From Russia with Gas an Analysis of the Nord Stream Pipeline's Impact

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Economics of the Nord Stream Pipeline System

The Economics of the Nord Stream Pipeline System Chi Kong Chyong, Pierre Noël and David M. Reiner September 2010 CWPE 1051 & EPRG 1026 The Economics of the Nord Stream Pipeline System EPRG Working Paper 1026 Cambridge Working Paper in Economics 1051 Chi Kong Chyong, Pierre Noёl and David M. Reiner Abstract We calculate the total cost of building Nord Stream and compare its levelised unit transportation cost with the existing options to transport Russian gas to western Europe. We find that the unit cost of shipping through Nord Stream is clearly lower than using the Ukrainian route and is only slightly above shipping through the Yamal-Europe pipeline. Using a large-scale gas simulation model we find a positive economic value for Nord Stream under various scenarios of demand for Russian gas in Europe. We disaggregate the value of Nord Stream into project economics (cost advantage), strategic value (impact on Ukraine’s transit fee) and security of supply value (insurance against disruption of the Ukrainian transit corridor). The economic fundamentals account for the bulk of Nord Stream’s positive value in all our scenarios. Keywords Nord Stream, Russia, Europe, Ukraine, Natural gas, Pipeline, Gazprom JEL Classification L95, H43, C63 Contact [email protected] Publication September 2010 EPRG WORKING PAPER Financial Support ESRC TSEC 3 www.eprg.group.cam.ac.uk The Economics of the Nord Stream Pipeline System1 Chi Kong Chyong* Electricity Policy Research Group (EPRG), Judge Business School, University of Cambridge (PhD Candidate) Pierre Noёl EPRG, Judge Business School, University of Cambridge David M. Reiner EPRG, Judge Business School, University of Cambridge 1. -

Material Fact Statement on Certain Decisions of Issuer’S Board of Directors

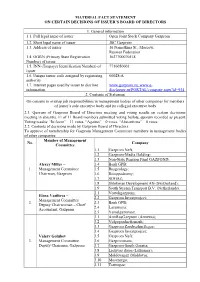

MATERIAL FACT STATEMENT ON CERTAIN DECISIONS OF ISSUER’S BOARD OF DIRECTORS 1. General information 1.1. Full legal name of issuer Open Joint Stock Company Gazprom 1.2. Short legal name of issuer JSC Gazprom 1.3. Address of issuer 16 Nametkina St., Moscow, Russian Federation 1.4. OGRN (Primary State Registration 1027700070518 Number) of issuer 1.5. INN (Taxpayer Identification Number) of 7736050003 issuer 1.6. Unique issuer code assigned by registering 00028-А authority 1.7. Internet pages used by issuer to disclose www.gazprom.ru; www.e- information disclosure.ru/PORTAL/company.aspx?id=934 2. Contents of Statement On consent to overlap job responsibilities in management bodies of other companies for members of issuer’s sole executive body and its collegial executive body 2.1. Quorum of Gazprom Board of Directors meeting and voting results on certain decisions: meeting in absentia, 11 of 11 Board members submitted voting ballots, quorum recorded as present. Voting results: “In favor” – 11 votes, “Against” – 0 votes, “Abstentions” – 0 votes. 2.2. Contents of decisions made by Gazprom Board of Directors: To approve of membership for Gazprom Management Committee members in management bodies of other companies: Member of Management No. Company Committee 1.1 Gazprom Neft; 1.2 Gazprom-Media Holding; 1.3 Non-State Pension Fund GAZFOND; Alexey Miller – 1.4 Bank GPB; 1. Management Committee 1.5 Rusgeology; Chairman, Gazprom 1.6 Rosippodromy; 1.7 SOGAZ; 1.8 Shtokman Development AG (Switzerland); 1.9 South Stream Transport B.V. (Netherlands). 2.1 Vostokgazprom; Elena Vasilieva – 2.2 Gazprom Investproject; Management Committee 2. -

