Blorebr Sept 2015 NL Cover

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

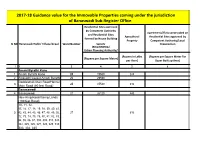

2017-18 Guidance Value for the Immovable Properties Coming Under the Jurisdiction of Banaswadi Sub-Register Office

2017-18 Guidance value for the Immovable Properties coming under the jurisdiction of Banaswadi Sub-Register Office. Residential Sites approved by Competent Authority Apartments/Flats constructed on and Residential Sites Agricultural Residential Sites approved by formed by House Building Property Competent Authority/Local Sl NO Banaswadi Hobli/ Village/Area/ Ward Number Society Organization (BDA/BMRDA/ Urban Planning Authority/ (Rupees in Lakhs (Rupees per Square Meter For (Rupees per Square Meter) per Acre) Super Built up Area) 1 2 3 4 5 6 Amani Byrathi Kane 1 Amani Byrathi Kane 25 19580 245 2 Arkavathi Layout Amani Byrathi 25 29590 Geddalahalli Main Road/Hennur 3 25 45540 610 Main Road (80 feet Road) Banasawadi 4 Banasawadi 27 26100 490 New Ring Road facing Lands (100 feet Road) 10, 11, 12, 15, 16, 17, 18, 19, 38, 39, 40, 41, 5 42, 43, 44, 45, 46, 47, 48, 49, 50, 27 610 72, 73, 74, 75, 76, 80, 81, 82, 83, 84, 85, 86, 87, 308, 309, 310, 323, 324, 325, 326, 327, 328, 329, 332, 333, 334, 335 Banasawadi - 6 Ramamurthy NagaraMain Road 27 46000 (80 feet Road) 7 Ex-Servicemen Colony 27 32560 8 Chandramma Layout 27 32540 9 Kalyanamma Layout 27 32560 10 Lakshmamma Layout 27 32560 11 Green Park Layout 27 32560 12 Vijaya Bank Colony 27 32560 13 Annaiah Reddy Layout 27 32560 14 Skyline Apartments (Apartments) 27 75900 Canapoy Apartments 15 27 37070 (Apartments) 16 Ex- Servicemen Colony/Layout 27 32600 17 Gopala Reddy Layout 27 32600 18 Krishna Reddy Layout 27 32560 19 100 feet Road/10 th Main Road 27 65120 Sai Charita Green Oaks 20 27 55000 (Apartments) -

