Country Profile 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![Pdf [2019-05-25] 21](https://docslib.b-cdn.net/cover/2261/pdf-2019-05-25-21-742261.webp)

Pdf [2019-05-25] 21

ISSN 1648-2603 (print) VIEŠOJI POLITIKA IR ADMINISTRAVIMAS ISSN 2029-2872 (online) PUBLIC POLICY AND ADMINISTRATION 2019, T 18, Nr. 3/2019, Vol. 18, Nr. 3, p. 46-58 The World Experience and a Unified Model for Government Regulation of Development of the Automotive Industry Illia A. Dmytriiev, Inna Yu. Shevchenko, Vyacheslav M. Kudryavtsev, Olena M. Lushnikova Department of Economics and Entrepreneurship Kharkiv National Automobile and Highway University 61002, 25 Yaroslav Mudriy Str., Kharkiv, Ukraine Tetiana S. Zhytnik Department of Social Work, Social Pedagogy and Preschool Education Bogdan Khmelnitsky Melitopol State Pedagogical University 72300, 20 Hetmanska Str., Melitopol, Ukraine http://dx.doi.org/10.5755/j01.ppaa.18.3.24720 Abstract. The article summarises the advanced world experience in government regulation of the automotive industry using the example of the leading automotive manufacturing countries – China, Japan, India, South Korea, the USA, and the European Union. Leading approach to the study of this problem is the comparative method that has afforded revealing peculiarities of the primary measures applied by governments of the world to regulate the automotive industry have been identified. A unified model for government regulation of the automotive industry has been elaborated. The presented model contains a set of measures for government support for the automotive industry depending on the life cycle stage (inception, growth, stabilisation, top position, stagnation, decline, crisis) of the automotive industry and the -

How to Fix Ukraine's Broken Legal System

June 26, 2015, Vol. 2, Issue 2 How To Fix Ukraine’s Broken Legal System Editors’ Note Contents If it ain't broke, don't fi x it. But if it is broke, as Ukraine's criminal justice system is, how to 4 Is it time to scrap Ukraine’s fi x it? Does society start from scratch or simply focus on a few areas at a time? These are legal system and start over with the questions that Ukrainians are still wrestling with, nearly 24 years after the collapse of the another nation’s system? Soviet Union The U.S.S.R.'s half-life is proving to be way too long, and the legal system pro- 6 Armine Sahakyan: Judicial reform vides one of the best examples of how much damage was infl icted during those 70 years. is still a pipe dream in former Basic legal concepts are either not appreciated or in force here. Soviet Union Probable cause – It still feels like a society where police can take people away in the dead of night on any pretext. 8 Soviet social guarantees for Presumption of innocence until proven guilty – Suspects can be subject to damning pre-tri- employees scare investors, often backfi re al publicity. Putting defendants in courtroom cages announces to the world: This is a guilty person. Lengthy pre-trial detention assumes guilt and ruins lives. 10 Anders Aslund: How to reform Plea bargains – These come in handy in getting lower-level suspects to turn state's evidence prosecutors and judicial system against top-level suspects, in murders and in fi nancial crimes, and also in ensuring justice is done without lengthy and costly trials. -

RESTRICTED WT/TPR/S/334 15 March 2016

RESTRICTED WT/TPR/S/334 15 March 2016 (16-1479) Page: 1/163 Trade Policy Review Body TRADE POLICY REVIEW REPORT BY THE SECRETARIAT UKRAINE This report, prepared for the first Trade Policy Review of Ukraine, has been drawn up by the WTO Secretariat on its own responsibility. The Secretariat has, as required by the Agreement establishing the Trade Policy Review Mechanism (Annex 3 of the Marrakesh Agreement Establishing the World Trade Organization), sought clarification from Ukraine on its trade policies and practices. Any technical questions arising from this report may be addressed to Cato Adrian (tel: 022/739 5469); and Thomas Friedheim (tel: 022/739 5083). Document WT/TPR/G/334 contains the policy statement submitted by Ukraine. Note: This report is subject to restricted circulation and press embargo until the end of the first session of the meeting of the Trade Policy Review Body on Ukraine. This report was drafted in English. WT/TPR/S/334 • Ukraine - 2 - CONTENTS SUMMARY ........................................................................................................................ 7 1 ECONOMIC ENVIRONMENT ........................................................................................ 11 1.1 Main Features .......................................................................................................... 11 1.2 Economic Developments ............................................................................................ 11 1.3 Developments in Trade ............................................................................................. -

