Creating the World's Largest Interdealer Broker

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Finn-Ancial Times Finncap Financials & Insurance Quarterly Sector Note

finn-ancial Times finnCap Financials & Insurance quarterly sector note Q3 2020 | Issue 9 Highlights this quarter: Elevated uncertainty and volatility have been hallmarks of the last 18 months, with Brexit, the UK General Election and more recently COVID-19 all contributing to the challenges that face investors wishing to carve out solid and stable returns amid these ‘unprecedented’ times. With this is mind, and simulating finnCap’s proven Slide Rule methodology, we found the highest quality and lowest value stocks across the financials space, assessing how the make-up of these lists changed over the period January 2019 to July 2020, tracking indexed share price performance over the period as well as movements in P/E and EV/EBIT valuations. The top quartile list of Quality companies outperformed both the Value list and the FTSE All Share by rising +2.5% over the period versus -5.4% for the All Share and -14.3% for Value stocks. Furthermore, the Quality list had protection on the downside in the market crash between February and March 2020, and accelerated faster amid the market rally between late March and July 2020. From high to low (January to March), Quality moved -36.3% against the Value list at -45.5%, while a move off the lows to July was +37.4% for Quality and +34.0% for Value. There was some crossover between the Quality and Value lists, with 7 companies of the top quartile (16 companies in total) appearing in both the Quality and Value lists. This meant that a) investors could capture what we call ‘Quality at Value’ (i.e. -

FTSE Factsheet

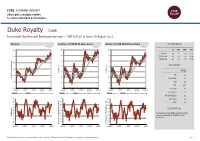

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Duke Royalty DUKE Investment Banking and Brokerage Services — GBP 0.4125 at close 10 August 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 10-Aug-2021 10-Aug-2021 10-Aug-2021 0.45 140 140 1D WTD MTD YTD Absolute -2.4 -1.2 -1.8 35.2 130 130 0.4 Rel.Sector -2.4 -0.5 -3.6 25.9 Rel.Market -2.8 -1.7 -3.7 20.9 120 120 0.35 VALUATION 110 110 0.3 Trailing 100 100 Relative Price Relative Price Relative 0.25 PE -ve Absolute Price (local (local currency) AbsolutePrice 90 90 EV/EBITDA -ve 0.2 80 80 PB 2.0 PCF 28.1 0.15 70 70 Div Yield 4.6 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Price/Sales -ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.2 90 90 90 Div Payout -ve 80 80 80 ROE -ve 70 70 70 Share Index) Share Share Sector) Share - 60 - 60 60 DESCRIPTION 50 50 50 40 40 The Company is a globally focused investment 40 RSI RSI (Absolute) 30 30 company specialising in diversified royalty investment. -

Annual Report and Accounts 2019

TP ICAP Annual Report and Accounts 2019 Annual Report and Accounts 2019 We provide access to global Contents financial and commodities Strategic report: Financial and strategic highlights 1 At a glance 2 markets, improving price Our business model 4 Chairman’s statement 6 discovery, flow of liquidity Chief Executive Officer’s review 8 Market factors 13 Strategy 14 and distribution of data, Case studies 15 Key performance indicators 18 working with and supporting Financial and operating review 20 Viability statement and the communities in which we going concern 33 Risk management 34 Principal risks and uncertainties 36 operate and facilitating Resources, relationships economic growth. and responsibilities 40 Governance report: Compliance with the UK Corporate Code 2018 46 Chairman’s introduction > Our brokers match buyers and sellers of financial, to governance 47 Board of Directors 50 energy and commodities products and facilitate Corporate governance report 52 price discovery, execution and risk management. How the Board has satisfied its section 172 duty 57 Report of the Nominations > We provide independent data to participants in and Governance Committee 66 the financial, energy and commodities markets, Report of the Audit Committee 70 Report of the Risk Committee 75 including live and historical pricing content, Report of the Remuneration and advanced valuation and risk analytics. Committee 78 Directors’ report 100 > We are a trusted partner to our clients, enabling Statement of Directors’ Responsibilities 105 them to transact with -

