Czech Republic in 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tariffs in Nordic Countries – Survey of Load Tariffs in DSO Grids

Tariffs in Nordic countries – survey of load tariffs in DSO grids Report 3/2015 Tariffs in Nordic countries – survey of load tariffs in DSO grids Nordic Energy Regulators 2015 Report 3/2015 NordREG c/o Danish Energy Regulatory Authority Valby 2500 Carl Jacobsens Vej 35 Denmark Telephone: + 45 41 71 54 00 Internet: www.nordicenergyregulators.org November 2015 2 Table of contents 1 Introduction ................................................................................... 7 1.1 Background – Why a survey of tariff design? ................................. 9 1.1.1 Technological change – smart grid and meters ..................... 9 1.1.2 Energy Efficiency Directive .................................................... 9 1.2 Seminar with stakeholders ............................................................10 1.3 Outline of the report ......................................................................11 2 The Nordic design of load tariffs ............................................... 12 2.1 Implementation of the Energy Efficiency Directive in the Nordic countries ................................................................................................12 2.1.1 Implementation of the directive in Denmark .........................12 2.1.2 Implementation of the directive in Finland ............................12 2.1.3 Implementation of the directive in Iceland ............................12 2.1.4 Implementation of the directive in Norway ............................12 2.1.5 Implementation of the directive in Sweden ...........................12 -

The Economics of the Nord Stream Pipeline System

The Economics of the Nord Stream Pipeline System Chi Kong Chyong, Pierre Noël and David M. Reiner September 2010 CWPE 1051 & EPRG 1026 The Economics of the Nord Stream Pipeline System EPRG Working Paper 1026 Cambridge Working Paper in Economics 1051 Chi Kong Chyong, Pierre Noёl and David M. Reiner Abstract We calculate the total cost of building Nord Stream and compare its levelised unit transportation cost with the existing options to transport Russian gas to western Europe. We find that the unit cost of shipping through Nord Stream is clearly lower than using the Ukrainian route and is only slightly above shipping through the Yamal-Europe pipeline. Using a large-scale gas simulation model we find a positive economic value for Nord Stream under various scenarios of demand for Russian gas in Europe. We disaggregate the value of Nord Stream into project economics (cost advantage), strategic value (impact on Ukraine’s transit fee) and security of supply value (insurance against disruption of the Ukrainian transit corridor). The economic fundamentals account for the bulk of Nord Stream’s positive value in all our scenarios. Keywords Nord Stream, Russia, Europe, Ukraine, Natural gas, Pipeline, Gazprom JEL Classification L95, H43, C63 Contact [email protected] Publication September 2010 EPRG WORKING PAPER Financial Support ESRC TSEC 3 www.eprg.group.cam.ac.uk The Economics of the Nord Stream Pipeline System1 Chi Kong Chyong* Electricity Policy Research Group (EPRG), Judge Business School, University of Cambridge (PhD Candidate) Pierre Noёl EPRG, Judge Business School, University of Cambridge David M. Reiner EPRG, Judge Business School, University of Cambridge 1. -

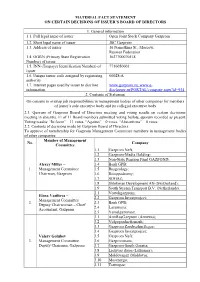

Material Fact Statement on Certain Decisions of Issuer’S Board of Directors

MATERIAL FACT STATEMENT ON CERTAIN DECISIONS OF ISSUER’S BOARD OF DIRECTORS 1. General information 1.1. Full legal name of issuer Open Joint Stock Company Gazprom 1.2. Short legal name of issuer JSC Gazprom 1.3. Address of issuer 16 Nametkina St., Moscow, Russian Federation 1.4. OGRN (Primary State Registration 1027700070518 Number) of issuer 1.5. INN (Taxpayer Identification Number) of 7736050003 issuer 1.6. Unique issuer code assigned by registering 00028-А authority 1.7. Internet pages used by issuer to disclose www.gazprom.ru; www.e- information disclosure.ru/PORTAL/company.aspx?id=934 2. Contents of Statement On consent to overlap job responsibilities in management bodies of other companies for members of issuer’s sole executive body and its collegial executive body 2.1. Quorum of Gazprom Board of Directors meeting and voting results on certain decisions: meeting in absentia, 11 of 11 Board members submitted voting ballots, quorum recorded as present. Voting results: “In favor” – 11 votes, “Against” – 0 votes, “Abstentions” – 0 votes. 2.2. Contents of decisions made by Gazprom Board of Directors: To approve of membership for Gazprom Management Committee members in management bodies of other companies: Member of Management No. Company Committee 1.1 Gazprom Neft; 1.2 Gazprom-Media Holding; 1.3 Non-State Pension Fund GAZFOND; Alexey Miller – 1.4 Bank GPB; 1. Management Committee 1.5 Rusgeology; Chairman, Gazprom 1.6 Rosippodromy; 1.7 SOGAZ; 1.8 Shtokman Development AG (Switzerland); 1.9 South Stream Transport B.V. (Netherlands). 2.1 Vostokgazprom; Elena Vasilieva – 2.2 Gazprom Investproject; Management Committee 2. -

