The Expectation Gap in Internet Financial Reporting: Evidence from an Emerging Capital Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Günlük Bülten S&P 500 Brent Petrol USD Endeks %0.36 -%0.75 %0.17

Türkiye | Piyasalar 26 Ocak 2021 Salı Günlük Bülten S&P 500 Brent Petrol USD Endeks %0.36 -%0.75 %0.17 Ekonomik Veriler Açıklanacak Veriler Saat Piyasa Yorumu: İngiltere İşsizlik Oranı 10:00 Amerika Tüketici Güveni 18:00 TSİ Bu sabah BIST100’de aşağı yönlü bir açılış bekliyoruz. Küresel piyasalardaki negatif seyir devam ederken, hisse senetlerinde satışların Hisse Senedi Piyasası devam ettiğini görüyoruz. Zayıf bankacılık ve havacılık hisse senetlerinin performansı endekse karşı genel duyarlılığı etkiliyor. 50,000 1,580 48,000 1,570 Bu sabah negatif açılış ve sonrasında 1510 – 1550 arasında işlem 46,000 1,560 aktivitesi bekliyoruz. 44,000 1,550 42,000 1,540 40,000 1,530 38,000 1,520 Bugünün Haberleri: 36,000 1,510 34,000 1,500 15-Oca 18-Oca 19-Oca 20-Oca 21-Oca 22-Oca 25-Oca Piyasa Gelişmesi İşlem Hacmi, TRY mln BIST 100 . Reel kesim güveninde düşüş Bono Piyasası . Ocak ayı - Kapasite Kullanım Oranı 60.0 13.6 13.5 50.0 Hisse Senetleri 13.5 40.0 13.4 13.4 . ARCLK; 4Ç20 sonuçları beklentilerin oldukça üzerinde geldi / 30.0 13.3 20.0 13.3 olumlu 13.2 10.0 13.2 0.0 13.1 . PETKM; Etilen-nafta spread’i yeniden 650 USD'ye yöneldi / olumlu 15-Oca 18-Oca 19-Oca 20-Oca 21-Oca 22-Oca 25-Oca . GUBRF; 2020 yılı faaliyetleri hakkında bilgilendirme / pozitif İşlem Hacmi, TRY mln Türkiye 2030 Endeksler, para piyasaları ve emtia . BAGFS; %200 bedelli sermaye artırımı / nötr Kapanış Önceki 1 Gün 1 Ay Yıl Baş. BIST100 1,540 1,542 -0.1% 8.0% 4.3% . -

1 Ocak 2021 Itibariyle Şirketlerin Katilim Endeksi

1 OCAK 2021 İTİBARİYLE ŞİRKETLERİN KATILIM ENDEKSİ KRİTERLERİNE UYGUNLUK DURUMU & ARINDIRMA ORANLARI Faaliyet alanı, grubu ve pazarı uygun olmayan şirketlerin finansal kriterleri hesaplanmamaktadır. Faizli krediler / (piyasa değeri ya da aktif toplamdan büyük olanı) < %33 kriterini geçemeyen şirketlerin diğer finansal kriterleri hesaplanmamaktadır. Faiz Getirili Nakit/(piyasa değeri ya da aktif toplamdan büyük olanı)<%33 kriterini geçemeyen şirketlerin diğer finansal kriterleri hesaplanmamaktadır. Toplam Faizli Uygunsuz Krediler / Piyasa (Nakit+Menkul Uygun Olmayan Sıra Hisse Kodu Hisse Adı Gerekçe Değeri veya Aktif (< Kıymet)/Piyasa Değeri Faaliyetlerden Gelir / %33) veya Aktif (<%33) Toplam Gelir (< %5) 1 BIMAS Bim Mağazalar Uygun 0,0% 0,0% 0,2% 2 EREGL Ereğli Demir Çelik Uygun 14,4% 25,3% 2,7% 3 ASELS Aselsan Uygun 9,6% 5,5% 1,5% 4 THYAO Türk Hava Yolları Uygun 18,3% 4,6% 4,3% 5 CCOLA Coca Cola İçecek Uygun 29,5% 18,4% 1,8% 6 GUBRF Gübre Fabrik. Uygun 22,7% 11,5% 0,3% 7 BERA Bera Holding Uygun 26,3% 0,0% 0,5% 8 TKFEN Tekfen Holding Uygun 14,0% 15,6% 1,2% 9 OYAKC Oyak Çimento Uygun 9,7% 6,2% -22,6% 10 PGSUS Pegasus Uygun 7,5% 12,4% 2,6% 11 EGEEN Ege Endüstri Uygun 4,3% 22,0% 2,1% 12 TTRAK Türk Traktör Uygun 30,7% 32,9% 2,3% 13 MAVI Mavi Giyim Uygun 30,2% 22,6% 1,5% 14 LOGO Logo Yazılım Uygun 7,6% 7,9% 2,8% 15 KARTN Kartonsan Uygun 0,0% 7,4% 1,8% 16 SELEC Selçuk Ecza Deposu Uygun 0,6% 10,6% 0,7% 17 ISDMR İskenderun Demir Çelik Uygun 4,9% 0,2% 1,3% 18 RTALB RTA Laboratuvarları Uygun 1,5% 0,1% 2,8% 19 CEMAS Çemaş Döküm Uygun 0,3% 17,9% -