Security Aspects of the South Stream Project

BRIEFING PAPER Policy Department External Policies SECURITY ASPECTS OF THE SOUTH STREAM PROJECT FOREIGN AFFAIRS October 2008 JANUARY 2004 EN This briefing paper was requested by the European Parliament's Committee on Foreign Affairs. It is published in the following language: English Author: Zeyno Baran, Director Center for Eurasian Policy (CEP), Hudson Institute www.hudson.org The author is grateful for the support of CEP Research Associates Onur Sazak and Emmet C. Tuohy as well as former CEP Research Assistant Rob A. Smith. Responsible Official: Levente Császi Directorate-General for External Policies of the Union Policy Department BD4 06 M 55 rue Wiertz B-1047 Brussels E-mail: [email protected] Publisher European Parliament Manuscript completed on 23 October 2008. The briefing paper is available on the Internet at http://www.europarl.europa.eu/activities/committees/studies.do?language=EN If you are unable to download the information you require, please request a paper copy by e-mail : [email protected] Brussels: European Parliament, 2008. Any opinions expressed in this document are the sole responsibility of the author and do not necessarily represent the official position of the European Parliament. © European Communities, 2008. Reproduction and translation, except for commercial purposes, are authorised, provided the source is acknowledged and provided the publisher is given prior notice and supplied with a copy of the publication. EXPO/B/AFET/2008/30 October 2008 PE 388.962 EN CONTENTS SECURITY ASPECTS OF THE SOUTH STREAM PROJECT ................................ ii EXECUTIVE SUMMARY .............................................................................................iii 1. INTRODUCTION......................................................................................................... 1 2. THE RUSSIAN CHALLENGE................................................................................... 2 2.1. -

Nord Stream 2

Updated August 24, 2021 Russia’s Nord Stream 2 Natural Gas Pipeline to Germany Nord Stream 2, a natural gas pipeline nearing completion, is which accounted for about 48% of EU natural gas imports expected to increase the volume of Russia’s natural gas in 2020. Russian gas exports to the EU were up 18% year- export capacity directly to Germany, bypassing Ukraine, on-year in the first quarter of 2021. Factors behind reliance Poland, and other transit states (Figure 1). Successive U.S. on Russian supply include diminishing European gas Administrations and Congresses have opposed Nord Stream supplies, commitments to reduce coal use, Russian 2, reflecting concerns about European dependence on investments in European infrastructure, Russian export Russian energy and the threat of increased Russian prices, and the perception of many Europeans that Russia aggression in Ukraine. The German government is a key remains a reliable supplier. proponent of the pipeline, which it says will be a reliable Figure 1. Nord Stream Gas Pipeline System source of natural gas as Germany is ending nuclear energy production and reducing coal use. Despite the Biden Administration’s stated opposition to Nord Stream 2, the Administration appears to have shifted its focus away from working to prevent the pipeline’s completion to mitigating the potential negative impacts of an operational pipeline. Some critics of this approach, including some Members of Congress and the Ukrainian and Polish governments, sharply criticized a U.S.-German joint statement on energy security, issued on July 21, 2021, which they perceived as indirectly affirming the pipeline’s completion. -

Brussels Admits EU Law Does Not Apply to Nord Stream 2 the European Commission Has Admitted There Is No Legal Ground to Apply Matter Before the End of the Year