Stoxx® Europe Total Market Financial Services Index

STOXX® EUROPE TOTAL MARKET FINANCIAL SERVICES INDEX Components1 Company Supersector Country Weight (%) LONDON STOCK EXCHANGE Financial Services GB 10.21 DEUTSCHE BOERSE Financial Services DE 9.72 INVESTOR B Financial Services SE 8.23 PARTNERS GRP HLDG Financial Services CH 5.46 3I GROUP PLC. Financial Services GB 4.58 STANDARD LIFE ABERDEEN Financial Services GB 3.39 EXOR NV Financial Services IT 2.91 INVESTOR A Financial Services SE 2.82 GRP BRUXELLES LAMBERT Financial Services BE 2.74 M&G Financial Services GB 2.63 HARGREAVES LANSDOWN Financial Services GB 2.32 INTERMEDIATE CAPITAL GRP Financial Services GB 2.01 KINNEVIK B Financial Services SE 1.93 SCHRODERS Financial Services GB 1.68 AMUNDI Financial Services FR 1.54 EURONEXT Financial Services FR 1.41 INDUSTRIVARDEN A Financial Services SE 1.37 INDUSTRIVARDEN C Financial Services SE 1.32 INVESTEC Financial Services GB 1.24 WENDEL Financial Services FR 1.20 QUILTER Financial Services GB 1.17 ACKERMANS & VAN HAAREN Financial Services BE 1.14 SOFINA Financial Services BE 1.09 IG GRP HLDG Financial Services GB 1.08 MAN GRP Financial Services GB 1.04 PARGESA Financial Services CH 1.01 TP ICAP Financial Services GB 0.98 EURAZEO Financial Services FR 0.98 ASHMORE GRP Financial Services GB 0.97 BOLSAS Y MERCADOS ESPANOLES Financial Services ES 0.93 GRENKE N Financial Services DE 0.92 AZIMUT HLDG Financial Services IT 0.84 ONESAVINGS BANK Financial Services GB 0.80 JUPITER FUND MANAGEMENT Financial Services GB 0.79 JOHN LAING GROUP Financial Services GB 0.78 LATOUR INVESTMENT B Financial -

Stoxx® Europe Ipo (60 Months) Index

STOXX® EUROPE IPO (60 MONTHS) INDEX Components1 Company Supersector Country Weight (%) CELLNEX TELECOM Telecommunications ES 6.13 DELIVERY HERO Retail DE 5.29 JUST EAT TAKEAWAY.COM NV Retail NL 5.21 SCOUT24 Technology DE 3.41 COVESTRO Chemicals DE 2.72 AUTO TRADER GROUP Media GB 2.50 HELLOFRESH AG Retail DE 2.18 AMUNDI Financial Services FR 2.08 KOJAMO OYJ Real Estate FI 2.00 GALENICA SANTE AG Retail CH 1.92 VAT GROUP AG Industrial Goods & Services CH 1.91 ASR NEDERLAND NV Insurance NL 1.79 SIG COMBIBLOC GROUP AG Industrial Goods & Services CH 1.72 CONVATEC PLC Health Care GB 1.70 SIGNIFY Industrial Goods & Services NL 1.54 NEXI SPA Industrial Goods & Services IT 1.50 TEAMVIEWER AG Technology DE 1.49 INWIT Telecommunications IT 1.43 AVAST PLC Technology GB 1.41 LA FRANCAISE DES JEUX Travel & Leisure FR 1.28 STADLER RAIL AG Industrial Goods & Services CH 1.19 BAWAG GROUP AG Banks AT 1.05 NETCOMPANY GROUP AS Technology DK 1.03 SOFTCAT Technology GB 0.89 PIRELLI & C. S.P.A. Automobiles & Parts IT 0.89 COUNTRYSIDE PROPERTIES PLC Personal & Household Goods GB 0.88 LANDIS GYR GROUP AG Industrial Goods & Services CH 0.86 INTEGRAFIN HOLDINGS PLC Financial Services GB 0.81 DOMETIC GROUP AB Personal & Household Goods SE 0.77 BRAVIDA HOLDING AB Industrial Goods & Services SE 0.72 SILTRONIC Technology DE 0.69 TRAINLINE PLC Travel & Leisure GB 0.68 SPIE Industrial Goods & Services FR 0.68 INTERTRUST NV Financial Services NL 0.68 ZUR ROSE GROUP Retail CH 0.66 ASCENTIAL PLC Media GB 0.64 SINCH Technology SE 0.64 Virgin Money UK Banks GB 0.62 HASTINGS -

