Cayman Islands&Countryoverview=Overview&Countryc…

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Treasury Reporting Rates of Exchange As of December 31, 2018

TREASURY REPORTING RATES OF EXCHANGE AS OF DECEMBER 31, 2018 COUNTRY-CURRENCY F.C. TO $1.00 AFGHANISTAN - AFGHANI 74.5760 ALBANIA - LEK 107.0500 ALGERIA - DINAR 117.8980 ANGOLA - KWANZA 310.0000 ANTIGUA - BARBUDA - E. CARIBBEAN DOLLAR 2.7000 ARGENTINA-PESO 37.6420 ARMENIA - DRAM 485.0000 AUSTRALIA - DOLLAR 1.4160 AUSTRIA - EURO 0.8720 AZERBAIJAN - NEW MANAT 1.7000 BAHAMAS - DOLLAR 1.0000 BAHRAIN - DINAR 0.3770 BANGLADESH - TAKA 84.0000 BARBADOS - DOLLAR 2.0200 BELARUS - NEW RUBLE 2.1600 BELGIUM-EURO 0.8720 BELIZE - DOLLAR 2.0000 BENIN - CFA FRANC 568.6500 BERMUDA - DOLLAR 1.0000 BOLIVIA - BOLIVIANO 6.8500 BOSNIA- MARKA 1.7060 BOTSWANA - PULA 10.6610 BRAZIL - REAL 3.8800 BRUNEI - DOLLAR 1.3610 BULGARIA - LEV 1.7070 BURKINA FASO - CFA FRANC 568.6500 BURUNDI - FRANC 1790.0000 CAMBODIA (KHMER) - RIEL 4103.0000 CAMEROON - CFA FRANC 603.8700 CANADA - DOLLAR 1.3620 CAPE VERDE - ESCUDO 94.8800 CAYMAN ISLANDS - DOLLAR 0.8200 CENTRAL AFRICAN REPUBLIC - CFA FRANC 603.8700 CHAD - CFA FRANC 603.8700 CHILE - PESO 693.0800 CHINA - RENMINBI 6.8760 COLOMBIA - PESO 3245.0000 COMOROS - FRANC 428.1400 COSTA RICA - COLON 603.5000 COTE D'IVOIRE - CFA FRANC 568.6500 CROATIA - KUNA 6.3100 CUBA-PESO 1.0000 CYPRUS-EURO 0.8720 CZECH REPUBLIC - KORUNA 21.9410 DEMOCRATIC REPUBLIC OF CONGO- FRANC 1630.0000 DENMARK - KRONE 6.5170 DJIBOUTI - FRANC 177.0000 DOMINICAN REPUBLIC - PESO 49.9400 ECUADOR-DOLARES 1.0000 EGYPT - POUND 17.8900 EL SALVADOR-DOLARES 1.0000 EQUATORIAL GUINEA - CFA FRANC 603.8700 ERITREA - NAKFA 15.0000 ESTONIA-EURO 0.8720 ETHIOPIA - BIRR 28.0400 -

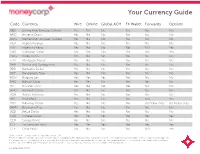

Your Currency Guide

Your Currency Guide Code Currency Wire Online Global ACH FX Wallet Forwards Options AED United Arab Emirates Dirham Yes Yes No Yes Yes No AMD Armenia Dram Yes No No No No No ANG Netherlands Antillean Guilder Yes No No No No No AOA Angola Kwanza Yes No No No No No ARS Argentina Peso Yes No No No NDF Yes AUD Australian Dollar Yes Yes Yes Yes Yes Yes AWG Aruba Florin Yes No No No No No AZN Azerbaijan Manat Yes No No No No No BAM Bosnia and Herzegovina Yes No No No No No BBD Barbados Dollar Yes No No Yes No No BDT Bangladesh Taka Yes No No No No No BGN Bulgaria Lev Yes Yes Yes Yes No No BHD Bahrain Dinar Yes Yes No Yes Yes No BIF Burundi Franc Yes No No No No No BMD Bermuda Dollar Yes No No No No No BOB Bolivia Boliviano Yes No No No No No BRL Brazil Real Yes No No No NDF Yes BSD Bahamas Dollar Yes No No No US Dollar only US Dollar only BWP Botswana Pula Yes No No Yes No No BZD Belize Dollar Yes No No No No No CAD Canada Dollar Yes Yes Yes Yes Yes Yes CDF Congo Franc Yes No No No No No CHF Switzerland Franc Yes Yes Yes Yes Yes Yes CLP Chile Peso Yes No No No NDF Yes *Some ciurrencies may require a copy of beneficiaries ID. This list is subject to change, and currencies are subject to availability. The ability you have to purchase currencies through moneycorp is subject to the completion and approval of a moneycorp account application and any other documentation deemed to be required by moneycorp. -

