2011 Q4 Retail

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Nepean, Rideau and Osgoode Community Resource Centre

What is the Nepean, Rideau Osgoode Community Resource Centre? The Nepean, Rideau and Osgoode Community Resource Centre (NROCRC) is a community based social service centre working in partnership with individuals, families and communities to promote optimal health, wellness and quality of life. Our office is located at Emerald Plaza in Nepean, Ontario and we serve a large proportion of the population throughout Ottawa. NROCRC is non-profit charitable organization and our services and programs are free. Our Charitable NO is 12139 6428 RR0002. The community our agency serves is large, diverse and mobile. Immigrant families, families new to the area, youth, and a growing senior population present a wide variety of needs. NROCRC supports Ottawa’s largest community population: over 200,000 people. NROCRC’s catchment area is also the largest out of all the community resource centres in Ottawa. At this time, the Tools 4 School Program is seeking donations and registrants for its 2015 campaign. What is the Tools 4 School Program? The Tools 4 School program was developed in the spring of 2000 after local newspapers acknowledged the need for school supplies for local school-aged children. This need for basic school supplies is linked directly with lower self- esteem in students and contributes to diminished school performance for children and youth in our communities. The Tools 4 School program collects the much needed supplies for school-aged children in the Ottawa Community through donations, community wide supply drives, strong partnerships and corporate challenges. Every year, the Tools 4 School program distributes school supplies to children and youth in need at the start of the school year (September 2015). -

Minto Commercial Properties Inc. Illustrative Purposes

Morgan’s Grant (Kanata) | Retail Plaza (73,000 sq. ft.) OTTAWA OVERVIEW MAP LOCATION MAP AERIAL MAP SITE MAP DUNROBIN ROAD FERRY ROAD 2001 Population and Households TORBOLTON RIDGE ROAD Zone Population Households GALETTA SIDE ROAD FITZROY PTA 6,909 2,165 HARBOUR CONSTANCE BAY STA1 14,544 5,015 QUEBEC STA2 12,790 4,470 CARP ROAD STA Total 27,334 9,485 WOODKILTON ROAD TA Total 34,243 11,650 VANCE SIDE ROAD 5 LINE ROAD Source: Statistics Canada 2001 Census Population Projections (TA Total) Year Population LOGGERS WAY JOHN SHAW ROAD DUNROBIN TORWOOD DRIVE 2005 41,200 MOHR ROAD 2010 50,500 DUNROBIN ROAD STA 2 2 LINE ROAD KERWIN ROAD KERWIN 2015 58,200 KINBURN SIDEROAD DIAMONDVIEW ROAD KINBURN PTA RIDDELL DRIVE MARCH VALLEY RD. DONALD B. MUNRO DRIVE 17 MARCHURST ROAD THOMAS A. DOLAN PARKWAY FARMVIEW ROAD MARCH ROAD OTTAWA RIVER 2 LINE ROAD UPPER DWYER HILL ROAD KLONDIKE ROAD CARP MARCH ROAD LEGGET DRIVESANDHILL ROAD THOMAS ARGUE ROAD TERRY FOX DRIVE SUBJECT SITE GOULBOURNFORCEDRD. SHANNA ROAD HINES ROAD CARLING AVENUEOTTAWA DIAMONDVIEW ROAD OLD CARPKANATA ROAD TERON ROAD CARP ROAD MARSHWOOD ROAD 417 417 HUNTMARSTA DRIVE 1 CONCESSION ROAD 12 OLD CREEK DRIVE TIMM ROAD CAMPEAU DRIVE ROBERTSON ROAD PANMURE ROAD MARCH ROAD PALLADIUM DRIVE HAZELDEAN ROAD RICHARDSON SIDE ROAD MAPLE GROVE ROAD 7 STITTSVILLE For discussion and/or Minto Commercial Properties Inc. illustrative purposes. Subject to change without notice 613-786-3000 minto.com Morgan’s Grant (Kanata) | Retail Plaza (73,000 sq. ft.) OTTAWA OVERVIEW MAP LOCATION MAP AERIAL MAP SITE MAP Future Residential Existing Future Residential Residential MARCH ROAD KLONDIKE ROAD FLAMBOROUGH WAY MERSEY DRIVE MORGAN’S GRANT For discussion and/or Minto Commercial Properties Inc. -

