New Business Opportunities in Pakistan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Final GCR Combined Copy May 2013

EXECUTIVE SUMMARY FOR GLOBAL / COUNTRY STUDY REPORT (Subject Code: 2830003) ON “PAKISTAN WITH RESPECT TO LEATHER INDUSTRY” SUBMITTED TO MBA-732: SEMESTER-III & IV LDRP-INSTITUTE OF TECHNOLOGY AND RESEARCH, GANDHINAGAR. [In partial Fulfillment of the Requirement of the award for the degree of Master of Business Administration (MBA)] By Gujarat Technological University, Ahmedabad Year: 2013 Semester III & IV Guided By: Name of Guides email Id Contact Designation No. Mr. Vinit M. Mistri [email protected] 09998873083 Lecturer Ms. Hemali G. Broker [email protected] 09099012233 Lecturer Dr. Pooja M. Sharma [email protected] 09726480698 Assistant professor Ms. Sejal C. Acharya [email protected] 07698029293 Lecturer Mr. Anand Nagrecha [email protected] 09824090958 Lecturer Student’s Declaration We hereby declare that the Global/ Country Study Report titled “GLOBAL / COUNTRY STUDY REPORT (Subject Code: 2830003) ON“PAKISTAN WITH RESPECT TO LEATHER INDUSTRY” in ( PAKISTAN ) is a result of our own work and our indebtedness to other work publications, references, if any, have been duly acknowledged. If I/we are found guilty of copying any other report or published information and showing as my/our original work, or extending plagiarism limit, I understand that I/we shall be liable and punishable by GTU, which may include ‘Fail’ in examination, ‘Repeat study & re Submission of report’ or any other punishment that GTU may decide. Place: Gandhinagar Date: All Students undersigned below. Enrollment Number NAME OF THE STUDENT -

Posted Issuer

Central Depository Company of Pakistan Limited Element Report Page# : 1 of 267 User : XKYFSI2 Report Selection : Posted Date : 04/11/2020 Element Type : Issuer Time : 06:02:58 Element ID : ALL Location : ALL Status : Active From Date : 01/01/1996 To Date : 04/11/2020 Element Id Element Code Element Name Phone / Fax Contact Name CDC Loc Role Code Maximum User Status Main A/c Address eMail Address Designation Client A/c CM Option No. Date -------- -------- ------------------------ ---------------------- --------------- --------- -------- ----------- -------- 00002 EFU GENERAL 2313471-90 ALTAF QAMRUDDIN KHI Active INSURANCE LIMITED GOKAL 3RD FLOOR, 2314288 CFO AND 08/06/1998 QAMAR HOUSE, CORPORATE M. A. JINNAH ROAD, SECRETARY KARACHI. 00003 HABIB INSURANCE 111-030303 SHABBIR A. KHI Active COMPANY LIMITED GULAMALI 1ST FLOOR, STATE 32421600 CHIEF 01/09/1997 LIFE BLDG. NO. 6, EXECUTIVE HABIB SQUARE, M. A. JINNAH ROAD, [email protected] KARACHI. et 00004 HAYDARI 2411247 ALI ASGHAR KHI Active CONSTRUCTION RAJANI COMPANY LIMITED MEZZANINE FLOOR, 2637965 CHIEF 10/03/2004 UBL BUILDING, EXECUTIVE OPP. POLICE HEAD OFFICER OFFICE, I.I CHUNDRIGAR ROAD, KARACHI. 00005 K-ELECTRIC LIMITED 38709132 EXT:9403 AMJAD MUSTAFA KHI Active Central Depository Company of Pakistan Limited Element Report Page# : 2 of 267 User : XKYFSI2 Report Selection : Posted Date : 04/11/2020 Element Type : Issuer Time : 06:02:58 Element ID : ALL Location : ALL Status : Active From Date : 01/01/1996 To Date : 04/11/2020 Element Id Element Code Element Name Phone / Fax Contact Name CDC Loc Role Code Maximum User Status Main A/c Address eMail Address Designation Client A/c CM Option No. Date -------- -------- ------------------------ ---------------------- --------------- --------- -------- ----------- -------- 1ST FLOOR, 32647159 MANAGER, 01/09/1997 BLOCK-A, CORPORATE AFFAIRS POWER HOUSE, [email protected] ELANDER ROAD, KARACHI 00006 MURREE BREWERY 5567041-7 CH. -

