Auto Parts Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Contacts in Japan Contacts in Asia

TheDirectoryof JapaneseAuto Manufacturers′ WbrldwidePurchaslng ● Contacts ● トOriginalEqulpment ● トOriginalEqulpment Service トAccessories トMaterials +RmR JA払NAuTOMOBILEMANUFACTURERSAssocIATION′INC. DAIHATSU CONTACTS IN JAPAN CONTACTS IN ASIA OE, Service, Accessories and Material OE Parts for Asian Plants: P.T. Astra Daihatsu Motor Daihatsu Motor Co., Ltd. JL. Gaya Motor 3/5, Sunter II, Jakarta 14350, urchasing Div. PO Box 1166 Jakarta 14011, Indonesia 1-1, Daihatsu-cho, Ikeda-shi, Phone: 62-21-651-0300 Osaka, 563-0044 Japan Fax: 62-21-651-0834 Phone: 072-754-3331 Fax: 072-751-7666 Perodua Manufacturing Sdn. Bhd. Lot 1896, Sungai Choh, Mukim Serendah, Locked Bag No.226, 48009 Rawang, Selangor Darul Ehsan, Malaysia Phone: 60-3-6092-8888 Fax: 60-3-6090-2167 1 HINO CONTACTS IN JAPAN CONTACTS IN ASIA OE, Service, Aceessories and Materials OE, Service Parts and Accessories Hino Motors, Ltd. For Indonesia Plant: Purchasing Planning Div. P.T. Hino Motors Manufacturing Indonesia 1-1, Hinodai 3-chome, Hino-shi, Kawasan Industri Kota Bukit Indah Blok D1 No.1 Tokyo 191-8660 Japan Purwakarta 41181, Phone: 042-586-5474/5481 Jawa Barat, Indonesia Fax: 042-586-5477 Phone: 0264-351-911 Fax: 0264-351-755 CONTACTS IN NORTH AMERICA For Malaysia Plant: Hino Motors (Malaysia) Sdn. Bhd. OE, Service Parts and Accessories Lot P.T. 24, Jalan 223, For America Plant: Section 51A 46100, Petaling Jaya, Hino Motors Manufacturing U.S.A., Inc. Selangor, Malaysia 290 S. Milliken Avenue Phone: 03-757-3517 Ontario, California 91761 Fax: 03-757-2235 Phone: 909-974-4850 Fax: 909-937-3480 For Thailand Plant: Hino Motors Manufacturing (Thailand)Ltd. -

Master List of DTP Participants

Institute of Business Administration, Karachi Center for Executive Education Directors' Training Program Certification Year - No Program Name Designation Organization No. Certitied CCL Pharmaceuticals 215 IBA/DTP - 0213 2019 Dr. Shahzad Khan Chief Operating Officer CCL Pharmaceuticals Pvt Ltd Pvt Ltd 216 IBA/DTP - 0214 2019 IBA-Karachi Faisal Jalal IBA Faculty IBA-Karachi 217 IBA/DTP - 0215 2019 Self Lubna Pathan Director own Business 218 IBA/DTP - 0216 2019 Indus Clean Energy Masood Hasan Khan Head of Commercial Indus Clean Energy 219 IBA/DTP - 0217 2019 Avanceon Limited Naveed Ali Baig Director Avanceon Limited Senior Executive Vice President - 220 IBA/DTP - 0218 2019 Premier Insurance Nina Afridi Premier Insurance Head of HR & Administration 221 IBA/DTP - 0219 2019 Hinopak Motors Ltd. Yoshihiko Nanami President & CEO Hinopak Motors Ltd. 222 IBA/DTP - 0220 2019 Hinopak Motors Ltd. Shigeru Tsuchiya Executive Vice President Hinopak Motors Ltd. Vice President & Director 223 IBA/DTP - 0221 2019 Hinopak Motors Ltd. Takehito Sasaki Hinopak Motors Ltd. Production Vice President & Chief Financial 224 IBA/DTP - 0222 2019 Hinopak Motors Ltd. Fahim Aijaz Sabzwari Hinopak Motors Ltd. Officer 225 IBA/DTP - 0223 2019 Hinopak Motors Ltd. Naushad Riaz Vice President Hinopak Motors Ltd. 226 IBA/DTP - 0224 2019 Hinopak Motors Ltd. Syed Samad Siraj Deputy General Manager Hinopak Motors Ltd. 227 IBA/DTP - 0225 2019 Hinopak Motors Ltd. Muhammad Zahid Hasan Deputy General Manager Hinopak Motors Ltd. 228 IBA/DTP - 0226 2019 Hinopak Motors Ltd. Ahsan Waseem Akhtar Senior Manager HR, Admin & HSE Hinopak Motors Ltd. 229 IBA/DTP - 0227 2019 Hinopak Motors Ltd. Abdul Basit Departmental Head Finance Hinopak Motors Ltd. -

