Estimation of Risk-Free Rate As a Part of Financial Management

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

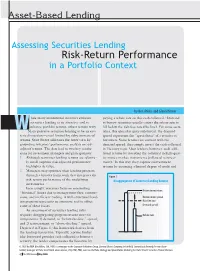

Assessing Securities Lending Risk-Return Performance in a Portfolio Context

Asset-Based Lending Assessing Securities Lending Risk-Return Performance in a Portfolio Context by Ben Atkins and Glenn Horner hile many institutional investors embrace paying a rebate rate on this cash collateral.1 Demand securities lending as an attractive tool to to borrow securities usually causes the rebate rate to enhance portfolio returns, others remain wary. fall below the risk-free rate (the line). For some secu- WMany perceive securities lending to be an eso- rities, this spread is quite substantial; the demand teric distraction—a tool limited by risky, immaterial spread represents the “specialness” of a security to returns. State Street addresses the latter view by borrowers. Some lenders are content with the grounding investors’ performance analysis on risk- demand spread; they simply invest the cash collateral adjusted returns. The data lead to two key conclu- in Treasury repo. Most lenders, however, seek addi- sions for investment managers and plan sponsors: tional returns by investing the collateral in high-qual- 1. Although securities lending returns are relative- ity money market instruments (collateral reinvest- ly small, superior risk-adjusted performance ment).2 In this way, they capture reinvestment highlights its value. returns by assuming a limited degree of credit and 2. Managers may optimize their lending program through a broader framework that integrates the Figure 1 risk-return performance of the underlying Disaggregation of Securities Lending Returns investments. Increasingly, investors focus on minimizing Reinvestment return “frictional” losses due to management fees, commis- sions, and inefficient trading. A well-structured lend- Reinvestment spread ing program represents an attractive tool to offset Risk-free rate some of these losses. -

The Effect of Systematic Risk Factors on the Performance of the Malaysia Stock Market

57 Proceedings of International Conference on Economics 2017 (ICE 2017) PROCEEDINGS ICE 2017 P57 – P68 ISBN 978-967-0521-99-2 THE EFFECT OF SYSTEMATIC RISK FACTORS ON THE PERFORMANCE OF THE MALAYSIA STOCK MARKET Shameer Fahmi, Caroline Geetha, Rosle Mohidin Faculty of Business, Economics and Accountancy, Universiti Malaysia Sabah ABSTRACT Malaysia has undergone a tremendous transformation in its economic due to the New Economic This has created instability on the changes in the macroeconomic fundamental, called systematic risk. The study aims to determine the effect of the systematic risk towards the performance of the stock returns. The paper aims to use the arbitrage pricing theory (APT) framework to relate the systematic risk with the performance of stock return. The variables chosen to represent the systematic risk were variables that were in line with the transformation policy implemented. The independent variables chosen were interest rate, inflation rate due to the removal of fuel subsidy and the implementation of good and service tax, exchange rate which is influenced by the inflow of foreign direct investment, crude oil price that determines the revenue of the country being an oil exporter and industrial production index that reflect political as well as business news meanwhile the dependent variable is stock returns. All the macroeconomic variables will be regressed with the lagged 2 of its own variable to obtain the residuals. The residuals will be powered by two to obtain the variance which represents the risk of each variable. The variables were run for unit root to determine the level of stationarity. This was followed by the establishment of long run relationship using Johansen Cointegration and short run relationship using Vector Error Correction Modeling. -

Understanding and Managing Risk in Public Investing

CDIAC/CMTA Advanced Public Funds Investing Workshop Session Three: Understanding and Managing Risk in Public Investing Presented by: Sarah Meacham, Managing Director January 15, 2020 PFM Asset 601 S. Figueroa Street, Suite 4500 Management LLC Los Angeles, CA 90017 www.pfm.com 213.489.4075 © PFM 1 TYPES OF FIXED INCOME INVESTMENT RISK Inflation Interest rate Topics Liquidity Reinvestment Credit HOW TO MANAGE AND MITIGATE RISK Investment policy development Diversification Discipline to long-term strategy Performance measurement © PFM 2 “Risk is inherent throughout the investment process. There is investment risk associated with any investment activity and opportunity risk related to inactivity.” ~Local Agency Investment Guidelines, CDIAC January 1, 2019 © PFM 3 Types of Fixed Income Investment Risk © PFM 4 Types of Fixed Income Investment Risk Inflation Risk Liquidity Risk Credit Risk Loss of purchasing Inability to sell portfolio Risk of default or power over time as a holdings at a competitive decline in security value result of inflation price due to issuer’s financial strength Reinvestment Risk Interest Rate Risk The risk that a security’s Variability of return/price cash flow will be related to changes in reinvested at a lower interest rates rate of return © PFM 5 Inflation Risk © PFM 6 Inflation (Purchasing Power) Risk Loss of purchasing power over time as a result of inflation Real interest rate is after inflation; nominal is before inflation • Real = nominal – inflation • Nominal = real + inflation • Inflation = nominal -

