Russian Electricity Reform

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Specialised Asset Management

specialised research and investment group Russian Power: The Greatest Sector Reform on Earth www.sprin-g.com November 2010 specialised research and investment group Specialised Research and Investment Group (SPRING) Manage Investments in Russian Utilities: - HH Generation - #1 among EM funds (12 Months Return)* #2 among EM funds (Monthly return)** David Herne - Portfolio Manager Previous positions: Member, Board of Directors - Unified Energy Systems, Federal Grid Company, RusHydro, TGK-1, TGK-2, TGK-4, OGK-3, OGK-5, System Operator, Aeroflot, etc. (2000-2008) Chairman, Committee for Strategy and Reform - Unified Energy Systems (2001-2008) Boston Consulting Group, Credit Suisse First Boston, Brunswick. * Top 10 (by 12 Months Return) Emerging Markets (E. Europe/CIS) funds in the world by BarclayHedge as of 30 September 2010 ** Top 10 (by Monthly Return) Emerging Markets (E. Europe/CIS) funds in the world by BarclayHedge as of 31 August 2010 2 specialised research and investment group Russian power sector reform: Privatization Pre-Reform Post-Reform Government Government 52% 1 RusHydro 1 FSK RAO ES RAO UES 58% 79% hydro generation HV distribution 53% Far East Holding control control Independent energos 53% 1 MRSK Holding 14 TGKs 0% (Bashkir, Novosibirsk, ~72 energos 0% generation (CHP) generation Irkutsk, Tat) 35 federal plants transmission thermal 11 MRSK distribution 51% hydro LV distribution 0% ~72 SupplyCos supply 6 OGKs other 0% generation 45% InterRAO 0% ~100 RepairCos Source: UES, Companies Data, SPRING research 3 specialised research -

Energy Without Borders

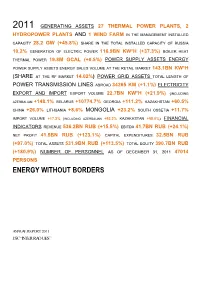

2011 GENERATING ASSETS 27 THERMAL POWER PLANTS, 2 HYDROPOWER PLANTS AND 1 WIND FARM IN THE MANAGEMENT INSTALLED CAPACITY 28.2 GW (+45.8%) SHARE IN THE TOTAL INSTALLED CAPACITY OF RUSSIA 10.2% GENERATION OF ELECTRIC POWER 116.9BN KW*H (+37.3%) BOILER HEAT THERMAL POWER 19.8M GCAL (+0.5%) POWER SUPPLY ASSETS ENERGY POWER SUPPLY ASSETS ENERGY SALES VOLUME AT THE RETAIL MARKET 143.1BN KW*H (SHARE AT THE RF MARKET 14.02%) POWER GRID ASSETS TOTAL LENGTH OF POWER TRANSMISSION LINES ABROAD 34265 KM (+1.1%) ELECTRICITY EXPORT AND IMPORT EXPORT VOLUME 22.7BN KW*H (+21.9%) (INCLUDING AZERBAIJAN +148.1% BELARUS +10774.7% GEORGIA +111.2% KAZAKHSTAN +60.5% CHINA +26.0% LITHUANIA +8.6% MONGOLIA +23.2% SOUTH OSSETIA +11.7% IMPORT VOLUME +17.2% (INCLUDING AZERBAIJAN +93.2% KAZAKHSTAN +58.0%) FINANCIAL INDICATORS REVENUE 536.2BN RUB (+15.5%) EBITDA 41.7BN RUB (+24.1%) NET PROFIT 41.5BN RUB (+123.1%) CAPITAL EXPENDITURES 32.5BN RUB (+97.0%) TOTAL ASSETS 531.9BN RUB (+113.5%) TOTAL EQUITY 390.7BN RUB (+180.9%) NUMBER OF PERSONNEL AS OF DECEMBER 31, 2011 47014 PERSONS ENERGY WITHOUT BORDERS ANNUAL REPORT 2011 JSC “INTER RAO UES” Contents ENERGY WITHOUT BORDERS.........................................................................................................................................................1 ADDRESS BY THE CHAIRMAN OF THE BOARD OF DIRECTORS AND THE CHAIRMAN OF THE MANAGEMENT BOARD OF JSC “INTER RAO UES”..............................................................................................................8 1. General Information about the Company and its Place in the Industry...........................................................10 1.1. Brief History of the Company......................................................................................................................... 10 1.2. Business Model of the Group..........................................................................................................................12 1.4. -