Günlük Bülten S&P 500 Brent Petrol USD Endeks %0.42 -%0.21 -%0.43

Türkiye | Piyasalar 09 Nisan 2021 Cuma Günlük Bülten S&P 500 Brent Petrol USD Endeks %0.42 -%0.21 -%0.43 Ekonomik Veriler Açıklanacak Veriler Saat Piyasa Yorumu: Amerika ÜFE 15:30 TSİ Bu sabah BIST100’de karışık bir açılış bekliyoruz. Bankacılık hisse Hisse Senedi Piyasası senetlerindeki satışların devam etmesi nedeniyle endekste zayıf seyir devam ediyor. 35,000 1,450 30,000 1,440 Bu sabah karışık açılış ve sonrasında 1400 – 1440 arasında işlem 1,430 25,000 aktivitesi bekliyoruz. 1,420 20,000 1,410 15,000 1,400 1,390 10,000 1,380 Bugünün Haberleri: 5,000 1,370 0 1,360 Piyasa Gelişmesi 31-Mar 01-Nis 02-Nis 05-Nis 06-Nis 07-Nis 08-Nis İşlem Hacmi, TRY mln BIST 100 . TCMB Haftalık Veriler - Yabancı çıkışı düşük ivmede de olsa devam etti; hisse senetlerindeki baskı kuvvetli Bono Piyasası 20.0 19.5 Hisse Senetleri 19.0 15.0 . DOHOL; Bağlı Ortaklık Galata Wind Enerji A.Ş. paylarının halka arz 18.5 10.0 edilmesi için SPK onayı gerçekleşti / olumlu 18.0 5.0 17.5 . INDES; SPK bedelsiz sermaye artırımını onayladı / sınırlı olumlu 0.0 17.0 31-Mar 01-Nis 02-Nis 05-Nis 06-Nis 07-Nis 08-Nis Ekonomik Veriler İşlem Hacmi, TRY mln Türkiye 2030 . 09.00: Almanya, sanayi üretimi, %1.5-aylık, %-2.3-yıllık, Şubat, Endeksler, para piyasaları ve emtia . 10.00: Türkiye, TCMB Beklenti Anketi, Nisan, Kapanış Önceki 1 Gün 1 Ay Yıl Baş. BIST100 1,417 1,418 -0.1% -7.4% -4.1% İşlem Hacmi, TL mln 24,239 25,117 -3.5% -34.9% -33.6% . -

Market Watch Tuesday, August 08, 2017 Agenda

Market Watch Tuesday, August 08, 2017 www.sekeryatirim.com.tr Agenda 07 Monday 08 Tuesday 09 Wednesday 10 Thursday 11 Friday Germany, June industrial TurkStat, June industrial U.S., June wholesale U.S., jobless claims CBRT, June balance of production production inventories U.S., July PPI payments U.S., July CPI Outlook: Major stock markets have advanced to new highs, and the BIST100 has Volume (mn TRY) BIST 100 also tested new record-highs, closing up 1.1% at 109,781 on Monday. Total trading volume in the market was at TRY 6.6bn. Today, market participants 109.781 will follow TurkStat’s June industrial production release; there are no other 10.000 110.000 108.545 major data announcements. Asian markets have seen mixed trading this 8.000 morning, and the European stock markets are expected to open slightly 107.154 108.000 106.525 down. We expect the BIST to maintain its uptrend in parallel to rising global 6.000 106.147 risk appetite, although we caution that the likelihood of profit taking rises 106.000 after swift upsurges. We expect the BIST to open positively today, refresh- 4.000 4.912 4.958 ing its new record highs. RESISTANCE: 110,000 /111,200 SUP- 5.418 104.000 4.667 2.000 4.667 PORT: 109,100/108,600. 0 102.000 1-Aug 2-Aug 3-Aug 4-Aug 7-Aug Money Market: The Lira was positive yesterday, gaining 0.14% against the USD to close at 3.5295. Additionally, the currency depreciated by 0.07% against the basket composed of $0.50 and €0.50. -

2016 Annual Report & Sustainability Report

2016 ANNUAL REPORT & SUSTAINABILITY REPORT BOYNER RETAIL AND TEXTILE INVESTMENTS BOYNER RETAIL AND TEXTILE INVESTMENTS www.boynerperakende.com www.boynergrup.com 2 2016 ANNUAL REPORT & SUSTAINABILITY REPORT 3 CONTENTS 05 10 29 69 106 121 137 FROM THE MANAGEMENT BOYNER GROUP BOYNER RETAIL AND SUSTAINABILITY CORPORATE AGENDA FOR THE INDEPENDENT TEXTILE INVESTMENTS REPORT GOVERNANCE ORDINARY GENERAL AUDITOR’S REPORT ON 06 12 CO. INC. and PRINCIPLES ASSEMBLY MEETING ANNUAL REPORT Message from the CEO and Our History 71 ITS COMPANIES COMPLIANCE REPORT FOR 2016 Chairman of the Board Sustainability 141 14 30 Management and our 117 122 INDEPENDENT 09 Our 2016 Awards Partnership Structure Stakeholders RISK MANAGEMENT AND Resumes and AUDITOR’S REPORT Members of the Board of 15 INTERNAL AUDIT Statements of & FINANCIAL Directors 33 73 Our Values Independent Members STATEMENTS Boyner Büyük Our Working Ecosystem 118 for Ordinary General 16 Mağazacılık A.Ş. DONATIONS AND GRANTS 83 Assembly Meeting for Our Working 43 Anti-Corruption 118 2016 Environment Beymen Mağazacılık CAPITAL MARKET 84 130 18 A.Ş. INSTRUMENTS ISSUED Our Environmental Dividend Distribution Our Strategies and IN 2016 51 Awareness Proposal and Statement Projects in 2016 AY Marka Mağazacılık 119 for 2016 - WEPUBLIC 90 A.Ş. LEGAL DISCLOSURES - Hopi Our Value Chain 132 - All Line Retail 61 Remuneration Policy 95 Altınyıldız Tekstil ve for Board Members and Our Contribution to Konfeksiyon A.Ş. Senior Executives Society 136 Dividend Distribution Policy FROM THE MANAGEMENT 05 6 2016 ANNUAL REPORT & SUSTAINABILITY REPORT 7 By making a very important investment in 2016, we enabled Boyner not be restricted and purchases will be realized with nominal value. -