Shell-Annual-Report-2019.Pdf

ANNUAL REPORT 2019 1 2 SHELL PAKISTAN LIMITED CONTENTS GOVERNANCE & COMPLIANCE Company Information........................................................................................................................... 06 Vision................................................................................................................................................ 07 Statement of General Business Principles.................................................................................................. 08 Chairperson’s Review............................................................................................................................ 12 Board of Directors ............................................................................................................................... 20 Report of the Directors ......................................................................................................................... 24 Notice of Anuual General Meeting ........................................................................................................ 28 Statement of Compliance ..................................................................................................................... 30 Independent Auditors’ Review Report ...................................................................................................... 33 OUR PERFORMANCE Retail ............................................................................................................................................... -

Gas and Petroleum Market Structure and Pricing

Gas and Petroleum Market Structure and Pricing Edited by Afia Malik PIDE Monograph PAKISTAN INSTITUTE OF DEVELOPMENT ECONOMICS Series ISLAMABAD All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means—electronic, mechanical, photocopying, recording or otherwise—without prior permission of the author and or the Pakistan Institute of Development Economics, P. O. Box 1091, Islamabad 44000. © Pakistan Institute of Development Economics, 2021. Pakistan Institute of Development Economics Quaid-i-Azam University Campus P. O. Box 1091, Islamabad 44000, Pakistan E-mail: [email protected] Website: http://www.pide.org.pk Fax: +92-51-9248065 Designed, composed, and finished at the Publications Division, PIDE. PIDE Monograph Series Gas and Petroleum Market Structure and Pricing Edited by Afia Malik PAKISTAN INSTITUTE OF DEVELOPMENT ECONOMICS ISLAMABAD CONTENTS CHAPTER 1: ENERGY MARKET STRUCTURE OIL AND GAS Afia Malik, Amna Urooj, Uzma Zia, Saba Anwar, and Saud Ahmad Khan 1. Introduction 1 2. Oil Market Structure and Supply Chain 2 2.1. Petroleum Supply Chain 3 2.2. Petroleum Demand 9 3. Gas Market Structure and Supply Chain 12 3.1. Gas Supply Chain 13 3.2. Gas Demand 16 3.3. LPG Supply and Demand 17 4. Regulations and Policies in Oil and Gas Sector 19 5. Challenges and Opportunities in Oil and Gas Upstream 20 6. Key Takeaways 22 References 22 CHAPTER 2: NATURAL GAS PRICES IN PAKISTAN Afia Malik and Hafsa Hina 1. Introduction 25 2. Pricing and Regulatory Regime 26 3. Gas Price Setting Framework in Pakistan 27 3.1a. -

Negativliste. Fossil Energi

Bilag 6. Negativliste. Fossil energi Maj 2017 Læsevejledning til negativlisten: Moderselskab / øverste ejer vises med fed skrift til venstre. Med almindelig tekst, indrykket, er de underliggende selskaber, der udsteder aktier og erhvervsobligationer. Det er de underliggende, udstedende selskaber, der er omfattet af negativlisten. Rækkeetiketter Acergy SA SUBSEA 7 Inc Subsea 7 SA Adani Enterprises Ltd Adani Enterprises Ltd Adani Power Ltd Adani Power Ltd Adaro Energy Tbk PT Adaro Energy Tbk PT Adaro Indonesia PT Alam Tri Abadi PT Advantage Oil & Gas Ltd Advantage Oil & Gas Ltd Africa Oil Corp Africa Oil Corp Alpha Natural Resources Inc Alex Energy Inc Alliance Coal Corp Alpha Appalachia Holdings Inc Alpha Appalachia Services Inc Alpha Natural Resource Inc/Old Alpha Natural Resources Inc Alpha Natural Resources LLC Alpha Natural Resources LLC / Alpha Natural Resources Capital Corp Alpha NR Holding Inc Aracoma Coal Co Inc AT Massey Coal Co Inc Bandmill Coal Corp Bandytown Coal Co Belfry Coal Corp Belle Coal Co Inc Ben Creek Coal Co Big Bear Mining Co Big Laurel Mining Corp Black King Mine Development Co Black Mountain Resources LLC Bluff Spur Coal Corp Boone Energy Co Bull Mountain Mining Corp Central Penn Energy Co Inc Central West Virginia Energy Co Clear Fork Coal Co CoalSolv LLC Cobra Natural Resources LLC Crystal Fuels Co Cumberland Resources Corp Dehue Coal Co Delbarton Mining Co Douglas Pocahontas Coal Corp Duchess Coal Co Duncan Fork Coal Co Eagle Energy Inc/US Elk Run Coal Co Inc Exeter Coal Corp Foglesong Energy Co Foundation Coal -