Annual Report ‘06 Contents

ANNUAL REPORT ‘06 CONTENTS MESSAGE TO SHAREHOLDERS ————————————————————————————— 4 MISSION AND STRATEGY ———————————————————————————————— 7 COMPANY OVERVIEW ————————————————————————————————— 13 ² GENERAL INFORMATION 13 ² GEOGRAPHIC LOCATION 14 ² CALENDAR OF KEY 2006 EVENTS 15 ² REORGANIZATION 16 CORPORATE GOVERNANCE —————————————————————————————— 21 ² PRINCIPLES AND DOCUMENTS 21 ² MANAGEMENT BODIES OF THE COMPANY 22 ² CONTROL BODIES 39 ² AUDITOR 40 ² ASSOCIATED AND AFFILIATED COMPANIES 40 ² INTERESTED PARTY TRANSACTIONS 41 SECURITIES AND EQUITY ——————————————————————————————— 43 ² CHARTER CAPITAL STRUCTURE 43 ² STOCK MARKET 44 ² DIVIDEND HISTORY 48 ² REGISTRAR 49 OPERATING ACTIVITIES. KEY PERFORMANCE INDICATORS ——————————————— 51 ² GENERATING FACILITIES 51 ² FUEL SUPPLY 52 ² ELECTRICITY PRODUCTION 56 ² HEAT PRODUCTION 59 ² BASIC PRODUCTION ASSETS REPAIR 59 ² INCIDENT AND INJURY RATES. OCCUPATIONAL SAFETY 60 ² ENVIRONMENTAL SAFETY 61 ELECTRICITY AND HEAT MARKETS ——————————————————————————— 65 ² COMPETITIVE ENVIRONMENT. OVERVIEW OF KEY MARKETS 65 ² ELECTRICITY AND HEAT SALES 67 FINANCIAL OVERVIEW ————————————————————————————————— 73 ² FINANCIAL STATEMENTS 73 ² REVENUES AND EXPENSES BREAKDOWN 81 INVESTMENT ACTIVITIES ———————————————————————————————— 83 ² INVESTMENT STRATEGY 83 ² INVESTMENT PROGRAM 84 ² INVESTMENT PROGRAM FINANCING SOURCES 86 ² DEVELOPMENT PROSPECTS 87 INFORMATION TECHNOLOGY DEVELOPMENT —————————————————————— 89 PERSONNEL AND SOCIAL POLICY. SOCIAL PARTNERSHIP ———————————————— 91 INFORMATION FOR INVESTORS AND SHAREHOLDERS —————————————————— -

a Leading Energy Company in the Nordic Area

- a leading energy company in the Nordic area Presentation for investors September 2007 Disclaimer This presentation does not constitute an invitation to underwrite, subscribe for, or otherwise acquire or dispose of any Fortum shares. Past performance is no guide to future performance, and persons needing advice should consult an independent financial adviser. 2 • Fortum today • European power markets • Russia • Financials / outlook • Supplementary material 3 Fortum's strategy Fortum focuses on the Nordic and Baltic Rim markets as a platform for profitable growth Become the leading Become the power and heat energy supplier company of choice Benchmark business performance 4 Presence in focus market areas Nordic Generation 53.2 TWh Electricity sales 60.2 TWh Distribution cust. 1.6 mill. Electricity cust. 1.3 mill. NW Russia Heat sales 20.1 TWh (in associated companies) Power generation ~6 TWh Heat production ~7 TWh Baltic countries Heat sales 1.0 TWh Poland Distribution cust. 23,000 Heat sales 3.6 TWh Electricity sales 8 GWh 2006 numbers 5 Fortum Business structure Fortum Markets Fortum's comparable Large operating profit in 2006 NordicNordic customers EUR 1,437 million Fortum wholesalewholesale Small Power marketmarket customers Generation Nord Pool and Markets 0% bilateral Other retail companies Deregulated Distribution 17% Regulated Transmission Power and system Fortum Heat 17% Generation services Distribution 66% 6 Strong financial position ROE (%) EPS, cont. (EUR) Total assets (EUR billion) 20 1.50 1.42 20.0 16.8 17.5 17.3 1.22 18 15.1 -