Systematic Risk of Cdos and CDO Arbitrage

Systematic risk of CDOs and CDO arbitrage Alfred Hamerle (University of Regensburg) Thilo Liebig (Deutsche Bundesbank) Hans-Jochen Schropp (University of Regensburg) Discussion Paper Series 2: Banking and Financial Studies No 13/2009 Discussion Papers represent the authors’ personal opinions and do not necessarily reflect the views of the Deutsche Bundesbank or its staff. Editorial Board: Heinz Herrmann Thilo Liebig Karl-Heinz Tödter Deutsche Bundesbank, Wilhelm-Epstein-Strasse 14, 60431 Frankfurt am Main, Postfach 10 06 02, 60006 Frankfurt am Main Tel +49 69 9566-0 Telex within Germany 41227, telex from abroad 414431 Please address all orders in writing to: Deutsche Bundesbank, Press and Public Relations Division, at the above address or via fax +49 69 9566-3077 Internet http://www.bundesbank.de Reproduction permitted only if source is stated. ISBN 978-3–86558–570–7 (Printversion) ISBN 978-3–86558–571–4 (Internetversion) Abstract “Arbitrage CDOs” have recorded an explosive growth during the years before the outbreak of the financial crisis. In the present paper we discuss potential sources of such arbitrage opportunities, in particular arbitrage gains due to mispricing. For this purpose we examine the risk profiles of Collateralized Debt Obligations (CDOs) in some detail. The analyses reveal significant differences in the risk profile between CDO tranches and corporate bonds, in particular concerning the considerably increased sensitivity to systematic risks. This has far- reaching consequences for risk management, pricing and regulatory capital requirements. A simple analytical valuation model based on the CAPM and the single-factor Merton model is used in order to keep the model framework simple. -

Property/Liability Insurance Risk Management and Securitization

PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Biography Trent R. Vaughn, FCAS, MAAA, is Vice President of Actuarial/Pricing at GRE Insurance Group in Keene, NH. Mr. Vaughn is a 1990 graduate of Central College in Pella, Iowa. He is also the author of a recent Proceedings paper and has been a member of the CAS Examination Committee since 1996. Acknowledgments The author would like to thank an anonymous reviewer from the CAS Continuing Education Committee for his or her helpful comments. PROPERTY/LIABILITY INSURANCE RISK MANAGEMENT AND SECURITIZATION Abstract This paper presents a comprehensive framework for property/liability insurance risk management and securitization. Section 2 presents a rationale for P/L insurance risk management. Sections 3 through 6 describe and evaluate the four categories of P/L insurance risk management techniques: (1) maintaining internal capital within the organization, (2) managing asset risk, (3) managing underwriting risk, and (4) managing the covariance between asset and liability returns. Securitization is specifically discussed as a potential method of managing underwriting risk. Lastly, Section 7 outlines four key guidelines for cost- effective risk management. 1. INTRODUCTION In recent years, the property-liability insurance industry has witnessed intense competition from alternative risk management techniques, such as large deductibles and retentions, risk retention groups, and captive insurance companies. Moreover, the next decade promises to bring additional competition from new players in the P/L insurance industry, including commercial banks and securities firms. In order to survive in this competitive new landscape, P/L insurers must manage total risk in a cost-efficient manner. This paper provides a rationale for P/L insurance risk management, then describes four categories of risk management techniques utilized by insurers. -

Diversification and Discussion of Risk

Diversification and Discussion of Risk Conference of the County Investment Academy San Antonio June 2019 PFIA 2256.008c Requires Training in: • Investment Diversification 2 Capital Market Theory 12.0% 10.0% 8.0% E( r) 6.0% P* * 4.0% 2.0% 0.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% Std. Dev. 3 Capital Market Theory • Points along the upper half of the curve represent the best risk/return diversified portfolios of risky assets • The straight line represents portfolios obtained by investing in the “optimal risky portfolio” (P*) and either lending or leveraging at the “risk‐free” rate. • Points on the line below the curve represent “lending” and points above represent “leveraging” (note increased “risk” as measured by standard deviation of returns!) 4 So in theory….. Key result? An undiversified portfolio yields inferior return for the level of risk! The same, or higher, return could be attained at a lower level of risk with a diversified portfolio. If you are not diversified, you are taking more risk than you can expect to be compensated for! 5 Diversification and Correlation of Returns Correlation, which measures the degree of “co‐ movement”, ranges from ‐1 to +1. When the correlation between returns is less than 1 there are diversification benefits—the risk of portfolio is less than the average of the risks of the individual assets. Which pair of stock returns is more correlated? Chevron, Exxon Chevron, Delta Airlines 6 International Diversification Correlations vs S&P 500: China 0.62 Korea 0.53 Japan 0.73 Germany 0.74 UK 0.73 Brazil 0.29 Chile 0.38 Monthly returns vs corresponding MSCI indexes (US dollar returns) 5 years ended April 2019 Source: FactSet 7 Global Market Capitalization Latin Canada 1% UK 3% Other 5% 1% Japan 8% Asia ex Japan 13% U.S. -