Bangalore for the Visitor

Bangalore For the Visitor PDF generated using the open source mwlib toolkit. See http://code.pediapress.com/ for more information. PDF generated at: Mon, 12 Dec 2011 08:58:04 UTC Contents Articles The City 11 BBaannggaalloorree 11 HHiissttoorryoofBB aann ggaalloorree 1188 KKaarrnnaattaakkaa 2233 KKaarrnnaattaakkaGGoovv eerrnnmmeenntt 4466 Geography 5151 LLaakkeesiinBB aanngg aalloorree 5511 HHeebbbbaalllaakkee 6611 SSaannkkeeyttaannkk 6644 MMaaddiiwwaallaLLaakkee 6677 Key Landmarks 6868 BBaannggaalloorreCCaann ttoonnmmeenntt 6688 BBaannggaalloorreFFoorrtt 7700 CCuubbbboonPPaarrkk 7711 LLaalBBaagghh 7777 Transportation 8282 BBaannggaalloorreMM eettrrooppoolliittaanTT rraannssppoorrtCC oorrppoorraattiioonn 8822 BBeennggaalluurruIInn tteerrnnaattiioonnaalAA iirrppoorrtt 8866 Culture 9595 Economy 9696 Notable people 9797 LLiisstoof ppee oopplleffrroo mBBaa nnggaalloorree 9977 Bangalore Brands 101 KKiinnggffiisshheerAAiirrll iinneess 110011 References AArrttiicclleSSoo uurrcceesaann dCC oonnttrriibbuuttoorrss 111155 IImmaaggeSS oouurrcceess,LL iicceennsseesaa nndCC oonnttrriibbuuttoorrss 111188 Article Licenses LLiicceennssee 112211 11 The City Bangalore Bengaluru (ಬೆಂಗಳೂರು)) Bangalore — — metropolitan city — — Clockwise from top: UB City, Infosys, Glass house at Lal Bagh, Vidhana Soudha, Shiva statue, Bagmane Tech Park Bengaluru (ಬೆಂಗಳೂರು)) Location of Bengaluru (ಬೆಂಗಳೂರು)) in Karnataka and India Coordinates 12°58′′00″″N 77°34′′00″″EE Country India Region Bayaluseeme Bangalore 22 State Karnataka District(s) Bangalore Urban [1][1] Mayor Sharadamma [2][2] Commissioner Shankarlinge Gowda [3][3] Population 8425970 (3rd) (2011) •• Density •• 11371 /km22 (29451 /sq mi) [4][4] •• Metro •• 8499399 (5th) (2011) Time zone IST (UTC+05:30) [5][5] Area 741.0 square kilometres (286.1 sq mi) •• Elevation •• 920 metres (3020 ft) [6][6] Website Bengaluru ? Bangalore English pronunciation: / / ˈˈbæŋɡəɡəllɔəɔər, bæŋɡəˈllɔəɔər/, also called Bengaluru (Kannada: ಬೆಂಗಳೂರು,, Bengaḷūru [[ˈˈbeŋɡəɭ uuːːru]ru] (( listen)) is the capital of the Indian state of Karnataka. -

Bengaluru Metro Rail Project Phase 2B (Airport Metro Line) KR Puram to Kempegowda International Airport

Environmental Impact Assessment (Draft) Vol. 4 of 6 June 2020 India: Bengaluru Metro Rail Project Phase 2B (Airport Metro Line) KR Puram to Kempegowda International Airport Prepared by Bangalore Metro Rail Corporation Ltd. (BMRCL), India for the Asian Development Bank. NOTES (i) The fiscal year (FY) of the Government of India and its agencies ends on 31 March. “FY” before a calendar year denotes the year in which the fiscal year ends, e.g., FY2019 ends on 31 March 2019. (ii) In this report, "$" refers to United States dollars. This environmental impact assessment is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. Your attention is directed to the “terms of use” section on ADB’s website. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. Environmental Impact Assessment - KR Puram to KIA Section of BMRCL Table 4- 15: Results of Ground Water Analysis Std. IS Sl. 10500:2012 Parameters Unit GW3 GW4 No. (Second Revision AL PL 1. pH 6.5-8.5 - 7.32 7.62 2. Colour 5 15 Hazen <1 <1 3. Odour Agreeable -- Agreeable Agreeable 4. Turbidity 1 5 NTU 0.12 0.34 5. Electrical Conductivity Not specified 980 1797 6. Total Dissolved Solids 500 2000 mg/L 668 1217 7. -

![Bangalore (Or ???????? Bengaluru, ['Be?G??U??U] ( Listen)) Is the Capital City O F the Indian State of Karnataka](https://docslib.b-cdn.net/cover/7497/bangalore-or-bengaluru-be-g-u-u-listen-is-the-capital-city-o-f-the-indian-state-of-karnataka-1767497.webp)

Bangalore (Or ???????? Bengaluru, ['Be?G??U??U] ( Listen)) Is the Capital City O F the Indian State of Karnataka