1 GOLDEN RING TOUR – PART 3 Golden Gate, Vladimir

GOLDEN RING TOUR – PART 3 https://en.wikipedia.org/wiki/Golden_Gate,_Vladimir Golden Gate, Vladimir The Golden Gate of Vladimir (Russian: Zolotye Vorota, Золотые ворота), constructed between 1158 and 1164, is the only (albeit partially) preserved ancient Russian city gate. A museum inside focuses on the history of the Mongol invasion of Russia in the 13th century. 1 Inside the museum. 2 Side view of the Golden Gate of Vladimir. The Trinity Church Vladimir II Monomakh Monument, founder http://ermakvagus.com/Europe/Russia/Vladimir/trinity_church_vladimir.html https://en.wikipedia.org/wiki/Vladimir_II_Monomakh 3 https://en.wikipedia.org/wiki/Dormition_Cathedral,_Vladimir The Dormition Cathedral in Vladimir (sometimes translated Assumption Cathedral) (Russian: Собор Успения Пресвятой Богородицы, Sobor Uspeniya Presvyatoy Bogoroditsy) was a mother church of Medieval Russia in the 13th and 14th centuries. It is part of a World Heritage Site, the White Monuments of Vladimir and Suzdal. https://rusmania.com/central/vladimir-region/vladimir/sights/around-sobornaya- ploschad/andrey-rublev-monument Andrey Rublev monument 4 5 Cathedral of Saint Demetrius in Vladimir https://en.wikipedia.org/wiki/Cathedral_of_Saint_Demetrius 6 7 Building of the Gubernia’s Administration museum (constructed in 1785-1790). Since 1990s it is museum. January 28, 2010 in Vladimir, Russia. Interior of old nobility Palace (XIX century) 8 Private street vendors 9 Water tower https://www.advantour.com/russia/vladimir/water-tower.htm 10 Savior Transfiguration church https://www.tourism33.ru/en/guide/places/vladimir/spasskii-i-nikolskiy-hramy/ Cities of the Golden Ring 11 Nikolo-Kremlevskaya (St. Nicholas the Kremlin) Church, 18th century. https://www.tourism33.ru/en/guide/places/vladimir/nikolo-kremlevskaya-tcerkov/ Prince Alexander Nevsky (Невский) https://en.wikipedia.org/wiki/Alexander_Nevsky 12 Just outside of Suzdal is the village of Kideksha which is famous for its Ss Boris and Gleb Church which is one of the oldest white stone churches in Russia, dating from 1152. -