Standard Settlement Instructions for Foreign Exchange, Money Market and Commercial Payments

Standard Settlement Instructions For Foreign Exchange, Money Market and Commercial Payments CURRENCY CORRESPONDENT BANK S.W.I.F.T ADDRESS Australian Dollar Westpac Banking Corporation WPACAU2S AUD Sydney, Australia Barbados Dollar The Bank of Nova Scotia, Bridgetown NOCSBBBB BBD Barbados Bermudian Dollar The Bank of N. T. Butterfield & Son Ltd. BNTBBMHM BMD Hamilton, Bermuda Bahamian Dollar Scotiabank (Bahamas) Ltd. NOSCBSNS BSD Nassau, Bahamas Belize Dollar Scotiabank (Belize) Ltd., NOSCBZBS BZD Belize City, Belize Canadian Dollar The Bank of Nova Scotia NOSCCATT CAD International Banking Division, Toronto Cyprus Pound Bank of Cyprus Public Company Ltd., BCYPCY2N010 CYP Nicosia, Cyrpus Czech Koruna Ceskolovenska Obchodni Banka A.S. CEKOCZPP CZK Prague Danish Krone Nordea Bank Danmark A/S NDEADKKK DKK Copenhagen, Denmark Euro Deutsche Bank AG DEUTDEFF EUR Frankfurt Fiji Dollar Wetspac Banking Corporation WPACFJFX FJD Suva, Fiji Guyana Dollar The Bank of Nova Scotia, Georgetown, NOSCGYGE GYD Guyana Hong Kong Dollar The Bank of Nova Scotia NOSCHKHH HKD Hong Kong Hungarian Forint MKB Bank ZRT MKKB HU HB HUF Indian Rupee The Bank of Nova Scotia NOSCINBB INR Mumbai Indonesian Rupiah Standard Chartered Bank SCBLIDJX IDR Jakarta, Indonesia Israeli Sheqel Bank Hapaolim BM POALILIT ILS Tel Aviv Jamaican Dollar The Bank of Nova Scotia Jamaica Ltd. NOSCBSNSKIN JMD Kingston, Jamaica Japanese Yen The Bank of Tokyo-Mitsubishi UFJ, Ltd. BOTKJPJT JPY Tokyo Cayman Islands Dollar Scotiabank and Trust (Cayman) Ltd. NOSCKYKX KYD Cayman Islands Malaysian -

Country Scheme Alpha 3 Alpha 2 Currency Albania MC / VI ALB AL

Country Scheme Alpha 3 Alpha 2 Currency Albania MC / VI ALB AL Lek Algeria MC / VI DZA DZ Algerian dinar Argentina MC / VI ARG AR Argentine peso Australia MC / VI AUS AU Australian dollar -Christmas Is. -Cocos (Keeling) Is. -Heard and McDonald Is. -Kiribati -Nauru -Norfolk Is. -Tuvalu Christmas Island MC CXR CX Australian dollar Cocos (Keeling) Islands MC CCK CC Australian dollar Heard and McDonald Islands MC HMD HM Australian dollar Kiribati MC KIR KI Australian dollar Nauru MC NRU NR Australian dollar Norfolk Island MC NFK NF Australian dollar Tuvalu MC TUV TV Australian dollar Bahamas MC / VI BHS BS Bahamian dollar Bahrain MC / VI BHR BH Bahraini dinar Bangladesh MC / VI BGD BD Taka Armenia VI ARM AM Armenian Dram Barbados MC / VI BRB BB Barbados dollar Bermuda MC / VI BMU BM Bermudian dollar Bolivia, MC / VI BOL BO Boliviano Plurinational State of Botswana MC / VI BWA BW Pula Belize MC / VI BLZ BZ Belize dollar Solomon Islands MC / VI SLB SB Solomon Islands dollar Brunei Darussalam MC / VI BRN BN Brunei dollar Myanmar MC / VI MMR MM Myanmar kyat (effective 1 November 2012) Burundi MC / VI BDI BI Burundi franc Cambodia MC / VI KHM KH Riel Canada MC / VI CAN CA Canadian dollar Cape Verde MC / VI CPV CV Cape Verde escudo Cayman Islands MC / VI CYM KY Cayman Islands dollar Sri Lanka MC / VI LKA LK Sri Lanka rupee Chile MC / VI CHL CL Chilean peso China VI CHN CN Colombia MC / VI COL CO Colombian peso Comoros MC / VI COM KM Comoro franc Costa Rica MC / VI CRI CR Costa Rican colony Croatia MC / VI HRV HR Kuna Cuba VI Czech Republic MC / VI CZE CZ Koruna Denmark MC / VI DNK DK Danish krone Faeroe Is. -

