Stoxx® Europe Total Market Financial Services Index

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

COVID-19 Proxy Governance Update

COVID-19 Proxy Governance Update 2020 AGM mid-season review FROM EQUINITI 01 Looking back and planning ahead It is incredible to note that it has been over 12 weeks since the official announcement on 23 March of the UK Government’s Stay at Home Measures, and nearly seven months since the severity of the pandemic became apparent in China. Over the said period, PLC boards, company secretaries and investor relations officers have kept their corporate calendars going thanks to rapid adoption of modified regulatory guidelines and inventive modes of engagement with investors. With annual general meetings being an obvious highlight in the corporate calendar, we take stock of the progress made so far over the 2020 AGM season, as well as using what we learned to plan ahead. Now that we are over the first ‘hump’ with the busy period of May AGMs out of the way, we are readying for the second ‘peak’ of June and July AGMs, and then an ‘easing’ until the second ‘mini’ season in the early autumn. As such, in this update, we look at: • 2020 AGM season statistics…so far • Proxy adviser engagement and ISS recommendations review • High-level assumptions for Q3 and Q4 • Relevant updates from the regulators, industry bodies and proxy advisers • Communications in the COVID-19 world – special commentary by leading financial PR firm,Camarco • How has COVID-19 impacted activism – special commentary by international law firm,White & Case 02 2020 AGM Season Statistics…so far Scope of data To assess progress and forecast what is to come, we look at the key statistics for the UK AGM season 2020 thus far. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

The Sectors Which Recover Quickest from a Sell-Off

VOL 21 / ISSUE 43 / 31 OCTOBER 2019 / £4.49 BOUNCING BACK THE SECTORS WHICH RECOVER QUICKEST FROM A SELL-OFF... AND STAND TALLEST IN A DOWNTURN GLAXOSMITHKLINE WHY ALTERNATIVE FUNDS EXPOSED TRANSFORMED BY ASSETS ARE IN TO HIGH-RISK NEW STRATEGY DEMAND DIVIDENDS EDITOR’S VIEW Why stewardship really matters with investing A new code draws the spotlight on how big investors engage with companies he introduction of a new UK Stewardship in the eyes of the wider public has to be a good Code by the Financial Reporting Council thing, particularly if it opens people’s eyes to the T will look to raise the bar on how big opportunities provided by putting their cash to investors hold the companies in which they invest work in the markets. to account. A lot of the headlines around the news focused DON’T LOSE SIGHT OF UK STRENGTHS on the climate change angle but there is more to In fairness, if it wanted to distract from its own the code than environmental concerns, including shortcomings, the investment world could easily how institutions make their decisions and what point to failures of stewardship among the political they are doing about issues such as governance class in the UK. and diversity. As we write the country remains mired in a Brexit Fundamentally this is about recognising that stalemate with the potential joys of a Christmas investors are part-owners of a business. Even big election. Companies and markets are still denied asset managers are sometimes guilty of buying the clarity on the UK’s future relationship with the shares and seeing their work as done. -

Finn-Ancial Times Finncap Financials & Insurance Quarterly Sector Note

finn-ancial Times finnCap Financials & Insurance quarterly sector note Q3 2020 | Issue 9 Highlights this quarter: Elevated uncertainty and volatility have been hallmarks of the last 18 months, with Brexit, the UK General Election and more recently COVID-19 all contributing to the challenges that face investors wishing to carve out solid and stable returns amid these ‘unprecedented’ times. With this is mind, and simulating finnCap’s proven Slide Rule methodology, we found the highest quality and lowest value stocks across the financials space, assessing how the make-up of these lists changed over the period January 2019 to July 2020, tracking indexed share price performance over the period as well as movements in P/E and EV/EBIT valuations. The top quartile list of Quality companies outperformed both the Value list and the FTSE All Share by rising +2.5% over the period versus -5.4% for the All Share and -14.3% for Value stocks. Furthermore, the Quality list had protection on the downside in the market crash between February and March 2020, and accelerated faster amid the market rally between late March and July 2020. From high to low (January to March), Quality moved -36.3% against the Value list at -45.5%, while a move off the lows to July was +37.4% for Quality and +34.0% for Value. There was some crossover between the Quality and Value lists, with 7 companies of the top quartile (16 companies in total) appearing in both the Quality and Value lists. This meant that a) investors could capture what we call ‘Quality at Value’ (i.e. -