Ward 16 Master THEME EN

Draft Budget 2020 – Ward 16 – River Councillor Riley Brockington Ward investments in 2020 Infrastructure • $31.2 million on infrastructure, including: o $5.5 million to rehabilitate Mooney’s Bay trunk sewer o $6.8 million for integrated road, sewer, and water work along Claymor and Senio avenues o $5.9 million for integrated road, sewer and water work along Larkin Street, Larose Avenue and Lepage Avenue o $8.8 million on structure renewal, including culverts along the Airport Parkway at Walkley Road, and O-Train overpasses at Heron Road, Riverside Drive and Walkley Road o $3.95 million to resurface Riverside Drive between Hunt Club and Walkley roads Transportation • $817 million to fund Stage 2 of Ottawa’s light-rail transit system, extending service to Limebank Station with a link to the Ottawa Macdonald–Cartier International Airport, adding 12 kilometres and eight stations along the Trillium Line, south of Greenboro Station • $125,000 to reconstruct sidewalks and curbs to improve road safety along McCarthy Road between Plante Drive and the rail crossing • $30,000 to apply high-friction asphalt on Prince of Wales Drive at Kochar Drive • $20,000 to repair streetlight cables at Kenzie Street and Leaside Avenue • $6,000 to replace streetlight poles on Riverside Drive at Malhotra Court Parks and facilities • $500,000 on renewal projects, including: o $85,000 for building improvements to the Water Services facility on Clyde Avenue o $80,000 for upgrades to the Deborah Anne Kirwan Pool o $270,000 for concrete walkways and retaining walls at -

Project Synopsis

Final Draft Road Network Development Report Submitted to the City of Ottawa by IBI Group September 2013 Table of Contents 1. Introduction .......................................................................................... 1 1.1 Objectives ............................................................................................................ 1 1.2 Approach ............................................................................................................. 1 1.3 Report Structure .................................................................................................. 3 2. Background Information ...................................................................... 4 2.1 The TRANS Screenline System ......................................................................... 4 2.2 The TRANS Forecasting Model ......................................................................... 4 2.3 The 2008 Transportation Master Plan ............................................................... 7 2.4 Progress Since 2008 ........................................................................................... 9 Community Design Plans and Other Studies ................................................................. 9 Environmental Assessments ........................................................................................ 10 Approvals and Construction .......................................................................................... 10 3. Needs and Opportunities .................................................................. -

Building Profile Corporate Holdings

® Known By The Company We Keep 2339 OGILVIE ROAD Corporate Holdings Building Profile OFFICE DOWNTOWN 75 Albert Street The downtown portfolio of 6 buildings captures over 800,000 square feet in 85 Albert Street National Capital’s coveted business district east from Bank Street to Elgin 116 Albert Street Street and south from Parliament Hill to Slater Street, providing opportunities 123 Slater Street for business professionals with office requirements from as small as 250 square 130 Albert Street feet to full floors of over 10,000 square feet. The downtown properties all reside 151 Slater Street within walking distance of Parliament Hill, the Banking district, the Ottawa Convention Centre, the Courthouse, the National Arts Centre, the Sparks Street Beacon Hill Shopping Centre promenade, major hotels and the Byward Market and Rideau Street shopping is an enclosed shopping mall district. serving the consumer needs of the growing family OFFICE CENTRETOWN community of Gloucester, 150 Isabella Street These multi-tenant buildings strategically located on high traffic routes, allow just southeast of Ottawa's 1385 Bank Street for excellent visibility and for easy access from the Queensway or from other major traffic routes across the City. For the commuter, they are equally city centre. The mall's accessible by rapid transit for tenant and client alike. Tenants include a Bank of Nova Scotia, Shoppers Drug 7 Hinton Avenue Mart, a Butcher, a Bakeshop, 161 Greenbank Road OFFICE SUBURBAN Post Office, Tailor, Hairstylist 1770 Woodward Drive From eclectic to traditional, the 6 suburban properties are located on and other such commercial 1926 Merivale Road strategic corners or are nestled in established business park settings. -