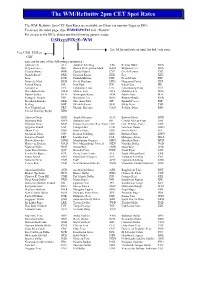

WM/Refinitiv Closing Spot Rates

The WM/Refinitiv Closing Spot Rates The WM/Refinitiv Closing Exchange Rates are available on Eikon via monitor pages or RICs. To access the index page, type WMRSPOT01 and <Return> For access to the RICs, please use the following generic codes :- USDxxxFIXz=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR, GBP or CHF xxx can be any of the following currencies :- Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy -

International Currency Codes

Country Capital Currency Name Code Afghanistan Kabul Afghanistan Afghani AFN Albania Tirana Albanian Lek ALL Algeria Algiers Algerian Dinar DZD American Samoa Pago Pago US Dollar USD Andorra Andorra Euro EUR Angola Luanda Angolan Kwanza AOA Anguilla The Valley East Caribbean Dollar XCD Antarctica None East Caribbean Dollar XCD Antigua and Barbuda St. Johns East Caribbean Dollar XCD Argentina Buenos Aires Argentine Peso ARS Armenia Yerevan Armenian Dram AMD Aruba Oranjestad Aruban Guilder AWG Australia Canberra Australian Dollar AUD Austria Vienna Euro EUR Azerbaijan Baku Azerbaijan New Manat AZN Bahamas Nassau Bahamian Dollar BSD Bahrain Al-Manamah Bahraini Dinar BHD Bangladesh Dhaka Bangladeshi Taka BDT Barbados Bridgetown Barbados Dollar BBD Belarus Minsk Belarussian Ruble BYR Belgium Brussels Euro EUR Belize Belmopan Belize Dollar BZD Benin Porto-Novo CFA Franc BCEAO XOF Bermuda Hamilton Bermudian Dollar BMD Bhutan Thimphu Bhutan Ngultrum BTN Bolivia La Paz Boliviano BOB Bosnia-Herzegovina Sarajevo Marka BAM Botswana Gaborone Botswana Pula BWP Bouvet Island None Norwegian Krone NOK Brazil Brasilia Brazilian Real BRL British Indian Ocean Territory None US Dollar USD Bandar Seri Brunei Darussalam Begawan Brunei Dollar BND Bulgaria Sofia Bulgarian Lev BGN Burkina Faso Ouagadougou CFA Franc BCEAO XOF Burundi Bujumbura Burundi Franc BIF Cambodia Phnom Penh Kampuchean Riel KHR Cameroon Yaounde CFA Franc BEAC XAF Canada Ottawa Canadian Dollar CAD Cape Verde Praia Cape Verde Escudo CVE Cayman Islands Georgetown Cayman Islands Dollar KYD _____________________________________________________________________________________________ -

Key Benefits of Cayman Islands Structures

Legal Guide Key Benefits of Cayman Islands Structures Companies incorporated in the Cayman Islands are amongst the most popular offshore holding structures in the world due to the political and economic stability of the Cayman Islands, the use of the English language and the US Dollar, and other unique advantages set out in this guide. Cayman vehicles are most commonly used in company or partnership-based fund arrangements, but holding company structures and Cayman trusts are also popular. Political and economic stability The Cayman Islands is a British overseas territory and has a history of stable government. The British government retains responsibility for internal security, defence and external affairs. Prudent economic policies and a strong financial services sector have resulted in the islands enjoying an AAA sovereign risk rating. The favourable economic situation of the Cayman Islands is reflected in its political stability. Absence of exchange controls There are no exchange control restrictions or regulations in the Cayman Islands. Funds can be freely transferred in and out of the Islands in unlimited amounts. The Cayman Islands dollar is tied to the US dollar and the latter is freely accepted and used within the local economy. Taxation In addition to the current tax-free status (companies are free from all Cayman Islands income, capital gains, corporation and withholding taxes), companies receive a tax exemption undertaking from the Cayman Islands government, confirming that such tax-free status will be maintained for a period of 20 years from incorporation, irrespective of any subsequent generally applicable law change, which period can be extended for a further period of ten years if the transaction requires it. -