Energy Reproduced with permission by Energy Intelligence for Oxford Institute of Energy Studies Intelligence Issue Vol.17, No. 186, Thursday, September 21, 2017 Vol. 17, No. 186 Thursday, September 21, 2017 Special Reprint from International Oil Daily for Oxford Institute of Energy Studies . Copyright © 2017 Energy Intelligence Group. Unauthorized copying, reproduc- ing or disseminating in any manner, in whole or in part, including through intranet or internet posting, or electronic forwarding even for internal use, is prohibited. Brussels Admits EU Law Does Not Apply to Nord Stream 2 The European Commission has admitted there is no legal ground to apply matter before the end of the year. EU energy laws to Gazprom’s Nord Stream 2 gas pipeline project despite its Observers believe Brussels’ mandate is plagued with problems, starting long-drawn opposition to the plan. with the fact that it would not ensure that Moscow must negotiate. PrintIn a Sep. 12 letter sent to a member of the European Parliament by the "If the commission does secure the mandate, it would acquire certain le- commission and leaked to the press, the commission’s legal service said gitimacy to negotiate, and it would be difficult for Russia to refuse entering that the application of the EU’s Third Energy Package regulations to off- negotiations; nonetheless Russia could still refuse to negotiate,” according shore import pipelines such as Nord Stream 2 "would raise specific legal to Katja Yafimava, senior research fellow at the Oxford Institute for Energy and practical questions, arising ... from the fact that Union rules cannot be Studies. Even if Russia does agree to negotiate, Yafimava doubts whether made unilaterally binding on the national authorities of third countries.” Moscow will accept the application of EU energy law to the project. -

Consolidated Financial Statements 2018

GAZPROM GERMANIA CONSOLIDATED FINANCIAL STATEMENTS 2018 www.gazprom-germania.de Consolidated Financial Statements 2018 GAZPROM Germania GmbH, Berlin Page 2 CONTENTS Contents ................................................................................................................................................. 2 Abbreviations ......................................................................................................................................... 5 Group management report ................................................................................................................... 7 Economic and regulatory conditions ................................................................................................... 7 General economic conditions .......................................................................................................... 7 Energy policy and regulatory environment ...................................................................................... 8 Business performance ......................................................................................................................... 9 Group performance ......................................................................................................................... 9 Marketing and trading business .................................................................................................... 10 Gas storage .................................................................................................................................. -

The Environmental Impacts of the P Nord Stream Gas Pipeline in The

The Environmental Impacts of the Nord Stream Gas Pipeline in the Baltic Sea Juha-Markku Leppänen SYKE Marine Research Centre Content Nord Stream is a natural gas pipeline through the Baltic Sea linking Russian gas fields to the central Europe . The Nord Stream ggpppjas pipeline project . Environmental concerns . Environmental Impact Assessments . Permitting process . CoConstructionnstruction . First results of the environmental monitoring The Nord Stream gas pipeline project . Most extensive single construction in the Baltic Sea . Total length of 1124 km . 2 parallel pipelines . 55 billion m3 gas per year . Total investment of 7, 4 billion € Construction Monitor . First pipeline completed . Second pipeline to be ready in 2012 Main environmental concerns before the construction . Physical damage to the seabed • Increase in water turbidity • Release of nutrients and hazardous substances • Impacts on bottom currents . Dumped munitions and barrels • leakage, poisoning . MitiMunitions cl earance • sediment disturbance • fish,,, seals, birds... Ship wrecks and other cultural heritage . Scientific heritage . Nature reserves . Fisheries, maritime transport, safety Permitting process before commencement of the construction . The pi peli ne passes th e t errit ori al wat ers or EEZ of Russia, Finland, Sweden, Denmark and Germany . Espoo Convention: Convention on Environmental Impact Assessment in a Transboundary Context requires • Contracting Parties to notify and consult each other on all major projects that might have adverse environmental impact across borders • Individual Parties to integrate environmental assessment into the plans and programmes at the earliest stages • RiRussia no tCttiPttEt a Contracting Party to Espoo Concen tion Permitting process before commencement of the construction . TbdTransboundary const ttidtbdruction and transboundary impacts require both national and international permitting processes . -