FTSE Factsheet

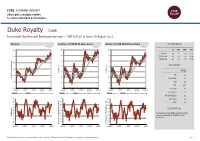

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Duke Royalty DUKE Investment Banking and Brokerage Services — GBP 0.4125 at close 10 August 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 10-Aug-2021 10-Aug-2021 10-Aug-2021 0.45 140 140 1D WTD MTD YTD Absolute -2.4 -1.2 -1.8 35.2 130 130 0.4 Rel.Sector -2.4 -0.5 -3.6 25.9 Rel.Market -2.8 -1.7 -3.7 20.9 120 120 0.35 VALUATION 110 110 0.3 Trailing 100 100 Relative Price Relative Price Relative 0.25 PE -ve Absolute Price (local (local currency) AbsolutePrice 90 90 EV/EBITDA -ve 0.2 80 80 PB 2.0 PCF 28.1 0.15 70 70 Div Yield 4.6 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Price/Sales -ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.2 90 90 90 Div Payout -ve 80 80 80 ROE -ve 70 70 70 Share Index) Share Share Sector) Share - 60 - 60 60 DESCRIPTION 50 50 50 40 40 The Company is a globally focused investment 40 RSI RSI (Absolute) 30 30 company specialising in diversified royalty investment. -

Annual Report and Accounts 2019

TP ICAP Annual Report and Accounts 2019 Annual Report and Accounts 2019 We provide access to global Contents financial and commodities Strategic report: Financial and strategic highlights 1 At a glance 2 markets, improving price Our business model 4 Chairman’s statement 6 discovery, flow of liquidity Chief Executive Officer’s review 8 Market factors 13 Strategy 14 and distribution of data, Case studies 15 Key performance indicators 18 working with and supporting Financial and operating review 20 Viability statement and the communities in which we going concern 33 Risk management 34 Principal risks and uncertainties 36 operate and facilitating Resources, relationships economic growth. and responsibilities 40 Governance report: Compliance with the UK Corporate Code 2018 46 Chairman’s introduction > Our brokers match buyers and sellers of financial, to governance 47 Board of Directors 50 energy and commodities products and facilitate Corporate governance report 52 price discovery, execution and risk management. How the Board has satisfied its section 172 duty 57 Report of the Nominations > We provide independent data to participants in and Governance Committee 66 the financial, energy and commodities markets, Report of the Audit Committee 70 Report of the Risk Committee 75 including live and historical pricing content, Report of the Remuneration and advanced valuation and risk analytics. Committee 78 Directors’ report 100 > We are a trusted partner to our clients, enabling Statement of Directors’ Responsibilities 105 them to transact with -

Good and Bad News for Investors

STOCKS | FUNDS | INVESTMENT TRUSTS | PENSIONS AND SAVINGS VOL 19 / ISSUE 46 / 23 NOVEMBER 2017 / £4.49 SHARES WE MAKE INVESTING EASIER CAN YOUR HOME FUND YOUR RETIREMENT? Good and bad news for investors WHY DO 5 QUESTIONS COMPANIES DIGITAL DISRUPTION RAISED BY BUY BACK HOW TO INVEST IN GAME ZPG’S MOVE ON SHARES? CHANGING COMPANIES GOCOMPARE Fundsmith LLP (“Fundsmith”) is authorised and regulated by The Fundsmith Emerging Equities Trust the Financial Conduct Authority and only acts for the funds (FEET) research team searches the world to to whom it provides regulated investment management and find companies that make their money from a transaction arrangement services. Fundsmith does not act for or advise potential investors in connection with acquiring large number of everyday, repeat, predictable shares in Fundsmith Emerging Equities Trust plc and will not transactions and will benefit from the rise of the be responsible to potential investors for providing them with protections afforded to clients of Fundsmith. consumer in developing economies. Prospective investors are strongly advised to take their own For example, Indofood sold 9 billion packets of legal, investment and tax advice from independent and suitably qualified advisers. The value of investments may Indomie noodles last year, Magnit welcomed 11 million go up as well as down. Past performance is not a guide to shoppers a day, MercadoLibre sold over 50 million future performance. items on its website last quarter and Dabur’s Hajmola FEET Performance, % Total Return tablets were taken 26 million times a day in India. Year ending 31st August 2017 2016 2015 Since inception You may never have heard of them, despite their FEET Share Price +3.6 +21.5 -16.2 +15.5 scale, but all can be found in the FEET portfolio. -

