Los Angeles Unified School District

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

594605000 Los Angeles Unified School District

Ratings: Fitch: "AAA" Moody's: "Aa2" See "MISCELLANEOUS - Ratings"herein. In the opinion of Hawkins Delafield & Wood LLP, Bond Counsel to the District, under existing statutes and court decisions and assuming continuing compliance with certain tax covenants described herein, (i) interest on the Refunding Bonds is excluded from gross income for Federal income tax purposes pursuant to Section 103 of the InternalRevenue Code of 1986, as amended (the "Code''), and (ii) interest on the Refunding Bonds is not treated as a preference item in calculating the alternative minimum tax under the Code. In addition, in the opinion of Bond Counsel to the District, under existing statutes, interest on the Refunding Bonds is exempt from personal income taxes imposed by the State of California. See "TAX MATTERS" herein. $594,605,000 LOS ANGELES UNIFIED SCHOOL DISTRICT ( County of Los Angeles, California) 2019 General Obligation Refunding Bonds, Series A (Dedicated Unlimited Ad Valorem Property Tax Bonds) Dated: Date of Delivery Due: As shown on inside cover The Los Angeles Unified School District (County of Los Angeles, California) 2019 General Obligation Refunding Bonds, Series A (Dedicated Unlimited Ad Valorem Property Tax Bonds) (the "Refunding Bonds") are being issued by the Los Angeles UnifiedSchool District (the "District"), located in the County of Los Angeles (the "County"), to refund and defease a portion of the Prior Bonds ( definedherein) as more fully described herein. A portion of the proceeds of the Refunding Bonds will be used to pay the costs of issuance incurred in connection with the issuance of the Refunding Bonds. See "ESTIMATED SOURCES AND USES OF FUNDS" and "PLAN OF REFUNDING" herein. -

Mission Report 2021 Meeting the Challenges of 2020

Putting the care in student healthcare THE LOS ANGELES TRUST FOR CHILDREN’S HEALTH MISSION REPORT 2021 MEETING THE CHALLENGES OF 2020 Top row: Supervisor Mark Ridley-Thomas distributed N95 masks at an on-campus 04 Advocacy health rally; Executive Director Maryjane Puffer delivered PPE to Dr. Anitha Mullangi, 05 Healthy living chief medical officer of St. John’s; The L.A. Trust moved its oral health education to 06 Mental health social media and televison, attracting 1.1million views. Center row: California State 07 Oral health Superintendent Tony Thurmond spoke at the virtual California School-Based Health 08 Research Alliance Conference; Trusters engaged students on Zoom; The L.A. Trust and its 09 Sexual/reproductive health partners distributed more than 100,000 toothbrushes during Operation Tooth Fairy. 10 Student engagement Bottom row: Program Manager Eddie Hu helped organize our Y2Y Summit; 11 Substance use prevention The L.A. Trust worked with partner FCancer to fight HPV; Superintendent Austin Beutner 12 Wellness Centers led LAUSD’s Grab and Go effort, which distributed more than 122 million meals. 13 Partners 14 Financial report © Copyright 2021 by The Los Angeles Trust for Children’s Health. All rights reserved. Cover photo by Rinzi Ruiz. 15 Leaders/staff The year that challenged everything he past year was like no other. The worldwide healthcare. We convened experts and stakeholders at pandemic hit Los Angeles hard, shutting schools, online forums. We increased community outreach on social T locking down students and families, closing media and TV. We engaged student health advocates businesses and causing thousands to lose their jobs. -