Bangalore (or ???????? Bengaluru, ['be?g??u??u] ( listen)) is the capital city o f the Indian state of Karnataka. Located on the Deccan Plateau in the south-east ern part of Karnataka. Bangalore is India's third most populous city and fifth-m ost populous urban agglomeration. Bangalore is known as the Silicon Valley of In dia because of its position as nation's leading Information technology (IT) expo rter.[7][8][9] Located at a height of over 3,000 feet (914.4 m) above sea level, Bangalore is known for its pleasant climate throughout the year.[10] The city i s amongst the top ten preferred entrepreneurial locations in the world.[11] A succession of South Indian dynasties, the Western Gangas, the Cholas, and the Hoysalas ruled the present region of Bangalore until in 1537 CE, Kempé Gowda a feu datory ruler under the Vijayanagara Empire established a mud fort considered to be the foundation of modern Bangalore. Following transitory occupation by the Ma rathas and Mughals, the city remained under the Mysore Kingdom. It later passed into the hands of Hyder Ali and his son Tipu Sultan, and was captured by the Bri tish after victory in the Fourth Anglo-Mysore War (1799), who returned administr ative control of the city to the Maharaja of Mysore. The old city developed in t he dominions of the Maharaja of Mysore, and was made capital of the Princely Sta te of Mysore, which existed as a nominally sovereign entity of the British Raj. In 1809, the British shifted their cantonment to Bangalore, outside the old city , and a town grew up around it, which was governed as part of British India. -

Battles for Bangalore: Reterritorialising the City Janaki Nair Centre for the Study of Culture and Society Bangalore, India

Battles for Bangalore: Reterritorialising the City Janaki Nair Centre for the Study of Culture and Society Bangalore, India A divided city, cleaved by a swathe of parkland and administrative buildings that runs from north west to south east, was united in the single Bangalore City Corporation in 1949.1 No longer did the Bangalore Civil and Military station (referred to as the Cantonment, and the location since 1809 of British troops and their followers), have a separate administration from the old city area. And not just a geographical unity was forged, since the maps of linguistic, cultural and political traditions were redrawn. A previous move to unite the Cantonment, then under the control of the British Resident, with the rest of Princely Mysore was resisted by several cultural and economic groups that had long resided in the Station and enjoyed the perquisites of serving the colonial masters.2 A flurry of petitions protested the proposed "retrocession" of 1935 which would bring the Bangalore Cantonment under the Mysore administration; only the war delayed this move until July 1947.3 By 1949, such petitions were no deterrent to the plans of the new masters. But in the five decades since the formation of the Bangalore corporation, the city's east-west zonation continues to persist, and the uncomfortable question of "independence"4, or at least administrative freedom of the erstwhile cantonment has often been reiterated5. Most frequently, this has been in response to emerging cultural and political movements that seek to reterritorialise the city, refashioning its symbols, monuments or open spaces to evoke other memories, or histories that reflect the triumphs of the nation state, the hopes and aspirations of linguistic nationalisms or of social groups who have long lacked either economic or symbolic capital in the burgeoning city of Bangalore. -

(Lakes) in Urban Areas- a Case Study on Bellandur Lake of Bangalore Metropolitan City

IOSR Journal of Mechanical and Civil Engineering (IOSR-JMCE) e-ISSN: 2278-1684,p-ISSN: 2320-334X, Volume 7, Issue 3 (Jul. - Aug. 2013), PP 06-14 www.iosrjournals.org Scenario of Water Bodies (Lakes) In Urban Areas- A case study on Bellandur Lake of Bangalore Metropolitan city Ramesh. N 1, Krishnaiah. S2 1(Department of Civil Engineering, Government Engineering College, K.R.Pet-571 426, Karnataka) 2(Department of Civil Engineering, JNTUA College of Engineering, Anantapur -515 002, Andra pradesh) Abstract: Environment is made up of natural factors like air, water and land. Each and every human activities supports directly/indirectly by natural factors. India is facing a problem of natural resource scarcity, especially of water in view of population growth and economic development. Due to growth of Population, advancement in agriculture, urbanization and industrialization has made surface water pollution a great problem and decreased the availability of drinking water. Many parts of the world face such a scarcity of water. Lakes are important feature of the Earth’s landscape which are not only the source of precious water, but provide valuable habitats to plants and animals, moderate hydrological cycles, influence microclimate, enhance the aesthetic beauty of the landscape and extend many recreational opportunities to humankind .For issues, perspectives on pollution, restoration and management of Bellandur Lake Falls under Bangalore Metropolitan city is very essential to know their status but so far, there was no systematic environmental study carried out. Hence now the following studies are essential namely Characteristics, Status, Effects (on surrounding Groundwater, Soil, Humans health, Vegetables, Animals etc.,), resolving the issues of degradation, preparation of conceptual design for restoration and management. -