WM/Refinitiv 2Pm CET Spot Rates

The WM/Refinitiv 2pm CET Spot Rates The WM/ Refinitiv 2pm CET Spot Rates are available on Eikon via monitor Pages or RICs. To access the index page, type WMRESPOT01 and <Return> For access to the RICs, please use the following generic codes : USDxxxFIXzE=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR or GBP xxx can be any of the following currencies : Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy Ariary -

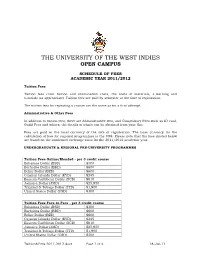

UWI Open Campus Accounts

THE UNIVERSITY OF THE WEST INDIES OPEN CAMPUS SCHEDULE OF FEES ACADEMIC YEAR 2011/2012 Tuition Fees Tuition fees cover tuition and examination costs, the costs of materials, e-learning and tutorials (as appropriate). Tuition fees are paid by semester at the time of registration. The tuition fees for repeating a course are the same as for a first attempt. Administrative & Other Fees In addition to tuition fees, there are Administrative fees, and Compulsory Fees such as ID card, Guild Fees and others; the details of which can be obtained from your Site. Fees are paid in the local currency of the Site of registration. The base currency for the calculation of fees for regional programmes is the US$. Please note that the fees quoted below are based on the confirmed exchange rates for the 2011/2012 academic year. UNDERGRADUATE & REGIONAL PRE-UNIVERSITY PROGRAMMES Tuition Fees Online/Blended - per 3 credit course Bahamas Dollar (BSD) $300 Barbados Dollar (BBD) $600 Belize Dollar (BZD) $600 Cayman Islands Dollar (KYD) $245 Eastern Caribbean Dollar (XCD) $810 Jamaica Dollar (JMD) $25,950 Trinidad & Tobago Dollar (TTD) $1,900 United States Dollar (USD) $300 Tuition Fees Face-to-Face - per 3 credit course Bahamas Dollar (BSD) $300 Barbados Dollar (BBD) $600 Belize Dollar (BZD) $600 Cayman Islands Dollar (KYD) $245 Eastern Caribbean Dollar (XCD) $810 Jamaica Dollar (JMD) $25,950 Trinidad & Tobago Dollar (TTD) $1,900 United States Dollar (USD) $300 Tuition&Fees 2011-2012.docx Page 1 of 4 18-Jul-11 BEd Literacy BEd Secondary Tuition Fees - per credit. -

CURRENCY BOARD FINANCIAL STATEMENTS Currency Board Working Paper

SAE./No.22/December 2014 Studies in Applied Economics CURRENCY BOARD FINANCIAL STATEMENTS Currency Board Working Paper Nicholas Krus and Kurt Schuler Johns Hopkins Institute for Applied Economics, Global Health, and Study of Business Enterprise & Center for Financial Stability Currency Board Financial Statements First version, December 2014 By Nicholas Krus and Kurt Schuler Paper and accompanying spreadsheets copyright 2014 by Nicholas Krus and Kurt Schuler. All rights reserved. Spreadsheets previously issued by other researchers are used by permission. About the series The Studies in Applied Economics of the Institute for Applied Economics, Global Health and the Study of Business Enterprise are under the general direction of Professor Steve H. Hanke, co-director of the Institute ([email protected]). This study is one in a series on currency boards for the Institute’s Currency Board Project. The series will fill gaps in the history, statistics, and scholarship of currency boards. This study is issued jointly with the Center for Financial Stability. The main summary data series will eventually be available in the Center’s Historical Financial Statistics data set. About the authors Nicholas Krus ([email protected]) is an Associate Analyst at Warner Music Group in New York. He has a bachelor’s degree in economics from The Johns Hopkins University in Baltimore, where he also worked as a research assistant at the Institute for Applied Economics and the Study of Business Enterprise and did most of his research for this paper. Kurt Schuler ([email protected]) is Senior Fellow in Financial History at the Center for Financial Stability in New York. -

