WM/Refinitiv Closing Spot Rates

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Public Opinion in Bulgaria in 2018: EU Membership and Further Integration

Policy brief June 2018 Public opinion in Bulgaria in 2018: EU membership and further integration Marin Lessenski, Open Society Institute – Sofia www.osis.bg Contents Introduction and summary of the findings ................................................................................................... 2 Results concerning EU membership ............................................................................................................. 3 Assessment of EU membership .................................................................................................................... 4 Advantages of EU membership ..................................................................................................................... 5 Support to parties that would want leaving the EU ..................................................................................... 7 Support to further integration: Eurozone membership ............................................................................... 8 Comparison between questions about Eurozone membership and replacing the lev with the euro ........ 10 Support to further integration: Schengen membership ............................................................................. 12 Trust in institutions and the EU .................................................................................................................. 12 Results according to profiles of the respondents ....................................................................................... 13 June 2018 Public -

List 283 | October 2014

Stephen Album Rare Coins Specializing in Islamic, Indian & Oriental Numismatics P.O. Box 7386, Santa Rosa, CA. 95407, U.S.A. 283 Telephone 707-539-2120 — Fax 707-539-3348 [email protected] Catalog price $5.00 www.stevealbum.com 137187. SAFAVID: Muhammad Khudabandah, 1578-1588, AV ½ OCTOBER 2014 mithqal (2.31g), Mashhad, AH[9]85, A-2616.2, type A, with epithet imam reza, some flatness, some (removable) dirt Gold Coins on obverse, VF, R, ex. Richard Accola collection $350 137186. SAFAVID: Muhammad Khudabandah, 1578-1588, AV mithqal (4.59g), Qazwin, AH[9]89, A-2617.2, type B, some weakness Ancient Gold towards the rim, VF, R, ex. Richard Accola collection $450 137190. SAFAVID: Sultan Husayn, 1694-1722, AV ashrafi (3.47g), Mashhad, AH1130, A-2669E, local design, used only at Mashhad, 138883. ROMAN EMPIRE: Valentinian I, 364-375 AD, AV solidus the site of the tomb of the 8th Shi’ite Imam, ‘Ali b. Musa al-Reza, (4.47g), Thessalonica, bust facing right, pearl-diademed, no weakness, VF, RRR, ex. Richard Accola collection $1,000 draped & cuirassed / Valentinian & Valens seated, holding The obverse text is hoseyn kalb-e astan-e ‘ali, “Husayn, dog at together a globe, Victory behind with outspread wings, the doorstep of ‘Ali.,” with additional royal text in the obverse SMTES below, very tiny rim nick, beautiful bold strike, margin, not found on the standard ashrafis of type #2669. choice EF, R $1,200 By far the most common variety of this type is of the Trier 137217. AFSHARID: Shahrukh, 2nd reign, 1750-1755, AV mohur mint, with Constantinople also relatively common. -