1600 Merivale Road REALTY INC., BROKERAGE Unit 10 - 1,460 Sq.Ft

LEASING OPPORTUNITY 1600 Merivale Road REALTY INC., BROKERAGE Unit 10 - 1,460 sq.ft. ✓ Highly visible location on prime ✓ Excellent visibility and parking Merivale corridor ✓ High traffic location: 57,436 vehicles ✓ Bright open concept space, with daily (City of Ottawa 2014 traffic count) laminate flooring ✓ Pylon signage available Prominent signage available above ✓ Op-Costs: $13.10/sq.ft. (2016) storefront ✓ ✓ Join Swiss Chalet, Domino's Pizza, Living Lighting and more. Unit 10 www.colonnadebridgeport.ca LEASING OPPORTUNITY 1600 Merivale Road Unit 10 - 1,460 sq.ft. Merivale Road Aerial Merivale Road Merivale Road Meadowlands Drive and Clyde Avenue and Clyde Avenue Merivale Rd. & West Daily Traffic Baseline Road Hunt Club Rd. Clyde Avenue 57,436 (City of Ottawa Traffic Count 2014) Merivale Road Merivale Road Merivale Road Merivale Rd. & Baseline Road. 1600 Merivale Meadowlands Drive West Hunt Club Road Merivale Road Colonnade Road www.colonnadebridgeport.ca Client: Bridgeport Realty Management Bridgeport Realty Management Version: Prepared: 20/06/2016 FP1A Measured: 14/05/2016 1600 Merivale Road Ottawa, Ontario Floor 01 LEASING OPPORTUNITY SUITE 16 1600 Merivale Road Unit 10 - 1,460 sq.ft. Please Refer to Corresponding Area Chart Merivale Road UP ELEV SUITE 11 SUITE 12 SUITE 14 SUITE 15 SUITE 3 SUITE 4 SUITE 5 SUITE 6 SUITE 7 SUITE 8 SUITE 10 SUITE 9 SUITE 13 UP CH=132.6" NO ACCESS WALK-IN FREEZER WALK-IN COOLER WALK-IN WALK-IN FREEZER FREEZER TELE. WOMEN WALK-IN WALK-IN LOCKER FREEZER ROOM FREEZER . ELEC. ELEC ELEC ELEC ELEC. MEN WH LOCKER ROOM ELECTRICAL . DN DN ROOM UP DN METER DN UP W H W H ROOM CH=131.7" ELEC CH=134.9" WH ELEC. -

Staltari's Transactions

Completed transactions Office The following are some of Mario Staltari’s transactions. Industrial Commercial Investment East Ottawa - Warehouse East Ottawa - Warehouse East Ottawa - Office West Ottawa - Warehouse 2750 Sheffield Road 2001 Bantree Road 2465 St. Laurent Boulevard (sold twice) 1600 Scott Street & 11 Holland Avenue 67,000 sq ft 257,788 sq ft 60,000 sq ft 242,000 sq ft Nepean - Retail/Office Kanata - Office Central Ottawa - Office Nepean - Office 1600 Merivale Road 580 Terry Fox Drive 434 Queen Street 245 Stafford Road (sold twice) 37,500 sq ft 38,500 sq ft 45,000 sq ft 35,000 sq ft East Ottawa - Office East Ottawa - Warehouse East Ottawa - Warehouse Stittsville - Warehouse 2713 Lancaster 1580-1590 Liverpool Court (sold twice) 1315-1317 Michael Street (sold twice) 5997 Hazeldean Road 34,500 sq ft 35,742 sq ft 20,109 sq ft 77,000 sq ft Completed transactions Office The following are some of Mario Staltari’s transactions. Industrial Commercial Investment East Ottawa Stittsville - Retail East Ottawa - School Kanata - Office/Retail 435 Donald Street 1250 Main Street 1644 Bank Street 150 Katimavik Road 19,630 sq ft 37,000 sq ft 46,800 sq ft 110,000 sq ft sq ft East Ottawa - Warehouse East Ottawa - Warehouse East Ottawa - Warehouse East Ottawa - Warehouse 1117-1141 Newmarket Road 1255 Leeds Avenue 2750-2772 Lancaster Road 2660-2678 Lancaster Road 51,114 sq ft 305,000 sq ft 38,083 sq ft 45,131 sq ft East Ottawa - Warehouse East Ottawa - Warehouse For Sale - Pembroke East Ottawa - Office 2700 Lancaster Road 2710 Lancaster Road 141 Lake Street 2200 Walkey Road 34,653 sq ft 34,957 sq ft 37,000 sq ft 54,100 sq ft Completed transactions Office The following are some of Mario Staltari’s transactions. -