Large-Scale Urban Development in India - Past and Present

Large-Scale Urban Development in India - Past and Present Sagar S. Gandhi Working Paper #35 November 2007 | Collaboratory for Research on Global Projects The Collaboratory for Research on Global Projects at Stanford University is a multidisciplinary cen- ter that supports research, education and industry outreach to improve the sustainability of large in- frastructure investment projects that involve participants from multiple institutional backgrounds. Its studies have examined public-private partnerships, infrastructure investment funds, stakeholder mapping and engagement strategies, comparative forms of project governance, and social, political, and institutional risk management. The Collaboratory, established in September 2002, also supports a global network of schol- ars and practitioners—based on five continents—with expertise in a broad range of academic disci- plines and in the power, transportation, water, telecommunications and natural resource sectors. Collaboratory for Research on Global Projects Yang & Yamazaki Energy & Environment (Y2E2) Bldg 473 Via Ortega, Suite 242 Stanford, CA 94305-4020 http://crgp.stanford.edu 2 About the Author Sagar Gandhi1 is a Building Information Modeling expert working with DPR Construction Inc. He is interested in implementation of BIM tools in practice for large scale developments. He has an ex- perience in Indian Construction industry for past 5 years and has been a successful partner at Gan- dhi Construction. He worked closely with Dr. Orr on understanding the urban development in India. Mr. Gandhi holds a Masters in Construction Engineering and Management from Stanford Univer- sity and B.E. in Civil Engineering from Maharashtra Institute of Technology, Pune University.. 1 [email protected] 3 Index 1. Acknowledgement 3 2. Abstract 4 3. -

French Bangalore

1 2 3 Laying out of mulberry orchards followed. Tipu Sultan who was fond of horticulture took particular interest in setting up mulberry orchards for the manufacture of silk. Under the various Governor Generals of France the two countries formed an urban city to the south, bordered by grape and mulberry fields, intersected with canals and large avenues. Bangalore developed into an urban horticultural centre of IN THE YEAR 1800 Napoleon Bonaparte sent South India under Tipu Sultan and his successors, and into a reinforcements to Tipu Sultan, the then ruler of Bangalore. well-administered and carefully planed city under the French French troops fought alongside the combined armies of Tipu who were ably aided in their efforts by capable Indian urban and the Nizam and together they forced back the British planners. army, which retreated to Madras, thus bringing to an end the third and last Anglo-Mysore war. Tipu Sultan never forgot the importance of military supremacy. He expanded the gunpowder works and lavished Thereafter, the French became an important player in the lots of care and expense on his army, which under the political set up of South India. In Bangalore they set up their strict military command of the French generals became a camp near Ulsoor Lake. By 1814, they had expanded and formidable force to be reckoned with. formed a well-guarded and planned city with canals running through Ulsoor to Lal Bagh. The combined efforts of the House of Tipu and its allies, the French, transformed Bangalore from a mere trade The ensuing period of peace allowed people to engage route station into a booming city of gardens and lakes, an themselves in more peaceful pursuits. -

BHM 2013 Aadil Basha a 76, Venugopal Swamy 8892729306 Temple Street, Anwar Adilbasha31@Gma Layout,, Bangalore Il.Com