Project Document

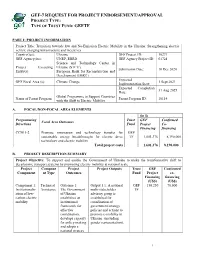

GEF-7 REQUEST FOR PROJECT ENDORSEMENT/APPROVAL PROJECT TYPE: TYPE OF TRUST FUND: GEFTF PART I: PROJECT INFORMATION Project Title: Transition towards low and No-Emission Electric Mobility in the Ukraine: Strengthening electric vehicle charging infrastructure and incentives Country(ies): Ukraine GEF Project ID: 10271 GEF Agency(ies): UNEP, EBRD GEF Agency Project ID: 01724 Science and Technology Center in Project Executing Ukraine (STCU), Submission Date: 10 Dec 2020 Entity(s): European Bank for Reconstruction and Development (EBRD) Expected GEF Focal Area (s): Climate Change 1 Sept 2021 Implementation Start: Expected Completion 31 Aug 2025 Date: Global Programme to Support Countries Name of Parent Program Parent Program ID: 10114 with the Shift to Electric Mobility A. FOCAL/NON-FOCAL AREA ELEMENTS (in $) Programming Trust GEF Confirmed Focal Area Outcomes Directions Fund Project Co- Financing financing CCM 1-2 Promote innovation and technology transfer for GEF sustainable energy breakthroughs for electric drive TF 1,601,376 8,190,000 technology and electric mobility Total project costs 1,601,376 8,190,000 B. PROJECT DESCRIPTION SUMMARY Project Objective: To support and enable the Government of Ukraine to make the transformative shift to decarbonize transport systems by promoting electric mobility at national scale Project Compone Project Project Outputs Trust GEF Confirmed Component nt Type Outcomes Fund Project co- Financing financing (US$) (US$) Component 1: Technical Outcome 1: Output 1.1: A national GEF 150,250 70,000 Institutionaliz Assistance The Government multi-stakeholder TF ation of low- of Ukraine advisory group is carbon electric establishes an established for mobility institutional coordination of framework for government strategy, effective policies and actions to coordination, promote e-mobility in develops capacity Ukraine. -

Page 1 of 3 2020 2020 July August 1 Prjsc "ZAZ" (Zaporizhia Automobile Building Plant) 9 7 -22,2 Cars

page 1 of 3 Motor vehicle production in Ukraine (units) 2020 2020 № MANUFACTURER % Chg July August PrJSC "ZAZ" (Zaporizhia Automobile 1 9 7 -22,2 Building Plant) Cars 0 0 - CV 0 0 - Buses 9 7 -22,2 PrJSC «AutoKrAZ» (Kremenchuk 2 n/a n/a - Automobile Plant) Cars - CV - Buses - 3 BOGDAN Corporation 0 16 - Cars 0 0 - CV 0 0 - Buses 0 16 - Etalon Corporation: PrJSC "Boryspil 4 0 0 - Autoplant" Cars - CV 0 - Buses 0 - Etalon Corporation: "Chernihiv autoplant" 5 24 30 +25,0 LLC Cars - CV 0 - Buses 24 30 +25,0 6 PrJSC "EUROCAR" 172 38 -77,9 Cars 172 38 -77,9 CV - Buses - 7 PJSC "Chаsiv Yar Buses Plant" 2 5 +150,0 Cars - CV - Buses 2 5 +150,0 8 JSC "Cherkassy Bus" 29 25 -13,8 Cars - CV 4 0 -100,0 Buses 25 25 +0,0 Cars 172 38 -77,9 CV 4 0 -100,0 Buses 60 83 +38,3 TOTAL 236 121 -48,7 © "Ukrautoprom" *PJSC «AUTOKRAZ» data are unavailable since August 2016 page 2 of 3 Motor vehicle production in Ukraine (units) 2019 2020 % Chg № MANUFACTURER August August 20/19 PrJSC "ZAZ" (Zaporizhia Automobile 1 13 7 -46,2 Building Plant) Cars 0 0 - CV 8 0 -100,0 Buses 5 7 +40,0 PrJSC «AutoKrAZ» (Kremenchuk 2 n/a n/a - Automobile Plant) Cars - CV - Buses - 3 BOGDAN Corporation 19 16 -15,8 Cars 0 0 - CV 0 0 - Buses 19 16 -15,8 Etalon Corporation: PrJSC "Boryspil 4 0 0 - Autoplant" Cars - CV 0 - Buses 0 - Etalon Corporation: "Chernihiv autoplant" 5 16 30 +87,5 LLC Cars - CV 0 - Buses 16 30 +87,5 6 PrJSC "EUROCAR" 553 38 -93,1 Cars 553 38 -93,1 CV - Buses - 7 PJSC "Chаsiv Yar Buses Plant" 6 5 -16,7 Cars - CV - Buses 6 5 -16,7 8 JSC "Cherkassy Bus" 61 25 -59,0 Cars - CV 26 0 -100,0 Buses 35 25 -28,6 Cars 553 38 -93,1 CV 34 0 -100,0 Buses 81 83 +2,5 TOTAL 668 121 -81,9 © "Ukrautoprom" *PJSC «AUTOKRAZ» data are unavailable since August 2016 page 3 of 3 Motor vehicle production in Ukraine (units) 2019 2020 % Chg № MANUFACTURER Jan.-Aug. -