Sanne Group Plc Annual Report and Accounts 2020 1 Sanne at a Glance

Annual Report and Accounts 2020 Sanne is a leading global provider of alternative asset and corporate services. Contents 01 03 04 Introduction Governance Financial Statements 01 Financial and operational highlights of 56 Chairman’s Introduction 110 Independent Auditors' Report YMJ^JFW 58 Corporate Governance Report 118 Consolidated Income Statement 02 Sanne at a glance 60 Board of Directors 119 Consolidated Statement of Comprehensive Income 62 Sanne’s Executive Committee 120 Consolidated Balance Sheet 02 63 Leadership 121 Consolidated Statement of Changes in Equity 64 Board Effectiveness Strategic Report 122 Consolidated Cash Flow Statement 70 Directors’ Report 123 Notes to the Consolidated 06 Chairman’s Statement 74 Nomination and Governance Financial Statements Committee Report 08 Chief Executive Officer’s Statement 171 Glossary of Terms 77 Audit Committee Report 12 Value Chain 173 Shareholder and Corporate Information 82 Risk Committee Report 14 Business Model 85 Directors’ Remuneration at-a-glance 16 Our Stakeholders 86 Remuneration Committee Report 20 Strategy Review 97 Annual Report on Remuneration 24 Key Performance Indicators 107 Directors’ Responsibilities Statement 28 Segmental Review 30 Chief Financial Officer’s Review 34 Alternative Performance Measure definitions 36 ESG and Sustainability 46 Risk Management 52 Viability Statement www.sannegroup.com/annualreport Introduction Strategic Report Governance Financial Statements Financial and operational highlights of the year Robust financial performance, 2 1 with strong profit -

Notice of the 2019 Annual General Meeting of TP ICAP Plc to Be

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to the action you should take, please take advice immediately from an independent professional adviser authorised under the Financial Services and Markets Act 2000. If you have sold or otherwise transferred all of your shares, please send this document, together with the accompanying documents, at once to the purchaser or transferee, or to the stockbroker, bank or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. Notice of the 2019 Annual General Meeting of TP ICAP plc to be held on Wednesday 15 May 2019 at 12.45pm (BST) at the offices of Allen & Overy LLP, One Bishops Square, London E1 6AD TP ICAP plc Registered in England and Wales no. 5807599 TP ICAP plc Registered in England and Wales no. 5807599 9 April 2019 Dear shareholder, On behalf of the Directors of TP ICAP plc (together the ‘Directors’), it gives me great pleasure to invite you to attend the Annual General Meeting (or ‘AGM’) of TP ICAP plc (the ‘Company’) which will be held at the offices of Allen & Overy LLP, One Bishops Square, London E1 6AD on Wednesday 15 May 2019 at 12.45pm (BST). Notice of AGM The formal Notice of AGM is set out on the following pages of this document, detailing the resolutions that the shareholders are being asked to vote on along with explanatory notes of the business to be conducted at the AGM. The AGM provides shareholders with an opportunity to communicate with the Directors and we welcome your participation. -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 30 January 2020 AA AA. Support Services — GBP 0.4766 at close 30 January 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 30-Jan-2020 30-Jan-2020 30-Jan-2020 1 120 120 1D WTD MTD YTD Absolute -4.2 -9.3 -18.0 -18.0 110 110 0.9 Rel.Sector -3.4 -7.9 -18.2 -18.2 Rel.Market -3.0 -6.9 -16.2 -16.2 100 100 0.8 90 90 VALUATION 0.7 80 80 Trailing RelativePrice RelativePrice 70 70 0.6 PE 8.5 Absolute Price (local (local Absolute currency)Price 60 60 EV/EBITDA 9.2 0.5 PB -ve 50 50 PCF 2.7 0.4 40 40 Div Yield 3.4 Jan-2019 Apr-2019 Jul-2019 Oct-2019 Jan-2019 Apr-2019 Jul-2019 Oct-2019 Jan-2019 Apr-2019 Jul-2019 Oct-2019 Price/Sales 0.4 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity - 100 90 90 Div Payout 28.6 90 80 80 ROE - 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 40 The principal activity of the Company is providing 40 RSI RSI (Absolute) service of consumer roadside assistance. 30 30 30 20 20 20 10 10 10 RSI (Relative to FTSE UKFTSE All to RSI (Relative RSI (Relative to FTSE UKFTSE All to RSI (Relative 0 0 0 Jan-2019 Mar-2019 May-2019 Jul-2019 Sep-2019 Nov-2019 Jan-2019 Mar-2019 May-2019 Jul-2019 Sep-2019 Nov-2019 Jan-2019 Mar-2019 May-2019 Jul-2019 Sep-2019 Nov-2019 See final page and http://www.londonstockexchange.com/prices-and-markets/stocks/services-stock/ftse-note.htm for further details. -