List of Alumni of M. S. Ramaiah University of Applied Sciences (SAMPARK), Bangalore Faculty of Hospitality Management & Catering Technology Sl. Programme Year of Name Contact Address Photograph e-mail id NO. Completed Admission Mobile no. 1376 BHM 2013 Aadil Basha A 76, Venugopal swamy 8892729306 Temple street, Anwar adilbasha31@gma Layout,, Bangalore il.com 1375 BHM 2013 Abhilash Biswas No 185 13th B Main 9663150948 Road, Gokul 1st stage I abhilashbiswas@ Phase mathikere msrchm.edu Layout B’lore 560054 1374 BHM 2013 Abhimanyu Pratap Kundan Kunj, 90 A, 8938899440 Singh Negi Dharamdur, Haridwar abhimanyu.psn13 Road Dehradun 248001 @gmail.com 1373 BHM 2013 Adarsh Vijay Tejus, Melathayparambil, Olayanna Post Opp Palakurumba Devi Temple, Calicut 673019 1372 BHM 2013 Akash Borgeo A 831, 12th cross, 16th 9739647084 Main Road BTM Layout 9738693549 II stage B’lore 560076 akash.borgeo95@ gmail.com 1371 BHM 2013 Amir Chauhan 650, 2nd floor MES 7353470066 Road 4th Cross chauhanamir817 Mutyalamma nagar @gmail.com B’lore 560054 1370 BHM 2013 Anoop Sharma Shashi nagar, Amehal Road, Near Shiva Mangal School, Siliguri 734001 1369 BHM 2013 Anthony Mathews 670, 5th Cross, 4th Main, 8904696859 M Kesare 3rd Stage RS 9986539332 Naidu nagar Mysore antonymathews44 570007 [email protected] 1368 BHM 2013 Anupan Valentine Peace Road, Lalpur By Minz Lane, Ranchi 834001 1367 BHM 2013 Anuraj KP Kotantavita House 9901088403 Chundayil St, PO 9066056537 Edacheri North Via anuraj.aryan@gm Vadakara Calicut Kerala ail.com 673520 1366 BHM 2013 Arjun TU 8002, Omara, Prestige -

Bangalore Urban Ward Details

Ward Name District Taluka Hobli Ward Number Ward Name in English Area Comes Under Concern Ward in Kannada Govindapura, Kulappa Layout, Vasudevapura, Kendriya Vihar, Manchenahalli, Yelahanka (P), Yelhanka Airport Area, Maheshwari Nagar, Sai spring field colony, Gandhi Nagar, Lake view residency, Nehru Nagar, Venkatala, Surabhi Layout, Venkatappa Layout, Shobha Ultima villas, Bangalore Bangalore North Addl Yelahanka-1 Ward-1 Kempegowda ಂಡ Venkatala Layout, Mantri township, Vikas layout, Yelahanka Kere, Shankaranna Layout, Sathyappa Anjanappa Kempamma Layout, Shivanahalli (P), Maruthi Nagar, Sapthagiri Layout (P), Jayanna Layout, Basaveshwara Nagar (P), Bhadranna Layout Harohalli, Harohalli kere, Kanchenahalli, ISRO Layout, Naganahalli, Naganahalli new layout, KEB Layout Phase I, Balaji Layout, Vinayaka Layout, Ramanashree Califonia East Garden layout, Deo Marvel Layout, Mahalaxmi Bangalore Bangalore North Addl Yelahanka-1 Ward-2 Chowdeshwari ಶ Layout, Nisarga Layout, CRPF Quarters, Puttanahalli, Puttanahalli kere, Monte Carlo apartment, DG staff quarters, Central excise quarters, Wheel and Axle plant, FM Goetze plant, Chowdeswari Layout, Kamakshiamma Layout, East Colony, Yelahanka (P), KHB Colony Ananthapura, Chikka Bettahalli, Dodda Bettahalli, Bharat Nagar (MS Palya), Chandrappa Layout, Hill side meadows layout, Sai Nagar Phase I and II, Basavalingappa Layout, Netravathi Layout (P), Sai orchards, Best country 3, G Ramaiah Layout, Jyothi Nagar, GPF Layout, Muneshwara Layout 1st and 2nd Bangalore Bangalore North Addl Yelahanka-3 Ward-3 -