Treasury Reporting Rates of Exchange As of December 31, 2018

TREASURY REPORTING RATES OF EXCHANGE AS OF DECEMBER 31, 2018 COUNTRY-CURRENCY F.C. TO $1.00 AFGHANISTAN - AFGHANI 74.5760 ALBANIA - LEK 107.0500 ALGERIA - DINAR 117.8980 ANGOLA - KWANZA 310.0000 ANTIGUA - BARBUDA - E. CARIBBEAN DOLLAR 2.7000 ARGENTINA-PESO 37.6420 ARMENIA - DRAM 485.0000 AUSTRALIA - DOLLAR 1.4160 AUSTRIA - EURO 0.8720 AZERBAIJAN - NEW MANAT 1.7000 BAHAMAS - DOLLAR 1.0000 BAHRAIN - DINAR 0.3770 BANGLADESH - TAKA 84.0000 BARBADOS - DOLLAR 2.0200 BELARUS - NEW RUBLE 2.1600 BELGIUM-EURO 0.8720 BELIZE - DOLLAR 2.0000 BENIN - CFA FRANC 568.6500 BERMUDA - DOLLAR 1.0000 BOLIVIA - BOLIVIANO 6.8500 BOSNIA- MARKA 1.7060 BOTSWANA - PULA 10.6610 BRAZIL - REAL 3.8800 BRUNEI - DOLLAR 1.3610 BULGARIA - LEV 1.7070 BURKINA FASO - CFA FRANC 568.6500 BURUNDI - FRANC 1790.0000 CAMBODIA (KHMER) - RIEL 4103.0000 CAMEROON - CFA FRANC 603.8700 CANADA - DOLLAR 1.3620 CAPE VERDE - ESCUDO 94.8800 CAYMAN ISLANDS - DOLLAR 0.8200 CENTRAL AFRICAN REPUBLIC - CFA FRANC 603.8700 CHAD - CFA FRANC 603.8700 CHILE - PESO 693.0800 CHINA - RENMINBI 6.8760 COLOMBIA - PESO 3245.0000 COMOROS - FRANC 428.1400 COSTA RICA - COLON 603.5000 COTE D'IVOIRE - CFA FRANC 568.6500 CROATIA - KUNA 6.3100 CUBA-PESO 1.0000 CYPRUS-EURO 0.8720 CZECH REPUBLIC - KORUNA 21.9410 DEMOCRATIC REPUBLIC OF CONGO- FRANC 1630.0000 DENMARK - KRONE 6.5170 DJIBOUTI - FRANC 177.0000 DOMINICAN REPUBLIC - PESO 49.9400 ECUADOR-DOLARES 1.0000 EGYPT - POUND 17.8900 EL SALVADOR-DOLARES 1.0000 EQUATORIAL GUINEA - CFA FRANC 603.8700 ERITREA - NAKFA 15.0000 ESTONIA-EURO 0.8720 ETHIOPIA - BIRR 28.0400 -

The Internationalization of the RMB Opportunities and Pitfalls

Maurice R. Greenberg Center for Geoeconomic Studies and International Institutions and Global Governance Program The Internationalization of the RMB Opportunities and Pitfalls Takatoshi Ito November 2011 This publication has been made possible by the generous support of the Robina Foundation. The Council on Foreign Relations (CFR) is an independent, nonpartisan membership organization, think tank, and publisher dedicated to being a resource for its members, government officials, busi- ness executives, journalists, educators and students, civic and religious leaders, and other interested citizens in order to help them better understand the world and the foreign policy choices facing the United States and other countries. Founded in 1921, CFR carries out its mission by maintaining a diverse membership, with special programs to promote interest and develop expertise in the next generation of foreign policy leaders; convening meetings at its headquarters in New York and in Washington, DC, and other cities where senior government officials, members of Congress, global leaders, and prominent thinkers come together with CFR members to discuss and debate major in- ternational issues; supporting a Studies Program that fosters independent research, enabling CFR scholars to produce articles, reports, and books and hold roundtables that analyze foreign policy is- sues and make concrete policy recommendations; publishing Foreign Affairs, the preeminent journal on international affairs and U.S. foreign policy; sponsoring Independent Task Forces that produce reports with both findings and policy prescriptions on the most important foreign policy topics; and providing up-to-date information and analysis about world events and American foreign policy on its website, CFR.org. The Council on Foreign Relations takes no institutional positions on policy issues and has no affilia- tion with the U.S. -

FCAS Rates of Exchange December 2019.Xlsx

TREASURY REPORTING RATES OF EXCHANGE As of December 31, 2019 Country‐Currency Foreign Currency To $1.00 Afghanistan-Afghani 77.6250 Albania-Lek 108.2100 Algeria-Dinar 118.7800 Angola-Kwanza 475.0000 Antigua & Barbuda-E. Caribbean Dollar 2.7000 Argentina-Peso 59.8700 Armenia-Dram 475.0000 Australia-Dollar 1.4250 Austria-Euro 0.8900 Azerbaijan-Manat 1.7000 Bahamas-Dollar 1.0000 Bahrain-Dinar 0.3770 Bangladesh-Taka 85.0000 Barbados-Dollar 2.0200 Belarus-New Ruble 2.1040 Belgium-Euro 0.8900 Belize-Dollar 2.0000 Benin-CFA Franc 582.0000 Bermuda-Dollar 1.0000 Bolivia-Boliviano 6.8300 Bosnia-Marka 1.7410 Botswana-Pula 10.5490 Brazil-Real 4.0200 Brunei-Dollar 1.3450 Bulgaria-Lev New 1.7410 Burkina Faso-CFA Franc 582.0000 Burma-Kyat 1,475.0000 Burundi-Franc 1,850.0000 Cambodia-Riel 4,051.0000 Cameroon-CFA Franc 578.1200 Canada-Dollar 1.3000 Cape Verde-Escudo 99.2910 Cayman Island-Dollar 0.8200 Central African Rep.-CFA Franc 578.1200 Chad-CFA Franc 578.1200 Chile-Peso 751.4800 China-Renminbi 6.9610 Colombia-Peso 3,278.7500 Comoros-Franc 439.0600 Congo-CFA Franc 578.1200 Costa Rica-Colon 569.6500 Cote D'ivoire-CFA Franc 582.0000 Croatia-KUNA 6.4900 Cross Border-Euro 0.8900 Cuba-Chavito 1.0000 Cyprus-Euro 0.8900 Czech. Republic-Koruna 22.1650 Dem. Rep. of Congo-Franc 1,650.0000 Denmark-Krone 6.6520 Djibouti-Franc 177.0000 Dominican Republic-Peso 52.6600 Ecuador-Dolares 1.0000 Egypt-Pound 16.0000 El Salvador-Dollar 1.0000 Equatorial Guinea-CFA Franc 578.1200 Eritrea-Nakfa 15.0000 Eritrea-Nakfa Salary Payment 15.0000 Estonia-Euro 0.8900 Ethiopia-Birr -