Kiyameti Beklerken: Hiristiyanlik'ta

Hitit Üniversitesi Đlahiyat Fakültesi Dergisi, 2008/2, c. 7, sayı: 14, ss. 5-36. KIYAMETİ BEKLERKEN: HIRİSTİYANLIK’TA KIYAMET BEKLENTİLERİ VE RUS ORTODOKS KİLİSESİNDEKİ YANSIMALARI Cengiz BATUK * Özet Kıyameti Beklerken: Hıristiyanlık’ta Kıyamet Beklentileri ve Rus Ortodoks Kilise- sindeki Yansımaları Bu çalışmanın amacı Hıristiyan tarihindeki kıyamet beklentilerini araştırmaktır. Hıristiyanlıktaki kıyamet beklentileri genellikle binyılcı ve Mesihçi hareketler şeklinde ortaya çıktığı için çalışmanın ilk bölümünde bu hareketlerden bir kısmı hakkında değerlendirmeler yapılmıştır. Đkinci bölümde Rus Ortodoks Kilisesi tarihinde apokaliptik hareketler hakkında incelemeler yapılmıştır. Bu hareketlerden bazıları Pyotr Kuznetsov’un kıyamet kültü, castrati ve neo-castrati tarikatları, Sergei Torop’un Son Ahit Kilisesi ve Mesihçiler/Flagellant hareketleridir. Anahtar kelimeler : Kıyamet Kültü, Binyılcılık, Apokaliptisizm, Mesihçilik, Ortodoks Kilisesi, Pyotr Kuznetsov, Sergei Torop, Skoptsy -Castrati. Abstract To Await Doomsday: Expectations of Doomsday in the Christianity and Reflections in the Russian Orthodox Church The Purpose of this article is to examine expectations of doomsday in the history of Christianity. Since expectations of doomsday in Christianity appears in form of millenarianist and messianic sects, analyzes have been done some of this sects in first chapter of the study. In second chapter, investigations have been done about apocalyptic movements in history of Russian Orthodox Church. Some of these movements are Pyotr Kuznetsov’s doomsday cult, sects of castrati and neo- castrati, Sergei Torop’s Church of the Last Testament and sect of Khristovshchina/Flagellant. Key words : Doomsday Cult, Millenarianism, Apocalypticism, Ortodox Church, Messianism, Pyotr Kuznetsov, Sergei Torop, Skoptsy–Castrati. * Yrd. Doç. Dr., Rize Üniversitesi İlahiyat Fakültesi Dinler Tarihi Anabilim Dalı. Hitit Üniversitesi Đlahiyat Fakültesi Dergisi, 2008/2, c. 7, sayı: 14 6 | Yrd. -

2018 FIFA WORLD CUP RUSSIA'n' WATERWAYS

- The 2018 FIFA World Cup will be the 21st FIFA World Cup, a quadrennial international football tournament contested by the men's national teams of the member associations of FIFA. It is scheduled to take place in Russia from 14 June to 15 July 2018,[2] 2018 FIFA WORLD CUP RUSSIA’n’WATERWAYS after the country was awarded the hosting rights on 2 December 2010. This will be the rst World Cup held in Europe since 2006; all but one of the stadium venues are in European Russia, west of the Ural Mountains to keep travel time manageable. - The nal tournament will involve 32 national teams, which include 31 teams determined through qualifying competitions and Routes from the Five Seas 14 June - 15 July 2018 the automatically quali ed host team. A total of 64 matches will be played in 12 venues located in 11 cities. The nal will take place on 15 July in Moscow at the Luzhniki Stadium. - The general visa policy of Russia will not apply to the World Cup participants and fans, who will be able to visit Russia without a visa right before and during the competition regardless of their citizenship [https://en.wikipedia.org/wiki/2018_FIFA_World_Cup]. IDWWS SECTION: Rybinsk – Moscow (433 km) Barents Sea WATERWAYS: Volga River, Rybinskoye, Ughlichskoye, Ivan’kovskoye Reservoirs, Moscow Electronic Navigation Charts for Russian Inland Waterways (RIWW) Canal, Ikshinskoye, Pestovskoye, Klyaz’minskoye Reservoirs, Moskva River 600 MOSCOW Luzhniki Arena Stadium (81.000), Spartak Arena Stadium (45.000) White Sea Finland Belomorsk [White Sea] Belomorsk – Petrozavodsk (402 km) Historic towns: Rybinsk, Ughlich, Kimry, Dubna, Dmitrov Baltic Sea Lock 13,2 White Sea – Baltic Canal, Onega Lake Small rivers: Medveditsa, Dubna, Yukhot’, Nerl’, Kimrka, 3 Helsinki 8 4,0 Shosha, Mologa, Sutka 400 402 Arkhangel’sk Towns: Seghezha, Medvezh’yegorsk, Povenets Lock 12,2 Vyborg Lakes: Vygozero, Segozero, Volozero (>60.000 lakes) 4 19 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 30 1 2 3 6 7 10 14 15 4,0 MOSCOW, Group stage 1/8 1/4 1/2 3 1 Estonia Petrozavodsk IDWWS SECTION: [Baltic Sea] St. -