UR Information Paper on Electricity Prices in Northern Ireland

EAI Response to Utility Regulator Information Paper on Electricity Prices in Northern Ireland Electricity Association of Ireland Energy and Environment Policy Committee 127 Baggot Street Lower Dublin 2 EU Transparency Register No: 400886110592-21 The Electricity Association of Ireland (EAI) is the trade association for the electricity industry on the island of Ireland, including generation, supply and distribution system operators. It is the local member of Eurelectric, the sector association representing the electricity industry at European level. EAI aims to contribute to the development of a sustainable and competitive electricity market on the island of Ireland. We believe this will be achieved through cost-reflective pricing and a stable investment environment within a framework of best-practice regulatory governance. Electricity Association of Ireland Tel: +353 1 5242726 www.eaireland.com 2 Contents INTRODUCTION AND SUMMARY ................................................................. 4 ABOUT ELECTRICITY PRICES ..................................................................... 4 The Wholesale Market ........................................................................................................................ 4 Market Redesign .................................................................................................................................. 5 Network Charges and Public Service Obligation ........................................................................ 5 COMMENTS ON THE INFORMATION PAPER ............................................. -

Czech Republic

June 2020 Czech Republic The OECD Inventory of Support Measures for Fossil Fuels identifies, documents and estimates direct budgetary support and tax expenditures supporting the production or consumption of fossil fuels in OECD countries, eight partner economies (Argentina, Brazil, the People’s Republic of China, Colombia, India, Indonesia, the Russian Federation, and South Africa) and EU Eastern Partnership (EaP) countries (Armenia, Azerbaijan, Belarus, Georgia, Moldova and Ukraine). Energy resources and market structure Total Primary Energy Supply* in 2018 The Czech Republic is the fourth-largest net electricity exporter in the EU in 2018, after France, Germany, and Sweden. Most of its Coal, 35% Geothermal, exports flow into Austria, the Slovak Republic solar & wind, and Germany. In 2018, electricity was mainly 1% generated from coal (50%) and nuclear energy Oil, 21% (34%). Small amounts of natural gas (4%) were used as a complement in multi-fired units and Biofuels & in peaking units. Roughly one-third of the waste, 10% Natural gas, 15% country’s electricity produced from coal is Nuclear, generated in combined-heat-and-power 18% plants. *excluding net electricity import Source: IEA In the Czech Republic, fossil fuels have always played a big role in the energy mix and still account for the bulk of total energy supply and domestic energy production. This is due to the substantial coal resources available in the country. Ostravsko-Karvinské Doly (OKD), the country’s sole hard-coal producer and one of the largest employers, operates four deep bituminous coal mines in the Moravian-Silesian Region. There have been ongoing re-organisation in the country’s mining industry in light of recent insolvency procedures in OKD, with the government announcing a gradual phasing out of mining by 2030 at the latest. -

Consolidated Financial Statements 2018

GAZPROM GERMANIA CONSOLIDATED FINANCIAL STATEMENTS 2018 www.gazprom-germania.de Consolidated Financial Statements 2018 GAZPROM Germania GmbH, Berlin Page 2 CONTENTS Contents ................................................................................................................................................. 2 Abbreviations ......................................................................................................................................... 5 Group management report ................................................................................................................... 7 Economic and regulatory conditions ................................................................................................... 7 General economic conditions .......................................................................................................... 7 Energy policy and regulatory environment ...................................................................................... 8 Business performance ......................................................................................................................... 9 Group performance ......................................................................................................................... 9 Marketing and trading business .................................................................................................... 10 Gas storage .................................................................................................................................. -