District: Benga

Details of Respective area engineers of BESCOM (Row 2 - District name) (Column 10 - Alphabetical order of Areas) District: Bengaluru uban Sl No Zone Circle Division Sub Division O&M Unit Areas 1 2 3 4 5 6 7 8 9 10 11 12 13 Service Superintending Executive Assistant Executive Assistant Engineer / Junior Name Chief Engineer Name Name Name Name Station Engineer Engineer Engineer Engineer Number Sri.T.S Chandran AE Sri. Venkatesh 9449864538 Abbigere F-2:- Raghavendra L/o, Old KG Halli, Abbigere F-3:-Lakshmi Pura, Vaderahalli (V), Sri. B.G Umesh Sri. Lakshmish Assistant Executive 94498 44988 JE Sri. Lingaraju 9449631101 Abbigere F-5:- Lakshmi Pura Main Rd, Singa Pura, Lakappa L/o, Singa Pura L/o, Abbigere Indl Area, BMAZ 8277892599 82778 93904 Engineer Sri. Mylarappa 1 North 080-22350436 Jalahalli C3 ABBIGERE JE Sri. Somashekar Reddy 94484 32824 9448365156 Abbigere F-7:- Abbigere (V), Pipe Line Rd, Venkateshwara l/o, Suraj L/o, NORTH [email protected] [email protected] senorthcircle.work@gmail A 9449844643 JE Sri. Yacob 9900723350 Abbigere F-8:- Kala Nagar, KG Halli,Abbigere F-9:- Vishweshwaraiah l/o, [email protected] n .com [email protected] JE Sri. Sunkaiah 9342892872 HVVY Vally, Kuvempu Nagar, Abbigere F-10:- KashVaderahalli L/o, Muneshwara l/o, Renuka L/o, Sri. M Sri.Thippesamy, Chennakeshava Assistant Executive Sri.Sriramegowda 9449877444 Adugodi, Koramangala 7th Block, 8th Block, Koramangala Village, KR Garden Village, Balappa L/o, 94498 44613 Engineer Sri. Manoj BMAZ 9449045888 sesouthcircle.work Koramangal AE 9449868075 Munikrishnappa L/o, AK Colony, Rajendra Nagar, Ambedkar Nagar, LR Nagar, Devegowda Block, 2 South eeadnlsouth.work@ S4 Kumar 9449844664 ADUGODI JE Sri. -

Urban Sociology Paper- Unit-IV Infrastructure in Bangalore

6sem- Urban Sociology paper- unit-IV Infrastructure in Bangalore Bengaluru (/ˈbæŋɡəlɔːr/; Kannada: ಬᢂಗ쳂상 [ˈbeŋɡaɭuːru]) is the capital and the largest city of the Indian state of Karnataka. It is India's third largest city and fifth largest metropolitan area. Modern Bengaluru was founded in 1537 CE by Kempe Gowda, a vassal of the Vijayanagara Empire. Kempe Gowda built a mud fort in the vicinity of modern Bengaluru. By 1831, the city was incorporated into the British Raj with the establishment of the Bangalore Cantonment. The British returned dominion of the city to the King of Mysore, choosing however, to retain jurisdiction over the cantonment. Therefore, Bengaluru essentially became a twin city, with civic and infrastructural developments of the cantonment conforming to European styles of planning. For most of the period after Indian independence in 1947, Bengaluru was a B-1 status city, and was not considered to be one of India's "4 major metropolitan cities". The growth of Information Technology in the city, which is the largest contributor to India's software exports, has led to a decadal growth that is second to only that of India's capital New Delhi. The city's roads, however, were not designed to accommodate the vehicular traffic, growing at an average of 8% annually, that prevails in Bengaluru. This leads to heavy slow traffic and traffic jams in Bengaluru Bangalore continues to fall behind in this area, and foreign visitors are often shocked to see the state of infrastructure, but now things are improving thanks to heavy investment of the Karnataka Government in infra projects.