CURRENCY BOARD FINANCIAL STATEMENTS Currency Board Working Paper

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Maltese Lira

THE MALTESE LIRA On 16 May 1972, the Central Bank of Malta issued the first series of decimal coinage based on the Maltese Lira, at the time being roughly equivalent to the British Pound. Each Lira was divided in 100 cents (abbreviation of centesimo, meaning 1/100), while each cent was subdivided in 10 mills (abbreviation of millesimo, meaning 1/1000). The mills coins of the 1972 series - withdrawn from circulation in 1994 9 COINS AND 3 BANKNOTES Initially, a total of 8 coins were issued, namely the 50 cent, 10 cent, 5 cent, 2 cent, 1 cent, 5 mill, 3 mill and 2 mill. These coins were complemented by the issue of three banknotes, namely the 1 Lira, 5 Lira and 10 Lira, on 15 January 1973. Furthermore, a 25 cent coin was introduced in June 1975 to commemorate Malta becoming a Republic within the Commonwealth of Nation on 13 December 1974. This was the first coin to feature the coat of arms of the Republic of Malta on the reverse. NEW SERIES The obverse of the 1986/1991 series - withdrawn from circulation in January 2008 A new series was issued on 19 May 1986. This comprised 7 coins, namely the 1 Lira, 50 cent, 25 cent, 10 cent, 5 cent, 2 cent and 1 cent. Each coin depicted local fauna and flora on the The banknotes of the 1989 series - withdrawn from circulation in January 2008 obverse and the emblem of the Republic on the reverse. No mills were struck as part of this series, though the 5 mil, 3 mil and 2 mil coins issued in 1972 continued to have legal tender. -

Guide to the Collection of Irish Antiquities

NATIONAL MUSEUM OF SCIENCE AND ART, DUBLIN. GUIDE TO THE COLLECTION OF IRISH ANTIQUITIES. (ROYAL IRISH ACADEMY COLLECTION). ANGLO IRISH COINS. BY G COFFEY, B.A.X., M.R.I.A. " dtm; i, in : printed for his majesty's stationery office By CAHILL & CO., LTD., 40 Lower Ormond Quay. 1911 Price One Shilling. cj 35X5*. I CATALOGUE OF \ IRISH COINS In the Collection of the Royal Irish Academy. (National Museum, Dublin.) PART II. ANGLO-IRISH. JOHN DE CURCY.—Farthings struck by John De Curcy (Earl of Ulster, 1181) at Downpatrick and Carrickfergus. (See Dr. A. Smith's paper in the Numismatic Chronicle, N.S., Vol. III., p. 149). £ OBVERSE. REVERSE. 17. Staff between JiCRAGF, with mark of R and I. abbreviation. In inner circle a double cross pommee, with pellet in centre. Smith No. 10. 18. (Duplicate). Do. 19. Smith No. 11. 20. Smith No. 12. 21. (Duplicate). Type with name Goan D'Qurci on reverse. Obverse—PATRIC or PATRICII, a small cross before and at end of word. In inner circle a cross without staff. Reverse—GOAN D QVRCI. In inner circle a short double cross. (Legend collected from several coins). 1. ^PIT .... GOANDQU . (Irish or Saxon T.) Smith No. 13. 2. ^PATRIC . „ J<. ANDQURCI. Smith No. 14. 3. ^PATRIGV^ QURCI. Smith No. 15. 4. ^PA . IOJ< ^GOA . URCI. Smith No. 16. 5. Duplicate (?) of S. No. 6. ,, (broken). 7. Similar in type of ob- Legend unintelligible. In single verse. Legend unin- inner circle a cross ; telligible. resembles the type of the mascle farthings of John. Weight 2.7 grains ; probably a forgery of the time. -