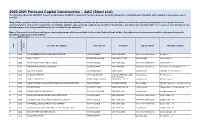

2021 Forecast Capital Construction - AAC (Short List) the List Below Shows the 2020/2021 Projects on Which Your Feedback Is Requested

2020-2021 Forecast Capital Construction - AAC (Short List) The list below shows the 2020/2021 projects on which your feedback is requested. For these projects, the City of Ottawa Accessibility Design Standards will be applied to the greatest extent possible. Many of these projects contain exterior paths of travel for which the potention provision and placement of a rest area will be decided in the upcoming design phase of the project based on numerous factors, such as the results of the consultation, available space, property requirements, location of transit stops, and volume of pedestrian traffic. If a rest area is to be provided on an individual project, its design would follow the Accessibility Design Standards. Many of the projects listed have existing on-street parking areas which are available to Accessible Parking Permit holders. Any adjustments to those areas would be determined during the upcoming design phase of the project. May 07, 2020 Location Description From Street To Street Type of Work Ward Description Item Year Construction Construction 1 2020 OLD GREENBANK ROAD AND KILBIRNIE DRIVE NOT AVAILABLE NOT AVAILABLE Intersection Modifications Jan Harder - 3 2 2020 VARLEY DRIVE BEAVERBROOK LANE CARR CRESECENT New Sidewalks Jenna Sudds - 4 3 2020 MARCH ROAD AND STREET C AND E NOT AVAILABLE NOT AVAILABLE Intersection Modifications Eli El-Chantiry - 5 4 2020 FERNBANK ROAD AND COPE DRIVE NOT AVAILABLE NOT AVAILABLE Intersection Modifications Glen Gower - 6, Scott Moffatt - 21 5 2020 CEDARVIEW ROAD RICHMOND ROAD BRUIN ROAD Cycling -

Pathway Network for Canada's Capital Region 2006 Strategic Plan PLANI

Pathway Network for Canada’s Capital Region 2006 Strategic Plan PLANI-CITÉ i June 2006 Pathway Network for Canada’s Capital Region 2006 Strategic Plan THE VISION The National Capital Commission (NCC) and its partners propose the following as a framework for the planning and development of the Capital Pathway network for the next 10 years: Multi-purpose use The Capital Pathway network covers Canada’s Capital Region in its entirety. It is a multi-purpose recreational and tourist network, which also supports non-motorized commuting vocations. Accessibility and safety The network extends to and links natural and built areas. Through its layout and design standards, the network encourages a quality user experience and accessibility, emphasizing the recognition of the “Green Capital”, and highlighting symbolic points of interest within the Capital. The network provides access to waterways, green spaces, cultural and heritage features while supporting the protection of natural areas and offering a wide range of easily accessible services. User education and awareness programs targeting pathway sharing in a respectful and tolerant manner result in a safe and pleasant experience. Connectivity The network, through its linkage with local cycling routes and regional/national trails, is connected to other non-motorized transportation networks within the region to encourage sustainable transportation and forms a key component of Canada’s Capital recreational and cycling experience. Recognition The network, as a result of its multi use vocation, its extensive and far reaching system of pathways and connection with regional, provincial and national trails and pathways within and outside Canada’s Capital Region as well as the quality of the experience is regarded as one of North America’s best. -