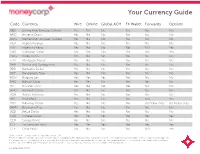

Your Currency Guide

Your Currency Guide Code Currency Wire Online Global ACH FX Wallet Forwards Options AED United Arab Emirates Dirham Yes Yes No Yes Yes No AMD Armenia Dram Yes No No No No No ANG Netherlands Antillean Guilder Yes No No No No No AOA Angola Kwanza Yes No No No No No ARS Argentina Peso Yes No No No NDF Yes AUD Australian Dollar Yes Yes Yes Yes Yes Yes AWG Aruba Florin Yes No No No No No AZN Azerbaijan Manat Yes No No No No No BAM Bosnia and Herzegovina Yes No No No No No BBD Barbados Dollar Yes No No Yes No No BDT Bangladesh Taka Yes No No No No No BGN Bulgaria Lev Yes Yes Yes Yes No No BHD Bahrain Dinar Yes Yes No Yes Yes No BIF Burundi Franc Yes No No No No No BMD Bermuda Dollar Yes No No No No No BOB Bolivia Boliviano Yes No No No No No BRL Brazil Real Yes No No No NDF Yes BSD Bahamas Dollar Yes No No No US Dollar only US Dollar only BWP Botswana Pula Yes No No Yes No No BZD Belize Dollar Yes No No No No No CAD Canada Dollar Yes Yes Yes Yes Yes Yes CDF Congo Franc Yes No No No No No CHF Switzerland Franc Yes Yes Yes Yes Yes Yes CLP Chile Peso Yes No No No NDF Yes *Some ciurrencies may require a copy of beneficiaries ID. This list is subject to change, and currencies are subject to availability. The ability you have to purchase currencies through moneycorp is subject to the completion and approval of a moneycorp account application and any other documentation deemed to be required by moneycorp. -

Is the Botswana Pula Misaligned?

BIDPA Working Paper 33 July 2012 Is the Botswana Pula Misaligned? Haile Taye BOTSWANA INSTITUTE FOR DEVELOPMENT POLICY ANALYSIS BIDPA The Botswana Institute for Development Policy Analysis (BIDPA) is an independent trust, which started operations in 1995 as a non-governmental policy research institution. BIDPA’s mission is to inform policy and build capacity through research and consultancy services. BIDPA is funded by the Botswana government and the African Capacity Building Foundation. BIDPA Working Paper Series The series comprises of papers which reflect work in progress or limited research efforts, which may be of interest to researchers and policy makers, or of a public education character. Working papers may already have been published elsewhere or may appear in other publications. Haile Taye is a Senior Research Fellow at the Botswana Institute for Development Policy Analysis. ISBN: 99912-65-44-9 © Botswana Institute for Development Policy Analysis, 2012 Disclaimer: The views expressed in this document are entirely those of the author and do not necessarily reflect the official opinion of BIDPA. TABLE OF CONTENTS Acknowledgements ................................................................................................. iv Abstract ................................................................................................................... iv 1. Introduction ......................................................................................................... 1 2. Determinants of the Equilibrium Exchange Rate ............................................ -