El Mercado De La Automoción En Ucrania

Oficina Económica y Comercial de la Embajada de España en Kiev El mercado de les a la automoción en Ucrania NotasSectori 1 El mercado de la automoción en Ucrania Esta nota ha sido elaborada por Diego Micol García bajo la supervisión de la Oficina Económica y Co- mercial de la Embajada de España en Kiev Abril 2009 NotasSectoriales 2 EL MERCADO DE LA AUTOMOCIÓN EN UCRANIA ÍNDICE CONCLUSIONES 4 I. DEFINICION DEL SECTOR 6 1. Delimitación del sector 6 2. Clasificación arancelaria 7 II. OFERTA 8 1. Tamaño del mercado 9 2. Producción local 11 3. Importaciones y Exportaciones 14 4. Competidores Nacionales 16 5. Competidores Extranjeros 20 III. ANÁLISIS CUALITATIVO DE LA DEMANDA 22 1.1 Parque móvil ucraniano 1.2 Análisis cualitativo del parque móvil ucraniano IV. PRECIOS Y SU FORMACIÓN 27 V. PERCEPCIÓN DEL PRODUCTO ESPAÑOL 28 VI. DISTRIBUCIÓN 29 VII. CONDICIONES DE ACCESO AL MERCADO 30 VIII. ANEXOS 32 1. Empresas 32 2. Ferias 33 3. Publicaciones del sector 34 4. Asociaciones 35 5. Otras direcciones de interés 35 Oficina Económica y Comercial de la Embajada de España en Kiev 3 EL MERCADO DE LA AUTOMOCIÓN EN UCRANIA CONCLUSIONES Para la industria de automoción ucraniana se configura una corta pero profunda disminución de la producción en 2009, debido al descenso de la demanda interna que junto con el des- censo de las exportaciones, no serán capaces de compensar el descenso de las ventas, de las que se prevé una bajada comprendida de 10-20%. Desde octubre de 2008, las ventas han sufrido un drástico descenso, a nivel mundial, como consecuencia de los efectos de la contracción del crédito. -

Eurasian Journal of Business and Management, 9(2), 2021, 164-183 DOI: 10.15604/Ejbm.2021.09.02.005

Eurasian Journal of Business and Management, 9(2), 2021, 164-183 DOI: 10.15604/ejbm.2021.09.02.005 EURASIAN JOURNAL OF BUSINESS AND MANAGEMENT www.eurasianpublications.com THE DEVELOPMENT OF THE AUTOMOTIVE INDUSTRY IN POST-SOVIET COUNTRIES SINCE 1991 Sardor Tadjiev Osaka University, Japan Email: [email protected] Pierre-Yves Donze Osaka University, Japan Email: [email protected] Received: March 4, 2021 Accepted: May 31, 2021 Abstract This paper discusses the impact of industrial policy on the development of the automotive industry in five post-Soviet countries since 1991 (Russia, Ukraine, Belarus, Uzbekistan, and Kazakhstan). By using foreign trade and production statistics as well as qualitative data on automobile companies from business news, this paper highlights three different paths: success in post-2000 Russia and Uzbekistan, stagnation and struggle for survival in Belarus and Kazakhstan, and failure in pre-2000 Russia and Ukraine. The existence of an automotive industry before 1991 was not a factor in success because most pre-existing firms collapsed after the break-up of the Soviet Union. Instead, the growth of these post-Soviet automotive industries has essentially relied on the presence of global car makers. This research demonstrates that inward foreign direct investment and licensing agreements were fostered by the combination of protectionist policies that made importation uncompetitive and access of global firms to the large Russian market (both direct access and indirect access via a country with privileged access to Russia). This paper also highlights different strategies adopted by foreign firms: whereas the largest Western and Japanese companies invested directly in Russia, companies from China and Korea used Central Asia and Belarus as back doors to enter the Russian market. -

