Algeria's Economic Challenges

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

View Currency List

Currency List business.westernunion.com.au CURRENCY TT OUTGOING DRAFT OUTGOING FOREIGN CHEQUE INCOMING TT INCOMING CURRENCY TT OUTGOING DRAFT OUTGOING FOREIGN CHEQUE INCOMING TT INCOMING CURRENCY TT OUTGOING DRAFT OUTGOING FOREIGN CHEQUE INCOMING TT INCOMING Africa Asia continued Middle East Algerian Dinar – DZD Laos Kip – LAK Bahrain Dinar – BHD Angola Kwanza – AOA Macau Pataca – MOP Israeli Shekel – ILS Botswana Pula – BWP Malaysian Ringgit – MYR Jordanian Dinar – JOD Burundi Franc – BIF Maldives Rufiyaa – MVR Kuwaiti Dinar – KWD Cape Verde Escudo – CVE Nepal Rupee – NPR Lebanese Pound – LBP Central African States – XOF Pakistan Rupee – PKR Omani Rial – OMR Central African States – XAF Philippine Peso – PHP Qatari Rial – QAR Comoros Franc – KMF Singapore Dollar – SGD Saudi Arabian Riyal – SAR Djibouti Franc – DJF Sri Lanka Rupee – LKR Turkish Lira – TRY Egyptian Pound – EGP Taiwanese Dollar – TWD UAE Dirham – AED Eritrea Nakfa – ERN Thai Baht – THB Yemeni Rial – YER Ethiopia Birr – ETB Uzbekistan Sum – UZS North America Gambian Dalasi – GMD Vietnamese Dong – VND Canadian Dollar – CAD Ghanian Cedi – GHS Oceania Mexican Peso – MXN Guinea Republic Franc – GNF Australian Dollar – AUD United States Dollar – USD Kenyan Shilling – KES Fiji Dollar – FJD South and Central America, The Caribbean Lesotho Malati – LSL New Zealand Dollar – NZD Argentine Peso – ARS Madagascar Ariary – MGA Papua New Guinea Kina – PGK Bahamian Dollar – BSD Malawi Kwacha – MWK Samoan Tala – WST Barbados Dollar – BBD Mauritanian Ouguiya – MRO Solomon Islands Dollar – -

An Empirical Test of Purchasing Power Parity of the Algerian Exchange Rate: Evidence from Panel Dynamic

Munich Personal RePEc Archive An Empirical Test of Purchasing Power Parity of the Algerian Exchange Rate: Evidence from Panel Dynamic Si Mohammed, Kamel and Chérif touil, Noreddine and Maliki, Samir University of Ain Temouchent, University of Mostaganem, University of Tlemcen November 2015 Online at https://mpra.ub.uni-muenchen.de/75285/ MPRA Paper No. 75285, posted 28 Nov 2016 10:24 UTC An Empirical Test of Purchasing Power Parity of the Algerian Exchange Rate: Evidence from Panel Dynamic Kamel Si Mohammed, (PhD economics) Assistant Professor, Ain Temouchent University, Algeria Noreddine Chérif Touil PhD in economy, Associate Professor, Mostaganem University, Algeria Samir MALIKI PhD , Full Professor, Tlemcen University, Algeria [email protected] Abstract: The goal of this study is to examine the validity of the long-run purchasing power parity (PPP) for a sample of nine principle trade partners of Algeria namely Canada, China, Japan, Switzerland, Sweden, Turkey, the United Kingdom, the United States and the euro zone countries. Using panel error correction model (PECM) upon monthly data for the period 2003 M1 – 2015M5, results suggested that the bilateral exchange rate movements is a suitable to support the purchasing power parity (PPP) hypothesis. However, suggesting that there is long run relationship between exchange rates and relative prices in foreign courtiers by using panel cointegraion of Pedroni (1999, 2004), that can be interpreted by the validity of purchasing power parity for nine principle trade partners of Algeria. Key Words: (Algeria, panel cointegration, Purchasing Power Parity (PPP), panel error correction model (PECM) 1 I. Introduction: Since 1996, the Bank of Algeria (Central Bank) adopted the floating exchange rate regime after a long period from 1997 to 1996 characterized by a strong dominance of the reference to US dollars due to the particularity of Algerian economy, an economy based on exports of oil - 98percent of export revenues paid in US dollars and imports, rising continuously, paid in euro ((Kamel et al, 2014). -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic -

Maximum Monthly Stipend Rates for Fellows And

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS Sep 2020 COUNTRY Local Currency Local DSA MAX RES RATE MAX TRV RATE Effective % date Afghanistan Afghani 12,500 131,250 196,875 1-Aug-07 * Albania Albania Lek(e) 13,100 206,325 309,488 1-Jan-05 Algeria Algerian Dinar 31,600 331,800 497,700 1-Aug-07 * Angola Kwanza 134,000 1,407,000 2,110,500 1-Aug-07 #N/A Antigua and Barbuda (1 Apr. - 30 Nov.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 #N/A Antigua and Barbuda (1 Dec. - 31 Mar.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 * Argentina Argentine Peso 19,700 162,525 243,788 1-Jan-05 Australia AUL Dollar 453 4,757 7,135 1-Aug-07 Australia - Academic AUL Dollar 453 1,200 7,135 1-Aug-07 Austria Euro 261 2,741 4,111 1-Aug-07 Azerbaijan (new)Azerbaijan Manat 239 1,613 2,420 1-Jan-05 Bahrain Bahraini Dinar 106 2,226 3,180 1-Jan-05 Bahrain - Academic Bahraini Dinar 106 1,113 1,670 1-Aug-07 Bangladesh Bangladesh Taka 12,400 130,200 195,300 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 * Belarus New Belarusian Ruble 680 6,630 9,945 1-Jan-06 Belgium Euro 338 3,549 5,324 1-Aug-07 Benin CFA Franc(XOF) 123,000 1,291,500 1,937,250 1-Aug-07 Bhutan Bhutan Ngultrum 7,290 76,545 114,818 1-Aug-07 Bolivia Boliviano 1,180 10,620 15,930 1-Jan-07 * Bosnia and Herzegovina Convertible Mark 264 3,366 5,049 1-Jan-05 Botswana Botswana Pula 2,220 23,310 34,965 1-Aug-07 Brazil Brazilian Real 530 4,373 6,559 1-Jan-05 British Virgin Islands (16 Apr. -

The Journal of Studies in Language, Culture and Society (JSLCS)

Volume 1/N°1 December, 2018 The Journal of Studies in Language, Culture and Society (JSLCS) Editor in chief: Dr. Nadia Idri UNIVERSITÉ ABDERRAHMANE MIRA BEJAIA FACULTÉ DES LETTRES ET DES LANGUES www.univ-bejaia/JSLCS ISSN : 1750-2676 © All rights reserved Journal of Studies in Language, Culture and Society (JSLCS) is an academic multidisciplinary open access and peer-reviewed journal that publishes original research that turns around phenomena related to language, culture and society. JSLCS welcomes papers that reflect sound methodologies, updated theoretical analyses and original empirical and practical findings related to various disciplines like linguistics and languages, civilisation and literature, sociology, psychology, translation, anthropology, education, pedagogy, ICT, communication, cultural/inter-cultural studies, philosophy, history, religion, and the like. Editor in Chief Dr Nadia Idri, Faculty of Arts and Languages, University of Bejaia, Algeria Editorial Board Abdelhak Elaggoune, University 8 Mai 1945, Guelma, Algeria Ahmed Chaouki Hoadjli, University of Biskra, Algeria Amar Guendouzi, University Mouloud Mammeri, Tizi Ouzou, Algeria Amine Belmekki, University of tlemcen, Algeria Anita Welch, Institute of Education, USA Christian Ludwig, Essen/NRW, Germany Christophe Ippolito Chris, School of Modern Languages at Georgia Tech’s Ivan Allen College of Liberal Arts, Georgia Institute of Technology, Atlanta, USA Farouk Bouhadiba, University of Oran, Algeria Fodil Sadek, University Mouloud Mammeri, Tizi Ouzou, Algeria Fouad Mami, University of Adrar, Algeria Ghania Ouahmiche, University of Oran, Algeria Hacène Hamada, Ens Constantine, Algeria Hanane Sarnou, University of Mostaganem, Algeria Judit Papp, Hungarian Language and Literature, University of Naples "L'Orientale" Leyla Bellour, Mila University Center, Algeria Limame Barbouchi, Faculty of Chariaa in Smara, Ibn Zohr University, Agadir, Morocco Manisha Anand Patil, Head, Yashavantrao Chavan Institute of Science, India Mimouna Zitouni, University of Mohamed Ben Ahmed, Oran 2, Algeria Mohammad H. -

