Reaching New Service Heights Page 30

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Misc Interface Guide

MiSC Interface Guide August 21, 2018 Version 4.2 Last updated: 8/21/2018 4:39:00 PM MI Supplier Connect – Supplier Interface Guide Version 4.1 Document Revision History Project Contacts Name Title Telephone E-mail Address Brenda Driver Business Analyst (205) 951-1146 [email protected] John Baird Http Server Certificates (205) 957-5285 [email protected] Christie Piazza EProcurement Integration Mgr. (205) 951-6128 [email protected] Information Technology Fax: (205) 951-1185 Systems Contracts Fax: (205) 951-1595 Objectives Business Provide increased efficiency and service to Motion’s customers through system to system interaction with our key suppliers for purposes, such as: Item Availability Order Submit Order Status Product Search System Provide a flexible architecture for system to system interaction with multiple suppliers. Provide transaction response times within specified requirements. Implement point-to-point connection with the supplier’s system. Scope MI Supplier Connect connects the Motion System directly to a vendor’s order fulfillment system using transaction- based processing via a program-to-program architecture. Functionality includes Ping, Item Availability, Order Submit, Order Status and Product Search. Supplier Locations Motion provides the supplier a table of Location Numbers from the Motion system for use when returning Item Availability information to the Motion System. By design, the Motion system references the Motion Location Number (located in the Order Submit Send transaction in the Header Section) when sending orders to the Supplier System via the MI Supplier Connect Interface. The Supplier Location Numbers are then loaded, left-justified, into the existing SUPPLIER_LOCATION fields in the Item Availability Reply transaction that Motion receives from the supplier’s system. -

2019 Sponsor / Exhibitor Prospectus

2019 SPONSOR / EXHIBITOR PROSPECTUS ™ SEP. 30-OCT. 2, 2019 | DALLAS,Women In Trucking TEXAS | 2019 Accelerate! Conference & Expo | 1 Join your transportation, logistics and supply chain peers at the fifth annual Accelerate! Conference & Expo, hosted by the Women In Trucking Association. Learn about critical transportation issues and trends, along with perspectives and the positive impact women have on the industry. Build business in this integrated conference and exhibition setting. Attach your company, brand, and reputation to our mission: To generate dialogue and action around the importance of gender diversity in transportation and logistics. Ellen Voie, President and CEO Women In Trucking SEP. 30 - OCT. 2, 2019 Women Make A POSITIVE SPONSOR & EXHIBITOR Impact On Transportation PROSPECTUS Exceptional 1,000+ Expected Table of Contents: Leaders to Attend Common strengths Leverage a diverse work- 3 About Women in Trucking include intuitive/logical force, develop leaders, thinking, team-building, strategize to engage 4 Membership Demographics communication. more female drivers. 5 Sponsorship & Booth Packages 8 Sponsorship & Booth Pricing 60+ Educational 100+ Brands As Sessions Part of Expo 9 Exhibition Floor Plan Tracks: Operations, Safety, Network with peers, top Compliance, HR/Talent executives, providers of 10 Sponsorships - Special Events Management, Leadership, transportation and logistics Sales & Marketing. services and products. 12 A La Carte Options 15 2019 Conference Venue Look for many New sponsor options this year! Women In Trucking -