Treasury Reporting Rates of Exchange As of December 31, 2018

TREASURY REPORTING RATES OF EXCHANGE AS OF DECEMBER 31, 2018 COUNTRY-CURRENCY F.C. TO $1.00 AFGHANISTAN - AFGHANI 74.5760 ALBANIA - LEK 107.0500 ALGERIA - DINAR 117.8980 ANGOLA - KWANZA 310.0000 ANTIGUA - BARBUDA - E. CARIBBEAN DOLLAR 2.7000 ARGENTINA-PESO 37.6420 ARMENIA - DRAM 485.0000 AUSTRALIA - DOLLAR 1.4160 AUSTRIA - EURO 0.8720 AZERBAIJAN - NEW MANAT 1.7000 BAHAMAS - DOLLAR 1.0000 BAHRAIN - DINAR 0.3770 BANGLADESH - TAKA 84.0000 BARBADOS - DOLLAR 2.0200 BELARUS - NEW RUBLE 2.1600 BELGIUM-EURO 0.8720 BELIZE - DOLLAR 2.0000 BENIN - CFA FRANC 568.6500 BERMUDA - DOLLAR 1.0000 BOLIVIA - BOLIVIANO 6.8500 BOSNIA- MARKA 1.7060 BOTSWANA - PULA 10.6610 BRAZIL - REAL 3.8800 BRUNEI - DOLLAR 1.3610 BULGARIA - LEV 1.7070 BURKINA FASO - CFA FRANC 568.6500 BURUNDI - FRANC 1790.0000 CAMBODIA (KHMER) - RIEL 4103.0000 CAMEROON - CFA FRANC 603.8700 CANADA - DOLLAR 1.3620 CAPE VERDE - ESCUDO 94.8800 CAYMAN ISLANDS - DOLLAR 0.8200 CENTRAL AFRICAN REPUBLIC - CFA FRANC 603.8700 CHAD - CFA FRANC 603.8700 CHILE - PESO 693.0800 CHINA - RENMINBI 6.8760 COLOMBIA - PESO 3245.0000 COMOROS - FRANC 428.1400 COSTA RICA - COLON 603.5000 COTE D'IVOIRE - CFA FRANC 568.6500 CROATIA - KUNA 6.3100 CUBA-PESO 1.0000 CYPRUS-EURO 0.8720 CZECH REPUBLIC - KORUNA 21.9410 DEMOCRATIC REPUBLIC OF CONGO- FRANC 1630.0000 DENMARK - KRONE 6.5170 DJIBOUTI - FRANC 177.0000 DOMINICAN REPUBLIC - PESO 49.9400 ECUADOR-DOLARES 1.0000 EGYPT - POUND 17.8900 EL SALVADOR-DOLARES 1.0000 EQUATORIAL GUINEA - CFA FRANC 603.8700 ERITREA - NAKFA 15.0000 ESTONIA-EURO 0.8720 ETHIOPIA - BIRR 28.0400 -

This PDF Is a Selection from an Out-Of-Print Volume from the National Bureau of Economic Research

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: The International Gold Standard Reinterpreted, 1914-1934 Volume Author/Editor: William Adams Brown, Jr. Volume Publisher: NBER Volume ISBN: 0-87014-036-1 Volume URL: http://www.nber.org/books/brow40-1 Publication Date: 1940 Chapter Title: Book III, Part V: The Impact of the World Economic Depression on the International Gold Standard, 1929-1931 Chapter Author: William Adams Brown, Jr. Chapter URL: http://www.nber.org/chapters/c5947 Chapter pages in book: (p. 808 - 1047) PART V The Impact of the World Economic Depression on the International Gold Standard, 1929-1931 S CHAPTER 22 The International Distribution of Credit under the Impact of World-wide Deflationary Forces For about twelve months after the critical decisions of June 1927 the international effects of generally easy money were among the most fundamental causes of a world-wide upswing in business.1 Though prices in gold standard countries were falling gradually, increasing productivity would probably have forced them much lower had it not been for the ex- pansion of credit. There was an upward pressure in many price groups. Profits from security and real estate speculation stimulated demand for many commodities. Low interest rates made it easy to finance valorization schemes and price arrangements and promoted the issue of foreign loans, par.. ticularly in the United States. Foreign loans in turn helped to maintain prices in many debtor countries and also pre- vented the growth of tariffs from checking the expansion of international trade.2 The continued extension of interna- tional credit was a dam that was holding back the onrushing torrent of economic readjustment. -