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk

Securities Loans Collateralized by Cash: Reinvestment Risk, Run Risk, and Incentive Issues Frank M. Keane Securities loans collateralized by cash are by far the most popular form of securities-lending transaction. But when the www.newyorkfed.org/research/current_issues F cash collateral associated with these transactions is actively reinvested by a lender’s agent, potential risks emerge. This 2013 F study argues that the standard compensation scheme for securities-lending agents, which typically provides for agents to share in gains but not losses, creates incentives for them to take excessive risk. It also highlights the need for greater scrutiny and understanding of cash reinvestment practices— especially in light of the AIG experience, which showed that Volume 19, Number 3 Volume risks related to cash reinvestment, by even a single participant, could have destabilizing effects. lthough less researched than the money markets, the collateral markets IN ECONOMICS AND FINANCE are critical to the efficiency of the asset markets—including the markets for ATreasury, agency, and agency mortgage-backed securities. Well-functioning collateral markets allow dealers and investors in the asset markets to finance short positions for the purposes of hedging, market making, settlement, and arbitrage. Two important mechanisms for accessing the U.S. money and collateral markets are repurchase agreements (repos) and securities-lending transactions. In a money market transaction, when cash and securities are exchanged, the securities act as collateral and mitigate the risks associated with a borrower’s failure to repay the cash. In a collateral market transaction, however, the cash serves as collateral and mitigates the risk associated with replacing the security if the borrower fails to return it. -

Is the Insurance Industry Systemically Risky?

Is the Insurance Industry Systemically Risky? Viral V Acharya and Matthew Richardson1 1 Authors are at New York University Stern School of Business. E-mail: [email protected], [email protected]. Some of this essay is based on “Systemic Risk and the Regulation of Insurance Companies”, by Viral V Acharya, John Biggs, Hanh Le, Matthew Richardson and Stephen Ryan, published as Chapter 9 in Regulating Wall Street: The Dodd-Frank Act and the Architecture of Global Finance, edited by Viral V Acharya, Thomas Cooley, Matthew Richardson and Ingo Walter, John Wiley & Sons, November 2010. [Type text] Is the Insurance Industry Systemically Risky? i VIRAL V ACHARYA AND MATTHEW RICHARDSON I. Introduction As a result of the financial crisis, the Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act and it was signed into law by President Obama on July 21, 2010. The Dodd-Frank Act did not create a new direct regulator of insurance but did impose on non-bank holding companies, possibly insurance entities, a major new and unknown form of regulation for those deemed “Systemically Important Financial Institutions” (SIFI) (sometimes denoted “Too Big To Fail” (TBTF)) or, presumably any entity which regulators believe represents a “contingent liability” for the federal government, in the event of severe stress or failure. In light of the financial crisis, and the somewhat benign changes to insurance regulation contained in the Dodd-Frank Act (regulation of SIFIs aside), how should a modern insurance regulatory structure be designed to deal with systemic risk? The economic theory of regulation is very clear. -

Multi-Factor Models and the Arbitrage Pricing Theory (APT)

Multi-Factor Models and the Arbitrage Pricing Theory (APT) Econ 471/571, F19 - Bollerslev APT 1 Introduction The empirical failures of the CAPM is not really that surprising ,! We had to make a number of strong and pretty unrealistic assumptions to arrive at the CAPM ,! All investors are rational, only care about mean and variance, have the same expectations, ... ,! Also, identifying and measuring the return on the market portfolio of all risky assets is difficult, if not impossible (Roll Critique) In this lecture series we will study an alternative approach to asset pricing called the Arbitrage Pricing Theory, or APT ,! The APT was originally developed in 1976 by Stephen A. Ross ,! The APT starts out by specifying a number of “systematic” risk factors ,! The only risk factor in the CAPM is the “market” Econ 471/571, F19 - Bollerslev APT 2 Introduction: Multiple Risk Factors Stocks in the same industry tend to move more closely together than stocks in different industries ,! European Banks (some old data): Source: BARRA Econ 471/571, F19 - Bollerslev APT 3 Introduction: Multiple Risk Factors Other common factors might also affect stocks within the same industry ,! The size effect at work within the banking industry (some old data): Source: BARRA ,! How does this compare to the CAPM tests that we just talked about? Econ 471/571, F19 - Bollerslev APT 4 Multiple Factors and the CAPM Suppose that there are only two fundamental sources of systematic risks, “technology” and “interest rate” risks Suppose that the return on asset i follows the -