Welcome to Kanata North Message from Councillor Wilkinson

WELCOME TO KANATA NORTH MESSAGE FROM COUNCILLOR WILKINSON anata North is the most fantastic ward in the City of Ottawa. As well as the Kanata North Business K Park, the largest employment area outside the City core, it contains natural environment lands, a provincially significant wetland, distinctive residential areas, the town centre that serves both Kanata North and Kanata South, schools, churches and retail areas. Just across Highway 417 is Canadian Tire Place, the home of the Ottawa Senators, and under construction is an outlet mall and Bass Pro Shop. I’ve had the great opportunity of representing this area on municipal councils for 25 years, with 9 of those years as Head of Council and 7 of those years as Mayor of Kanata, when Kanata was a separate municipality. My job is to serve all aspects of the community, from individual con- cerns to dealing with large developments and the services they need. Welcome to Kanata North. Feel free to contact me via phone 613-580-2474 or email Marianne.Wilkinson@ ottawa.ca if you have any concerns or suggestions to make Kanata North an even better place. MESSAGE FROM KANATA NORTH BIA anata North is a fantastic place to live, work and play. We have over 500 businesses doing incredible work K – and yet we have access to green space and many, many trails, right outside our door. Truthfully, we think there is no better place! The Kanata North BIA works hard every day to support our local businesses, and to promote the area as a center of expertise in technology and innovation. -

Date Printed: 04/09/2009 JTS Box Number: IFES 61 Tab Number: 2

Date Printed: 04/09/2009 JTS Box Number: IFES 61 Tab Number: 2 Document Title: Are you on the List? Document Date: n.d. Document Country: Canada Document Language: English IFES 10: CE00434 re ou on t e ist? Did you know that you must be on the voters list to vote in the upcoming federal election? Elections Canada is mailing you: YOUR NAME YOUR AODRESS • an information pamphlet. It gives you ",..... ,."..w,,',_, ,~.. "w,,,. ".w everything you need to know about ..J voting on election day. It also explains how you can register and vote before election day. This information is also available in many languages on the Elections Canada Web site at www.elections.ca • your personal voter information card. It tells you that you are on the voters list, and says where and when you can vote. If you do not receive your voter information card in the mail, you might not be registered to vote. If your card does not arrive and you want to know whether you are on the voters list, call I 800 463-6868. Canadians outside the country can also vote. If family members, friends or employees are not in Canada, please tell them that they can find out how to register and vote by visiting our Web site. How to contact Elections Canada: call I 800 463-6868 'Ii TTY (for persons who are deaf or hard of hearing): I 800 36r-8935 Web site: www.elections.ca If you know someone who has difficulty reading, please tell them what you have read here. -

Phase One Environmental Site Assessment 950 Terry Fox Drive Ottawa, Ontario

Phase One Environmental Site Assessment 950 Terry Fox Drive Ottawa, Ontario Houle Chevrier Engineering Ltd. • 180 Wescar Lane • Ottawa, Ontario • K0A 1L0 • www.hceng.ca Submitted to: SPB Developments Inc. 114 Arbourbrook Blvd. Ottawa, Ontario K0A 1L0 Phase One Environmental Site Assessment 950 Terry Fox Drive Ottawa, Ontario September 11, 2014 Project: 14-346 Houle Chevrier Engineering Ltd. • 180 Wescar Lane • Ottawa, Ontario • K0A 1L0 • www.hceng.ca EXECUTIVE SUMMARY Houle Chevrier Engineering Ltd. (HCEL) was retained by SPB Developments Inc. to carry out a Phase One Environmental Site Assessment (ESA) for the properties located at 950 Terry Fox Drive and the southeast portion of the adjacent property located at 820 Terry Fox Drive in Ottawa, Ontario (hereafter collectively referred to as “the subject property”). The primary objective of this Phase One ESA was to identify any former or current potentially contaminating activities at the subject property and its vicinity to determine if they create any areas of potential environmental concern on the subject property. This Phase One ESA was carried out in accordance with Ontario Regulation 153/04 made under the Environmental Protection Act and meets the requirements of Part VII (Sections 23 to 31) and Schedule D of the regulation. Section 1.0 of this report provides a brief description of the site and Section 2.0 of this report provides the scope of investigation. Section 3.0 presents the findings of the records review. Section 4.0 presents the results of the interviews conducted. Section 5.0 presents the findings of the site reconnaissance. Section 6.0 provides a review and evaluation of information gathered.