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 1 of 137 Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 2 of 137 Exhibit A Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 3 of 137 Exhibit A1 Served via Overnight Mail Name Attention Address 1 Address 2 City State Zip Country Aastha Broadcasting Network Limited Attn: Legal Unit213 MezzanineFl Morya LandMark1 Off Link Road, Andheri (West) Mumbai 400053 IN Abs Global LTD Attn: Legal O'Hara House 3 Bermudiana Road Hamilton HM08 BM Abs-Cbn Global Limited Attn: Legal Mother Ignacia Quezon City Manila PH Aditya Jain S/O Sudhir Kumar Jain Attn: Legal 12, Printing Press Area behind Punjab Kesari Wazirpur Delhi 110035 IN AdminNacinl TelecomunicacionUruguay Complejo Torre De Telecomuniciones Guatemala 1075. Nivel 22 HojaDeEntrada 1000007292 5000009660 Montevideo CP 11800 UY Advert Bereau Company Limited Attn: Legal East Legon Ars Obojo Road Asafoatse Accra GH Africa Digital Network Limited c/o Nation Media Group Nation Centre 7th Floor Kimathi St PO Box 28753-00100 Nairobi KE Africa Media Group Limited Attn: Legal Jamhuri/Zaramo Streets Dar Es Salaam TZ Africa Mobile Network Communication Attn: Legal 2 Jide Close, Idimu Council Alimosho Lagos NG Africa Mobile Networks Cameroon Attn: Legal 131Rue1221 Entree Des Hydrocarbures Derriere Star Land Hotel Bonapriso-Douala Douala CM Africa Mobile Networks Cameroon Attn: Legal BP12153 Bonapriso Douala CM Africa Mobile Networks Gb, -

Annual Report and Accounts for the Year Ended 31 December 2018 Sannegroup.Com Stock Code: SNN Code: Stock

a Sanne Group plc Group Sanne Annual Report for the year ended 31 December 2018 Annual Report and Accounts for the year ended 31 December 2018 sannegroup.com Stock code: SNN Sanne Group Plc AR2018 - Front.indd 3 08/04/2019 11:49:23 26236 8 April 2019 11:48 am Proof 13 Welcome to Sanne Group plc’s 2018 Annual Report and Accounts SANNE is a leading global provider of outsourced alternative asset and corporate services. We provide high quality administration, reporting and fiduciary services to the leading alternative asset managers, financial institutions, family offices and corporates. We service clients from 18 locations spread across the Americas, Europe, Africa and Asia- Pacific. Our dedicated asset class and market experts are supported by the latest industry technology, systems and accredited business processes. Sanne Group Plc AR2018 - Front.indd 4 08/04/2019 11:49:24 26236 8 April 2019 11:48 am Proof 13 Annual Report and Accounts for the year ended 2018 Stock code: SNN sannegroup.com notes-heading-level- one What you’ll find inside this report notes-heading-level-two notes-heading-level-three notes-heading-level-four SANNE operates across global markets and in a highly Introduction notes-strapline specialised industry, serving a wide range of alternative Investment Proposition 4 notes-text-body asset managers, financial institutions, family offices Operational Highlights 6 > notes-list-bullet and corporates. Chairman’s Statement 8 > notes-list-bespoke Chief Executive Officer’s Statement 10 − notes-list-dash Strategic Report d. notes-list-alpha Strategy 16 5. notes-list-number Investment Strategic KPIs 18 vi.