China 0.62 Korea 0.53 Japan 0.73 Germany 0.74 UK 0.73 Brazil 0.29 Chile 0.38 Monthly returns vs corresponding MSCI indexes (US dollar returns) 5 years ended April 2019 Source: FactSet 7 Global Market Capitalization Latin Canada 1% UK 3% Other 5% 1% Japan 8% Asia ex Japan 13% U.S. -

FT PARTNERS RESEARCH 2 Fintech Meets Alternative Investments

FT PARTNERS FINTECH INDUSTRY RESEARCH Alternative Investments FinTech Meets Alternative Investments Innovation in a Burgeoning Asset Class March 2020 DRAFT ©2020 FinTech Meets Alternative Investments Alternative Investments FT Partners | Focused Exclusively on FinTech FT Partners’ Advisory Capabilities FT Partners’ FinTech Industry Research Private Capital Debt & Raising Equity Sell-Side / In-Depth Industry Capital Buy-Side Markets M&A Research Reports Advisory Capital Strategic Structuring / Consortium Efficiency Proprietary FinTech Building Advisory FT Services FINTECH Infographics Partners RESEARCH & Board of INSIGHTS Anti-Raid Advisory Directors / Advisory / Monthly FinTech Special Shareholder Committee Rights Plans Market Analysis Advisory Sell-Side Valuations / LBO Fairness FinTech M&A / Financing Advisory Opinion for M&A Restructuring Transaction Profiles and Divestitures Named Silicon Valley’s #1 FinTech Banker Ranked #1 Most Influential Person in all of Numerous Awards for Transaction (2016) and ranked #2 Overall by The FinTech in Institutional Investors “FinTech Excellence including Information Finance 40” “Deal of the Decade” • Financial Technology Partners ("FT Partners") was founded in 2001 and is the only investment banking firm focused exclusively on FinTech • FT Partners regularly publishes research highlighting the most important transactions, trends and insights impacting the global Financial Technology landscape. Our unique insight into FinTech is a direct result of executing hundreds of transactions in the sector combined with over 18 years of exclusive focus on Financial Technology FT PARTNERS RESEARCH 2 FinTech Meets Alternative Investments I. Executive Summary 5 II. Industry Overview and The Rise of Alternative Investments 8 i. An Introduction to Alternative Investments 9 ii. Trends Within the Alternative Investment Industry 23 III. Executive Interviews 53 IV. -

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk, and Incentive Issues Frank M. Keane Securities loans collateralized by cash are by far the most popular form of securities-lending transaction. But when the www.newyorkfed.org/research/current_issues F cash collateral associated with these transactions is actively reinvested by a lender’s agent, potential risks emerge. This 2013 F study argues that the standard compensation scheme for securities-lending agents, which typically provides for agents to share in gains but not losses, creates incentives for them to take excessive risk. It also highlights the need for greater scrutiny and understanding of cash reinvestment practices— especially in light of the AIG experience, which showed that Volume 19, Number 3 Volume risks related to cash reinvestment, by even a single participant, could have destabilizing effects. lthough less researched than the money markets, the collateral markets IN ECONOMICS AND FINANCE are critical to the efficiency of the asset markets—including the markets for ATreasury, agency, and agency mortgage-backed securities. Well-functioning collateral markets allow dealers and investors in the asset markets to finance short positions for the purposes of hedging, market making, settlement, and arbitrage. Two important mechanisms for accessing the U.S. money and collateral markets are repurchase agreements (repos) and securities-lending transactions. In a money market transaction, when cash and securities are exchanged, the securities act as collateral and mitigate the risks associated with a borrower’s failure to repay the cash. In a collateral market transaction, however, the cash serves as collateral and mitigates the risk associated with replacing the security if the borrower fails to return it. -

The Guide to Securities Lending

3&"$)#&:0/%&91&$5"5*0/4 An Introduction to Securities Lending First Canadian Edition An Introduction to $IPPTFTFDVSJUJFTMFOEJOHTFSWJDFTXJUIBO Securities Lending JOUFSOBUJPOBMSFBDIBOEBEFUBJMFEGPDVT Mark C. Faulkner, Managing Director, Spitalfields Advisors Spitalfields Managing Director, Mark C. Faulkner, First Canadian Edition 5SVTUFECZNPSFUIBOCPSSPXFSTXPSMEXJEFJOHMPCBMNBSLFUT QMVTUIF64 BOE$BOBEB $*#$.FMMPOJTDPNNJUUFEUPQSPWJEJOHVOSJWBMMFETFDVSJUJFTMFOEJOH TFSWJDFTUP$BOBEJBOJOTUJUVUJPOBMJOWFTUPST8FMFWFSBHFOFBSMZZFBSTPG EFBMFSBOEUSBEJOHFYQFSJFODFUPIFMQDMJFOUTBDIJFWFIJHIFSSFUVSOTXJUIPVU Mark C. Faulkner, Managing Director DPNQSPNJTJOHBTTFUTFDVSJUZ 0VSTUSBUFHZJTUPNBYJNJ[FSFUVSOTBOEDPOUSPMSJTLCZGPDVTJOHJOUFOUMZPOUIF Spitalfields Advisors TUSVDUVSFBOEEFUBJMTPGFBDIMPBO5IBUJTXIZXFPGGFSBMFOEJOHQSPHSBNUIBUJT USBOTQBSFOU SJTLDPOUSPMMFEBOEEPFTOPUJNQFEFZPVSGVOETUSBEJOHBOEWBMVBUJPO QSPDFTT4PZPVDBOFYDFFEFYQFDUBUJPOT ■ (MPCBM$VTUPEZ ■ 4FDVSJUJFT-FOEJOH ■ 0VUTPVSDJOH ■ 8PSLCFODI ■ #FOFmU1BZNFOUT ■ 'PSFJHO&YDIBOHF &OBCMJOH:PVUP 'PDVTPO:PVS8PSME XXXDJCDNFMMPODPN XXXXPSLCFODIDJCDNFMMPODPN $*#$.FMMPO(MPCBM4FDVSJUJFT4FSWJDFT$PNQBOZJTBMJDFOTFEVTFSPGUIF$*#$BOE.FMMPOUSBEFNBSLT ______________________________ An Introduction to Securities Lending First Canadian Edition Mark C. Faulkner Spitalfields Advisors Limited 155 Commercial Street London E1 6BJ United Kingdom Published in Canada First published, 2006 © Mark C. Faulkner, 2006 First Edition, 2006 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted,