The Financialisation of Big Tech

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rich Corporations Poor Societies

Rich corporations, poor societies: The financialisation of Apple By Rodrigo Fernandez (SOMO) and Reijer Hendrikse October 2015 Contents 1 Introduction ..................................................................................................... 3 2 Corporate financialisation .................................................................................. 5 3 The financialisation of Apple ............................................................................10 3.1 A short overview ......................................................................................10 3.2 Offshoring/outsourcing production ...............................................................12 3.3 Offshoring paper trails ...............................................................................13 3.4 Apple’s cash pile ......................................................................................15 3.5 A corporate cash machine .........................................................................17 4 Conclusion .....................................................................................................19 Glossary .............................................................................................................21 Colophon ............................................................................................................22 1 Introduction At the dawn of the new millennium, Apple Inc. stands as the epitome of a digitalised and globalised economy shaped by information and communication technologies. A world -

The Silicon Six

The Silicon Six and their $100 billion global tax gap December 2019 © Fair Tax Mark 2019 About the Fair Tax Mark The Fair Tax Mark certification scheme was launched in - regulators, investors and municipalities across the UK in 2014, and seeks to encourage and recognise the globe have expressed a desire to support Fair organisations that pay the right amount of corporation tax Tax Mark accreditation (or equivalent) in their at the right time and in the right place. Tax contributions jurisdictions; are a key part of the wider social and economic contribution made by business, helping the communities - there is in many parts of the world an ongoing in which they operate to deliver valuable public services international race to the bottom on tax, and and build the infrastructure that paves the way for growth. this creates a downward pressure on standards everywhere (including in the UK); and More than fifty businesses have now been certified in the UK, including FTSE-listed PLCs, co-operatives, - if no action is taken by civil society, unscrupulous social enterprises and large private business – which accounting and auditing entities will step into the between them have over 7,000 offices and outlets. vacuum and propagate low-bar tax kitemarks. We operate as a not-for-profit social enterprise and believe that companies paying tax responsibly should Further information at: be celebrated, and any race to the bottom resisted. • Website: www.fairtaxmark.net To date, the Fair Tax Mark’s activities have been focused on the UK; however, a new suite of international • Phone: (within UK) 0161 7690427 / standards is now under development. -

Global Voting Activity Report to March 2019

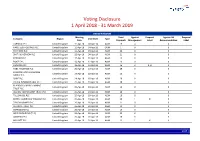

Voting Disclosure 1 April 2018 - 31 March 2019 UNITED KINGDOM Meeting Total Against Proposal Against ISS Proposal Company Region Vote Date Type Date Proposals Management Label Recommendation Label CARNIVAL PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 19 0 0 HANSTEEN HOLDINGS PLC United Kingdom 11-Apr-18 04-Apr-18 OGM 1 0 0 RIO TINTO PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 22 0 0 SMITH & NEPHEW PLC United Kingdom 12-Apr-18 04-Apr-18 AGM 21 0 0 PORVAIR PLC United Kingdom 17-Apr-18 10-Apr-18 AGM 15 0 0 BUNZL PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 19 0 0 HUNTING PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 16 2 3, 8 0 HSBC HOLDINGS PLC United Kingdom 20-Apr-18 13-Apr-18 AGM 29 0 0 LONDON STOCK EXCHANGE United Kingdom 24-Apr-18 18-Apr-18 AGM 26 0 0 GROUP PLC SHIRE PLC United Kingdom 24-Apr-18 18-Apr-18 AGM 20 0 0 CRODA INTERNATIONAL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 18 0 0 BLACKROCK WORLD MINING United Kingdom 25-Apr-18 19-Apr-18 AGM 15 0 0 TRUST PLC ALLIANZ TECHNOLOGY TRUST PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 10 0 0 TULLOW OIL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 16 0 0 BRITISH AMERICAN TOBACCO PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 20 1 8 0 TAYLOR WIMPEY PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 21 0 0 ALLIANCE TRUST PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 13 0 0 SCHRODERS PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 19 0 0 WEIR GROUP PLC (THE) United Kingdom 26-Apr-18 20-Apr-18 AGM 23 0 0 AGGREKO PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 20 0 0 MEGGITT PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 22 1 4 0 1/47 -

Google, Bing, Yahoo!, Yandex & Baidu

Google, bing, Yahoo!, Yandex & Baidu – major differences and ranking factors. NO IMPACT » MAJOR IMPACT 1 2 3 4 TECHNICAL Domains & URLs - Use main pinyin keyword in domain - Main keyword in the domain - Main keyword in the domain - Main keyword in the domain - Easy to remember Keyword Domain 1 - As short as possible 2 - As short as possible 2 - As short as possible 11 - As short as possible - Use main pinyin keyword in URL - Main keyword as early as possible - Main keyword as early as possible - Main keyword as early as possible - Easy to remember Keyword in URL Path 3 - One specific keyword 3 - One specific keyword 3 - One specific keyword 11 - As short as possible - As short as possible - As short as possible - As short as possible - No filling words - No filling words - As short as possible Length of URL 2 2 2 22 - URL directory depth as brief as possible - No repeat of terms - No repeat of terms - Complete website secured with SSL -No ranking boost from HTTPS - No active SSL promotion - Complete website secured with SSL HTTPS 3 - No mix of HTTP and HTTPS 2 -Complete website secured with SSL 1 - Mostly recommended for authentication 22 - HTTPS is easier to be indexed than HTTP Country & Language - ccTLD or gTLD with country and language directories - ccTLD or gTLD with country and language directories - Better ranking with ccTLD (.cn or .com.cn) - Slightly better rankings in Russia with ccTLD .ru Local Top-Level Domain 3 - No regional domains, e.g. domain.eu, domain.asia 3 - No regional domains, e.g. -

Big Tech and Democracy: the Critical Role of Congress

TECHNOLOGY AND PUBLIC PURPOSE PROJECT Big Tech and Democracy: The Critical Role of Congress Key Policy Considerations to Address Tech Platforms PAPER APRIL 2019 Technology and Public Purpose Project Belfer Center for Science and International Affairs Harvard Kennedy School 79 JFK Street Cambridge, MA 02138 www.belfercenter.org/TAPP Platform Accountability Project Shorenstein Center for Media, Politics and Public Policy Harvard Kennedy School 124 Mount Auburn Street, 2nd Floor, South Elevators Cambridge, MA 02138 www.shorensteincenter.org Statements and views expressed in this report are solely those of the authors and do not imply endorsement by Harvard University, Harvard Kennedy School, the Belfer Center for Science and International Affairs, or the Shorenstein Center for Media, Politics and Public Policy. Design and layout by Andrew Facini Cover photo: Adobe Stock Copyright 2019, President and Fellows of Harvard College Printed in the United States of America TECHNOLOGY AND PUBLIC PURPOSE PROJECT Big Tech and Democracy: The Critical Role of Congress Key Policy Considerations to Address Tech Platforms Bogdan Belei Bennett Craig Nicco Mele Toni Bush Daniel Gastfriend Hong Qu Maeve Campbell Dipayan Ghosh Amy Robinson Ash Carter Gene Kimmelman Philip Verveer Lucy Chase Heidi Legg Tom Wheeler Mignon Clyburn Laura Manley PAPER APRIL 2019 Co-Sponsoring Organizations The Technology and Public Purpose (TAPP) Project at the Harvard Kennedy School’s Belfer Center for Science and International Affairs works to ensure that emerging technologies are developed and managed in ways that serve the overall public good. Led by Belfer Center Director, MIT Innovation Fellow, and former Secretary of Defense Ash Carter, the TAPP Project leverages a network of experts from Harvard University, MIT, and Stanford, along with leaders in technology, government, and business. -