Los Angeles City Clerk

BOARD OF RECREATION AND PARK COMMISSIONERS · ~ITY OF Los ANGELES DEPARTMENT OF RECREATION AND PARKS BARRY A SANDERS CALIFORNIA PARTNERSHIP AND REVENUE BRANCH PRESIDENT 221 NORTH FIGUEROA STREET LYNN ALVAREZ 15TH FLOOR, SUITE 1550 VICE-PRESIDENT LOS ANGELES, CA 90012 W. JEROME STANLEY (213) 202-2633 JILL T. WERNER FAX- (213) 202-2613 JOHNATHAN WILLIAMS MARY E. ALVAREZ VICKI ISRAEL EXECUTIVE ASSISTANT ANTONIO R. VllLARAIGOSA ASSISTANT GENERAL MANAGER MAYOR JON KIRK MUKRI GENERAL MANAGER April2, 2012 Honorable Richard Alarcon, Chair Alis, Parks, Health and Aging Committee c/o City Clerk, Room 395, City Hall Los Angeles, CA 90012 Attention: Adam R. Lid, Legislative Assistant COUNCIL FILE NO. 10-1076: SURVEY FINDINGS FROM SCHOOL-PARKS SHARED USE STUDY The Department of Recreation and Parks (Depaliment) began its shared use relationship with Los Angeles Unified School District (LA US D) in 1967 with an agreement for the construction and operation of a pool at Venice High SchooL The pool was subsequently built by the City on LAUSD property. The Department cunently has 36 formal agreements with LAUSD through Joint Use Agreements (JUA) and License Agreements. An additional 199 school or park sites have a shared use relationship through a permit or an informal reciprocal agreement. Use fees have historically not been collected from or paid to LAUSD under these arrangements_ However, recent discussions with LAUSD have indicated that this may change in the future, as LA USD is considering a policy change that would impose use fees on the Department for use of non JUA related school sites. , Besides LAUSD schools, the Depmtment also has working relationships with private schools and independent · chmter schools not under LAUSD. -

Charter Schools Indicators

CHARTER SCHOOLS INDICATORS 9-10 100 7-8 5-6 0 3-4 06 07 04 05 02 03 00 011-2 98 99 96 97 94 95 a report from The Center on Educational Governance University of Southern California Table of Contents Foreword Introduction . 2 Figure: Transforming Data into Knowledge . 3 Understanding the Charts . 4 The Report: Across California Financial Resources and Investment Reserves Ratios . 6 Liquidity Ratios . 7 Direct Classroom Investment . 8 School Quality Staffing Resources . 9 Teacher Qualification . 10 English Learner Reclassification . 11 School Performance API Composite . 12 Adequate Yearly Progress . 13 Academic Momentum . 14 Academic Productivity English/Language Arts Productivity. 15 Math Productivity . 16 School Productivity . 17 Snapshot: California Charter Schools, 2008 - 2009 . 18 The Report: Individual Schools Understanding the Tables . 21 Map of California Counties . 22 Charter School Scores, Grouped by County . 23 Appendices Appendix A - Data Sources and Terms . 46 Appendix B - Creating CSI-USC . 48 Appendix C - Index and Data Sources . 50 Credits . 55 report design - www.integraphicsdesign.com Charter Schools Indicators - USC - 1 Introduction: Charter Schools Indicators a report from the University of Southern California More charter schools – specifically, more high-quality charter schools – are a cornerstone of the Obama administration’s $4 billion Race to the Top initiative. By encouraging choice and competi- tion within the public school system, the administration hopes to improve student achievement in the United States. One stipulation of RTT funding is that states must have a charter school law in place and no limit or cap on the number of allowable charter schools – prompting aggressive lobbying campaigns in many states to change charter school policies in order to qualify for the competition. -

Big Donation Comes in Small Package

WWW.BEVERLYPRESS.COM INSIDE • City Council absences Sunny and revealed. pg. 3 clear, with • Store raided for temps around drug sales. pg. 4 73º Volume 21 No. 6 Serving the West Hollywood, Hancock Park and Wilshire Communities February 10, 2011 Film School Has Plans to Expand Big Donation Comes n Negotiations With Hwd. Farmersʼ in Small Package Market Continue n Gift Inspires L.A. Gay & Lesbian Center BY JOSE MARTINEZ to Start Fundraising Campaign in Boyʼs Name hile city officials scram- BY RAFAEL GUERRERO Malcolm was given $140 by his ble to find an answer to grandmother to donate to charity Wthe heated and high pro- young boy has shown that and teach him the importance of file issue between the Los Angeles no gift to charity is too improving the world around him. Film School and the Hollywood Asmall. The L.A. Gay and “I was brought to tears,” said Farmers’ Market over access to Lesbian Center received an enve- Lorri L. Jean, CEO of the L.A. Gay one of the school’s parking struc- lope Feb. 3 and Lesbian Center. “Things like tures, the contentious situation containing that don’t happen very often.” took a surprising turn when the two letters Jean and Stevie St. John, com- school announced it is considering and a check munications manager for the L.A. building a major development at for $70. The Gay and Lesbian Center, contacted the intersection of Ivar and Selma first letter Malcolm’s mother to find out what Avenues, leaving the future of the was from a inspired him to make the donation. -