Hisse Senedi Veri Bankasi

Günlük Haftalık Aylık 3 Aylık 12 Aylık Yılbaşına Göre 22.04.2021 21.04.2021 15.04.2021 22.03.2021 22.01.2021 22.04.2020 31.12.2020 22 Nisan 2021 HİSSE SENEDİ VERİ BANKASI ENDEKSLER KAPANIŞ P E R F O R M A N S TL US $ Günlük (TL) 1 Hafta (TL/US$) 1 Ay (TL/US$) 3 Ay (TL/US$) YBB (TL/US$) 1 Yıl (TL/US$) BIST-100 1,345.2 162.7 %1.10 -%4.4 -%6.9 -%2.5 -%6.8 -%12.8 -%22.0 -%8.9 -%18.3 %37.0 %15.5 BIST-30 1,412.7 170.8 %1.12 -%3.6 -%6.1 -%1.4 -%5.8 -%14.4 -%23.4 -%13.7 -%22.5 %22.0 %2.8 Mali 1,253.1 151.5 %0.82 -%6.3 -%8.7 -%9.5 -%13.5 -%23.0 -%31.1 -%19.9 -%28.2 %18.2 -%0.4 Sanayi 2,475.9 299.4 %1.65 -%5.3 -%7.7 %0.4 -%4.0 -%3.1 -%13.3 %5.8 -%5.1 %99.0 %67.8 Hizmetler 1,082.1 130.9 %1.35 -%5.5 -%7.9 -%2.5 -%6.8 -%12.7 -%21.9 -%9.3 -%18.6 %28.2 %8.0 Banka 1,086.5 131.4 %0.85 -%4.1 -%6.6 -%9.9 -%13.9 -%28.3 -%35.8 -%30.3 -%37.4 -%9.0 -%23.3 XU100_Getiri 2,350.8 284.3 %1.10 -%4.44 -%6.9 -%0.7 -%5.1 -%11.2 -%20.5 -%7.0 -%16.6 %40.8 %18.7 PİY. -

Standardization and Measurement Services in Turkey

NAT'L INST. OF STAND & TECH NI8T PUBLICATIONS REFERENCE AlllDb 7El'lb3 NBSIR 73-172 Standardization and liHeasurement Services in Turkey A Report of a National Bureau of Standards/Agency for International Development Survey Conducted October 14-28, 1972 A Report of a Survey Conducted jointly by the National Bureau of Standards and the Agency for International Development. October 14-28, 1972 QC /oO U. S. DEPARTMENT OF COMMERCE NATIONAL BUREAU OF STANDARDS NBSIR 73-172 STANDARDIZATION AND MEASUREMENT SERVICES IN TURKEY (A Report of an National Bureau of Standards/Agency for International Development Survey Conducted October 14-28, 1972) Survey Team Director: Professor Dr. Tarik G. Somer, President, Turkish Standards Institution Survey Team Members: William E. Andrus, National Bureau of Standards, USA Robert J. Corruccini, National Bureau of Standards, USA Raul Estrada, Ecuadorean Institute of Standards, Ecuador Velid Isfendiyar, Turkish Standards Institution, Turkey Jeong, Byong Sik, Bureau of Standards, Korea Sanford B. Newman, National Bureau of Standards, USA H. Steffen Peiser, National Bureau of Standards, USA Charoen Vashrangsi, Department of Science, Thailand (as observer) H. Thomas Yolken, National Bureau of Standards, USA M. Fuat Yucesoy, Turkish Standards Institution, Turkey This survey was conducted as a part of the program under the US/NBS/Agency for International Development, PASA TA(CE)5-71. U. S. DEPARTMENT OF COMMERCE, Frederick B. Dent. Secretary NATIONAL BUREAU OF STANDARDS, Richard W. Roberts, Director ACKNOWLEDGEMENTS The encouragement, planning assistance and generous financial support from the U.S. Agency of International Development, U.S. Department of State are gratefully acknowledged. In addition the Team sincerely thanks the numerous unnamed government, industry and university colleagues in Turkey who gave freely of their time and advice to assist the Survey, Dr. -