Public Service Companies --- Contact List JEREMY WENGERD JENNIE

Public Service Companies --- Contact List JEREMY WENGERD JENNIE BISCHOF 52 EIGHTY TOWER PARTNERS I, LLC ABF FREIGHT SYSTEM INC PO BOX 460389 ATTN TAX DEPT HOUSTON, TX 77056 PO BOX 10048 FORT SMITH, AR 72917-0048 LINDA FINK LYNN BLAKE A C WIDENHOUSE ABX AIR INC PO BOX 5010 AIR TRANSPORT SERVICE GROUP CONCORD, NC 28027-1500 145 HUNTER DR. MS-2061-F WILMINGTON, OH 45177- DAVID GUILER DOROTHY PINGLEY AAA COOPER TRANSPORTATION ACCESS FIBER GROUP, INC. PO BOX 6827 PMB 400 DOTHAN, AL 36302 4017 WASHINGTON RD MCMURRAY, PA 15317 GARLAND HORTON LYNN BLAKE ABERDEEN & ROCKFISH RR CO AIR TRANSPORT INTERNATIONAL LLC PO BOX 917 AIR TRANSPORT SERVICE GROUP ABERDEEN, NC 28315 145 HUNTER DR 2061-F WILMINGTON, OH 45177- JENNIFER HARRELL NICK RADLIFF ABERDEEN CAROLINA & WESTERN RWY CO AIR WISCONSIN AIRLINES CORP 967 NC HWY 211 E W6390 CHALLENGER DR CANDOR, NC 27229- STE 203 APPLETON, WI 54914-9120 Company Contact List 11-Sep-19 Page 1 of 37 TIM RODDY SUZANNE WILSON ALASKA AIRLINES, INC. AMERICAN AIRLINES PO BOX 68900 ATTN: SEABZ TAX DEPT MD 5657 SEATTLE, WA 98168- PO BOX 619616 DFW AIRPORT, TX 75261-9616 CLARISSA PERRY DOUG BRAUN ALBEMARLE ELEC MEMB CORP AMERICAN TOWER CORPORATION PO BOX 69 PO BOX 723597 HERTFORD, NC 27944- ATLANTA, GA 31139- BENJAMIN ZACHARY JANET MCGEE ALEXANDER RAILROAD CO APC TOWERS, LLC PO BOX 277 57 EAST WASHINGTON ST TAYLORSVILLE, NC 28681 CHAGRIN FALLS, OH 44022 SUSANNA YOO NATALIE STOVER ALLEGIANT AIR, LLC APEX TOWERS, LLC 1201 NORTH TOWN CENTER DR STE 110 125 WHITESTICK RD LAS VEGAS, NV 89144- BECKLEY, WV 25801- SHERI LARKIN DENNY HOUSE AMERFLIGHT LLC AT&T CHARTER SERVICE INC. -

Mediocreat Best

MEDIOCRE AT BEST The CCJ Top 250’s specialized carriers fared best – and worst – in 2007. But most general freight carriers saw anemic growth – or none at all. BY AVERY VISE t the time, most trucking Three carriers that were in A widespread slowdown companies probably saw last year’s CCJ Top 250 – No. The CCJ Top 250’s growth slowed A2007 as fairly miserable – 67 Performance Transportation further in 2007. Revenues grew 3.9 soft freight demand, ample capacity Services, No. 88 Jevic Transportation percent, down from the 9 percent and high fuel prices. Diesel averaged and No. 248 Alvan Motor Freight – increase recorded the year before and $2.89 a gallon in 2007, rising steadily ceased operations this year and so the 16.1 percent rise in 2005 over throughout the year from a low have been dropped from this year’s 2004. For LTL and truckload gen- of $2.41 in January to an unprec- CCJ Top 250. Fuel wasn’t the lone eral freight carriers – the majority of edented $3.44 by late November. culprit. For example, the troubled the CCJ Top 250 – 2007 was truly a For many, those were the good old automobile industry contributed to lackluster year. In fact, 2007 was just days. Today’s diesel prices are more the demise of Alvan Motor Freight another 2006 for LTL carriers, which than 35 percent higher than even the and car hauler PTS, which shut saw no change in revenues. Truckload highest average price during 2007. down in bankruptcy principally due general freight carriers posted a 3.3 Escalating prices coupled with the lag to a Teamsters strike. -

1. Appendix 1 Codes Prep Codes, Data Element 751

VOLVO Applications of ASC 12 Version: 9705-4 Published 2005-02-10 1. Appendix 1 Codes Prep Codes, Data element 751 00 According to Drawing 01 No Surface Treatment 02 Primer, Undercoats or Corr. Finish 03 Rustproof, parts ‘Y700/3’ 04 Top Coat 05 Zinc-plating 06 Hot Zinc Coat 09 Prep According to separate notes 14 Top Coat, Black 15 Top Coat, Black, High Gloss Packaging Codes, Data element 754 A Vendor packs in VTNA multiple package quantity B Vendor packages individually in suitable container C Vendor packs multiple components into individual kits D VTNA packs in selling multiple (corr container) E VTNA packs in selling multiple (merchandising carton) F VTNA packs individually (corr container) G VTNA packs individually (merchandise carton) H VTNA packs individually (wood crate) K VTNA packs multiple components into kits L VTNA packages individually (polybag) M VTNA packs in selling multiple (polybag) N Vendor: quantity ordered is for sets not pieces P VTNA special packaging instructions S Please cut and supply in .... foot lengths T Vendor cut and supply in .... meter lengths Z Package to VTNA work instruction 930.350 issue 02 VV Description gives an extended code, the Volvo company involved will gives a separate instruction about the codes. Appendix 1 Codes 1:1 VOLVO Applications of ASC 12 Version: 9705-4 Published 2005-02-10 Ship/Delivery or Calendar Pattern Codes, Data element 678 Code Description A Monday through Friday B Monday through Saturday C Monday through Sunday D Monday E Tuesday F Wednesday G Thursday H Friday J Saturday K Sunday L Monday through Thursday M Immediately N As Directed O Daily Mon. -