Eagle Rock Elementary School (As It Should Appear on an Award) Official School Name Mailing Address: 2057 Fair Park Avenue, Los Angeles, CA 90047 (If Address Is P.O

School Nominee Presentation Form ELIGIBILITY CERTIFICATIONS School and District’s Certifications The signatures of the school principal and district superintendent (or equivalents) on the next page certify that each of the statements below concerning the school’s eligibility and compliance with the following requirements is true and correct to the best of their knowledge. In no case is a private school required to make any certification with regard to the public school district in which it is located. 1. The school has some configuration that includes grades early learning to 12. 2. The school has been evaluated and selected from among schools within the Nominating Authority’s jurisdiction, based on high achievement in the three ED-GRS Pillars: 1) reduced environmental impact and costs; 2) improved health and wellness; and 3) effective environmental and sustainability education. 3. Neither the nominated public school nor its public school district is refusing the U.S. Department of Education Office of Civil Rights (OCR) access to information necessary to investigate a civil rights complaint or to conduct a district wide compliance review. The Department of Defense Education Activity (DoDEA) is not subject to the jurisdiction of OCR. The nominated DoDEA schools, however, are subject to and in compliance with statutory and regulatory requirements to comply with Federal civil rights laws. 4. OCR has not issued a violation letter of findings to the public school district concluding that the nominated public school or the public school district as a whole has violated one or more of the civil rights statutes. A violation letter of findings will not be considered outstanding if OCR has accepted a corrective action plan to remedy the violation. -

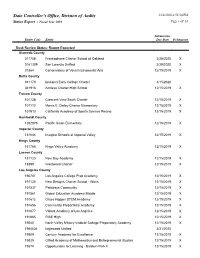

State Controller's Office, Division of Audits 3/16/2020 2:55:54 PM Status Report - Fiscal Year 2019 Page 1 of 53

State Controller's Office, Division of Audits 3/16/2020 2:55:54 PM Status Report - Fiscal Year 2019 Page 1 of 53 Submission Entity Code Entity Due Date Delinquent Desk Review Status: Report Expected Alameda County 011708 Francophone Charter School of Oakland 2/28/2020 X 0161309 San Lorenzo Unified 2/29/2020 X 01864 Conservatory of Vocal Instrumental Arts 12/15/2019 X Butte County 041170 Ipakanni Early College Charter 4/15/2020 041916 Achieve Charter High School 12/15/2019 X Fresno County 101138 Crescent View South Charter 12/15/2019 X 101172 Morris E. Dailey Charter Elementary 12/15/2019 X 101913 California Academy of Sports Science Fresno 12/15/2019 X Humboldt County 1262976 Pacific Union Elementary 12/15/2019 X Imperial County 131044 Imagine Schools at Imperial Valley 12/15/2019 X Kings County 161766 Kings Valley Academy 12/15/2019 X Lassen County 181123 New Day Academy 12/15/2019 X 18399 Westwood Charter 12/15/2019 X Los Angeles County 190741 Los Angeles College Prep Academy 12/15/2019 X 191120 New Designs Charter School - Watts 12/15/2019 X 191537 Pathways Community 12/15/2019 X 191561 Global Education Academy Middle 12/15/2019 X 191612 Grace Hopper STEM Academy 12/15/2019 X 191656 Community Preparatory Academy 12/15/2019 X 191677 Valiant Academy of Los Angeles 12/15/2019 X 191865 RISE High 12/15/2019 X 19540 North Valley Military Institute College Preparatory Academy 12/15/2019 X 1964634 Inglewood Unified 3/31/2020 19809 Century Academy for Excellence 12/15/2019 X 19829 Gifted Academy of Mathematics and Entrepreneurial Studies 12/15/2019 -