Rostov Kremlin), Finift Museum (Traditional Craft)

SPECIAL OFFER GEMS OF MORE THAN TRAVEL THE GOLDEN RING TAILOR-MADE TOURS TO 10 days RUSSIA 31 July – 9 August, 2020 ___________________________ In-depth cultural tour ENQUIRIES: through millennia of [email protected] Russia’s history USA: +1 (646) 751 78 53 10d/9n Australia: +61 2 8310 7667 New Zealand: +64 428 07 471 This package is available Canada: +1 888 644 87 34 either Group Tour (scheduled departures) UK & Europe: +44 20 3608 2859 or Private Tour (flexible dates) www.discoveryrussia.com 1Safe. Secure.2 Reliable.3 . • Australian-owned • Over 10 years • 24/7 support in company experience in Australia and Russia Russia Day 1– Vladimir/Bogolyubovo Day 2 – Suzdal Day 3– Schurovo Gorodische/ Kideksha Day 4 – Plyos Day 5 – Kostroma Day 6 – Kostroma Day 7 – Karabikha/Yaroslavl Day 8 – Yaroslavl Day 9 – Rostov Day 10 - Departure ex Moscow Russian visa OPTION A • get you personal Visa Support Letter (VSL) • fill in Visa Application form • send Application, passport, photo and VSL to the Embassy • get your Russian visa delivered to you by mail OPTION B • request full Russian visa service and get your visa DAY 1: Vladimir & Bogolyobovo Unique and the most ancient Russian Pokrova-na-Nerli Church of the 12 century located on the Nerl river among picturesque meadows. • Transfer from Moscow to Vladimir town (UNESCO World Heritage Site). Centuries before Mr. Putin, Russia had much more valuable “Vladimir” asset: Andrey Rublev’s frescoes, stone carving, and cathedrals; guided tour • Transfer to the village of Bogolyubovo by private transportation & excursion in the unique Bogolyubovo Pokrov na Nerli church (UNESCO World Heritage Site) • Late evening, transfer to Suzdal by private transportation (45 min drive) • Group departure: welcome dinner & vodka degustation • Unic the most ancient Russian Pokrova-na-Nerli Church of the 12 century located on the Nerl river among picturesque meadows. -

2017 Annual Report of PJSC Inter RAO / Report on Sustainable Development and Environmental Responsibility

INFORMATION TRANSLATION Draft 2017 Annual Report of PJSC Inter RAO / Report on Sustainable Development and Environmental Responsibility Chairman of the Management Board Boris Kovalchuk Chief Accountant Alla Vainilavichute Contents 1. Strategic Report ...................................................................................................................................................................................... 8 1.1. At a Glance .................................................................................................................................................................................. 8 1.2. About the Report ........................................................................................................................................................................ 11 Differences from the Development Process of the 2016 Report ............................................................................................................ 11 Scope of Information ............................................................................................................................................................................. 11 Responsibility for the Report Preparation .............................................................................................................................................. 11 Statement on Liability Limitations ......................................................................................................................................................... -

Journal American Historical Society of Germans from Russia

Journal of the American Historical Society of Germans from Russia Winter 1998 Volume 21. No. 4 Editor JO ANN KUHR AHSGR Headquarters, Lincoln, Nebraska Editorial Board IRMGARD HEDM ELLINGSON PETER J.KLASSEN Bukovina Society, Ellis, K.S California State University, Fresno ARTHUR E.FLEGEL TIMOTHY KLOBERDANZ Certified Genealogist, Menio Park, CA North Dakota State University, Fargo ADAM GIESINGER GEORGE KUFELDT University of Manitoba, Canada, emeritus Anderson University, Indiana, emeritus CHRIS LOVETT NANCY BERNHARDT HOLLAND Emporia State University, Kansas Trinity College, Burlington, VT LEONAPFEIFER WILLIAM KEEL Fort Hays State University, Kansas, emeritus University of Kansas, Lawrence On the cover: Wearing a traditional Russian fur hat, en- tertainer John Denver stands outside the U.S. Embassy in Moscow, Russia, 1984. He The Journal of the American Historical Society of Germans from Russia is published quarterly by AHSGR. was one of the first American recording Members of the Society receive a quarterly Journal and Newsletter. Members qualify for discounts on artists to be allowed to do a public concert in material available for purchase from AHSGR. Membership categories are: Individual, $50; the former USSR. John Denver used this Family, $50; Contributing. $75; Sustaining. $100; Life, $750. Memberships are based on a calendar year, due each January I. Dues in excess of $50 may be tax-deductible as allowed by law. Applications for membership photo for a Christmas card that he sent out should be sent to AHSGR, 631 D Street, Lincoln, NE 68502-1199. to friends and relatives. (Picture by Norman The Journal welcomes the submission of articles, essays, family histories, anecdotes, folklore, book Gershman. -