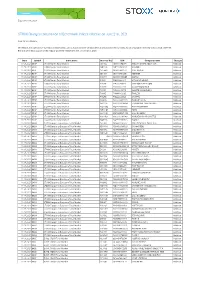

STOXX Changes Composition of Benchmark Indices Effective on June 21St, 2021

Zug, June 11th, 2021 STOXX Changes composition of Benchmark Indices effective on June 21st, 2021 Dear Sir and Madam, STOXX Ltd., the operator of Qontigo’s index business and a global provider of innovative and tradable index concepts, today announced the new composition of STOXX Benchmark Indices as part of the regular quarterly review effective on June 21st, 2021 Date Symbol Index name Internal Key ISIN Company name Changes 11.06.2021 BDXP STOXX Nordic Total Market SE10V2 SE0001174970 MILLICOM INTL.CELU. SDR Addition 11.06.2021 BDXP STOXX Nordic Total Market NO112F NO0010823131 KAHOOT! Addition 11.06.2021 BDXP STOXX Nordic Total Market SE10W3 SE0015483276 CINT GROUP Addition 11.06.2021 BDXP STOXX Nordic Total Market SE10X4 SE0015671995 HEMNET Addition 11.06.2021 BDXP STOXX Nordic Total Market DK3011 DK0060497295 MATAS Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10JH FI4000480215 SITOWISE GROUP Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10HF FI4000049812 VERKKOKAUPPA COM Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10FD FI0009001127 ALANDSBANKEN B Addition 11.06.2021 BDXP STOXX Nordic Total Market FI6036 FI4000048418 AHLSTROM-MUNKSJO Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10IG FI4000062195 TAALERI Addition 11.06.2021 BDXP STOXX Nordic Total Market FI10GE FI4000029905 SCANFIL Addition 11.06.2021 BDXP STOXX Nordic Total Market NO90I2 NO0010861115 NORSKE SKOG Addition 11.06.2021 BDXP STOXX Nordic Total Market NO111E NO0010029804 SPAREBANK 1 HELGELAND Addition 11.06.2021 BDXP STOXX Nordic Total Market NO113G NO0010886625 AKER BIOMARINE Addition 11.06.2021 BDXP STOXX Nordic Total Market NO114H NO0010936792 FROY Addition 11.06.2021 BDXP STOXX Nordic Total Market NO110D BMG9156K1018 2020 BULKERS Addition 11.06.2021 BDXP STOXX Nordic Total Market NO10R3 NO0010196140 NORWEGIAN AIR SHUTTLE Addition 11.06.2021 BDXP STOXX Nordic Total Market NO809S NO0010792625 FJORD1 Deletion 11.06.2021 BKXA STOXX Europe ex Eurozone Total Market SE10V2 SE0001174970 MILLICOM INTL.CELU. -