` Santa Monica Community College District District Planning And

Santa Monica Community College District District Planning and Advisory Council MEETING – MARCH 13, 2019 AGENDA ` A meeting of tHe Santa Monica Community College District Planning and Advisory Council (DPAC) is scHeduled to be Held on Wednesday, MarcH 13, 2019 at 3:00 p.m. at Santa Monica College DrescHer Hall Room 300-E (tHe Loft), 1900 Pico Boulevard, Santa Monica, California. I. Call to Order II. Members Teresita Rodriguez, Administration, CHair Designee Nate DonaHue, Academic Senate President, Vice-Chair Mike Tuitasi, Administration Representative Eve Adler, Management Association President Erica LeBlanc, Management Association Representative Mitra Moassessi, Academic Senate Representative Peter Morse, Faculty Association President Tracey Ellis, Faculty Association Representative Cindy Ordaz, CSEA Representative Dee Upshaw, CSEA Representative Isabel Rodriguez, Associated Students President ItzcHak MagHen, Associated Student Representative III. Review of Minutes: February 27, 2019 IV. Reports V. Superintendent/President’s Response to DPAC Recommendations, if any. VI. Agenda Public Comments Individuals may address tHe District Planning and Advisory Council (DPAC) concerning any subject tHat lies witHin tHe jurisdiction of DPAC by submitting an information card with name and topic on which comment is to be made. The Chair reserves tHe rigHt to limit tHe time for each speaker. 1. Report: SMC Promise Program 2. Student Services Center Directory 3. DPAC Restructure/ScHedule • Chief Director of Business Services Chris Bonvenuto will attend -

May 3, 2021 Superintendent Austin Beutner Los Angeles Unified

Sent via Electronic Mail May 3, 2021 Superintendent Austin Beutner Los Angeles Unified School District 333 South Beaudry Avenue Los Angeles, CA 90017 [email protected] Dear LAUSD Superintendent Beutner, We write on behalf of LAUSD students from the Youth Liberty Squad and InnerCity Struggle. The Youth Liberty Squad (YLS) is a student-led youth group founded by the ACLU of Southern California. YLS works on a variety of social justice issues in Los Angeles and across California and is made up of high school students, the majority of whom attend LAUSD schools, including Manual Arts High School, Girls Academic Leadership Academy, Foshay Learning Center, Ramon C. Cortines, Fairfax High School, César Chávez Learning Academies, Bravo Medical Magnet, Venice High School, South Gate High School, and many others. InnerCity Struggle is a grassroots community-based organization with the mission to achieve social and economic justice for youth and families in the Eastside of LA. InnerCity Struggle’s student leaders attend LAUSD schools, including Garfield High School, Mendez High School, Wilson High School, Roosevelt High School, Lincoln High School, and Esteban Torres High School. As you know, this past year has been extremely hard for us and our peers. Beyond experiencing the same distance learning problems that all students have faced, we live in predominately Black and Brown communities that have been hit the hardest by the pandemic. We have had friends and family members lose their jobs, get sick, and even pass away. Despite these challenges, we remain hopeful that students, community leaders, and LAUSD leadership will be able to work together to develop a plan that will safely and effectively support all those who make up the LAUSD community—and specifically a plan that prioritizes equity and our communities that need the most help. -

California Public Employees' Retirement System

California Public Employees’ Retirement System Schools Cost-Sharing Multiple-Employer Defined Benefit Pension Plan Schedules of Employer Allocations and Collective Pension Amounts Year Ended June 30, 2019 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO International Limited, a UK company limited by guarantee. California Public Employees’ Retirement System Schools Cost-Sharing Multiple-Employer Defined Benefit Pension Plan Schedules of Employer Allocations and Collective Pension Amounts Year Ended June 30, 2019 California Public Employees’ Retirement System Schools Cost-Sharing Multiple-Employer Defined Benefit Pension Plan Contents June 30, 2019 Independent Auditor’s Report 3-4 Schedules of Employer Allocations and Collective Pension Amounts Schedule of Employer Allocations 6-28 Schedule of Collective Pension Amounts 29 Notes to Schedules of Employer Allocations and Collective Pension Amounts 30-35 2 Tel: 415-397-7900 One Bush Street, Suite 1800 Fax: 415-397-2161 San Francisco, CA 94104 www.bdo.com Independent Auditor’s Report To the Board of Administration California Public Employees’ Retirement System Sacramento, California Report on the Schedules We have audited the accompanying schedule of employer allocations of the California Public Employees’ Retirement System (the System) Schools Cost-Sharing Multiple-Employer Defined Benefit Pension Plan (the Plan) as of and for the year ended June 30, 2019, and the related notes. We have also audited the total for all of the columns titled net pension liability, total deferred outflows of resources excluding employer-specific amounts, total deferred inflows of resources excluding employer-specific amounts, and pension expense (specified column totals) included in the accompanying schedule of collective pension amounts of the Plan as of and for the year ended June 30, 2019, and the related notes. -