New Business Opportunities in Pakistan

NEW BUSINESS OPPORTUNITIES IN PAKISTAN NEW BUSINESS OPPORTUNITIES IN PAKISTAN AN INVESTOR’S GUIDEBOOK Consultants and authors of this report: Philippe Guitard Shahid Ahmed Khan Derk Bienen This report has been produced with the assistance of the European Union under the Asia-Invest programme. The views expressed herein are those of the consultant and can therefore in no way be taken to reflect the views of the European Union. New Business Opportunities in Pakistan TABLE OF CONTENTS LIST OF TABLES ................................................................................................................................. VIII LIST OF FIGURES .................................................................................................................................. X LIST OF BOXES..................................................................................................................................... XI LIST OF ACRONYMS ........................................................................................................................... XII INTRODUCTION ..................................................................................................................................... 1 EXECUTIVE SUMMARY......................................................................................................................... 2 PART I: PAKISTAN GENERAL INFORMATION ................................................................................... 8 MAP OF THE COUNTRY....................................................................................................................... -

Survey on Strengthening Bilateral Economic Relationship Between Pakistan and Japan FINAL REPORT

Survey on Strengthening Bilateral Economic Relationship between Pakistan and Japan FINAL REPORT February 2019 Ministry of Economy, Trade and Industry International Development Center of Japan Inc. (IDCJ) CONTENTS Chapter 1 Overview of Pakistan’s Economy .................................................................. 1 1-1 Macro Economy ....................................................................................................... 1 1-2 Industry................................................................................................................... 2 1-3 Trade ....................................................................................................................... 4 1-4 Inward Foreign Direct Investment ......................................................................... 6 Chapter 2 Pakistan’s Business Environment ................................................................ 8 2-1 Government Organization ...................................................................................... 8 2-2 Business-related Acts .............................................................................................. 9 2-3 Approval and Authorization for Foreign Direct Investment .................................10 2-4 Investment Policy .................................................................................................. 11 2-5 Infrastructure ........................................................................................................14 2-5-1 Electric Power .....................................................................................................14 -

Shell-Annual-Report-2019.Pdf

ANNUAL REPORT 2019 1 2 SHELL PAKISTAN LIMITED CONTENTS GOVERNANCE & COMPLIANCE Company Information........................................................................................................................... 06 Vision................................................................................................................................................ 07 Statement of General Business Principles.................................................................................................. 08 Chairperson’s Review............................................................................................................................ 12 Board of Directors ............................................................................................................................... 20 Report of the Directors ......................................................................................................................... 24 Notice of Anuual General Meeting ........................................................................................................ 28 Statement of Compliance ..................................................................................................................... 30 Independent Auditors’ Review Report ...................................................................................................... 33 OUR PERFORMANCE Retail ............................................................................................................................................... -

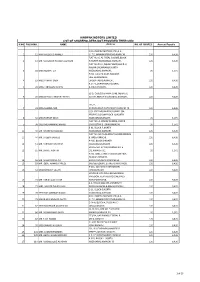

Hinopak Motors Limited List of Shareholders Not Provided Their Cnic S.No Folio No