Systematic Risk Influences a Large Number of Assets. a Significant Political Event, for Example, Could Affect Several of the Assets in Your Portfolio

Let's take a look at the two basic types of risk: Systematic Risk - Systematic risk influences a large number of assets. A significant political event, for example, could affect several of the assets in your portfolio. It is virtually impossible to protect yourself against this type of risk. Unsystematic Risk - Unsystematic risk is sometimes referred to as "specific risk". This kind of risk affects a very small number of assets. An example is news that affects a specific stock such as a sudden strike by employees. Diversification is the only way to protect yourself from unsystematic risk. What is 'Systematic Risk'? The risk inherent to the entire market or an entire market segment. Systematic risk, also known as “undiversifiable risk,” “volatility” or “market risk,” affects the overall market, not just a particular stock or industry. This type of risk is both unpredictable and impossible to completely avoid. It cannot be mitigated through diversification, only through hedging or by using the right asset allocation strategy. For example, putting some assets in bonds and other assets in stocks can mitigate systematic risk because an interest rate shift that makes bonds less valuable will tend to make stocks more valuable, and vice versa, thus limiting the overall change in the portfolio’s value from systematic changes. Interest rate changes, inflation, recessions and wars all represent sources of systematic risk because they affect the entire market. Systematic risk underlies all other investment risks. The Great Recession provides a prime example of systematic risk. Anyone who was invested in the market in 2008 saw the values of their investments change because of this market-wide economic event, regardless of what types of securities they held. -

The Volatility of Industrial Stock Returns and an Empirical Test of Arbitrage Pricing Theory

Rev. Integr. Bus. Econ. Res. Vol 4(2) 254 The Volatility of Industrial Stock Returns and An Empirical Test of Arbitrage Pricing Theory Bahri Accounting Department of Politeknik Negeri Ujung Pandang ABSTRACT This study focused on the investigation of the sensitivity of industrial stock returns and empirical test of the model of arbitrage pricing theory (APT). Three issues were the basis of this study. The first issue was the difference in industrial stock returns volatility. The second issue was concerning the validity and robustness of CAPM as well as APT models. And, the third issue was the time-varying volatility with the phenomenon of structural breaks. This study used a nested model approach with the second-pass regression. Method of estimation using ordinary least squares method, ARCH/GARCH method, and the dummy variable method. This study used secondary data for the observation period January 2003 to December 2010 in the Indonesian stock market. This investigation produced three empirical findings. First, there was no difference in sensitivity of industrial stock returns among sectors, based on systematic risk factors. Second, the testing of CAPM and APT multifactor models revealed inconsistent results in testing industrial stocks. But the model of CAPM seemed more valid and robust than APT multifactor was. Finally, there were differences in the risk premium for systematic risks caused by the structural break during the financial crisis in 2008. Keywords: Arbitrage pricing theory, industrial stock return volatility, systematic risk factors, structural-breaks 1. INTRODUCTION Investments are current expenditures of investors to expect a return in the future. There is a variety of investment options for investors; one of them is an investment in common stock. -

Modern Portfolio Theory

Modern portfolio theory “Portfolio analysis” redirects here. For theorems about where Rp is the return on the port- the mean-variance efficient frontier, see Mutual fund folio, Ri is the return on asset i and separation theorem. For non-mean-variance portfolio wi is the weighting of component analysis, see Marginal conditional stochastic dominance. asset i (that is, the proportion of as- set “i” in the portfolio). Modern portfolio theory (MPT), or mean-variance • Portfolio return variance: analysis, is a mathematical framework for assembling a P σ2 = w2σ2 + portfolio of assets such that the expected return is maxi- Pp P i i i w w σ σ ρ , mized for a given level of risk, defined as variance. Its key i j=6 i i j i j ij insight is that an asset’s risk and return should not be as- where σ is the (sample) standard sessed by itself, but by how it contributes to a portfolio’s deviation of the periodic returns on overall risk and return. an asset, and ρij is the correlation coefficient between the returns on Economist Harry Markowitz introduced MPT in a 1952 [1] assets i and j. Alternatively the ex- essay, for which he was later awarded a Nobel Prize in pression can be written as: economics. P P 2 σp = i j wiwjσiσjρij , where ρij = 1 for i = j , or P P 1 Mathematical model 2 σp = i j wiwjσij , where σij = σiσjρij is the (sam- 1.1 Risk and expected return ple) covariance of the periodic re- turns on the two assets, or alterna- MPT assumes that investors are risk averse, meaning that tively denoted as σ(i; j) , covij or given two portfolios that offer the same expected return, cov(i; j) .