The Fluctuations of the Algerian Dinar Exchange Rate Against the Euro and Its Impact on the Algerian Trade Balance During the Period (1999- 2014)

(2014 - 1999) [email protected] Aggoun.charaf@yahoo. The Fluctuations of the Algerian Dinar Exchange Rate Against the Euro and its Impact on the Algerian Trade Balance During the Period (1999- 2014) : %97 . ( ) . : Abstract: This studyaimed to investigate the impact of the fluctuations of the Algerian dinar exchange rate against the euro on the Algerian trade balance. Yet, in light of the continuousreduction of the Algerian dinar against the euro in order to encourage exports and reduce imports. EspeciallythosebroughtfromEuropean Union,takingintoconsiderationAlgeria'sforeigntradesector, whichaccounts for more than 97% of its exportson fuel and denominated in US dollars and about two-thirds of imports come from the European Union and priced in euros.Therefore,the state chargedthe cost of differencesbetweencurrencies.Theco-integration test wasemployed to examine the relationshipbetween the Algerian trade balance and the Algerian dinar exchange rateagainst the euro. The studyconcludedthatthereis no long-termrelationshipbetween the Algerian trade balance and the dollar exchange rate for the euro,thisis due to the nature of Algeria'sforeigntrade, which relies mainly on the hydrocarbonsector. Key words: Exchange rate, Trade Balance, Import, Export, Euro. : ( ) . %97 ( ) . ( ) . : : . - : . : -1 -2 . -3 209 « » 2017 03 : : . : -1-1 .1 : . : . 2 : :( ) - 3 . .( ) : - . : -2-1 : ( ) - . ( ) - : -3-1 . : : -1-3-1 « » 210 2017 03 : Dépriciation ( ) - . :Appréciation ( ) - . .4 :Dévaluation - .6 5 . :Réévaluation - : -2-3-1 . ) : - ( . : - . : - - - .7 ( ) - : : . 211 « » 2017 03 : -1-2 01 2003 %5 %5 % 2 2008 2014 106.9 2008 94.89 . :(2014 -1999) -2-2 2014 1999 02 2000 12.3 1999 3.36 . 6.7 2002 2001 2000 40.6 2008 2003 . 7.78 2009 2008 2012 2011 20.17 25.96 2010 . -

WM/Refinitiv Closing Spot Rates

The WM/Refinitiv Closing Spot Rates The WM/Refinitiv Closing Exchange Rates are available on Eikon via monitor pages or RICs. To access the index page, type WMRSPOT01 and <Return> For access to the RICs, please use the following generic codes :- USDxxxFIXz=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR, GBP or CHF xxx can be any of the following currencies :- Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy -

January 2020

Country Policy and Information Note Algeria: Internal relocation and background information Version 1.0 September 2020 Preface Purpose This note provides a summary of and links to country of origin information (COI) for use by Home Office decision makers handling particular types of protection and human rights claims. It is not intended to be an exhaustive survey of a particular subject or theme. It is split into two main sections: (1) general background to the country concerned, including demography and geography; and (2) issues which may be relevant to protection claims. Unlike country policy and information notes, it does not contain an assessment of risk, availability of protection or reasonableness of internal relocation. Decision makers must, however, still consider all claims on an individual basis, taking into account each case’s specific facts. Country of origin information The country information in this note has been carefully selected in accordance with the general principles of COI research as set out in the Common EU [European Union] Guidelines for Processing Country of Origin Information (COI), dated April 2008, and the Austrian Centre for Country of Origin and Asylum Research and Documentation’s (ACCORD), Researching Country Origin Information – Training Manual, 2013. Namely, taking into account the COI’s relevance, reliability, accuracy, balance, currency, transparency and traceability. The structure and content of the country information section follows a terms of reference which sets out the general and specific topics relevant to this note. All information included in the note was published or made publicly available on or before the ‘cut-off’ date in the country information section. -

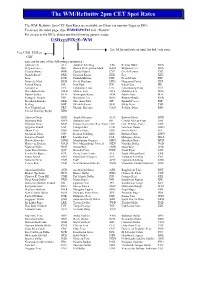

WM/Refinitiv 2Pm CET Spot Rates

The WM/Refinitiv 2pm CET Spot Rates The WM/ Refinitiv 2pm CET Spot Rates are available on Eikon via monitor Pages or RICs. To access the index page, type WMRESPOT01 and <Return> For access to the RICs, please use the following generic codes : USDxxxFIXzE=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR or GBP xxx can be any of the following currencies : Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy Ariary -

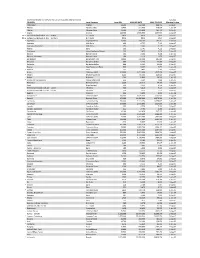

Maximum Monthly Stipend Rates For

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS Mar 2021 COUNTRY Local Currency Local DSA MAX RES RATE MAX TRV RATE Effective % date Afghanistan Afghani 12,600 132,300 198,450 1-Aug-07 * Albania Albania Lek(e) 13,400 211,050 316,575 1-Jan-05 Algeria Algerian Dinar 31,600 331,800 497,700 1-Aug-07 * Angola Kwanza 146,000 1,533,000 2,299,500 1-Aug-07 #N/A Antigua and Barbuda (1 Apr. - 30 Nov.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 #N/A Antigua and Barbuda (1 Dec. - 31 Mar.) E.C. Dollar #N/A #N/A #N/A 1-Aug-07 * Argentina Argentine Peso 23,900 197,175 295,763 1-Jan-05 Australia AUL Dollar 453 4,757 7,135 1-Aug-07 Australia - Academic AUL Dollar 453 1,200 7,135 1-Aug-07 Austria Euro 261 2,741 4,111 1-Aug-07 * Azerbaijan (new)Azerbaijan Manat 240 1,620 2,430 1-Jan-05 Bahrain Bahraini Dinar 106 2,226 3,180 1-Jan-05 Bahrain - Academic Bahraini Dinar 106 1,113 1,670 1-Aug-07 Bangladesh Bangladesh Taka 12,400 130,200 195,300 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 Barbados Barbados Dollar 880 9,240 13,860 1-Aug-07 Belarus New Belarusian Ruble 660 6,435 9,653 1-Jan-06 * Belgium Euro 333 3,497 5,245 1-Aug-07 Benin CFA Franc(XOF) 123,000 1,291,500 1,937,250 1-Aug-07 * Bhutan Bhutan Ngultrum 8,200 86,100 129,150 1-Aug-07 * Bolivia Boliviano 1,200 10,800 16,200 1-Jan-07 * Bosnia and Herzegovina Convertible Mark 256 3,264 4,896 1-Jan-05 Botswana Botswana Pula 2,220 23,310 34,965 1-Aug-07 Brazil Brazilian Real 530 4,373 6,559 1-Jan-05 British Virgin Islands (16 Apr. -