Secondary School/ Community College Code List 2014–15

Secondary School/ Community College Code List 2014–15 The numbers in this code list are used by both the College Board® and ACT® connect to college successTM www.collegeboard.com Alabama - United States Code School Name & Address Alabama 010000 ABBEVILLE HIGH SCHOOL, 411 GRABALL CUTOFF, ABBEVILLE AL 36310-2073 010001 ABBEVILLE CHRISTIAN ACADEMY, PO BOX 9, ABBEVILLE AL 36310-0009 010040 WOODLAND WEST CHRISTIAN SCHOOL, 3717 OLD JASPER HWY, PO BOX 190, ADAMSVILLE AL 35005 010375 MINOR HIGH SCHOOL, 2285 MINOR PKWY, ADAMSVILLE AL 35005-2532 010010 ADDISON HIGH SCHOOL, 151 SCHOOL DRIVE, PO BOX 240, ADDISON AL 35540 010017 AKRON COMMUNITY SCHOOL EAST, PO BOX 38, AKRON AL 35441-0038 010022 KINGWOOD CHRISTIAN SCHOOL, 1351 ROYALTY DR, ALABASTER AL 35007-3035 010026 EVANGEL CHRISTIAN SCHOOL, PO BOX 1670, ALABASTER AL 35007-2066 010028 EVANGEL CLASSICAL CHRISTIAN, 423 THOMPSON RD, ALABASTER AL 35007-2066 012485 THOMPSON HIGH SCHOOL, 100 WARRIOR DR, ALABASTER AL 35007-8700 010025 ALBERTVILLE HIGH SCHOOL, 402 EAST MCCORD AVE, ALBERTVILLE AL 35950 010027 ASBURY HIGH SCHOOL, 1990 ASBURY RD, ALBERTVILLE AL 35951-6040 010030 MARSHALL CHRISTIAN ACADEMY, 1631 BRASHERS CHAPEL RD, ALBERTVILLE AL 35951-3511 010035 BENJAMIN RUSSELL HIGH SCHOOL, 225 HEARD BLVD, ALEXANDER CITY AL 35011-2702 010047 LAUREL HIGH SCHOOL, LAUREL STREET, ALEXANDER CITY AL 35010 010051 VICTORY BAPTIST ACADEMY, 210 SOUTH ROAD, ALEXANDER CITY AL 35010 010055 ALEXANDRIA HIGH SCHOOL, PO BOX 180, ALEXANDRIA AL 36250-0180 010060 ALICEVILLE HIGH SCHOOL, 417 3RD STREET SE, ALICEVILLE AL 35442 -

AUG 1 7 2021 Attachment A

RESOLUTION PUBLIC WORKS WHEREAS, the Los Angeles Municipal Code (LAMC), Section 41.18(c)(1) states that sitting, lieing, sleeping, or storing, useing, maintaining, or placing personal property, in or upon any street, sidewalk, or other public right-of-way within the distance stated on the posted signage (up to a maximum of 500 feet) of a property designated as a sensitive use. For a property to be designated as a "sensitive use," the property must be a School, Day Care Center, Public Park, or Public Library, as those terms are defined in Section 105.01 of this Code; and WHEREAS, pursuant to Los Angeles Municipal Code, section 105.01, "School" means an institution of learning for minors, whether public or private, which offers instruction in grades K through 12 in those courses of study required by the California Education Code or which is maintained pursuant to standards set by the State Board of Education; and WHEREAS, the Los Angeles Municipal Code, section 41.18(d), states: No person shall be found to be in violation of any prohibition set forth in Subsection (c), unless and until: (i) the City Council has taken action, by resolution, to designate a specified area or areas for enforcement against sitting, lying, sleeping, or storing, using, maintaining, or placing personal property, or otherwise obstructing the public right-of-way; (ii} the City has posted signage at the designated area or areas set forth in the resolution, with such signage including reference to any required findings adopted in the resolution, and giving notice of the date after which no sitting, lying, sleeping, or storing, using, maintaining, or placing personal property, or otherwise obstructing the public right-of-way will be allowed; and (iii) at least 14 calendar days have passed from the date on which the signage is posted at the designated area or areas.