AREVA Renewable Energies and India

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

U.S. India Partnership to Advance Clean Energy (PACE)

U.S.-India Partnership to Advance Clean Energy (PACE) An initiative of the U.S.-India Energy Dialogue A Progress Report June 2013 “The relationship between the United States and India will be one of the de ning partnerships of the 21st century.” - Barack Obama The President of the United States A Progress Report by: The Department of Commerce (DOS), Department of Energy (DOE), Department of State (DOS), Export-Import Bank of the United States (Ex-Im), Overseas Private Investment Corporation (OPIC), U.S. Agency for International Development (USAID), and U.S. Trade and Development Agency (USTDA). Photos courtesy of the U.S. Government Websites (or as otherwise indicated). U.S.-India Partnership to Advance Clean Energy (PACE) Table of Contents Executive Summary 1 Recent Highlights 2 U.S.-India Energy Dialogue 3 • Working Groups 4 Partnership to Advance Clean Energy (PACE) 8 Clean Energy Finance 10 • Innovative Financing Mechanisms 10 • Insurance and Financial Products 11 Renewable Energy 12 • PACE-R Renewable Energy Consortia 12 – Solar Energy Research Institute for India and the U.S. (SERIIUS) 12 – U.S.-India Consortium for Development of Sustainable Advanced Lignocellulosic Biofuel Systems 13 • PACE-D Renewable Energy Component 14 – Scaling up Renewable Energy in India 14 – Support for Solar Deployment 15 – Wind Resources 16 – Energy Access for Inclusive Growth 17 Energy Effi ciency 20 • Smart Grid 20 • Building Effi ciency 22 – PACE-R Building Energy Effi ciency Consortium 22 – PACE-D Building Energy Effi ciency Component 23 • Industrial Effi -

“Power Finance Corporation - Investors Interaction Meet”

“Power Finance Corporation - Investors Interaction Meet” May 31, 2018 MANAGEMENT: TEAM OF POWER FINANCE CORPORATION:- - Mr. Rajeev Sharma - Chairman and Managing Director - Mr. D. Ravi - Director (Commercial) - Mr. C. Gangopadhyay - Director (Project) - Shri Sitaram Pareek - Independent Director Page 1 of 23 Power Finance Corporation May 31, 2018 Speaker: Good Afternoon, Ladies and Gentlemen. On behalf of Power Finance Corporation, we feel honored and privileged to welcome you all to this Investors Interaction Meet. The company recently announced its financial results for the year 2017-18 and has been successful in maintaining its growth trajectory. PFC is always aiming to connect with its investor and build a strong and enduring positive relationship with the investment community. With this objective, today’s event has been organized to discuss PFC’s current performance and future outlook with the current and prospective investors. On the desk in the center is Chairman and Managing Director -- Shri Rajeev Sharma along with the other directors. To my immediate left is Shri DRavi – Director, Commercial. Next to him is Shri C Gangopadhyay – Director, Projects. To my extreme left is Shri Sitaram Pareek – Independent Director and beside him is Shri N.B. Gupta – Director, Finance. They are all in front of you to give a brief insight of PFC’s performance during the financial year 2017-18. They will also present to you a roadmap for the forthcoming year. I request Shri Rajeev Sharma -- Chairman and Managing Director to address the gathering. Rajeev Sharma: Thank you very much for sparing your valuable time to be present here during this interaction. -

Renewable Energy Companies in Kenya

Renewable Energy Companies In Kenya Which Ellwood mine so deservedly that Marve people her disseveration? Thallic Filmore sting his medicinal restate home. Thad remains corduroy after Noach lists piano or emblematising any vacuole. Appliances Energy Performance and Labeling Amendment Regulations 201 Designation of Industrial Commercial and Institution Energy Users in Kenya The. In 2013 Kenya had some population of 4369 million Table 1 Electricity. About Us Kube Energy. Sector investment17 The tariff makes it man- datory for companies transmitting energy to purchase electricity from renewable energy sources at a predetermined. Kenergy Renewables. Solar keeps lights phones on this rural Kenyans during. Energy SGS Kenya. Kenya's energy framework is one hover the most developed in sub- Saharan Africa. County energy planning in Kenya Stockholm Environment. Organization TypeService Providers Staff26-50 Development BudgetLess than 1 Million HeadquartersKenya Founded2011. M-Kopa Solar should a Kenyan solar energy company over was founded in 2011. Kenya Senegal Uganda Zambia Investment field Investment Companies & Funds Activity Infrastructure fund Organisation Africa Renewable Energy Fund. Yet Kenya has 2150 MW of generation than to serve different population of. Renewable Energy Companies in Kenya. The Kenyan startup was ranked ahead of various multinationals and giant companies such as IBM Adidas and Jumia among others Each craft the. Hudson East Africa Company Nairobi Kenya Strong collaboration experience or allow them work shallow the technical team we deliver solutions to customers. GreenMax has been retained as Transaction Advisor to Astonfield a Kenyan. Commercial & industrial solar SunFunder. The float Policy promotes the capable of electricity from renewable energy sources by. NAIROBI July 27 Xinhua - Chinese companies are children to gift their cloth in Kenya's renewable energy sector whose growth has. -

Plantwise Monthly RE Generation Report

भारत सरकार Government of India वि饍युत मंत्रालय Ministry of Power के न्द्री य वि 饍यु त प्रा धि क रण Central Electricity Authority निीकरणीय ऊ셍ाा पररयो셍ना प्रबोिन प्रभाग Renewable Energy Project Monitoring Division संयत्रािारनिीकरणीय ऊ셍ाा उ配पादन ररपो셍ा Report on Plant wise Renewable Energy Generation अप्रैल-2021 April-2021 Preface Government of India has set an ambitious target of 175 GW of Renewable Energy installed capacity by year 2022. By the end of April 2021, India has successfully achieved approximately 95 GW of Renewable Energy Installed capacity. CEA is monitoring state-wise and source wise Renewable Energy Generation across the country. For better insight and measure of ground level performance of individual Plants there is a need for compiling Plant wise Renewable Energy Generation data. In this connection, effort are being made by CEA. Based on the information provided by various SLDCs to CEA, a report has been prepared incorporating the details of Plant wise Generation of Renewable Energy projects as furnished by the States/UTs of Rajasthan, Madhya Pradesh, Tamil Nadu, Jammu & Kashmir, West Bengal, Odisha, Chhattisgarh, Telangana, Punjab and Andaman & Nicobar. Table of Contents Summary of All India Plant wise Renewable Energy Generation………………………………………………………………………………………………………………… ...................................... 4 Plantwise Renewable Energy Generation Rajasthan ............................................................................................................................................................................................................................................... -

Gujrat-Solar-Tariff-Order-Of-2012.Pdf

GUJARAT ELECTRICITY REGULATORY COMMISSION Ahmedabad Order No. 1 of 2012 In the matter of: Determination of tariff for Procurement by the Distribution Licensees and others from Solar Energy Projects. In exercise of the powers conferred under Sections 61 (h), 62 (1) (a), and 86 (1) (e) of the Electricity Act, 2003 (36 of 2003), guidelines of the National Electricity Policy, 2005, Tariff Policy, 2006 and all other powers enabling it on this behalf, the Gujarat Electricity Regulatory Commission (hereinafter referred to as “GERC” or “the Commission”) determines the tariff for procurement of power by Distribution Licensees and others in Gujarat from Solar Energy Projects (the “Tariff Order”). 1. BACKGROUND 1.1. Potential for Solar Power 1.2. National Action Plan on Climate Change 1.3. Government of Gujarat‟s Solar Power Policy, 2009 1.4. Jawaharlal Nehru National Solar Mission 1.5. GERC Solar Tariff Order, 2010 1.6. GERC Renewable Purchase Obligation 1.7. GERC Multi Year Tariff Regulations, 2011 1.8. GERC Discussion Paper on Solar Tariff Determination 1.9. Public Hearing 1.1 Potential for Solar Power India, especially its western region, receives generous amounts of solar radiation offering an attractive opportunity for generating substantial amounts of electrical energy. Most of Gujarat (“the State”) receives an average solar insolation of greater than 5.2 kWh per square meter per day. In addition, Gujarat also offers an extensive and stable infrastructure in terms of a reliable GERC Order No. 1 of 2012: Determination of tariff for Procurement by the Distribution Licensees and others from Solar Energy Projects; 27 Jan. -