Older April 2021

OLDER! APRIL 2021 AFGHANISTAN 1/2 Afghani SH1306 Yr.9 Original VF – 7.00~ Afghani SH1304 Yr. 7 VF – 14.00~ ALBANIA 1/2 Lek 1926-R ChVF – 5.00 ALGERIA Token 10 Centimes 1916 without J. Bory KM-Tn5 ChVF – 6.00 Token 10 Centimes 1918 with J. Bory KM-TnA5 Aluminum EF – 8.00~ Token 10 Centimes 1919 with J. Bory KM-TnA5 Aluminum ChVF+ - 4.00~ ARGENTINA CentaVo 1890 VF – 3.00 AUSTRALIA Half Penny 1913 ChVF – 10.00 Half Penny 1914 ChVF(2) – 7.00 Half Penny 1916-I ChEF – 8.50 Half Penny 1918-I VF+ - 13.00 Half Penny 1924 EF – 22.00 Half Penny 1930 EF – 29.00 Half Penny 1930 ChVF+(3) – 15.00 Half Penny 1933 AU - 13.00 Half Penny 1933 VF – 0.75 Half Penny 1939 “Kangaroo” EF(2) – 22.00 Half Penny 1939 “Kangaroo” ChVF – 13.00 Half Penny 1940(m) ChVF+ - 1.00 Half Penny 1942-P ChEF – 1.00 Penny 1911 ChEF, lustre, some pVc – 34.00 Penny 1912-H Dark ChVF, some dirt in deVices – 5.00 Penny 1912-H EF, 2 tiny rim nicks reV. – 13.00 Penny 1912-H ChVF – 8.50 Penny 1913 EF – 28.00 Penny 1915(L) VF –24.00 Penny 1915(L) Fine – 7.00 Penny 1916-I EF – 15.00 Penny 1918-I VF – 10.00 Penny 1919 Dot Below EF – 17.00 Penny 1919 Dot Below VF – 2.00 Penny 1919 Dot Below Fine(2) – 1.25 Penny 1921 VF, retoning – 3.00 Penny 1922 EF – 17.00 Penny 1922 ChVF(2) – 2.75 Penny 1923 EF – 17.00 Penny 1923 EF, cleaned with soap – 10.00 Penny 1924 Cleaned EF - 7.00 Penny 1927 VF+ - 1.75 Penny 1933 EF – 6.50 Penny 1934 EF – 6.50 Penny 1935 EF – 6.50 Penny 1941(m), KG with no dot ChEF – 6.50 Threepence 1910 AU – 28.00 Threepence 1910 EF(2) – 10.00 Threepence 1911 Original ChVF+ - 42.00 -