Günlük Bülten S&P 500 Brent Petrol USD Endeks -%0.29 %0.38 %0.49

Türkiye | Piyasalar 20 Mayıs 2021 Perşembe Günlük Bülten S&P 500 Brent Petrol USD Endeks -%0.29 %0.38 %0.49 Ekonomik Veriler Açıklanacak Veriler Saat Piyasa Yorumu: - - TSİ Bu sabah BIST100’de yatay/negatif yönlü bir açılış bekliyoruz. Hisse Senedi Piyasası Geçtiğimiz günlerde bankacılık hisse senetlerinde güçlü performans olduğu gözlemlenirken bazı sanayi hisselerinden bankacılık hisselerine 35,000 1,470 geçişlerin önümüzdeki günlerde devam edeceğini tahmin ediyoruz. 30,000 1,460 25,000 Bu sabah yatay/negatif açılış ve sonrasında 1450 – 1470 arasında işlem 1,450 20,000 aktivitesi bekliyoruz. 1,440 15,000 1,430 10,000 5,000 1,420 Bugünün Haberleri: 0 1,410 06-May 07-May 10-May 11-May 12-May 17-May 18-May İşlem Hacmi, TRY mln BIST 100 Ekonomik Veriler . Saat 15:30 – Amerika, İşsizlik haklarından yararlanma başvuruları Bono Piyasası . Saat 15:30 – Amerika, Philadelphia Fed istihdam (May) 60.0 18.3 50.0 18.2 18.2 . Saat 17:30 – Türkiye, Merkezi hükümet borç stoku (Nis) 40.0 18.1 30.0 18.1 20.0 18.0 10.0 18.0 0.0 17.9 06-May 07-May 10-May 11-May 12-May 17-May 18-May İşlem Hacmi, TRY mln Türkiye 2030 Endeksler, para piyasaları ve emtia Kapanış Önceki 1 Gün 1 Ay Yıl Baş. BIST100 1,460 1,454 0.4% 6.0% -1.2% İşlem Hacmi, TL mln 24,080 21,610 11.4% 3.4% -34.1% Turkey 2030 (13.11.2030) 18.17% 18.23% -6 bps 20 bps 526 bps Turkey 2030 6.31% 6.26% 5 bps 2 bps 94 bps TCMB karışık fonlama mlyt 19.00% 19.00% 0 bps 0 bps 197 bps USD/TRY 8.41 8.36 0.7% 3.9% 13.1% EUR/TRY 10.25 10.21 0.3% 5.1% 12.9% Sepet (50/50) 9.33 9.29 0.5% 4.5% 13.0% DOW 33,896 34,061 -0.5% -0.5% 10.7% S&P500 4,116 4,128 -0.3% -1.1% 9.6% FTSE 6,950 7,034 -1.2% -0.7% 7.6% MSCI EM 1,328 1,333 -0.4% -1.6% 2.8% MSCI EE 178.69 181.25 -1.4% 6.3% 9.8% Shanghai SE Comp 3,511 3,529 -0.5% 1.0% 1.1% Nikkei 28,044 28,407 -1.3% -5.5% 2.2% Petrol (Brent) 66.92 66.66 0.4% 30.0% 30.0% Altın 1,870 1,869 0.0% 5.5% -1.5% En Çok Yükselen & Düşenler Hisse Kodu Son Kapanış Gün Değ. -

The "Prospectus "), and You Are Therefore Advised to Read This Carefully Before Reading, Accessing Or Making Any Other Use of the Prospectus

IMPORTANT NOTICE THIS OFFERING IS AVAILABLE ONLY TO INVESTORS WHO ARE EITHER: (a) PURCHASING IN OFFSHORE TRANSACTIONS AND NOT U.S. PERSONS (EACH AS DEFINED IN REGULATION S) OR (b) QIBS (AS DEFINED BELOW) IMPORTANT: You must read the following before continuing. The following applies to the attached Prospectus (the "Prospectus "), and you are therefore advised to read this carefully before reading, accessing or making any other use of the Prospectus. In accessing the Prospectus, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from (or on behalf of) Akbank T.A.Ş. (the "Issuer ") as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OF AMERICA (WITH ITS TERRITORIES AND POSSESSIONS, ANY STATE OF THE UNITED STATES AND THE DISTRICT OF COLUMBIA, COLLECTIVELY THE "UNITED STATES ") OR ANY OTHER JURISDICTION TO THE EXTENT THAT IT IS UNLAWFUL TO DO SO. THE SECURITIES DESCRIBED HEREIN HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE UNITED STATES SECURITIES ACT OF 1933, AS AMENDED (THE "SECURITIES ACT "), OR THE SECURITIES LAWS OF ANY STATE OF THE UNITED STATES OR ANY OTHER JURISDICTION AND SUCH SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT ("REGULATION S ")) EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. -