A Case Study by Manning & Napier

Historical Impact of Regulation on Big Tech A Case Study by Manning & Napier Originally Published: January 2019 www.manning-napier.com Introduction After years of growth, the information technology sector is facing renewed regulatory scrutiny over its size and power. The inquiries have come at a time when the roles of privacy, fake news, and information bubbles are being challenged in our increasingly digital lives. While little has derailed the internet giants thus far, calls for government oversight are on the rise. With the immense scale and market power of these companies, we should expect regulatory scrutiny to be an ongoing issue. To better understand the consequences of ongoing regulatory scrutiny, Manning & Napier’s technology group looked at past tech industry leaders that faced similar bouts of government oversight, and analyzed the regulatory impact on historical stock performance. The Process In conducting the analysis, our team analyzed eight US-based technology companies that were dominant in their respective eras. Within the companies, we identified 54 discrete regulatory cases from 1900 through the present day1 . We built regulatory timelines for each case and measured the before and after stock price returns per case, per company. Additionally, among the identified cases that led to a significantly negative impact, we observed key warning signs. 2 www.manning-napier.com Key Takeaways The Companies Studied Regulatory scrutiny is usually a non-event. IBM • The vast majority of the tech companies IBM’s first brush with anti-trust scrutiny was reviewed posted strong absolute and relative in 1932. Then again in the 1950s. The famous returns well beyond their first brush with 1969 -1982 case was actually IBM’s third brush with regulators. -

Southwestern Journal of International Law

\\jciprod01\productn\s\swt\24-1\toc241.txt unknown Seq: 1 9-MAR-18 8:49 SOUTHWESTERN JOURNAL OF INTERNATIONAL LAW VOLUME XXIV 2018 NUMBER 1 TABLE OF CONTENTS SYMPOSIUM FREEDOM OF INFORMATION LAW S O N T H E GLOBAL STAGE: PAST, PRESENT AND FUTURE JOHN MOSS AND THE ROOTS OF THE FREEDOM OF INFORMATION ACT: WORLDWIDE IMPLICATIONS .................................... 1 Michael R. Lemov & Nate Jones RALPH NADER, LONE CRUSADER? THE ROLE OF CONSUMER AND PUBLIC INTEREST ADVOCATES IN THE HISTORY OF FREEDOM OF INFORMATION ....................................................... 41 Tom McClean Articles ARGENTINA’S SOLUTION TO THE MICHAEL BROWN TRAVESTY: A ROLE FOR THE COMPLAINANT VICTIM IN CRIMINAL PROCEEDINGS ... 73 Federico S. Efron MARTIAL LAW IN INDIA: THE DEPLOYMENT OF MILITARY UNDER THE ARMED FORCES SPECIAL POWERS ACT, 1958 ................... 117 Khagesh Gautam © 2018 by Southwestern Law School \\jciprod01\productn\s\swt\24-1\toc241.txt unknown Seq: 2 9-MAR-18 8:49 Notes & Comments A CRITIQUE OF PERINCEK ¸ V. SWITZERLAND: INCORPORATING AN INTERNATIONAL AND HISTORICAL CONTEXT IS THE MORE PRUDENT APPROACH TO GENOCIDE DENIAL CASES ........................... 147 Shant N. Nashalian A CUTE COWBOY STOLE OUR MONEY: APPLE, IRELAND, AND WHY THE COURT OF JUSTICE OF THE EUROPEAN UNION SHOULD REVERSE THE EUROPEAN COMMISSION’S DECISION .................. 177 Chantal C. Renta Review BOOK REVIEW PHILIPPE SANDS, EAST WEST STREET: ON THE ORIGINS OF “GENOCIDE” AND “CRIMES AGAINST HUMANITY” (ALFRED A. KNOPF ED., 2016) ...................................... 209 Vik Kanwar \\jciprod01\productn\s\swt\24-1\boe241.txt unknown Seq: 3 9-MAR-18 8:49 SOUTHWESTERN JOURNAL OF INTERNATIONAL LAW VOLUME XXIV 2018 NUMBER 1 Editor-in-Chief SHANT N. -

The Calling Card of Russian Digital Antitrust✩ Natalia S

Russian Journal of Economics 6 (2020) 258–276 DOI 10.32609/j.ruje.6.53904 Publication date: 25 September 2020 www.rujec.org The calling card of Russian digital antitrust✩ Natalia S. Pavlova a,b,*, Andrey E. Shastitko a,b, Alexander A. Kurdin b a Russian Presidential Academy of National Economy and Public Administration, Moscow, Russia b Lomonosov Moscow State University, Moscow, Russia Abstract Digital antitrust is at the forefront of all expert discussions and is far from becoming an area of consensus among researchers. Moreover, the prescriptions for developed countries do not fit well the situation in developing countries, and namely in BRICS: where the violator of antitrust laws is based compared to national firms becomes an important factor that links competition and industrial policy. The article uses three recent cases from Russian antitrust policy in the digital sphere to illustrate typical patterns of platform conduct that lead not just to a restriction of competition that needs to be remedied by antitrust measures, but also to noteworthy distribution effects. The cases also illustrate the approach taken by the Russian competition authority to some typical problems that arise in digital markets, e.g. market definition, conduct interpretation, behavioral ef- fects, and remedies. The analysis sheds light on the specifics of Russian antitrust policy in digital markets, as well as their interpretation in the context of competition policy in developing countries and the link between competition and industrial policies. Keywords: digital antitrust, competition policy, industrial policy, platforms, multi-sided markets, essential facilities, consumer bias. JEL classification: K21, L41. 1. Introduction Russian antitrust as a direction of economic policy has a relatively short history, but a rich experience in the application of antitrust laws in areas that are considered digital. -

Digital Trade Rules and Big Tech

PUBLIC SERVICES INTERNATIONAL The global union federation of workers in public services ENGLISH Digital trade rules and big tech: SURRENDERING PUBLIC GOOD TO PRIVATE POWER CONTENTS Abbreviations Overview 1. KEY IMPACTS OF DIGITISATION ON PUBLIC SERVICES 2. BIG TECH’S ‘DIGITAL TRADE’ DEMANDS 3. DIGITISED HEALTHCARE 4. “SMART CITIES” 5. RECOMMENDATIONS References Digital trade rules and Big Tech: SURRENDERING PUBLIC GOOD TO PRIVATE POWER Written by Professor Jane Kelsey, Faculty of Law, The University of Auckland, New Zealand, with research support from Mary Ann Manahan, and peer reviewed by Dr Bill Rosenberg. © Public Services International February 2020 © Cover illustration Anthony Russo 2 DIGITAL TRADE RULES AND BIG TECH: ABBREVIATIONS AI Artificial intelligence AIIB Asian Infrastructure Investment Bank D2D Digital 2 Dozen principles FTA Free trade agreement GAFA Google, Amazon, Facebook, Apple GATS General Agreement on Trade in Services IoT Internet of Things IT Information technology PPP Public Private Partnerships R&D Research and development SOE State-owned enterprise SPV Special Purpose Vehicle TPPA Trans-Pacific Partnership Agreement USTR United States Trade Representative WTO World Trade Organization SURRENDERING PUBLIC GOOD TO PRIVATE POWER 3 OVERVIEW ig Tech companies like Google, intelligence that does the work of doc- Amazon, Facebook and Apple – tors, technicians and prison officers. BGAFA for short - are using free Private contractors run the IT opera- trade agreements to protect them- tions and data bases of government selves from regulation. The idea of a agencies, storing our data on their own ‘free and open’ Internet sounds liberat- servers or in the ‘cloud’, which usually ing. But a world in which powerful and means they are controlled in the United unregulated private corporations con- States. -