3. Inter RAO Group Today | 11

10 | PJSC Inter RAO | 2016 Annual Report 3. INTER RAO GROUP TODAY The Group operates in the following segments: A leading electricity export and import operator in Rus- — Electricity and heat generation sia. The Inter RAO Group’s supply geography comprises — Electricity supply and heat supply Finland, Belarus, Lithuania, Latvia, Estonia, Poland, Nor- — International electricity trading way, Ukraine, Georgia, Azerbaijan, South Ossetia, Ka- A diversified energy holding company — Engineering, power equipment export zakhstan, China and Mongolia. managing assets in Russia, as well as — Management of electricity distribution grids outside Russia Effectively manages power supply companies – guaran- in European and CIS countries. teed suppliers in 12 regions of Russia. Since 2010, PJSC Inter RAO has been rated in the List of Strategic Enterprises and Strategic Joint Stock Compa- Owns independent suppliers of electricity to large indus- nies of the Russian Federation1. trial consumers. GENERATING ASSETS SUPPLY ACTIVITIES ELECTRICITY EXPORT in 2016 THERMAL POWER PLANTS 41 17.0bn kWh ELECTRICITY IMPORT HYDROPOWER PLANTS 62 (including 5 low capacity HPPs) 10 in 2016 IN 62 REGIONS OF RUSSIA bn kWh WIND FARMS 3.1 1 According to the Decree of the President of Russia No. 1190 dated 30.09.2010 PJSC Inter RAO was included in the List of Strategic Enterprises and Strategic Joint-Stock Companies (Section 2 of the List of Open Joint Stock Companies with its assets held in federal ownership managed by the Russian Federation in order to ensure strategic 2 interests of State defence and security, moral values, healthcare, rights and legitimate interests protection of the citizens of the Russian Federation). -

CABRI-Volga Report Deliverable D2

CABRI-Volga Report Deliverable D2 CABRI - Cooperation along a Big River: Institutional coordination among stakeholders for environmental risk management in the Volga Basin Environmental Risk Management in the Volga Basin: Overview of present situation and challenges in Russia and the EU Co-authors of the CABRI-Volga D2 Report This Report is produced by Nizhny Novgorod State University of Architecture and Civil Engineering and the International Ocean Institute with the collaboration of all CABRI-Volga partners. It is edited by the project scientific coordinator (EcoPolicy). The contact details of contributors to this Report are given below: Rupprecht Consult - Forschung & RC Germany [email protected] Beratung GmbH Environmental Policy Research and EcoPolicy Russia [email protected] Consulting United Nations Educational, Scientific UNESCO Russia [email protected] and Cultural Organisation MO Nizhny Novgorod State University of NNSUACE Russia [email protected] Architecture and Civil Engineering Saratov State Socio-Economic SSEU Russia [email protected] University Caspian Marine Scientific and KASPMNIZ Russia [email protected] Research Center of RosHydromet Autonomous Non-commercial Cadaster Russia [email protected] Organisation (ANO) Institute of Environmental Economics and Natural Resources Accounting "Cadaster" Ecological Projects Consulting EPCI Russia [email protected] Institute Open joint-stock company Ammophos Russia [email protected] "Ammophos" United Nations University Institute for UNU/EHS Germany [email protected]