Germany - Regulatory Reform in Electricity, Gas, and Pharmacies 2004

Germany - Regulatory Reform in Electricity, Gas, and Pharmacies 2004 The Review is one of a series of country reports carried out under the OECD’s Regulatory Reform Programme, in response to the 1997 mandate by OECD Ministers. This report on regulatory reform in electricity, gas and pharmacies in Germany was principally prepared by Ms. Sally Van Siclen for the OECD. OECD REVIEWS OF REGULATORY REFORM REGULATORY REFORM IN GERMANY ELECTRICITY, GAS, AND PHARMACIES -- PART I -- ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT © OECD (2004). All rights reserved. 1 ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT Pursuant to Article 1 of the Convention signed in Paris on 14th December 1960, and which came into force on 30th September 1961, the Organisation for Economic Co-operation and Development (OECD) shall promote policies designed: • to achieve the highest sustainable economic growth and employment and a rising standard of living in Member countries, while maintaining financial stability, and thus to contribute to the development of the world economy; • to contribute to sound economic expansion in Member as well as non-member countries in the process of economic development; and • to contribute to the expansion of world trade on a multilateral, non-discriminatory basis in accordance with international obligations. The original Member countries of the OECD are Austria, Belgium, Canada, Denmark, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States. The following countries became Members subsequently through accession at the dates indicated hereafter: Japan (28th April 1964), Finland (28th January 1969), Australia (7th June 1971), New Zealand (29th May 1973), Mexico (18th May 1994), the Czech Republic (21st December 1995), Hungary (7th May 1996), Poland (22nd November 1996), Korea (12th December 1996) and the Slovak Republic (14th December 2000). -

Gazprom Germania, Gm&T and Wingas with Corporate Stand at E-World 2019

— PRESS RELEASE MORE ENERGY TOGETHER: GAZPROM GERMANIA, GM&T AND WINGAS WITH CORPORATE STAND AT E-WORLD 2019 Berlin/London/Kassel/Essen, 5 February 2019: Gazprom Marketing & Trading Ltd (GM&T) and WINGAS GmbH (WINGAS) welcome customers and counterparties to their jointly hosted stand at E-world 2019. As part of continued integration, the GAZPROM Germania Group, GM&T and WINGAS are developing commercial partnership to enhance their trading and marketing capabilities across Europe. At E-world 2019 WINGAS is presenting Customer Portal 2.0 with new transaction area for the first time. In the portal WINGAS customers will have the opportunity to exercise contractual options and to buy new products directly online. Mr. Daniel Gornig, the Director of Trading for the GAZPROM Germania Group emphasizes that: “GM&T and WINGAS’ commercial and support functions work together towards the same goals and objectives. What this last year has shown is that we are stronger together. The joint stand of GAZPROM Germania, WINGAS and GM&T is another sign of further integration of the marketing and trading activities within the Group.” Mr. Matthias Peter, the Head of the Marketing for the GAZPROM Germania Group said: “The objective of closer partnership between GM&T and WINGAS is to have a global reach while keeping a focus on the development of the important European gas markets and on the needs of every individual customer. In this context we are also continuously optimising WINGAS product and service portfolio.” E-world is Europe's largest energy trade fair and takes place from 05th till 07th February, 2019 in Essen. -

Nord Stream 2: Background, Objections, and Possible Outcomes Steven Pifer

NORD STREAM 2: BACKGROUND, OBJECTIONS, AND POSSIBLE OUTCOMES STEVEN PIFER APRIL 2021 EXECUTIVE SUMMARY Nord Stream 2 is an almost-finished natural gas pipeline from Russia to Germany. The Biden administration opposes it and has come under congressional pressure to invoke sanctions to prevent its completion, in large part because the pipeline seems a geopolitical project targeted at Ukraine. The German government, however, regards the pipeline as a “commercial project” and appears committed to its completion, perhaps in the next few months. U.S. sanctions applied on Russian entities to date have failed to stop Nord Stream 2, raising the question of whether the U.S. government would sanction German and other European companies for servicing or certifying the pipeline. Such sanctions would provoke controversy with Germany at a time when both Berlin and the Biden administration seek to rebuild good relations. The two sides have work to do if they wish to avoid Nord Stream 2 becoming a major point of U.S.-German contention. THE PIPELINE The European Union currently imports about 40% of its natural gas from Russia, or about one-third Nord Stream 2 is actually a pair of natural gas of its total gas consumption.4 Gazprom began pipelines that, if/when completed, will run some discussions with European companies on a direct 1,200 kilometers along the bottom of the Baltic Russia-Germany gas pipeline in 2001. At that time, 1 Sea from Ust-Luga, Russia to Greifswald, Germany. it shipped gas to western Europe via pipelines that The two pipelines, collectively referred to as Nord mainly transited Ukraine, and also Belarus and Stream 2, are projected to have the capacity to Poland (the Yamal system). -