TT100 For-Hire 07 Online.Qxd

A Word From the Publisher n this 2007 edition of the Trans- The shift to private owner- port Topics Top 100 For-Hire ship is also reflected in the pur- Carriers, the focus has shifted chase of Swift Transportation from Main Street to Wall Street. by its former chairman Jerry Private equity investment firms Moyes and the proposed buy- have become the driving force for out of U.S. Xpress Enterprises I by top executives of that com- change, based on our annual review of financial and operating statistics pany. for the nation’s top for-hire trucking No one knows how long this companies. trend will last, or even how suc- Of course, well-heeled investors cessful these new investment and Wall Street money managers strategies will be over the long have been involved in trucking term. But what is clear from a before, but today’s breed of money reading of the Transport Topics men appears to be taking a different Top 100 For-Hire Carriers list approach than did the corporate is a sense that the game has raiders in the 1980s who used high- Howard S. Abramson changed. interest debt to target vulnerable With private equity funds companies. And they are different from the Inter- providing a source of new capital, many carriers net-inspired corporate roll-ups that we saw in the are making investments in technology and 1990s when small companies were patched expanding services in order to increase their together to create new, bigger businesses that share of the freight market. were assumed to have magical superhero market They say you can’t tell the players without a power. -

Did You Know… As of This Month, There Are 140 Companies Represented in the Traffic Club Membership

News | Events | Networking January 2012 www.indytrafficclub.org MISSION: To promote closer relationships through networking, building mutual understanding among members and stimulating education in transportation, warehousing, logistics, and INDIANAPOLIS TRAFFIC CLUB NEWSLETTER supply chain management. Did You Know… As of this month, there are 140 companies represented in the Traffic Club membership. 1st Priority Services-RR Donnelley Co. Lighting Resources Tabco Print and Promotions ABAS Consulting Liquid Transport Corp The Austin Group ABF Freight System Inc Louisville & Indiana Railroad The Hill Group Inc Aflac M&M Transport Services Inc Thermo King of Indiana Inc AIM NationaLease Marvin Johnson & Associates TKO Graphix American Sleep Medicine Maxim Services, LLC TNT Powerwash Inc Arthur J Gallagher Risk Mgmt Serv MBA Professional Services, LLC Transcorr LLC Averitt Express MED/Dispose Inc TruckersB2B Inc Avram Worldwide Mid-States Power & Refrigeration TWS Inc BNB Battery, LLC MKM Distribution Services Inc Underwood Machinery Transport Inc Carter Logistics Morgan Keegan USDOT-FMCSA Carter Truck Lines Multi Modal Trucking Inc Venture Logistics Celtic International National Transportation Consultants Vertical Alliance Group Central Transport Nice Pak Waitt Trucking Inc Clarke Power Service Old Dominion Freight Lines WhiteHorn, LLC Commercial Transport Inc Pace Air Freight Worthington Company CTM Global Logistics Palmer Leasing Group Xtra Lease Cummins Crosspoint LLC Palmer Trucks/Kenworth Indpls Zimmer Welding Co D-A Lubricant Company Inc PB Logistics Services DB Schenker Perfect Transportation LLC Dickinson Fleet Services Pilot Freight Services Driving Ambition Inc PNC Bank Exel Transportation Services Inc PrincetonOne “Our membership is growing and our FedEx Ground Qualcomm hope is to continue this growth in Galagher Benefit Services Quick Fuel/Jacobus Energy 2012. -