OICCI CSR Report 2018-2019

COMBINING THE POWER OF SOCIAL RESPONSIBILITY Corporate Social Responsibility Report 2018-19 03 Foreword CONTENTS 05 OICCI Members’ CSR Impact 06 CSR Footprint – Members’ Participation In Focus Areas 07 CSR Footprint – Geographic Spread of CSR Activities 90 Snapshot of Participants’ CSR Activities 96 Social Sector Partners DISCLAIMER The report has been prepared by the Overseas Investors Chamber of Commerce and Industry (OICCI) based on data/information provided by participating companies. The OICCI is not liable for incorrect representation, if any, relating to a company or its activities. 02 | OICCI FOREWORD The landscape of CSR initiatives and activities is actively supported health and nutrition related initiatives We are pleased to present improving rapidly as the corporate sector in Pakistan has through donations to reputable hospitals, medical care been widely adopting the CSR and Sustainability camps and health awareness campaigns. Infrastructure OICCI members practices and making them permanent feature of the Development was also one of the growing areas of consolidated 2018-19 businesses. The social areas such as education, human interest for 65% of the members who assisted communi- capital development, healthcare, nutrition, environment ties in the vicinity of their respective major operating Corporate Social and infrastructure development are the main focus of the facilities. businesses to reach out to the underprivileged sections of Responsibility (CSR) the population. The readers will be pleased to note that 79% of our member companies also promoted the “OICCI Women” Report, highlighting the We, at OICCI, are privileged to have about 200 leading initiative towards increasing level of Women Empower- foreign investors among our membership who besides ment/Gender Equality. -

Women Working in Fisheries at Ibrahim Hydri, Rehri Goth and Arkanabad

Pakistan Journal of Gender Studies 207 Vol. 13, pp. 207-220, ISSN: 2072-0394 Women Working In Fisheries At Ibrahim Hydri, Rehri Goth And Arkanabad Nasreen Aslam Shah Women’s Studies & Department of Social Work University of Karachi Abstract This article emerges out of my study on fisheries at Ibrahim Hydri, Rehri Goth & Arkanabad, a project assigned by Women Development Department, Government of Sindh. The overall objective of this study is to seek out information regarding the following issues: the status of women in family and community, type of work they are doing, reason of doing work and their system and mode of payment, overall their hygiene and health conditions of the women folk. Both qualitative and quantitative research methodologies were adopted for this study through which the researcher has analyzed different factors and circumstances which these women are experiencing. This study has, therefore, been conducted to explore the factual data about the women working in fisheries at Ibrahim Hydri, Rehri Goth and Arkanabad. Keywords: Fisherwomen, Health Issues, Working Conditions, Socio-Economic Status, Physical and Mental Ailment. !"#$ !"#$%&' ()*+ ,-./0 123456789:;<=>?@A 5IJ57 KDLMNO)DPQR5 STDR5@ BCDEF*@GH UVW6IJXTY Z*[\789]^*+ _@a _34D@` 6'm789nopQqrWEF@5s 9b'c5Nde fgh@PijklQ PQtWuvwxy*+ EFzPQR5*{|D 89}Dm …/ CM NdeR5,-_| :~•€ Introduction Fisheries play a significant role in the growth of national income. This sector directly provides employment to 300,000 fishermen and in addition to this another 400,000 people 208 Women Working in Fisheries at Ibrahim Hydri, Rehri Goth and Arkanabad are employed in ancillary industries. Pakistan is gifted with rich fishery potential and it is a major source of earning foreign exchange for the country. -

And Others TITLE Student Study Guide: INSTITUTION Ohio State

DCOUMENT RESUME ED'073 327 - VT 019 456 AUTHOR Daugherty, Ronald D.; And Others TITLE Highway Traffic Accident Investigation' and Reporting: Student Study Guide: INSTITUTION Ohio State Univ., Columbus. Center for Vocational and Technical Education. SPONS AGENCY' National-Highway Traffic Safety Administration (DOT), Washington, D. C. PUB DATE Dec 72 NOTE 75p. ERRS PRICE MF-$0.65 HC-$3.29 DESCRIPTORS Behavioral Objectives; Bibliographies; Course . 'Descriptions; Data Collection; *Investigations;Job Training; Learning Activities; Resource Materials; *Skill Development; *Study Guides; Technical Education; *Technical Occupations;.*Traffic Accidents; Transportation; Vocational Education; Worksheets IDENTIFIERS ,*Accident Investigation Technicians ABSTRACT This study guide for students in a basic training program for accident investigation is intended for use with lesson plans for the instructor and a manual for administratorsand planners,'available as VT 019 457 and VT+019 455, respectively.As part of a curriculum package developed by the Center for Vocational and-Technical Education after d nationwide survey, thisdocument contains a rationale detailing the needs for accident investigation technicians, an instructional outline,a course' description, extensive student worksheets, and appended resource materials. Included in this'guide, which is 3-hole punched for insertion intoa _notebook, are a bibliography, teaching suggestions, andan instructor rating sheet for student use. Intended to develop entry-level skills and to train technicians to identify, collect, record, andreport data regarding the driver, vehicle, and environmentas it relates to the pre-crash, crash, and post-crash phases ofan accident, the course consists of five flexible instructional units. Each lesson provides teaching procedures, behavioral objectives, and suggested learning activities. A related document is available ina previous issue as ED 069 848. -