FAO Country Name ISO Currency Code* Currency Name*

FAO Country Name ISO Currency Code* Currency Name* Afghanistan AFA Afghani Albania ALL Lek Algeria DZD Algerian Dinar Amer Samoa USD US Dollar Andorra ADP Andorran Peseta Angola AON New Kwanza Anguilla XCD East Caribbean Dollar Antigua Barb XCD East Caribbean Dollar Argentina ARS Argentine Peso Armenia AMD Armeniam Dram Aruba AWG Aruban Guilder Australia AUD Australian Dollar Austria ATS Schilling Azerbaijan AZM Azerbaijanian Manat Bahamas BSD Bahamian Dollar Bahrain BHD Bahraini Dinar Bangladesh BDT Taka Barbados BBD Barbados Dollar Belarus BYB Belarussian Ruble Belgium BEF Belgian Franc Belize BZD Belize Dollar Benin XOF CFA Franc Bermuda BMD Bermudian Dollar Bhutan BTN Ngultrum Bolivia BOB Boliviano Botswana BWP Pula Br Ind Oc Tr USD US Dollar Br Virgin Is USD US Dollar Brazil BRL Brazilian Real Brunei Darsm BND Brunei Dollar Bulgaria BGN New Lev Burkina Faso XOF CFA Franc Burundi BIF Burundi Franc Côte dIvoire XOF CFA Franc Cambodia KHR Riel Cameroon XAF CFA Franc Canada CAD Canadian Dollar Cape Verde CVE Cape Verde Escudo Cayman Is KYD Cayman Islands Dollar Cent Afr Rep XAF CFA Franc Chad XAF CFA Franc Channel Is GBP Pound Sterling Chile CLP Chilean Peso China CNY Yuan Renminbi China, Macao MOP Pataca China,H.Kong HKD Hong Kong Dollar China,Taiwan TWD New Taiwan Dollar Christmas Is AUD Australian Dollar Cocos Is AUD Australian Dollar Colombia COP Colombian Peso Comoros KMF Comoro Franc FAO Country Name ISO Currency Code* Currency Name* Congo Dem R CDF Franc Congolais Congo Rep XAF CFA Franc Cook Is NZD New Zealand Dollar Costa Rica -

List of Currencies of All Countries

The CSS Point List Of Currencies Of All Countries Country Currency ISO-4217 A Afghanistan Afghan afghani AFN Albania Albanian lek ALL Algeria Algerian dinar DZD Andorra European euro EUR Angola Angolan kwanza AOA Anguilla East Caribbean dollar XCD Antigua and Barbuda East Caribbean dollar XCD Argentina Argentine peso ARS Armenia Armenian dram AMD Aruba Aruban florin AWG Australia Australian dollar AUD Austria European euro EUR Azerbaijan Azerbaijani manat AZN B Bahamas Bahamian dollar BSD Bahrain Bahraini dinar BHD Bangladesh Bangladeshi taka BDT Barbados Barbadian dollar BBD Belarus Belarusian ruble BYR Belgium European euro EUR Belize Belize dollar BZD Benin West African CFA franc XOF Bhutan Bhutanese ngultrum BTN Bolivia Bolivian boliviano BOB Bosnia-Herzegovina Bosnia and Herzegovina konvertibilna marka BAM Botswana Botswana pula BWP 1 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Brazil Brazilian real BRL Brunei Brunei dollar BND Bulgaria Bulgarian lev BGN Burkina Faso West African CFA franc XOF Burundi Burundi franc BIF C Cambodia Cambodian riel KHR Cameroon Central African CFA franc XAF Canada Canadian dollar CAD Cape Verde Cape Verdean escudo CVE Cayman Islands Cayman Islands dollar KYD Central African Republic Central African CFA franc XAF Chad Central African CFA franc XAF Chile Chilean peso CLP China Chinese renminbi CNY Colombia Colombian peso COP Comoros Comorian franc KMF Congo Central African CFA franc XAF Congo, Democratic Republic Congolese franc CDF Costa Rica Costa Rican colon CRC Côte d'Ivoire West African CFA franc XOF Croatia Croatian kuna HRK Cuba Cuban peso CUC Cyprus European euro EUR Czech Republic Czech koruna CZK D Denmark Danish krone DKK Djibouti Djiboutian franc DJF Dominica East Caribbean dollar XCD 2 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Dominican Republic Dominican peso DOP E East Timor uses the U.S.