North American Commercial Vehicle Show the Fleet Technology Showcase

September 27-30, 2021 Georgia World Congress Center, Atlanta North American Commercial Vehicle Show The Fleet Technology Showcase The North American Commercial Vehicle (NACV) Show, the premier biennial B2B trucking industry event focusing on the needs of fleet owners, managers and decision makers, is North America’s largest and most comprehensive commercial vehicle trade show for fleets. North America is the world’s largest market for commercial vehicles with over 141 million vehicles in use across the continent. We are committed to serving the needs of this market and continuing to nurture its vital role in global commercial activity. Kyle Behnke, CEO & Owner, United Federal Logistics, Inc. “The NACV Show put all of the major manufacturers in one room and let us compare all of their new technology, apples to apples. That, and the people we met, helped us drive our truck-buying decision in the following year. We ended up buying 13 trucks, which for a small fleet like ours, was huge.” NACV Show 2017 by the numbers 439 370,000 234 6,000 exhibitors sq. ft. of exhibits accredited international journalists unique visitors NACV Show 2017 Attendees*: 93% rated the show as good or great had plans to purchase products or services 82% they saw on display at NACV Show 2017 planned to purchase from a new supplier after 63% the show were able to see all the products and services 89% they wanted to experience 95% indicated they were planning to attend in 2019 *Based on NACV Show 2017 attendee post-show survey. nacvshow.com Why NACV Show 2021? The NACV Show brings together fleets of ALL sizes, including the biggest and best, with a full range of industry products and services. -

Women in Trucking Association Holds 7Th Annual ˝Salute to Women Behind

Women In Trucking Association Holds 7th Annual “Salute to Women Behind the Wheel" The Women In Trucking Association, Inc. prepares to honor hundreds of female professional drivers at its seventh annual "Salute to Women Behind the Wheel" celebration held during the Mid-America Trucking Show in Louisville, Kentucky on April 2nd. Plover, WI (PRWEB) February 29, 2016 -- Although the trucking industry continues to be a male dominated business, more women are becoming drivers, technicians, managers, and owners. The Women In Trucking Association’s mission is to encourage and support these pioneers and to help address the challenges they face as a minority. The mission of the organization is to also celebrate the success of its members. The “Salute to Women Behind the Wheel” is an annual ceremony to honor female drivers and recognize them for their service. Any female professional driver is welcome to attend and will be honored on Saturday, April 2, at the Mid-America Trucking Show at the Kentucky Exposition Center in Louisville, Kentucky. The celebration begins at 11:00 am on the second floor of the South Wing (rooms C201-204) with exhibitors, music, goodie bags for the female drivers, and the WIT signature chocolate fountain. This year we’re adding a butterscotch fountain along with a huge tractor-trailer-shaped cake. Kari Rihm, President and CEO Rihm Kenworth and winner of the 2015 “Influential Woman in Trucking” Award, will address the group and honor the female drivers for their service. Rihm took over Rihm Kenworth, a family-owned business since 1932, after the passing of her husband in 2010. -

2010 Top 100 For-Hire

Europe: 1,052,045 Class 8 Luxembourg: 13,629 HCVs China: United States: 2,447 Concrete Mixers 6,692,703 Class 6–8 VIO 2010 April Reg Kansas City: • 82.1% cash 1,277 Class 8, 2005–2010 YM, purchases Freightliners • 17.9% loans Wayne County, MI: Chengdu City: 114,965 Commercial Pickups 321 Concrete Mixers Better Decisions. No Boundaries. The level of geography you want at the level of detail you need. When it comes to understanding which commercial vehicles are in your markets, having the world’s best data in-hand is crucial. Our data-driven solutions for the commercial vehicle industry help you maximize market share, identify emerging market trends, optimize inventory and target your best prospects – locally, globally or somewhere in between. Data-Driven Solutions for the Global Commercial Vehicle Industry www.polk.com/commercialvehicle A Word From the Publisher he headline for the 2010 TRANSPORT TOP- hire carriers are becoming more deeply involved in ICS’ Top 100 For-Hire Carriers was this: managing the movement of freight across many dif- “The Recovery Appears to Take Hold.” ferent modes and to and from many different places And while some trucking companies have in the world. reacted to positive economic news by ex- Still, it’s important to remember that over-the-road Tpanding the size of their fleets, many of the largest for- trucking is not going to disappear, or even shrink in hire carriers are taking a different approach — size. keeping a lid on the number of tractors and trailers American Trucking Associations said it expects rail while shifting the focus of their operations from long- intermodal tonnage will rise 83% to 253.1 million tons haul freight movement to local and regional distribu- in 2021 from 138.6 million tons in 2009. -