Argentina's Economic Crisis

Updated January 28, 2020 Argentina’s Economic Crisis Argentina is grappling with a serious economic crisis. Its Meanwhile, capital inflows into the country to finance the currency, the peso, has lost two-thirds of its value since deficit contributed to an overvaluation of the peso, by 10- 2018; inflation is hovering around 30%; and since 2015 the 25%. This overvaluation also exacerbated Argentina’s economy has contracted by about 4% and its external debt current account deficit (a broad measure of the trade has increased by 60%. In June 2018, the Argentine balance), which increased from 2.7% of GDP in 2016 to government turned to the International Monetary Fund 4.8% of GDP in 2017. (IMF) for support and currently has a $57 billion IMF program, the largest program (in dollar terms) in IMF Crisis and Initial Policy Response history. Despite these resources, the government in late Argentina’s increasing reliance on external financing to August and early September 2019 postponed payments on fund its budget and current account deficits left it some of its debts and imposed currency controls. vulnerable to changes in the cost or availability of financing. Starting in late 2017, several factors created In the October 2019 general election, the center-right problems for Argentina’s economy: the U.S. Federal incumbent President Mauricio Macri lost to the center-left Reserve (Fed) began raising interest rates, reducing investor Peronist ticket of Alberto Fernández for president and interest in Argentine bonds; the Argentine central bank former President Cristina Fernández de Kirchner for vice reset its inflation targets, raising questions about its president. -

Bulgaria Economy Briefing: BULGARIA on HER WAY to the EUROZONE – CURRENT STATUS, POSITIVE and NEGATIVE IMPACTS Evgeniy Kandilarov

ISSN: 2560-1601 Vol. 17, No. 2 (BG) April 2019 Bulgaria economy briefing: BULGARIA ON HER WAY TO THE EUROZONE – CURRENT STATUS, POSITIVE AND NEGATIVE IMPACTS Evgeniy Kandilarov 1052 Budapest Petőfi Sándor utca 11. +36 1 5858 690 Kiadó: Kína-KKE Intézet Nonprofit Kft. [email protected] Szerkesztésért felelős személy: Chen Xin Kiadásért felelős személy: Huang Ping china-cee.eu 2017/01 BULGARIA ON HER WAY TO THE EUROZONE – CURRENT STATUS, POSITIVE AND NEGATIVE IMPACTS One of the very substantial things with a serious financial and economic impact that has been planned to happen in 2019 is the Bulgaria to join t the so called Exchange Rate Mechanism (ERM2) as well as the European Banking Union as a precondition of the entrance of country in the Eurozone. The ERM II is the European Central Bank’s exchange rate mechanism, sometimes referred to as the “waiting room” for the Euro. Bulgaria’s government approved on July 18 2018 the formal application for close co-operation with the European central bank (ECB), the first step towards joining the ERM II. The agreement on ERM II preparation includes several additional commitments, which will help support financial sector supervision, improve SOE governance, and strengthen the anti-money laundering (AML) framework. Completing these commitments and joining ERM II and the banking union would further underpin the credibility of policies, in addition to many benefits that the EU membership has brought. The "Eurozone waiting room" is a jargon that appeared about 20 years ago. The idea is that when countries did not have a very fixed exchange rate between themselves before entering the euro, they had a minimum of 2 years of preparatory period in which the exchange rates were expected, the interest rates to get closer. -