People's Democratic Republic of Algeria

People’s Democratic Republic of Algeria Ministry of Higher Education and Scientific Research Higher School of Management Sciences Annaba A Course of Business English for 1st year Preparatory Class Students Elaborated by: Dr GUERID Fethi The author has taught this module for 4 years from the academic year 2014/2015 to 2018/2019 Academic Year 2020/2021 1 Table of Contents Table of Contents...………………………………………………………….….I Acknowelegments……………………………………………………………....II Aim of the Course……………………………………………………………..III Lesson 1: English Tenses………………………………………………………..5 Lesson 2: Organizations………………………………………………………..13 Lesson 3: Production…………………………………………………………...18 Lesson 4: Distribution channels: Wholesale and Retail………………………..22 Lesson 5: Marketing …………………………………………………………...25 Lesson 6: Advertising …………………………………………………………28 Lesson 7: Conditional Sentences………………………………………………32 Lesson 8: Accounting1…………………………………………………………35 Lesson 9: Money and Work……………………………………………………39 Lesson 10: Types of Business Ownership……………………………………..43 Lesson 11: Passive voice……………………………………………………….46 Lesson 12: Management……………………………………………………….50 SUPPORTS: 1- Grammatical support: List of Irregular Verbs of English………..54 2- List of Currencies of the World………………………………….66 3- Business English Terminology in English and French………….75 References and Further Reading…………………………………………….89 I 2 Acknowledgments I am grateful to my teaching colleagues who preceded me in teaching this business English module at our school. This contribution is an addition to their efforts. I am thankful to Mrs Benghomrani Naziha, who has contributed before in designing English programmes to different levels, years and classes at Annaba Higher School of Management Sciences. I am also grateful to the administrative staff for their support. II 3 Aim of the Course The course aims is to equip 1st year students with the needed skills in business English to help them succeed in their study of economics and business and master English to be used at work when they finish the study. -

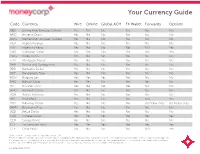

Your Currency Guide

Your Currency Guide Code Currency Wire Online Global ACH FX Wallet Forwards Options AED United Arab Emirates Dirham Yes Yes No Yes Yes No AMD Armenia Dram Yes No No No No No ANG Netherlands Antillean Guilder Yes No No No No No AOA Angola Kwanza Yes No No No No No ARS Argentina Peso Yes No No No NDF Yes AUD Australian Dollar Yes Yes Yes Yes Yes Yes AWG Aruba Florin Yes No No No No No AZN Azerbaijan Manat Yes No No No No No BAM Bosnia and Herzegovina Yes No No No No No BBD Barbados Dollar Yes No No Yes No No BDT Bangladesh Taka Yes No No No No No BGN Bulgaria Lev Yes Yes Yes Yes No No BHD Bahrain Dinar Yes Yes No Yes Yes No BIF Burundi Franc Yes No No No No No BMD Bermuda Dollar Yes No No No No No BOB Bolivia Boliviano Yes No No No No No BRL Brazil Real Yes No No No NDF Yes BSD Bahamas Dollar Yes No No No US Dollar only US Dollar only BWP Botswana Pula Yes No No Yes No No BZD Belize Dollar Yes No No No No No CAD Canada Dollar Yes Yes Yes Yes Yes Yes CDF Congo Franc Yes No No No No No CHF Switzerland Franc Yes Yes Yes Yes Yes Yes CLP Chile Peso Yes No No No NDF Yes *Some ciurrencies may require a copy of beneficiaries ID. This list is subject to change, and currencies are subject to availability. The ability you have to purchase currencies through moneycorp is subject to the completion and approval of a moneycorp account application and any other documentation deemed to be required by moneycorp. -

Christopher Kent: the Resources Boom and the Australian Dollar

Christopher Kent: The resources boom and the Australian dollar Address by Mr Christopher Kent, Assistant Governor (Economic) of the Reserve Bank of Australia, to the Committee for Economic Development of Australia (CEDA) Economic and Political Overview, Sydney, 14 February 2014. * * * I thank Jonathan Hambur, Daniel Rees and Michelle Wright for assistance in preparing these remarks. I would like to thank CEDA for the invitation to speak here today. I thought I would take the opportunity to talk to you about the implications of the resources boom for the Australian dollar. The past decade saw the Australian dollar appreciate by around 50 per cent in trade- weighted terms (Graph 1).1 The appreciation was an important means by which the economy was able to adjust to the historic increase in commodity prices and the unprecedented investment boom in the resources sector.2 Even though there was a significant increase in incomes and domestic demand over a number of years, average inflation over the past decade has remained within the target. Also, growth has generally not been too far from trend. This is all the more significant in light of the substantial swings in the macroeconomy that were all too common during earlier commodity booms.3 The high nominal exchange rate helped to facilitate the reallocation of labour and capital across industries. While this has made conditions difficult in some industries, the appreciation, in combination with a relatively flexible labour market and low and stable inflation expectations, meant that high demand for labour in the resources sector did not spill over to a broad-based increase in wage inflation.4 So the high level of the exchange rate was helpful for the economy as a whole. -