HITTING the MARK: Transportation Companies That Work for Women

Edition 3 | 2018 INSIDE... HITTING FOSTERING DIALOGUE THE MARK: About Gender Diversity Traits for SUCCESS 2018TOP 0 ANIES Driver Campaigns for MILLENNIALS Managing Holiday Stress SAME-GENDER TRAINING POLICY PHOTO CONTEST WINNERS At United Road, what makes us different makes us better. As the nation’s premier car-hauling expert, we transport over three million vehicles throughout North America each and every year. And what makes us the best, besides Carhaul Acquisition Expands Our Fleet Size Teamwork, New Investments In Equipment And Our North American Footprintour leading edge technology, industry-best capacity,Will andProduce Significant Positive Impacts Kathleen McCann, CEO Pat Riley, Senior Vice President diverse service offerings? Welcome to our newest team members! This edition of On the Road Our recent Over the coming months, you will see the was intentionally delayed because we wantedOUR to wait and PE shareO thisPLE. acquisition of transfer of truck equipment that is better suited to good news with you: United Road has completed its acquisition of the The Waggoners conduct the business that it was designed to do, carhaul divisionWe of Theinvite Waggoners you toTrucking learn Co. more We are soabout excited tothe women and men Trucking auto resulting in improved productivity and efficiency. welcome such a great group of professionals to our team! transport busi- Day cab quick loaders and high rail units will 2 3 Althoughthat this has make previously the been wheels communicated of United in various Roadways turn. ness expands work in rail ramp and regional locations where they over the last few weeks, it may be helpful to share the highlights of our United Road’s are best suited. -

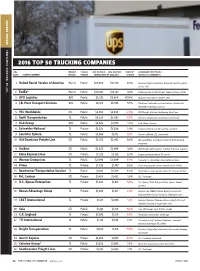

2016 Top 50 Trucking Companies 2016 Top 50 Trucking Companies

SPECIAL REPORT SPECIAL 2016 TOP 50 TRUCKING COMPANIES 2016 TOP 50 TRUCKING COMPANIES 2016 PRIMARY PUBLIC/ 2015 REVENUE 2016 REVENUE PERCENT SUBSIDIARY PORTFOLIO / RANK PARENT COMPANY SERVICE PRIVATE (IN MILLIONS OF DOLLARS) CHANGE SERVICES & COMMENTS 1 United Parcel Service of America Parcel Public $29,829 $31,770 6.5% Ground, freight, brokerage. Acquired Coyote Logistics in July 2015 TOP 50 TRUCKING COMPANIES TRUCKING 50 TOP 2 FedEx* Parcel Public $20,307 $22,127 9.0% FedEx Ground, FedEx Freight, FedEx Custom Critical 3 XPO Logistics IMC Public $3,273 $6,860 109.6% Acquired Con-way in October 2015 4 J.B. Hunt Transport Services IMC Public $6,188 $6,555 5.9% Truckload, dedicated contract service, intermodal, integrated capacity solutions 5 YRC Worldwide LTL Public $4,832 $4,698 -2.8% YRC Freight, Holland, Reddaway, New Penn 6 Swift Transportation TL Public $4,229 $4,032 -4.7% Dry-van, refrigerated, dedicated, nntermodal 7 Hub Group IMC Public $3,526 $3,573 1.3% Hub, Mode, Unyson 8 Schneider National TL Private $3,423 $3,506 2.4% Largest privately owned trucking company 9 Landstar System TL Public $3,364 $3,172 -5.7% Dry-van, flatbed, LTL, intermodal 10 Old Dominion Freight Line LTL Public $2,972 $2,992 0.6% Most profitable asset-based publicly held trucking company 11 ArcBest LTL Public $2,422 $2,496 3.0% ABF Freight, ABF Logistics, Panther Premium Logistics 12 Estes Express Lines LTL Private $2,135 $2,155 0.9% Largest privately owned LTL carrier 13 Werner Enterprises TL Public $2,094 $2,009 -4.0% One-way TL, dedicated, value-added services 14 Prime TL Private $1,736 $1,747 0.6% Prime Refrigerated, Prime Flatbed, Prime Tanker 15 Roadrunner Transportation Services TL Public $1,610 $1,709 6.2% Truckload revenue growth offset LTL revenue decline 16 R+L Carriers LTL Private $1,429 $1,452 1.6% LTL, Truckload 17 U.S.