Currency Codes COP Colombian Peso KWD Kuwaiti Dinar RON Romanian Leu

Global Wire is an available payment method for the currencies listed below. This list is subject to change at any time. Currency Codes COP Colombian Peso KWD Kuwaiti Dinar RON Romanian Leu ALL Albanian Lek KMF Comoros Franc KGS Kyrgyzstan Som RUB Russian Ruble DZD Algerian Dinar CDF Congolese Franc LAK Laos Kip RWF Rwandan Franc AMD Armenian Dram CRC Costa Rican Colon LSL Lesotho Malati WST Samoan Tala AOA Angola Kwanza HRK Croatian Kuna LBP Lebanese Pound STD Sao Tomean Dobra AUD Australian Dollar CZK Czech Koruna LT L Lithuanian Litas SAR Saudi Riyal AWG Arubian Florin DKK Danish Krone MKD Macedonia Denar RSD Serbian Dinar AZN Azerbaijan Manat DJF Djibouti Franc MOP Macau Pataca SCR Seychelles Rupee BSD Bahamian Dollar DOP Dominican Peso MGA Madagascar Ariary SLL Sierra Leonean Leone BHD Bahraini Dinar XCD Eastern Caribbean Dollar MWK Malawi Kwacha SGD Singapore Dollar BDT Bangladesh Taka EGP Egyptian Pound MVR Maldives Rufi yaa SBD Solomon Islands Dollar BBD Barbados Dollar EUR EMU Euro MRO Mauritanian Olguiya ZAR South African Rand BYR Belarus Ruble ERN Eritrea Nakfa MUR Mauritius Rupee SRD Suriname Dollar BZD Belize Dollar ETB Ethiopia Birr MXN Mexican Peso SEK Swedish Krona BMD Bermudian Dollar FJD Fiji Dollar MDL Maldavian Lieu SZL Swaziland Lilangeni BTN Bhutan Ngultram GMD Gambian Dalasi MNT Mongolian Tugrik CHF Swiss Franc BOB Bolivian Boliviano GEL Georgian Lari MAD Moroccan Dirham LKR Sri Lankan Rupee BAM Bosnia & Herzagovina GHS Ghanian Cedi MZN Mozambique Metical TWD Taiwan New Dollar BWP Botswana Pula GTQ Guatemalan Quetzal -

Q3-Q4/16 – Two Centuries of Currency Policy in Austria

Two centuries of currency policy in Austria This paper is devoted to currency policies in Austria over the last 200 years, attempting to Heinz Handler1 sketch historical developments and uncover regularities and interconnections with macroeco- nomic variables. While during the 19th century the exchange rate resembled a kind of technical relation, since World War I (WW I) it has evolved as a policy instrument with the main objec- tives of controlling inflation and fostering productivity. During most of the 200-year period, Austrian currencies were subject to fixed exchange rates, in the form of silver and gold standards in the 19th century, as a gold-exchange standard and hard currency policy in much of the 20th century, and with the euro as the single currency in the early 21st century. Given Austria’s euro area membership, national exchange rate policy has been relinquished in favor of a common currency which itself is floating vis-à-vis third currencies. Austria’s predilection for keeping exchange rates stable is due not least to the country’s transformation from one of Europe’s few great powers (up to WW I) to a small open economy closely tied to the large German economy. JEL classification: E58, F31, N13, N14, N23, N24 Keywords: currency history, exchange rate policy, central bank, Austria When the privilegirte oesterreichische versus flexible exchange rates. During National-Bank (now Oesterreichische most of the period considered here, Nationalbank – OeNB)2 was chartered Austrian currencies were subject to in 1816, the currency systems of major fixed exchange rates, in the form of sil- nations were not standardized by any ver and gold standards in the 19th cen- formal agreement, although in practice tury, as a gold-exchange standard in a sort of specie standard prevailed. -

GENERAL CONFERENCE Industrial Development Board

Distr. GENERAL GC.8/15 IDB.21/30 31 August 1999 United Nations Industrial Development Organization ORIGINAL: ENGLISH GENERAL CONFERENCE Eighth session Vienna, 29 November - 3 December 1999 Item 11 (g) of the provisional agenda Industrial Development Board Resumed twenty-first session Vienna, 29 November 1999 Agenda item 4 (j) IMPLICATIONS OF THE EURO FOR UNIDO Report by the Director-General Reports on the budgetary, operational and financial aspects of the adoption of a single-currency system of assessment based on the euro, in compliance with decision IDB.21/Dec.8. CONTENTS Paragraphs Page Introduction .................................................................. 1 - 3 2 Chapter I. THE EURO............................................................ 4 - 7 2 II. ACTION TAKEN BY UNIDO ............................................ 8 - 9 2 III. SPLIT-CURRENCY SYSTEM OF ASSESSMENT ............................ 10 - 15 3 IV. OTHER ORGANIZATIONS .............................................. 16 - 17 4 V. THE ISSUE............................................................ 18 - 39 4 A. Replace schillings with euros under the split-currency system ................. 19 - 22 4 B. Introduce a euro-based single-currency system ............................ 23 - 39 5 VI. CONCLUSION......................................................... 40 8 VII. ACTION REQUIRED OF THE BOARD .................................... 41 8 Annexes I. Summary of major budgetary, operational and financial implications ................................... 9 II. Other organizations........................................................................