Unpacking Policy Space in International Trade Law: the Auto Industry in Brazil and the United States

_________________________________________________________________________________ page i Unpacking Policy Space in International Trade Law: The Auto Industry in Brazil and the United States Ada Bogliolo Piancastelli de Siqueira Submitted in partial fulfillment of the requirements of the degree of Doctor of Juridical Science (SJD) at the Georgetown University Law Center 2019 Dissertation supervisor: Professor Alvaro Santos _________________________________________________________________________________ page ii Abstract This thesis aims to deconstruct the notion of policy space in international trade law. It presents the idea of “unpacking policy space” to suggest that policy space is not merely a concept relating to what room for policy is available under the law. Rather, it demonstrates that this commonly used concept overlooks important regulatory influences that define countries ability to regulate. The dissertation makes two main claims. First, it claims that policy space for industrial and developmental policies extends beyond WTO law and depends not only on international rules; but rather, on systems of domestic and transnational rules and regulations. Second, it argues that by analyzing how different domestic structures lead to different regulatory preferences and possibilities, this analysis provides an insight into how similar transnational and international rules translate differently into different countries. It presents four case studies that assess how the existing regulatory frameworks shaped policies for the automotive industry -

Companies Listed On

Companies Listed on KSE SYMBOL COMPANY AABS AL-Abbas Sugur AACIL Al-Abbas CementXR AASM AL-Abid Silk AASML Al-Asif Sugar AATM Ali Asghar ABL Allied Bank Limited ABLTFC Allied Bank (TFC) ABOT Abbott (Lab) ABSON Abson Ind. ACBL Askari Bank ACBL-MAR ACBL-MAR ACCM Accord Tex. ACPL Attock Cement ADAMS Adam SugarXD ADMM Artistic Denim ADOS Ados Pakistan ADPP Adil Polyprop. ADTM Adil Text. AGIC Ask.Gen.Insurance AGIL Agriautos Ind. AGTL AL-Ghazi AHL Arif Habib Limited AHSL Arif Habib Sec. AHSM Ahmed Spining AHTM Ahmed Hassan AIBL Asset Inv.Bank AICL Adamjee Ins. AJTM Al-Jadeed Tex AKDCL AKD Capital Ltd AKDITF AKD Index AKGL AL-Khair Gadoon ALFT Alif Tex. ALICO American Life ALNRS AL-Noor SugerXD ALQT AL-Qadir Tex ALTN Altern Energy ALWIN Allwin Engin. AMAT Amazai Tex. AMFL Amin Fabrics AMMF AL-Meezan Mutual AMSL AL-Mal Sec. AMZV AMZ Ventures ANL Azgard Nine ANLCPS Azg Con.P.8.95 Perc.XD ANLNCPS AzgN.ConP.8.95 Perc.XD ANLPS Azgard (Pref)XD ANLTFC Azgard Nine(TFC) ANNT Annoor Tex. ANSS Ansari Sugar APL Attock Petroleum APOT Apollo Tex. APXM Apex Fabrics AQTM Al-Qaim Tex. ARM Allied Rental Mod. ARPAK Arpak Int. ARUJ Aruj Garments ASFL Asian Stocks ASHT Ashfaq Textile ASIC Asia Ins. ASKL Askari Leasing ASML Amin Sp. ASMLRAL Amin Sp.(RAL) ASTM Asim Textile ATBA Atlas Battery ATBL Atlas Bank Ltd. ATFF Atlas Fund of Funds ATIL Atlas Insurance ATLH Atlas Honda ATRL Attock Refinery AUBC Automotive Battery AWAT Awan Textile AWTX Allawasaya AYTM Ayesha Textile AYZT Ayaz Textile AZAMT Azam Tex AZLM AL-Zamin Mod. -