Press-Release Morgan Lewis Advises Yandex 31.08.2021 ENG

Contacts: Emily Carhart Director of Public Relations & Communications +1.202.739.5392 [email protected] Olga Karavaeva Marketing & Communications Manager in Russia +7.495.212.25.18 [email protected] Morgan Lewis Advising Yandex on $1B Acquisition of Interests in Businesses from Uber LONDON and MOSCOW, September 8, 2021: Morgan Lewis is advising Yandex on the restructuring of the ownership of its MLU and Self-Driving joint ventures with Uber, which will see Yandex own 100% of the Yandex.Eats, Yandex.Lavka, Yandex.Delivery and Self-Driving businesses, for consideration of $1.0 billion in cash. Yandex has also received an option to purchase Uber’s remaining stake in MLU over a two-year period for approximately $1.8 billion in cash. Yandex is one of Europe's largest internet companies and a leading search and ride-hailing provider in Russia. The cross-border Morgan Lewis team advising Yandex includes partners Tim Corbett, Nick Moore, Ksenia Andreeva, Anastasia Dergacheva and Omar Shah, and associates Ben Davies, Abbey Brimson, and Leonidas Theodosiou. For more, see Yandex’s announcement. About Morgan, Lewis & Bockius LLP Morgan Lewis is recognized for exceptional client service, legal innovation, and commitment to its communities. Our global depth reaches across North America, Asia, Europe, and the Middle East with the collaboration of more than 2,200 lawyers and specialists who provide elite legal services across industry sectors for multinational corporations to startups around the world. For more information about us, please visit www.morganlewis.com and connect with us on LinkedIn, Twitter, Facebook, Instagram, and WeChat. -

Apple Inc's Marketing Plan

University of Puthisastra Faculty of Economic and Business Marketing Research Topic: Apple Inc.’s Marketing Strategies Lecturer: Sreang Kimlee Group Members: Yorn Sophearith Kong Veasna Khan Sokna Academic Year: 2011-2012 Semester I:Y4 Contents I. Introduction to Apple Inc. II. Marketing Strategies of Apple III. Conclusion I. Introduction to Apple inc Apple is a multinational corporation designing and selling consumer electronics, computer’s software and personal computers It was established on April 1, 1976 and became Apple Computer Inc. on January 3, 1977 then changed to Apple Inc in 2007 Founders: Steve Jobs, Steve Wozniak and Ronald Wayne with the start-up cost was only $1300 I. Introduction to Apple inc Apple has: Staff: 60,400 Retailed stores: 357 (Oct 2011) Subsidiaries: Braeburn Capital, FileMaker Inc., and Anobit Revenues:$108.249 billion (2011) Asset: $116.371 billion (2011) Profit: $25.922 billion (2011) International Rank: The Most Value Company (2010) I. Introduction to Apple inc Apple’s products: Hardware products: Macintosh line of computers, iPod (iPod Nana, iPod Touch), iPhone, and iPad Software products: Mac OS X operating system, iTune media browser, the iLife, the iWork, Aperture, Final Cut Studio, Logic Studio, Safari browser and iOS I. Introduction to Apple Inc I. Introduction to Apple inc Apple’s progressions: 1976-1980: Apple I introduced in1976, and Apple II in 1977. 1981-1985: Lisa and Mocintosh era and Management conflict. 1986-1993: Rise and Fall. Apple introduced Power Book that brought success and increased revenue. Then Apple failed consumer targeted some products. 1994-1997: Attempts at reinvention. 1998-2004: Return to profitability I. -

Why Are Some Websites Researched More Than Others? a Review of Research Into the Global Top Twenty Mike Thelwall

Why are some websites researched more than others? A review of research into the global top twenty Mike Thelwall How to cite this article: Thelwall, Mike (2020). “Why are some websites researched more than others? A review of research into the global top twenty”. El profesional de la información, v. 29, n. 1, e290101. https://doi.org/10.3145/epi.2020.ene.01 Manuscript received on 28th September 2019 Accepted on 15th October 2019 Mike Thelwall * https://orcid.org/0000-0001-6065-205X University of Wolverhampton, Statistical Cybermetrics Research Group Wulfruna Street Wolverhampton WV1 1LY, UK [email protected] Abstract The web is central to the work and social lives of a substantial fraction of the world’s population, but the role of popular websites may not always be subject to academic scrutiny. This is a concern if social scientists are unable to understand an aspect of users’ daily lives because one or more major websites have been ignored. To test whether popular websites may be ignored in academia, this article assesses the volume and citation impact of research mentioning any of twenty major websites. The results are consistent with the user geographic base affecting research interest and citation impact. In addition, site affordances that are useful for research also influence academic interest. Because of the latter factor, however, it is not possible to estimate the extent of academic knowledge about a site from the number of publications that mention it. Nevertheless, the virtual absence of international research about some globally important Chinese and Russian websites is a serious limitation for those seeking to understand reasons for their web success, the markets they serve or the users that spend time on them.