HINOPAK MOTORS LIMITED LIST OF SHAREHOLDERS NOT PROVIDED THEIR CNIC S.NO FOLIO NO. NAME Address NO. OF SHARES Amount Payable C/O HINOPAK MOTORS LTD.,D-2, 1 12 MIR MAQSOOD AHMED S.I.T.E.,MANGHOPIR ROAD,KARACHI., 120 6,426 FLAT NO. 6, AL-FAZAL SQUARE,BLOCK- 2 13 MR. MANZOOR HUSSAIN QURESHI H,NORTH NAZIMABAD,KARACHI., 120 6,426 FLAT NO.19-O, IQBAL PLAZA,BLOCK-O, NAGAN CHOWRANGI,NORTH 3 18 MISS NUSRAT ZIA NAZIMABAD,KARACHI., 20 1,071 H.NO. E-13/40,NEAR RAILWAY LINE,GHARIBABAD, 4 19 MISS FARHAT SABA LIAQUATABAD,KARACHI., 120 6,426 R.177-1,SHARIFABADFEDERAL 5 24 MISS TABASSUM NISHAT B.AREA,KARACHI., 120 6,426 52-D, Q-BLOCK,PAHAR GANJ, NEAR LAL 6 28 MISS SHAKILA ANWAR FATIMA KOTTHI,NORTH NAZIMABAD,KARACHI., 120 6,426 171/2, 7 31 MISS SAMINA NAZ AURANGABAD,NAZIMABAD,KARACHI-18. 120 6,426 C/O. SYED MUJAHID HUSSAINP-394, PEOPLES COLONYBLOCK-N, NORTH 8 32 MISS FARHAT ABIDI NAZIMABADKARACHI, 20 1,071 FLAT NO. A-3FARAZ AVENUE, BLOCK- 9 38 SYED MOHAMMAD HAMID 20GULISTAN-E-JOHARKARACHI, 20 1,071 B-91, BLOCK-P,NORTH 10 40 MR. KHURSHID MAJEED NAZIMABAD,KARACHI. 120 6,426 FLAT NO. M-45,AL-AZAM SQUARE,FEDRAL 11 44 MR. SALEEM JAWEED B. AREA,KARACHI., 120 6,426 A-485, BLOCK-DNORTH 12 51 MR. FARRUKH GHAFFAR NAZIMABADKARACHI. 120 6,426 HOUSE NO. D/401,KORANGI NO. 5 13 55 MR. SHAKIL AKHTAR 1/2,KARACHI-31. 20 1,071 H.NO. 3281, STREET NO.10,NEW FIDA HUSSAIN SHAIKHA 14 56 MR. -

Factors Affecting Consumer's Purchase Intention When Buying a Sedan Car

Factors Affecting Consumer's Purchase Intention When Buying Toyota Corolla in Pakistan By AHSAN RAZA AYESHA MAJID VINZA ZAFAR YAHA REHMAN MBA-II-C MARKETING RESEARCH SUBMITTED TO PROF. SAAD SHAHID RUNNING HEADER: Marketing Research Toyota Indus Motors 1 Table of Contents Executive Summary ................................................................................................................... 4 Introduction ................................................................................................................................ 6 Background ............................................................................................................................ 6 Why did we choose this company? ........................................................................................ 9 Literature Review..................................................................................................................... 10 Industry Analysis ..................................................................................................................... 13 Competitor analysis ......................................................................................................... 13 Automotive Industry trends in Pakistan ........................................................................... 13 Company Analysis ............................................................................................................... 15 Problem Definition.................................................................................................................. -