Nord Stream 2 – Germany's Dilemma

NO. 32 APRIL 2021 Introduction Nord Stream 2 – Germany’s Dilemma Kirsten Westphal The Nord Stream 2 project presents the German government with the dilemma of choosing between energy and foreign policy interests. Geopolitical arguments often prevail in the political discourse. Yet, a weighing of priorities requires a look at the energy policy context, too. When it comes to balancing interests, there are no easy or “cheap” answers. With a focus on the energy context, it has to be emphasized that a cooperative approach toward energy transformation promises the greatest dividend for a balance of interests, but it presupposes a minimum consensus within the Euro- pean Union (EU), along with the United States (US), Ukraine, and Russia. By mid-April 2021, there were still nearly the German government to take a political 130 km missing from the Nord Stream 2 stance. pipeline (100 km in Denmark and 30 km in Germany), which stretches from Russia to Germany through the Baltic Sea and is built Foreign Policy Changes in two strings of 1,230 km each. US sanc- tions had halted construction work for more Nord Stream 2 was launched by Gazprom than a year starting in December 2019. and five European companies in 2015, one As a result of the sanctions, the continued year after the annexation of Crimea. In its construction, insurance, and certification dealings with the project, the German gov- of the pipeline is now a Russian matter. ernment took a fallback position early on, The package of US sanctions (Countering relying on existing German law and an eco- America’s Adversaries Through Sanctions nomic-technical position, and therefore it Act [CAATSA], the Protecting Europe’s classified the expansion of Nord Stream as a Energy Security Act [PEESA], and the Protect- commercial project. -

Nord Stream 2 and Turkstream – Update on New Us Sanctions

IG CIRCULAR – NORD STREAM 2 AND TURKSTREAM – UPDATE ON NEW U.S. SANCTIONS Nord Stream is a system of offshore natural gas pipelines from Russia to Germany. It includes two lines running from Vyborg to Greifswald forming the original Nord Stream (NS1), and two lines running from Ust-Luga to Greifswald termed Nord Stream 2 (NS2). NS1 is owned and operated by Nord Stream AG, whose majority shareholder is the Russian state company Gazprom, and NS2 is owned and will be operated by Nord Stream 2 AG, a wholly owned subsidiary of Gazprom. NS1 was completed on 8 October 2012. Work to lay NS2 took place between 2018–2019 but has been disrupted by US sanctions. Prior to the imposition of U.S. sanctions, it had been expected to become operational in mid-2020. TurkStream is a natural gas pipeline running from Russia to Turkey. It starts from Russkaya compressor station near Anapa in Russia crossing the Black Sea to the receiving terminal at Kıyıköy. Construction on TurkStream started in May 2017 and gas deliveries to Bulgaria via the pipeline began on 1 January 2020. This Circular concerns efforts by the United States to enhance the sanction provisions targeting the construction of the NS2 and TurkStream pipeline projects and those who provide vessels and services in connection with either project. The recent efforts are mainly focused on two pieces of legislation – the Countering America’s Adversaries Through Sanctions Act (CAATSA) and the Protecting Europe’s Energy Security Act (PEESA). While the wording in the CAATSA and PEESA sanction authorizations is different, both Acts have the potential to reach the activities of non-U.S.