STOXX EASTERN EUROPE 300 Selection List

STOXX EASTERN EUROPE 300 Last Updated: 20210802 ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) Rank (FINAL)Rank (PREVIOUS) RU0009024277 B59SNS8 LKOH.MM EV020 LUKOIL RU RUB Large 50.2 1 1 RU0007661625 B59L4L7 GAZP.MM EV019 GAZPROM RU RUB Large 39.4 2 2 RU0009029540 4767981 SBER.MM EV023 SBERBANK RU RUB Large 36.3 3 3 RU000A0DKVS5 B59HPK1 NVTK.MM B058LB NOVATEK RU RUB Large 35.3 4 4 RU0007288411 B5B1TX2 GMKN.MM EV022 MMC NORILSK NICKEL RU RUB Large 20 5 5 RU0008926258 B5BHQP1 SNGS.MM EV014 SURGUTNEFTEGAS RU RUB Large 13.4 6 6 HU0000061726 7320154 OTPB.BU 732015 OTP BANK HU HUF Large 10.8 7 7 RU0009033591 B59BXN2 TATN.MM EV015 TATNEFT RU RUB Large 8.7 8 8 RU000A0J2Q06 B59SS16 ROSN.MM EV021 ROSNEFT RU RUB Large 7.8 9 9 PLPKO0000016 B03NGS5 PKO.WA B03NGS PKO BANK PL PLN Large 7.3 10 10 RU000A0JKQU8 B59GLW2 MGNT.MM EV050 MAGNIT RU RUB Large 6.3 11 11 RU000A0JP7J7 B59Q6G1 PIKK.MM EV007 PIK SHB RU RUB Large 5.9 12 14 PLKGHM000017 5263251 KGH.WA 526325 KGHM PL PLN Large 5.8 13 12 LU2237380790 BMBQDF6 ALEP.WA PL00OY ALLEGRO.EU PL PLN Large 5.6 14 13 RU000A0JNAA8 B57R0L9 PLZL.MM EV010 POLYUS RU RUB Large 5.2 15 16 PLPKN0000018 5810066 PKN.WA 581006 PKNORLEN PL PLN Large 5 16 15 PLPZU0000011 B63DG21 PZU.WA PL001B PZU GROUP PL PLN Large 4.7 17 18 RU0007252813 B6QPBP2 ALRS.MM RU501R ALROSA RU RUB Large 4.6 18 17 RU0009046510 B5B9C59 CHMF.MM EV013 SEVERSTAL RU RUB Large 4 19 21 CZ0005112300 5624030 CEZP.PR 562403 CEZ CZ CZK Large 3.8 20 19 RU0009046452 B59FPC7 NLMK.MM EV009 NLMK RU RUB Large 3.7 21 25 PLPEKAO00016 5473113 -

Financialization of Turkey Industry Sector

www.sciedu.ca/ijfr International Journal of Financial Research Vol. 4, No. 3; 2013 Financialization of Turkey Industry Sector Işıl Tellalbaşı1 & Ferudun Kaya1 1 Abant İzzet Baysal University, Bolu, Turkey Correspondence: Ferudun Kaya, Abant İzzet Baysal University, Bolu, Turkey. Tel: 90-532-386-7266. E-mail: [email protected] Received: May 6, 2013 Accepted: June 27, 2013 Online Published: July 9, 2013 doi:10.5430/ijfr.v4n3p127 URL: http://dx.doi.org/10.5430/ijfr.v4n3p127 Abstract Financial markets in the world, especially for the last three decades, have been evolving significantly in terms of market volumes, operational intensity, institutional and regulations as well as the authorities governing them. The increase in operational volumes and the changing nature of financial markets, creations of new financial products; led to the increase of the importance of financial capital and how it affected day to day life directly became one of the most important theoretical problems. Thus, the transformation witnessed in the financial markets led to a new era, dubbed as “financialization”. In this article, the financialization of companies listed in the Istanbul Stock Exchange’s Industrial Index is analyzed using an econometric technique known as Generalized Method of Moments. The quantitative analysis has used two distinct methods to measure the relationship between firms’ investments and their debts, financial profits, sales and financial payments, variables that constitute variables for measuring financialization. Both models revealed a negative relationship between higher financial benefits and amount of investments. Keywords: financialization, mortgage crisis, generalized method of moments 1. Introduction Financial statements are the final product of accounting process.