And Others TITLE Student Study Guide: INSTITUTION Ohio State

DCOUMENT RESUME ED'073 327 - VT 019 456 AUTHOR Daugherty, Ronald D.; And Others TITLE Highway Traffic Accident Investigation' and Reporting: Student Study Guide: INSTITUTION Ohio State Univ., Columbus. Center for Vocational and Technical Education. SPONS AGENCY' National-Highway Traffic Safety Administration (DOT), Washington, D. C. PUB DATE Dec 72 NOTE 75p. ERRS PRICE MF-$0.65 HC-$3.29 DESCRIPTORS Behavioral Objectives; Bibliographies; Course . 'Descriptions; Data Collection; *Investigations;Job Training; Learning Activities; Resource Materials; *Skill Development; *Study Guides; Technical Education; *Technical Occupations;.*Traffic Accidents; Transportation; Vocational Education; Worksheets IDENTIFIERS ,*Accident Investigation Technicians ABSTRACT This study guide for students in a basic training program for accident investigation is intended for use with lesson plans for the instructor and a manual for administratorsand planners,'available as VT 019 457 and VT+019 455, respectively.As part of a curriculum package developed by the Center for Vocational and-Technical Education after d nationwide survey, thisdocument contains a rationale detailing the needs for accident investigation technicians, an instructional outline,a course' description, extensive student worksheets, and appended resource materials. Included in this'guide, which is 3-hole punched for insertion intoa _notebook, are a bibliography, teaching suggestions, andan instructor rating sheet for student use. Intended to develop entry-level skills and to train technicians to identify, collect, record, andreport data regarding the driver, vehicle, and environmentas it relates to the pre-crash, crash, and post-crash phases ofan accident, the course consists of five flexible instructional units. Each lesson provides teaching procedures, behavioral objectives, and suggested learning activities. A related document is available ina previous issue as ED 069 848. -

Shariah Compliance Screening Report

Al-Hilal Shariah Advisors December 2016 Shariah Compliance Screening Report INSIDE Key Highlights ......................................................................................................................................... 3 Shariah Compliant Companies ............................................................................................................... 5 Shariah Non - Compliant Companies ...................................................................................................... 7 Suspended & Delisted Companies………………………………………………………………………………………………….....9 Approved Islamic Banks & Windows for Placements ........................................................................... 10 Screening Guidelines for Equity Securities ........................................................................................... 11 Purification Guidelines .......................................................................................................................... 12 Al-Hilal Shariah Advisors (Pvt.) Limited. (Formerly Fortune Islamic (Pvt.) Limited) P a g e | 2 Al-Hilal Shariah Advisors (Pvt.) Limited. (Formerly Fortune Islamic (Pvt.) Limited) 27 April, 2017 KEY HIGHLIGHTS We have conducted Shariah compliance screening of 524 selected companies listed on the Pakistan Stock Exchange as per their latest financial statements (December’16), on the basis of the Shariah compliance screening mechanism approved by our Shariah Supervisory Council headed by Mufti Irshad Ahmad Aijaz. Following are the results for -

Unpacking Policy Space in International Trade Law: the Auto Industry in Brazil and the United States

_________________________________________________________________________________ page i Unpacking Policy Space in International Trade Law: The Auto Industry in Brazil and the United States Ada Bogliolo Piancastelli de Siqueira Submitted in partial fulfillment of the requirements of the degree of Doctor of Juridical Science (SJD) at the Georgetown University Law Center 2019 Dissertation supervisor: Professor Alvaro Santos _________________________________________________________________________________ page ii Abstract This thesis aims to deconstruct the notion of policy space in international trade law. It presents the idea of “unpacking policy space” to suggest that policy space is not merely a concept relating to what room for policy is available under the law. Rather, it demonstrates that this commonly used concept overlooks important regulatory influences that define countries ability to regulate. The dissertation makes two main claims. First, it claims that policy space for industrial and developmental policies extends beyond WTO law and depends not only on international rules; but rather, on systems of domestic and transnational rules and regulations. Second, it argues that by analyzing how different domestic structures lead to different regulatory preferences and possibilities, this analysis provides an insight into how similar transnational and international rules translate differently into different countries. It presents four case studies that assess how the existing regulatory frameworks shaped policies for the automotive industry -