World Bank Document

Document of The World Bank FOR OFFICIAL USE ONLY Public Disclosure Authorized Report 1.a: 47748-A .J PROJECT APPRAISAL DOCUMENT ON A PROPOSED INTERNATIONAL BANK FOR RECONSTRUCTIONAND DEVELOPMENT Public Disclosure Authorized PARTIAL RISK GUARANTEE IN THE AMOUNT OF EURO 60 MILLION (USD 78 MILLION EQUIVALENT) FOR THE PRIVATIZATION OF THE POWER DISTRIBUTION SYSTEM OPERATOR OPERATOR1 I SISTEMIT TE SHPERNDARJES SHA (OSSH) Public Disclosure Authorized IN ALBANIA April 14,2009 Sustainable Development Department South East Europe Country Management Unit Europe and Central Asia Region Public Disclosure Authorized This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. CURRENCY EQUIVALENTS (Exchange Rate Effective February 2009) CurrencyUnit = Lek Lek 102 = US$1 US$1.3 = €1 CZK1 = US$0.04 FISCAL YEAR January 1 - December31 ABBREVIATIONS AND ACRONYMS AMM Albanian Market Model APL Adaptable Program Loan CAS Country Assistance Strategy COOP1 Cooperazione Internazionale - Italian Bilateral Aid Agency DSO Distribution System Operator EBRD European Bank for Reconstruction and Development EC European Commission ECSEE Energy Community of South East Europe EIB European Investment Bank EIRR Economic Internal Rate of Return EMP Environmental Management Plan ERE Electricity Regulatory Entity ETSO European Transmission System Operators EU European Union FDI Foreign Direct Investment GOA Government of Albania IAS International -

Gazprom Germania, Gm&T and Wingas with Corporate Stand at E-World 2019

— PRESS RELEASE MORE ENERGY TOGETHER: GAZPROM GERMANIA, GM&T AND WINGAS WITH CORPORATE STAND AT E-WORLD 2019 Berlin/London/Kassel/Essen, 5 February 2019: Gazprom Marketing & Trading Ltd (GM&T) and WINGAS GmbH (WINGAS) welcome customers and counterparties to their jointly hosted stand at E-world 2019. As part of continued integration, the GAZPROM Germania Group, GM&T and WINGAS are developing commercial partnership to enhance their trading and marketing capabilities across Europe. At E-world 2019 WINGAS is presenting Customer Portal 2.0 with new transaction area for the first time. In the portal WINGAS customers will have the opportunity to exercise contractual options and to buy new products directly online. Mr. Daniel Gornig, the Director of Trading for the GAZPROM Germania Group emphasizes that: “GM&T and WINGAS’ commercial and support functions work together towards the same goals and objectives. What this last year has shown is that we are stronger together. The joint stand of GAZPROM Germania, WINGAS and GM&T is another sign of further integration of the marketing and trading activities within the Group.” Mr. Matthias Peter, the Head of the Marketing for the GAZPROM Germania Group said: “The objective of closer partnership between GM&T and WINGAS is to have a global reach while keeping a focus on the development of the important European gas markets and on the needs of every individual customer. In this context we are also continuously optimising WINGAS product and service portfolio.” E-world is Europe's largest energy trade fair and takes place from 05th till 07th February, 2019 in Essen. -

The Commercial Deals Connected with Gazprom's Nord Stream 2

The commercial deals connected with Gazprom's Nord Stream 2 A review of strings and benefits attached to the controversial Russian pipelines Anke Schmidt-Felzmann, PhD Senior Researcher at the Research Centre of the General Jonas Žemaitis Military Academy of Lithuania Abstract This paper reviews the multiple strings and benefits attached to the single most controversial gas pipeline project in Europe - the second Russian twin subsea pipeline that is currently under construction in the Baltic Sea. While much attention has been paid to the question of why and how the Russian state- controlled energy giant seeks to circumvent Ukraine as a transit country for its delivery of gas to Western Europe, hardly any attention has been paid to the benefits gained by the companies and political entities directly involved in the preparation and construction of Nord Stream 2. The paper seeks to fill this gap in the debate by taking a closer look at the business deals and commercial actors involved in the implementation of this second Russian natural gas pipeline project in the Baltic Sea. It highlights how local and national economic interests and European energy companies' motivations for participating in the project go beyond the volumes of Russian natural gas that Gazprom expects to deliver to European customers through its Baltic Sea pipelines from 2020. Keywords: Baltic Sea, Nord Stream, Gazprom, Russia, Germany, Sweden, Denmark, Finland, Latvia. This analysis was produced within the Think Visegrad Non-V4 Fellowship programme. Think Visegrad – V4 Think Tank Platform is a network for structured dialog on issues of strategic regional importance. The network analyses key issues for the Visegrad Group, and provides recommendations to the governments of V4 countries, the annual presidencies of the group, and the International Visegrad Fund. -

Case COMP/M.6910 — Gazprom/Wintershall/Target Companies) (Text with EEA Relevance) (2013/C 321/07)