UA Automotive Industry Overview

18.09.2013 Brussels Ukrainian car industry overview Summary 1 Ukraine car industry – core data Indicator Ukraine Population 2013 45,5 Mio Population growth rate 0,56 % Share of employed in automotive <0,1% sector from total employed RU GDP growth 2012 0,2 % GDP per capita 2012 5.770 € Share of automotive sector in GDP 0,9 % DE Inflation (official) 0,1 % CZ UA Unemployment 7,8 % Car density (per 1000 people) 158 Average car age 18,7 Trade deficit formed by automotive -3,9 bln $ import 2012 1 USD = 8,1 UAH; 1 EUR = Exchange Rate (4.09.2013) 10,6 UAH 2 Market review 2 Car producers in Ukraine: capacity underloading Enterprise Model Model Bohdan PrJSC Zaporozhe Automobile ZAZ Lanos, ZAZ Sense, ZAZ Vida, CKD Building Plant ZAZ Chance, ZAZ Forza (ZAZ) 2 Cherkassy PJSC LuAZ Bogdan (VAZ 2110), Hyundai Uzhgorod (Bogdan CKD Tucson 4 Motors) PrJSC Eurocar Illichevsk Skoda (Octavia, Rapid, Fabia, Zaporozhe SKD 1 Superb, Roomster, Yeti) Eurocar 1 Kremenchuk car Geely (MK-1, MK Cross, Emgrand), UkrAvto assembly plant SKD SsangYong (Rexton, Kyron, UkrAvto Ltd. (KrASZ) Korando) Current average plant Car production by year 05 06 07 08 09 10 11 12 capacity loading is only In k units per year 196,7 267,2 380,1 400,8 65,6 75,3 97,6 69,7 17,4%. Existing total plant capacity in 2012 amounted to 400 k units per year Source: Ukrautoprom 3 New passenger cars market 4 Passenger cars sales dynamics of locally produced and imported cars – sales of locally produced cars X – passenger cars market in k units Х% – share of internally produced cars From May10%. -

Parimatch Parimatch Increases Tra C from Organic Search by 64% in 6 Months Thanks to Promodo’S Innovative Approach to SEO

2013 Case Study Parimatch Parimatch increases trac from organic search by 64% in 6 months thanks to Promodo’s innovative approach to SEO 2013 Challenge Parimatch is a being shop founded in 1996. With time it transforms from small bookmaker’s office into international games network with over 400 branches operating in Russia, Belarus, Kazakhstan, Moldova, Kyrgyzstan and Georgia. At present Parimatch is one of the leaders in the gambling industry on CIS territory. One of the most challenging tasks in gambling is to aract players as the market is quite saturated with many companies competing for the clients’ aention. At the beginning of cooperation with Promodo Parimatch website used only half of its potential. That is why the primary goal was to fix current problems and build quality link mass to improve website rankings in the search engines. 2013 Solution Considering client’s long term goals Promodo specialists suggested two-step process. During the first step the main focus was on cleaning and improving website from SEO perspective. It included the next stages: — New website architecture has been offered; — Complete technical optimization has been done; — All pages have been optimized; — External link popularity has been corrected (some suspicious external links have been deleted); Special aention has been given to building comfortable interaction between Promodo experts and Parimatch technical specialists, who have in charge of recommendation implementation. It made possible to always find the most optimal variant when ideal from SEO perspective solution for some reasons appeared to be resource-consuming in implementation. The second step included building link popularity which helped considerably improve website positions in the search engines. -