Download Report

- † † Met target 3% On track Not on track 10% No data 45% 42% Increased Maintained 15% Decreased 14% 72% Targeted increase 23% 38% 31% 29% 2017 2018 Target • • • • • • • • • • • Met On target track On track 45% 4% 42% Not on track Above 18% No data Below 42% Not 58% on 78% track No 10% data 3% Insurance (20) 15 1 4 Global/investment banking (18) 15 1 2 UK banking (16) 14 1 1 Other* (14) 7 3 4 Professional services (12) 6 5 1 Investment management (11) 10 1 Building society/credit union (10) 5 3 2 Increased Fintech (9) 7 2 Maintained Government/regulator/trade 5 1 1 body (7) Decreased 47% Building society/credit union (10) 53% Government/regulator/trade body 44% (9) 51% 44% Other* (14) 46% 44% Professional services (15) 44% 36% Fintech (9) 42% 34% Average (123) 38% 30% UK banking (17) 34% 31% Insurance (20) 33% 26% Investment management (11) 30% 2017 22% Global/investment banking (18) 25% 2018 100% 90% Nearly two-thirds of signatories have a target of at least 33% 80% 70% 60% Above 50% 50% Parity (3) 40% 50:50 40% up to 30% 33% up to 50% 30% (31) 20% Up to 40% 30% (24) 10% (30) (23) (10) 0% 100% 80% 60% 40% 20% 0% Government/regulator/trade 41% body (5) 47% Fintech (4) 37% 48% Insurance (16) 32% 40% Professional services (5) 32% 38% UK banking (11) 32% 41% Building society/credit union 31% (2) 36% Average (67) 31% 38% Other* (4) 29% 35% Investment management (5) 27% 2018 33% Target Global/investment banking 25% (15) 29% Firms that have met or 47% exceeded their targets (54) 40% 31% 28% 15% 15% 11% % of firms % of 43 29 26 20 5 Number of -

Issue Country of Domicile GICS Sector Portfolio Weight (%) AJ BELL United

Issue Country of domicile GICS sector Portfolio weight (%) AJ BELL United Kingdom Financials 3.35% AVAST United Kingdom Information Technology 2.45% CAPITAL FOR COLLEAGUES United Kingdom Financials 0.03% CERES POWER HOLDINGS United Kingdom Industrials 0.76% COMPASS GROUP United Kingdom Consumer Discretionary 1.73% COUNTRYSIDE PROPERTIES United Kingdom Consumer Discretionary 3.84% CREST NICHOLSON HOLDINGS United Kingdom Consumer Discretionary 1.84% DFS FURNITURE United Kingdom Consumer Discretionary 3.08% DISTRIBUTION FINANCE CAPITAL United Kingdom Financials 0.70% ETHICAL PROPERTY CO United Kingdom Real Estate 0.06% FIRST DERIVATIVES United Kingdom Information Technology 2.00% GB GROUP United Kingdom Information Technology 2.58% GENUIT GROUP United Kingdom Industrials 1.04% GREENCOAT UK WIND United Kingdom Utilities 0.96% GYM GROUP United Kingdom Consumer Discretionary 2.75% HALMA United Kingdom Information Technology 2.74% HARGREAVES LANSDOWN United Kingdom Financials 3.53% HELIOS TOWERS United Kingdom Communication Services 2.93% HOME REIT United Kingdom Consumer Discretionary 0.88% INTERTEK GROUP United Kingdom Industrials 3.23% KINGSPAN GROUP Ireland Industrials 2.52% LEARNING TECHNOLOGIES GROUP United Kingdom Information Technology 4.01% LEGAL & GENERAL GROUP United Kingdom Financials 3.72% LONDON STOCK EXCHANGE GROUP United Kingdom Financials 3.78% MORTGAGE ADVICE BUREAU HOLDINGS United Kingdom Financials 1.57% NATIONAL EXPRESS GROUP United Kingdom Industrials 3.35% NATIONAL GRID United Kingdom Utilities 1.30% OXFORD INSTRUMENTS -