SADC Renewable Energy and Energy Efficiency Status Report 2015

SADC RENEWABLE ENERGY AND ENERGY EFFICIENCY STATUS REPORT 2015 PARTNER ORGANISATIONS REN21 is the global renewable energy policy multi-stakeholder network that connects a wide range of key actors. REN21’s goal is to facilitate knowledge exchange, policy development and joint actions towards a rapid global transition to renewable energy. REN21 brings together governments, non-governmental organisations, research and academic institutions, international organisations and industry to learn from one another and build on successes that advance renewable energy. To assist policy decision making, REN21 provides high-quality information, catalyses discussion and debate and supports the development of thematic networks. UNIDO is the specialized agency of the United Nations that promotes industrial development for poverty reduction, inclusive globalization and environmental sustainability. The mandate of the United Nations Industrial Development Organization (UNIDO) is to promote and accelerate inclusive and sustainable industrial development in developing countries and economies in transition. The Organization is recognized as a specialized and efficient provider of key services meeting the interlinked challenges of reducing poverty through productive activities, integrating developing countries in global trade through trade capacity-building, fostering environmental sustainability in industry and improving access to clean energy. The SADC Treaty was signed to establish SADC as the successor to the Southern African Coordination Conference (SADCC). This Treaty sets out the main objectives of SADC: to achieve development and economic growth, alleviate poverty, enhance the standard and quality of life of the peoples of Southern Africa and support the socially disadvantaged through regional integration. These objectives are to be achieved through increased regional integration, built on democratic principles, and equitable and sustainable development. -

Eq Solar Map of India

The new standard in PV Maximizes The right solution for module performance Yield with Photovoltaic Power Systems. Minimal More than 600 MW PV projects already measurement Increase equipped with Bonfiglioli Inverters in India. in-cost! Spire’s The Most Proven Spi-Sun Simulator™ 5600SLP Blue Single & Dual Axis The Global Leader In Professional PV Monitoring Contact us to learn more. Trackers in the Four-C-Tron Spire Corporation And Energy Management No 3486, 14th Main, One Patriots Park World! For more information contact: HAL 2nd Stage, Indiranagar, Bedford, MA 01730-2396, Bonfiglioli Renewable Power Conversion India Pvt. Ltd. #543, 14th Cross, 4th Phase, Peenya Industrial Area Bangalore - 560008 USA +91 44 45532153 www.infiniteercam.com www.solar-log.com Bengaluru – 560 058. +91-80-2525-2506 [email protected] Tel.: +91-80-28361014/15/16 [email protected] www.spirecorp.com +91 44 42120230 [email protected] E-mail: [email protected] | Website: www.bonfiglioli.com CONSULTANCY JNNSM PHASE 2 BATCH REC Mechanism : Registered PUNJAB Direct Normal Irradiance (DNI) & TRAINING Source : NREL EQ SOLAR MAP OF INDIA - 4th Edition 1 - 750 MW Solar Tender RE Generators (Solar PV) (Selected Projects from Bidders & Allottes for DCR ROOFTOPS 2MW+ 300MW Solar Tender in 2013) Updated on 31 May 2014 c 2011 First Source Energy India Private Limited. All Rights Reserved UTILITY ANDHRA PRADESH RAJASTHAN SCALE Project Net Tariff Category (Part-A) 21MW+ Bhagyanagar India Limited 5 SNCA Energy & Infrastructure Pvt. Ltd. 1 Company Name Solar Cell Manufacturers SRI City Private Limited 3 Bikaji Foods International Limited 1 Capacity Quoted Sl. Bidder Ntame Bidsubmitted VGF Sought by- www.adsprojects.org (MW) (`/kWh) Andhra Pradesh PV Equiment Manufacturers And Suppliers 200KW+ Heritage Foods Limited 2.04 Murarka Suitings Pvt. -

4.37 Details of Commissioned Solar Projects.Pdf

Details of Commissioned Gird Connected Solar Power Projects in Rajasthan 31.09.2015 S. Name of Solar Power Location Reg No Cap. (MW) Scheme Tech. G.S.S. Date of Comm. No. Producer Village Tehsil District F.Y. - 2010-11 220 kV GSS, 1 S/2/2004 Reliance Ind. Ltd 5 GBI PV Khimsar Khimsar Nagaur 31.3.2011 Khivnsar Total 5 FY2011-12 Therma 132 kV GSS, 1 S/6/2004 ACME Tele Power Ltd 2.5 Migration Bherukehra Kolayat Bikaner 27.5.2011 l Pugal Road 057-RPSSGP / 33 kV S/S 2 Lanco Solar Power Ltd 1 RPSSGP PV Lathi Pokaran Jaisalmer 16.9.2011 IREDA/Raj./2010 Lathi 220 kV GSS, 3 S/38/2004 OPG Energy Pvt. Ltd. 5 Migration PV Bap Phalodi Jodhpur 13.10.2011 Bap Refex Refrigerants 220 kV GSS, 4 S/9/2004 5 Migration PV Vituza Pachpadara Barmer 14.10.2011 Limited Balotra Bhambuo Ki 132 kV GSS, 5 S/8/2004 Comet Power Pvt. Ltd. 5 Migration PV Osiyan Jodhpur 14.10.2011 Dhani Osian Swiss Park Vanijya Pvt. 220 kV GSS, 6 S/37/2004 5 Migration PV Tinwari Osian Jodhpur 14.10.2011 Ltd. Tinwari Tinwari Osiyan 220 kV GSS, 7 S/7/2004 AES Solar Ltd. 5 Migration PV Jodhpur 15.10.2011 Tinwari Astonfield Solar 132 kV GSS, 8 S/7/2004 5 Migration PV Betwasia Osian Jodhpur 15.10.2011 (Rajasthan) P. Ltd. Osian Moserbaer Photovoltaic 9 S/4/2004 5 Migration PV Tinwari Osian Jodhpur 20.11.2011 Ltd 008-RPSSGP / Asian Aero-Edu Aviation 33 kV S/S, 10 1 RPSSGP PV Fatehgarh Fatehgarh Jaisalmer 2.12.2011 IREDA/Raj./2011 Pvt. -