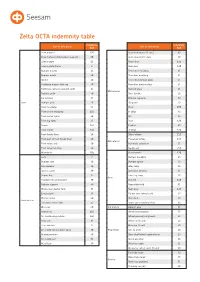

Zelta OCTA Indemnity Table

Zelta OCTA indemnity table Indemnity, Indemnity, List of auto parts List of auto parts EUR EUR Front bumper 120 Rear-view mirror (1 unit) 80 Front bumper reinforcement support 20 Rear-view mirror glass 30 Licence plate 15 Front door 120 Licence plate frame 2 Rear door 120 Bumper bracket 16 Front door moulding 15 Bumper mould 20 Rear door moulding 15 Spoiler 40 Front door window glass 45 Headlamp washer with cap 40 Rear door window glass 45 Parktronic, wires included (1 unit) 36 Sunroof glass 45 Mid exterior Radiator grille 60 Door handle 20 Car emblem 15 Window regulator 50 Front Bumper grille 20 Sill guard 70 Front headlamp 55 Floor 100 Front xenon headlamp 115 A-pillar 60 Front corner lights 20 Sill 80 Front fog lights 35 Roof 120 Bonnet 140 C-pillar 80 Front fender 100 B-pillar 120 Front fender liner 20 Driver airbag 115 Front part of front fender liner 20 Passenger airbag 115 Mid interior Front wheel arch 60 Automatic safety belt 55 Front wing moulding 20 Dashboard 255 Windshield 105 Rear bumper 120 Horn 7 Bumper moulding 20 Bumper core 40 Bumper spoiler 30 Side member 30 Wing lamp 55 Ignition panel 30 Door/boot lid lamp 55 Bonnet key 15 Extra fog lamp 30 Rear Headlight mounting panel 30 Boot lid 120 Radiator support 60 Rear windshield 85 Windscreen washer tank 35 Rear wing 120 Coolant tank 35 Fender liner (wheel arch) 30 Washer pump 20 Rear dash 90 Front interior Electronic control unit 55 Spare tyre cover/boot floor 90 Oil cooler 60 Car bottom Exhaust pipe 55 Intercooler 115 Steering mechanism 70 Air conditioning radiator 105 Wheel geometry alignment 20 Heat sink 85 Metal rim (1 unit) 20 Heat sink tube 15 Alloy rim (1 unit) 60 Air conditioning radiator pipes 30 Powertrain Tyre (1 unit) 40 Engine protector 40 Drive shaft/wheel bearing/lever 20 Air conditioner 55 Shock absorber 30 AC diffuser 30 Steering nozzle 15 Decorative wheel cover (1 unit) 10 Car body repair 30 Drive train repair 30 Service Restoring geometry 55 Polishing car part 20. -

Driving in Lahore AASIM ZAFAR KHAN Streets

VOLUME 13 | No 315 Lahore Regd No. CPI 251 6P9 SPORTS WORLD STOCKS/COMMODITIES 610 The Babar opposes Karachi Kings decision to An English Daily published simultaneously from Lahore and Faisalabad Gold falls to one-month relegate him PAGES 12 | Rs 20 Buwww.thsebusiiness.ncom.pk esRab- ul- sAwal 02, 1440, Sundlaowy, aNso Fveedm abffeirr m11s, 2018 rate-hiking stance PSX records 1.4 percent decline in outgoing week The Business Report g volatile in the near-term due to worsen- Week began on a negative note, with 1,000 points being wiped off in seven days ing economic indicators, thereby main- KARACHI: The capital market taining our cautious stance and recorded a decline of around 1.4 percent modalities not being finalised with the week with the index closing at 41,389. Tobacco 64 points, and v) Oil and Gas and Advisor to Prime Minister on tex- recommending exposure in blue-chip during the outgoing week where banks, Chinese government during Prime Min- Sector-wise negative contribution Marketing Companies 45 points. tile and industries announced that soon names. cements, oil and exploration and to- ister Imran Khan’s visit. came from Commercial Banks losing Whereas, positive contributions were package will be unfolded which would Meanwhile an analyst from BMA bacco companies witnessed battering Bulls rushed in on Wednesday with 278 points, Oil & Gas Exploration led by Fertilizer gaining 102 points and double exports to China, which helped Capital Management said that with IMF on lack clarity from the government Finance Minister Asad Umer asserting Companies 165 points amid fall in in- Technology & Communication shares 24 textile stocks gain investors’ attention.