6 Cheap Stocks in an Expensive Market We Use Three Methods to Spot Rare Pockets of Value

STOCKS | FUNDS | INVESTMENT TRUSTS | PENSIONS AND SAVINGS VOL 19 / ISSUE 44 / 09 NOVEMBER 2017 / £4.49 SHARES WE MAKE INVESTING EASIER 6 CHEAP STOCKS IN AN EXPENSIVE MARKET WE USE THREE METHODS TO SPOT RARE POCKETS OF VALUE RETAIL INVESTORS LOSE OUT BIG TIME WITH IPOS SCOTTISH MORTGAGE PLEADS FOR PATIENCE INTEREST RATE HIKE: WHY EXPERTS DON’T EXPECT ANOTHER ONE SOON TO KNOW LOCAL COMPANIES, KEEP LOCAL COMPANY. LET’STALKHOW. FIDELITYCHINA That’s whyDaleNicholls, managerofFidelity ChinaSpecialSituations, andhis team of SPECIALSITUATIONSPLC researchersare basedinHongKongand Chinaischanging, presenting significantinvestment Shanghai. Theirlocal knowledgeand opportunitiesfor thosewho knowwhere to look. connectionsmakethemwell-placed to identifyand benefit fromvaluation anomalies Why? Well,the spendingpowerofagrowingand affluent as they arise. middle class is increasingly driving theeconomy. And governmentreforms supportthisshift to afocus on the So,ifyou’relooking forlocal knowledge-basedinvestment new consumer. in amarketthat’s toobig to ignore, take acloserlookat theUK’slargest Chinainvestmenttrust. In suchavastand complexmarket, youneed on-the- groundexpertise to take fulladvantage of thesechanges Please note thatpastperformanceisnot aguideto andthe resultingundervaluations, particularly of small and thefuture. Thevalue of investments cangodownaswell medium-sized companies,which can occur. as up andyou maynot get back theamountinvested. Overseas investments are subject to currency fluctuations. PAST PERFORMANCE Investments in small and emergingmarkets -

FOR SMALL CAP VALUE Why Fund Managers Are Cashing out of Star Performers Like Fevertree to Reinvest in Better Opportunities

STOCKS | FUNDS | INVESTMENT TRUSTS | PENSIONS AND SAVINGS VOL 19 / ISSUE 28 / 20 JULY 2017 / £4.49 SHARES WE MAKE INVESTING EASIER SEARCHING FOR SMALL CAP VALUE Why fund managers are cashing out of star performers like Fevertree to reinvest in better opportunities OUR GREAT ALL CHANGE IDEAS ARE at the top BEATING THE for EasyJet MARKET and ITV 14% AVERAGE GAIN CARILLION OVER 12 bounces back MONTHS from share price collapse FIVE WAYS TO BOOST YOUR RETIREMENT INCOME EDITOR’S VIEW Do the rewards compensate for the risks taken? We look at performance for investors risking their money in the mining sector hareholders in miner Rio Tinto (RIO) have for half of the year; sustaining that trend for enjoyed a 12.3% total return so far this year. the rest of 2017 would imply a 24% return on S While more than twice the total return an annualised basis. Therefore you are being from the FTSE 100 index (5.6%), is such a reward adequately compensated in this situation for the adequate to compensate for the risks involved with risk of investing in mining, in my opinion. investing in such a volatile sector? Just remember that past performance doesn’t Investors should always think about the ‘equity always equate to future performance – you aren’t risk premium’ when establishing the desired return guaranteed to make that extra 12% in the second from putting money in a certain sector. That is the half of the year. extra return you hope to generate on top of the ‘risk-free’ rate, which in the UK is benchmarked WHY INVEST IN RIO? against the UK 10-year government bond (aka gilt).