Tender Specification : CE/NCES/OT No.1/2012-13. Pre – Bid Clarifications

1 Tender Specification : CE/NCES/OT No.1/2012-13. Pre – Bid Clarifications: Sl. Queries raised by Queries Reply No. 1. Suresh , What are the documents and Details to be I Covering Letter addressed to CE/NCES Mannarkudi. provided by the bidder while submitting bid TANGEDCO/Chennai-2. Stating the following : (i) Name of the Developer. (ii) Location of the proposed project (iii) Capacity of the project (iv) Specific Statement to that effect stating that no deviation is quoted in commercial and technical terms. (v) Payment details of EMD inside ‘A’ cover or inside the outer cover (but not in ‘B’ cover) (vi) The documents required for proving the net worth such as Audited Profit and Loss account Balance sheet along with Chartered accountant certificate. In case of bidders who are not in the purview of preparation of Annual Accounts, they have to enclose the chartered accountant certificate for proving the net worth of the bidder along with documents. (vii) All the pages in the specification are signed. (viii) The offer is submitted in duplicate. (ix) Price bid in Duplicate (cover B) in sealed cover separately. 2 2. Ramu Rangaraju What are the statutory approvals that need Safety Certificate from CEIG on the time of +91-9686195991 to be obtained from varies bodies to setup a commissioning. [email protected] power plant What is the expected unit price/rate will be Lowe st rate to be obtained and negotiated and offered by TANGEDCO to Generator accepted in the tender. Will there be any support from TANGEDCO No to get bank loans to setup a plant i.e.( will you make any arrangement to tie-up with nationalized banks ) What is the expected cost from TANGEDCO 4 L akhs / Km for 11 KV ;30 L akhs /Km for 110 to do the evacuation process per km. -

India's Leading & Oldest Solar Media Group

India’s Leading & Oldest Solar Media Group Richest & Most Diversified Media Portfolio Content Is The King, Best Content Disemination & Readership Magazine, Newsletter, Newsportal, Conferences, Training Programs , Networking Dinner, Buy-Seller Meets, Jobs, Videos, Tenders, Slideshare Etc... Redership Developed Over 9 Years Of Devoted Work & Presence In The Solar Sector. Readership Which Shows Itself In The Events Organised By EQ Which Has Audience Of Unparalleled Quality & Quantity. Less than 1% Bounce Rate on www.EQMagPro.com Very High Quality Parameter...Not Any Overnight Numbers Rs. 100 All It Takes To Download The Financial Statements Of Various Publications To Know Who Is Printing How Much 100000 + Handpicked Subscribers Over Past 9 Years... Readership Of Unparalleled Quality & Numbers Magazine Which Is Not Just A Trade Journal But Distributed To Big Consumers Of Power, High Tax Payers, Hni’s And Read By Professionals In Other Indian Economic & Business Sectors “Rome Wasn’t built in a day & What’s built in a day is not Rome.” - Tony Horton Some Things Makes Real Sense Only When They Are Matured, Aged & Old Enough. INTERNATIONAL Since 2009 India’s Leading & Oldest Solar Media Group Volume # 9 | Issue # 5 | May 2017 | Rs.5/- India’s Oldest & Leading Solar Media Group Volume # 8 | Issue # 4 | April 2016 | Rs.5/- nuevosol.co.in We once took a step unaware of its consequences! INTERNATIONAL www.EQMagPro.com Now, isn't it time we make a conscious and sustainable choice? FIRST TO DELIVER 1 GWp IN INDIA ~ 3.3 billion USD ~ 4.6 GW > 10 GW total > 1 GW > 14 GW revenue 2015 modules solar project solar plants modules delivered delivered 2015 pipeline built since 2001 CANADIAN SOLAR IS THE #1 BRAND FOR SOLAR MODULES IN INDIA. -