Malton Antique Sale

Boulton & Cooper MALTON ANTIQUE SALE WEDNESDAY 22ND OCTOBER AT 10.00am At The Milton Rooms, Market Place, Malton, North Yorkshire. YO17 7LX VIEWING: Tuesday 21st October 10.00am – 7.00pm & on morning of sale from 9.00am REQUESTS FOR FURTHER INFORMATION OR IMAGES SHOULD BE RECEIVED BY US NO LATER THAN 1PM THE DAY BEFORE THE SALE China 1 – 48 Glassware 49 – 65 Metalware 66 – 80 Books 81 – 99 Platedware & Silver 100 - 128 Jewellery 129 – 206 Coins, Banknotes & Token 207 – 372 Stamps 373 – 403 Collector’s Items 404 – 492 Pictures & Prints 493 – 521 Clocks & Barometers 522 – 526 Carpets & Rugs 527 – 533 Furniture 534 – 590 CHINA 1. A Royal Doulton Character Jug 'Winston Churchill', 9" (23cms) high and a Doulton tobacco set comprising cigarette box (cover missing) and five small oblong dishes decorated with hounds and foxes (one chipped). £40-60 2. A Cantonese Plate decorated with panels of figures and flowers, 10" (26cms) diameter, an Imari pattern plate, two ginger jars and three other Oriental plates. £30-40 3. Six Royal Crown Derby Coffee Cans and Saucers (one cup a/f), 19th Century Masons Ironstone plate, two other plates and a small Dresden oval box and cover. £30-40 4. A Paragon Cup, Saucer and Plate commemorating the Coronation of Edward VIII and a similar George VI coronation cup. £10-20 5. A Royal Doulton Character Jug 'Gondolier' DH6589, large size. £50-70 6. A set of twelve Royal Worcester 'Months of the Year' figures of children, modelled by F C Doughty. (June & November damaged). £400-500 7. An English Delft oval Meat Plate decorated with Oriental landscapes in blue and white. -

View Currency List

Currency List business.westernunion.com.au CURRENCY TT OUTGOING DRAFT OUTGOING FOREIGN CHEQUE INCOMING TT INCOMING CURRENCY TT OUTGOING DRAFT OUTGOING FOREIGN CHEQUE INCOMING TT INCOMING CURRENCY TT OUTGOING DRAFT OUTGOING FOREIGN CHEQUE INCOMING TT INCOMING Africa Asia continued Middle East Algerian Dinar – DZD Laos Kip – LAK Bahrain Dinar – BHD Angola Kwanza – AOA Macau Pataca – MOP Israeli Shekel – ILS Botswana Pula – BWP Malaysian Ringgit – MYR Jordanian Dinar – JOD Burundi Franc – BIF Maldives Rufiyaa – MVR Kuwaiti Dinar – KWD Cape Verde Escudo – CVE Nepal Rupee – NPR Lebanese Pound – LBP Central African States – XOF Pakistan Rupee – PKR Omani Rial – OMR Central African States – XAF Philippine Peso – PHP Qatari Rial – QAR Comoros Franc – KMF Singapore Dollar – SGD Saudi Arabian Riyal – SAR Djibouti Franc – DJF Sri Lanka Rupee – LKR Turkish Lira – TRY Egyptian Pound – EGP Taiwanese Dollar – TWD UAE Dirham – AED Eritrea Nakfa – ERN Thai Baht – THB Yemeni Rial – YER Ethiopia Birr – ETB Uzbekistan Sum – UZS North America Gambian Dalasi – GMD Vietnamese Dong – VND Canadian Dollar – CAD Ghanian Cedi – GHS Oceania Mexican Peso – MXN Guinea Republic Franc – GNF Australian Dollar – AUD United States Dollar – USD Kenyan Shilling – KES Fiji Dollar – FJD South and Central America, The Caribbean Lesotho Malati – LSL New Zealand Dollar – NZD Argentine Peso – ARS Madagascar Ariary – MGA Papua New Guinea Kina – PGK Bahamian Dollar – BSD Malawi Kwacha – MWK Samoan Tala – WST Barbados Dollar – BBD Mauritanian Ouguiya – MRO Solomon Islands Dollar – -