Sportradar Coverage List

Global coverage of Digital Sports Solutions Last update: 07.09.2021 SOCCER INTERNATIONAL Odds Comparison Statistics Live Scores Live Centre World Championship 1 4 1 1 World Championship Qualification (1) 1 2 1 1 World Championship Women 1 4 1 1 World Championship Women Qualification (1) 1 4 AFC Challenge Cup 1 4 3 AFF Suzuki Cup (6) 1 4 1 1 Africa Cup of Nations 1 4 1 1 African Nations Championship 1 4 2 Algarve Cup Women 1 4 3 Asian Cup (6) 1 4 1 1 Asian Cup Qualification 1 5 3 Asian Cup Women 1 5 Baltic Cup 1 4 Caribbean Cup 1 5 CONCACAF Womens Championship 1 5 Confederations Cup (1) 1 4 1 1 Copa America 1 4 1 1 COSAFA Cup 1 4 Cyprus Women Cup 1 4 3 SheBelieves Cup Women 1 5 European Championship 1 4 1 1 European Championship Qualification (1) 1 2 1 1 European Championship Women 1 4 1 1 European Championship Women Qualification 1 4 Gold Cup (6) 1 4 1 1 Gold Cup Qualification 1 4 Olympic Tournament 1 4 1 2 Olympic Tournament Women 1 4 1 2 SAFF Championship 1 4 WAFF Championship 1 4 2 Friendly Games Women (1) 1 2 Friendly Games, Domestic Cups (1) (2) 1 2 Africa Cup of Nations Qualification 1 3 3 Africa Cup of Nations Women (1) 1 4 Asian Games Women 1 4 1 1 Central American and Caribbean Games Women 1 3 3 CONCACAF Nations League A 1 5 CONCACAF Nations League B 1 5 3 CONCACAF Nations League C 1 5 3 Copa Centroamericana 1 5 3 Four Nations Tournament Women 1 4 Intercontinental Cup 1 5 Kings Cup 1 4 3 Pan American Games 1 3 2 Pan American Games Women 1 3 2 Pinatar Cup Women 1 5 1 1st Level 2 2nd Level 3 3rd Level 4 4th Level 5 5th Level Page: -

Problems and Prospects of Development of the Automotive Industry in Ukraine

PERIODYK NAUKOWY AKADEMII POLONIJNEJ 20 (2017) nr 1 PROBLEMS AND PROSPECTS OF DEVELOPMENT OF THE AUTOMOTIVE INDUSTRY IN UKRAINE Illia Dmitriiev DSc, Kharkiv National Automobile and Highway University, e-mail: [email protected], Ukraine Inna Shevchenko PhD, Kharkiv National Automobile and Highway University, e-mail: [email protected], Ukraine Abstract. The article identifies major problems of the development of the automotive industry in Ukraine in 2010-2015, such as: catastrophic decrease of the production volume of cars, trucks and buses; reduction of the production capacity of automotive industry enterprises; loss of the competitiveness of the domestic automakers on the national automobiles market; increase of the dependence of automakers from borrowed funds; prevailing unprofitability of automakers and bankruptcy of some of them. Nowadays the only way to preserve the Ukrainian automotive industry is an active state protectionism of the development of the automotive industry as a strategically important sector of the national economy. Keywords: automotive industry, automaker, automobiles market, mechanical engineering. DOI: http://dx.doi.org/10.23856/2001 Introduction Automotive industry is the important part of the mechanical engineering in Ukraine. According to the «Concept of the state target economic program of the passenger car industry development for the period until 2020» «…vehicle production in Ukraine provides the high level of the added value (over 70 percent), generates the demand for goods and services of the related industries enterprises (production of metal, plastics, car windows, chemicals, etc.) and promotes the research activity. Creation of one workplace in enterprises of the automotive industry entails the creation of six workplaces in the related industries» (Concept of the state target economic program of the passenger car industry development for the period until 2020). -

Does Safeguards Need Saving? Lessons from the Ukraine–Passenger Cars Dispute

World Trade Review (2017), 16: 2, 227–251 © Arevik Gnutzmann-Mkrtchyan And Simon Lester doi:10.1017/S1474745616000525 Does Safeguards Need Saving? Lessons from the Ukraine–Passenger Cars Dispute AREVIK GNUTZMANN-MKRTCHYAN* Leibniz University of Hanover SIMON LESTER** Cato Institute Abstract: The Panel Report in Ukraine–Passenger Cars provides an opportunity to revisit an old debate over the role of safeguard measures in the WTO. With regard to the legal findings, the Panel followed the established jurisprudence in this area, and found a number of violations of the Safeguards Agreement. With regard to the economics, we delve more deeply into the economic and political background of the safeguards investigation. Ukraine was hit by the economic crisis shortly after its WTO accession that significantly liberalized import tariffs on passenger cars. Next, we offer a de novo look at the injury and causation issues in this case, and discuss the challenges of an industry reliant on offshored production that sees a safeguard as a mechanism to attract foreign direct investment (FDI) for production. We conclude with an assessment of the operation of the WTO’s safeguards regime, along with some tentative suggestions for reform. Overall, our examination of the economic analysis by the investigating authority and the legal review by the WTO Panel raises questions about particular aspects of the domestic and WTO processes, but concludes that the system worked well in this case. 1. Introduction Safeguards is a long-standing mechanism by which GATT Contracting Parties, and now WTO Members, can deviate from their normal free trade obligations, and impose tariffs to protect a domestic industry.