7.11.2013 EN Official Journal of the European Union C 321/7 Prior notification of a concentration (Case COMP/M.6910 — Gazprom/Wintershall/Target Companies) (Text with EEA relevance) (2013/C 321/07) 1. On 30 October 2013 the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 ( 1 ), concerning a swap of certain assets between JSC Gazprom (‘Gazprom’) and Wintershall Holding GmbH (‘Wintershall’) pursuant to a Basic Swap Agreement dated November 14, 2012. Under the Agreement, in exchange for minority interests in certain of its natural gas and gas condensate exploration and production assets in Western Siberia, Gazprom will acquire from Wintershall: (1) sole control of Wingas GmbH (‘Wingas’) and Wintershall Erdgas Handelshaus GmbH & Co. KG (‘WIEH’), two natural gas supply and storage joint ventures formed and jointly controlled by Wintershall and Gazprom, and (2) joint control of Wintershall Noordzee BV (‘WINZ’) and Wintershall Services BV (‘Wintershall Services’), two wholly owned Wintershall subsidiaries engaged in relatively minor oil and gas exploration and production activities in the North Sea. The proposed acquisitions are interdependent and therefore constitute a single concentration within the meaning of Regulation (EC) No 139/2004. 2. The business activities of the undertakings concerned are: — Gazprom is active in the exploration, production, transportation, supply, trading, distribution, and storage of natural gas, — Wintershall, owned by BASF SE (‘BASF’), engages in the exploration and production of crude oil and natural gas in particular in Europe, Northern Africa, South America and Russia, as well as in natural gas pipeline operation, investment and natural gas supply and storage, — Wintershall and Gazprom also jointly own and control a German gas transmission business, which is conducted through the transmission operators GASCADE Gastransport GmbH, OPAL Gastransport GmbH & Co. -

Real-Time Pricing in the Swedish Electricity Market Bachelor Thesis, Department of Economics

Real-Time Pricing in the Swedish Electricity Market Bachelor Thesis, Department of Economics Hjalmar Pihl Advisor: Associate Professor Tommy Andersson, PhD 17 January 2012 ABSTRACT An introduction of real-time prices of electricity, i.e. prices that correspond to the hourly spot market price, for residential consumers in Sweden has recently been suggested. Support for real-time pricing comes from governmental agencies as well as commercial interests, however without a good understanding of how a shift to real-time prices would affect prices and volumes in the market, and what welfare effects these changes would induce. This thesis addresses these issues by developing a model of the Swedish electricity market. The conclusion is that an introduction of real-time pricing would have a smoothing effect on prices and volumes, which in turn is likely to have positive welfare effects on producers and on the consumers that shift, but a negative effect on the larger consumers that already pay by the hour. The net welfare effect is likely to be positive. Keywords: Electricity, Real-Time Pricing, Sweden 1 TABLE OF CONTENTS 1. INTRODUCTION............................................................................................................. 3 2. BACKGROUND ............................................................................................................... 5 2.1 ELECTRICITY AS A COMMODITY ............................................................................................................. 5 2.2 THE NORDIC ELECTRICITY MARKET -

Increasing Space Granularity in Electricity Markets

INCREASING SPACE GRANULARITY IN ELECTRICITY MARKETS INNOVATION LANDSCAPE BRIEF © IRENA 2019 Unless otherwise stated, material in this publication may be freely used, shared, copied, reproduced, printed and/or stored, provided that appropriate acknowledgement is given of IRENA as the source and copyright holder. Material in this publication that is attributed to third parties may be subject to separate terms of use and restrictions, and appropriate permissions from these third parties may need to be secured before any use of such material. ISBN 978-92-9260-128-7 Citation: IRENA (2019), Innovation landscape brief: Increasing space granularity in electricity markets, International Renewable Energy Agency, Abu Dhabi. About IRENA The International Renewable Energy Agency (IRENA) is an intergovernmental organisation that supports countries in their transition to a sustainable energy future, and serves as the principal platform for international co-operation, a centre of excellence, and a repository of policy, technology, resource and financial knowledge on renewable energy. IRENA promotes the widespread adoption and sustainable use of all forms of renewable energy, including bioenergy, geothermal, hydropower, ocean, solar and wind energy in the pursuit of sustainable development, energy access, energy security and low-carbon economic growth and prosperity. www.irena.org Acknowledgements This report was prepared by the Innovation team at IRENA’s Innovation and Technology Centre (IITC) and was authored by Arina Anisie, Elena Ocenic and Francisco Boshell with additional contributions and support by Harsh Kanani, Rajesh Singla (KPMG India). Valuable external review was provided by Helena Gerard (VITO), Pablo Masteropietro (Comillas Pontifical University), Rafael Ferreira (former CCEE, Brazilian market operator) and Gerard Wynn (IEEFA), along with Carlos Fernández, Martina Lyons and Paul Komor (IRENA).