Regional Integration Experience

K6114.46.61_East Africa article 11.2.2004 11:27 Page 46 Regional Integration Experience in East Africa BY N JUGUNA S. NDUNG’ U Kenya, Tanzania and Uganda have experienced half a century of regional integration REGIONAL INTEGRATION EXPERIENCE IN EAST AFRICA REGIONAL INTEGRATION efforts, going back to colonial times. Since 1991, they have been building an East African Community that starts with a customs union but covers many other domains — economic, environmental, social and political. Where this cooperation is headed, and recommendations for how it can get there, are discussed by Njuguna S. Ndung’u of the African Economic Research Consortium in Nairobi. REGIONALISM HAS GAINED momentum the 1990s. It is hoped that this will support in sub-Saharan Africa. Regional group- industrialization and generate benefits of ings provide opportunities for addressing regional economic integration. common challenges — improving eco- Tracing the history of the EAC since nomic policy, increasing market size and the colonial period helps to identify the competitiveness, attracting foreign direct problems and constraints that led to investment and pooling resources for its break-up in 1977. A survey of recent investments of mutual benefit (Kasek- attempts to revive EAC over the last ende and Ng’eno, 2000; Mullei, 2002). decade helps explain why regional inte- By combining fragmented domestic mar- gration is again being considered a feasi- kets, regional cooperation may spur eco- ble and viable development strategy and nomic growth and development by pro- -

Exchange Rate Statistics

Exchange rate statistics Updated issue Statistical Series Deutsche Bundesbank Exchange rate statistics 2 This Statistical Series is released once a month and pub- Deutsche Bundesbank lished on the basis of Section 18 of the Bundesbank Act Wilhelm-Epstein-Straße 14 (Gesetz über die Deutsche Bundesbank). 60431 Frankfurt am Main Germany To be informed when new issues of this Statistical Series are published, subscribe to the newsletter at: Postfach 10 06 02 www.bundesbank.de/statistik-newsletter_en 60006 Frankfurt am Main Germany Compared with the regular issue, which you may subscribe to as a newsletter, this issue contains data, which have Tel.: +49 (0)69 9566 3512 been updated in the meantime. Email: www.bundesbank.de/contact Up-to-date information and time series are also available Information pursuant to Section 5 of the German Tele- online at: media Act (Telemediengesetz) can be found at: www.bundesbank.de/content/821976 www.bundesbank.de/imprint www.bundesbank.de/timeseries Reproduction permitted only if source is stated. Further statistics compiled by the Deutsche Bundesbank can also be accessed at the Bundesbank web pages. ISSN 2699–9188 A publication schedule for selected statistics can be viewed Please consult the relevant table for the date of the last on the following page: update. www.bundesbank.de/statisticalcalender Deutsche Bundesbank Exchange rate statistics 3 Contents I. Euro area and exchange rate stability convergence criterion 1. Euro area countries and irrevoc able euro conversion rates in the third stage of Economic and Monetary Union .................................................................. 7 2. Central rates and intervention rates in Exchange Rate Mechanism II ............................... 7 II.