The Automotive Sector in Pakistan

Final Report THE AUTOMOTIVE SECTOR IN PAKISTAN TABLE OF CONTENTS LIST OF ACRONYMS 1 EXECUTIVE SUMMARY 4 CHAPTER 1: INTRODUCTION 9 1.1. Terms of Reference 9 1.2. History of the Sector 10 1.3. Review of Literature 12 CHAPTER 2: THE AUTOMOTIVE SECTOR 16 2.1. Coverage 16 2.2. Sizing of the Sector 16 2.3. Contribution To The Economy 26 2.4. Demand Analysis 32 CHAPTER 3: POLICY AND REGULATORY FRAMEWORK 34 3.1. TRIMS 34 3.2. Investment Policy 36 3.3. Trade Policies 38 3.4. Tariff Policy 39 3.5. Auto Industry Development Programme 43 3.6. Policy and Standards 44 CHAPTER 4: EXTENT OF EFFECTIVE PROTECTION 45 4.1. Methodology 45 4.2. Results 46 4.3. Recommendations on Tariff Reform 47 CHAPTER 5: ASSESSMENT OF COMPETITION IN THE SECTOR 52 5.1. Methodology for Assessing Degree of Competition 52 5.2. Measure of Extent of Competition 53 5.3. Assessment of Competition in the Automotive Sector 54 CHAPTER 6: PROFILE OF THE SAMPLE OF VENDORS 58 6.1. Objectives of the Survey 58 6.2. The Sample 58 6.3. Legal Status 61 ii 6.4. Membership of Associations 61 6.5. Investment and Capacity 62 6.6. Turnover 63 6.7. Employment 63 6.8. Cost Structure 64 6.9. Gross Profit and Value Added 64 CHAPTER 7: KEY ISSUES IN THE VENDING INDUSTRY 66 7.1. Impact of Tariff Protection 66 7.2. Extent of Competition 70 7.3. Degree of Competitiveness 71 7.4. Factors Influencing Growth 71 7.5. -

Zelta OCTA Indemnity Table

Zelta OCTA indemnity table Indemnity, Indemnity, List of auto parts List of auto parts EUR EUR Front bumper 120 Rear-view mirror (1 unit) 80 Front bumper reinforcement support 20 Rear-view mirror glass 30 Licence plate 15 Front door 120 Licence plate frame 2 Rear door 120 Bumper bracket 16 Front door moulding 15 Bumper mould 20 Rear door moulding 15 Spoiler 40 Front door window glass 45 Headlamp washer with cap 40 Rear door window glass 45 Parktronic, wires included (1 unit) 36 Sunroof glass 45 Mid exterior Radiator grille 60 Door handle 20 Car emblem 15 Window regulator 50 Front Bumper grille 20 Sill guard 70 Front headlamp 55 Floor 100 Front xenon headlamp 115 A-pillar 60 Front corner lights 20 Sill 80 Front fog lights 35 Roof 120 Bonnet 140 C-pillar 80 Front fender 100 B-pillar 120 Front fender liner 20 Driver airbag 115 Front part of front fender liner 20 Passenger airbag 115 Mid interior Front wheel arch 60 Automatic safety belt 55 Front wing moulding 20 Dashboard 255 Windshield 105 Rear bumper 120 Horn 7 Bumper moulding 20 Bumper core 40 Bumper spoiler 30 Side member 30 Wing lamp 55 Ignition panel 30 Door/boot lid lamp 55 Bonnet key 15 Extra fog lamp 30 Rear Headlight mounting panel 30 Boot lid 120 Radiator support 60 Rear windshield 85 Windscreen washer tank 35 Rear wing 120 Coolant tank 35 Fender liner (wheel arch) 30 Washer pump 20 Rear dash 90 Front interior Electronic control unit 55 Spare tyre cover/boot floor 90 Oil cooler 60 Car bottom Exhaust pipe 55 Intercooler 115 Steering mechanism 70 Air conditioning radiator 105 Wheel geometry alignment 20 Heat sink 85 Metal rim (1 unit) 20 Heat sink tube 15 Alloy rim (1 unit) 60 Air conditioning radiator pipes 30 Powertrain Tyre (1 unit) 40 Engine protector 40 Drive shaft/wheel bearing/lever 20 Air conditioner 55 Shock absorber 30 AC diffuser 30 Steering nozzle 15 Decorative wheel cover (1 unit) 10 Car body repair 30 Drive train repair 30 Service Restoring geometry 55 Polishing car part 20.