FAO Country Name ISO Currency Code* Currency Name*

FAO Country Name ISO Currency Code* Currency Name* Afghanistan AFA Afghani Albania ALL Lek Algeria DZD Algerian Dinar Amer Samoa USD US Dollar Andorra ADP Andorran Peseta Angola AON New Kwanza Anguilla XCD East Caribbean Dollar Antigua Barb XCD East Caribbean Dollar Argentina ARS Argentine Peso Armenia AMD Armeniam Dram Aruba AWG Aruban Guilder Australia AUD Australian Dollar Austria ATS Schilling Azerbaijan AZM Azerbaijanian Manat Bahamas BSD Bahamian Dollar Bahrain BHD Bahraini Dinar Bangladesh BDT Taka Barbados BBD Barbados Dollar Belarus BYB Belarussian Ruble Belgium BEF Belgian Franc Belize BZD Belize Dollar Benin XOF CFA Franc Bermuda BMD Bermudian Dollar Bhutan BTN Ngultrum Bolivia BOB Boliviano Botswana BWP Pula Br Ind Oc Tr USD US Dollar Br Virgin Is USD US Dollar Brazil BRL Brazilian Real Brunei Darsm BND Brunei Dollar Bulgaria BGN New Lev Burkina Faso XOF CFA Franc Burundi BIF Burundi Franc Côte dIvoire XOF CFA Franc Cambodia KHR Riel Cameroon XAF CFA Franc Canada CAD Canadian Dollar Cape Verde CVE Cape Verde Escudo Cayman Is KYD Cayman Islands Dollar Cent Afr Rep XAF CFA Franc Chad XAF CFA Franc Channel Is GBP Pound Sterling Chile CLP Chilean Peso China CNY Yuan Renminbi China, Macao MOP Pataca China,H.Kong HKD Hong Kong Dollar China,Taiwan TWD New Taiwan Dollar Christmas Is AUD Australian Dollar Cocos Is AUD Australian Dollar Colombia COP Colombian Peso Comoros KMF Comoro Franc FAO Country Name ISO Currency Code* Currency Name* Congo Dem R CDF Franc Congolais Congo Rep XAF CFA Franc Cook Is NZD New Zealand Dollar Costa Rica -

List of Currencies of All Countries

The CSS Point List Of Currencies Of All Countries Country Currency ISO-4217 A Afghanistan Afghan afghani AFN Albania Albanian lek ALL Algeria Algerian dinar DZD Andorra European euro EUR Angola Angolan kwanza AOA Anguilla East Caribbean dollar XCD Antigua and Barbuda East Caribbean dollar XCD Argentina Argentine peso ARS Armenia Armenian dram AMD Aruba Aruban florin AWG Australia Australian dollar AUD Austria European euro EUR Azerbaijan Azerbaijani manat AZN B Bahamas Bahamian dollar BSD Bahrain Bahraini dinar BHD Bangladesh Bangladeshi taka BDT Barbados Barbadian dollar BBD Belarus Belarusian ruble BYR Belgium European euro EUR Belize Belize dollar BZD Benin West African CFA franc XOF Bhutan Bhutanese ngultrum BTN Bolivia Bolivian boliviano BOB Bosnia-Herzegovina Bosnia and Herzegovina konvertibilna marka BAM Botswana Botswana pula BWP 1 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Brazil Brazilian real BRL Brunei Brunei dollar BND Bulgaria Bulgarian lev BGN Burkina Faso West African CFA franc XOF Burundi Burundi franc BIF C Cambodia Cambodian riel KHR Cameroon Central African CFA franc XAF Canada Canadian dollar CAD Cape Verde Cape Verdean escudo CVE Cayman Islands Cayman Islands dollar KYD Central African Republic Central African CFA franc XAF Chad Central African CFA franc XAF Chile Chilean peso CLP China Chinese renminbi CNY Colombia Colombian peso COP Comoros Comorian franc KMF Congo Central African CFA franc XAF Congo, Democratic Republic Congolese franc CDF Costa Rica Costa Rican colon CRC Côte d'Ivoire West African CFA franc XOF Croatia Croatian kuna HRK Cuba Cuban peso CUC Cyprus European euro EUR Czech Republic Czech koruna CZK D Denmark Danish krone DKK Djibouti Djiboutian franc DJF Dominica East Caribbean dollar XCD 2 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Dominican Republic Dominican peso DOP E East Timor uses the U.S.