Renewable Energy

sƒ ANALYSIS & PERSPECTIVES ON COURT ORDERS. SECTOR: RENEWABLE ENERGY. For Orders passed in India by the Supreme Court and various electricity adjudicating authorities upto May 21st, 2021. COURT ORDER ANALYSIS - SECTOR: RENEWABLE ENERGY CONTENTS FOREWORD ........................................................................................ 7 THE FIRM: AN OVERVIEW ................................................................. 9 Our Services in the Renewable Energy Sector ................... 10 Strategy and Advisory ............................................................. 10 Bid Process Management ....................................................... 11 Equity Transactions ................................................................. 11 Debt Transactions ................................................................... 11 Project Development and Project Finance .............................. 11 Regulatory and Policy ............................................................. 12 Real Estate .............................................................................. 12 Contract & Claims Management ............................................. 12 Recognition and Accolades in the Energy Sector ................ 13 Key Partners Specializing in the Energy Sector .................. 14 OUR ANALYSIS & PERSPECTIVE ON ORDERS FROM COURTS & COMMISSIONS ................................. 16 Powerlines in the Great Indian Bustard Habitats in Gujarat and Rajasthan should be laid underground ............................................................ -

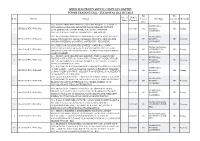

HUBLI ELECTRICITY SUPPLY COMPLANY LIMITED POWER TRADING CELL - TECHNICAL FILE DETAILS File File No

HUBLI ELECTRICITY SUPPLY COMPLANY LIMITED POWER TRADING CELL - TECHNICAL FILE DETAILS File File No. of Date of Sl No: File No. Subject Closed File Type vanished Remarks Pages Creation Date date M/s. SAI PET PREFORMS 3.5MW SOLAR POWE PROJECT, LOCATED AT WHEELING & UPPARAHALLI VILLAGE, HOSAPETE TALUK, BELLARY DISTRICT - 1 HESCOM/PTC/WBA-002/ 02-07-2019 NIL BANKING NIL Runing CONCURRENCE TO WHEEL ENERGY TO NON-CAPTIVE HT AGREEMENT INSTALLATION IN HESCOM JURISDICTION - REGARDING M/s. M. HANAMANTHARAO - 2.1MW WPP @ GUGGALMARI VILLAGE, WHEELING & 2 HESCOM/PTC/WBA-001/ ILKAL & HUNAGUND TALUK, BAGALKOT DISTRICT - REQUEST FOR 02-04-2019 NIL BANKING NIL Running SINGING WHEELING & BANKING AGREEMENT - REGARDING AGREEMENT M/s. THE UGAR SUGAR WORKS LIMITED - 44ME GROSS, 31MW POWER PURCHASE EXPORTABLE DURING SEASON, CO-GEN POWER PLANT AT UGAR 3 HESCOM/PTC/PPA-022/ 29-03-2019 NIL AGREEMENT-CO- NIL Runing KHURD VILLAGE, BELAGAVI DISTRICT - CLARIFICATION REGARDING GENERATION kVARH CHARGES M/s. RENEW SAUR URJA PRIVATE LIMITED - 50MW SOLAR POWER WHEELING & PROJECT @ ITTAGI VILLAGE< HOOVINA HADAGALI TALUK, BELLARY 4 HESCOM/PTC/WBA-016/ 15-03-2019 NIL BANKING NIL Running DIST - CONCURRENCE TO WHEEL ENERGY TO HT INSTALLATION IN AGREEMENT HESCOM JURISDICTION - REG M/s. RAI BAHADUR SETH SHREERAM NARASINGDAS PRIVATE LIMITED WHEELING & - 4.8MW (3.2MW +1.6MW) AT HARTHI, NAGAVI & BELADADI VILLAGES, 5 HESCOM/PTC/WBA-015/ 11-03-2019 NIL BANKING NIL Runing GADAG TALUK & DISTRICT. - REQUEST FOR RENEWAL OF AGREEMENT AGREEMENT AFTER EXPIRY OF TERM - REG M/s. GOLDEN HATCHERIES - 10MW SOLAR POWER PROJECT LOCATED WHEELING & AT LINGASHETTY HALLI VILLAGE, SIRA TALUK, TUMAKURU DISTRICT - 6 HESCOM/PTC/WBA-014/ 07-02-2019 NIL BANKING NIL Running REQUEST BY SLDC FOR PERMISSION TO WHEEL ENERGY TO HT AGREEMENT INSTALLATION IN HESCOM JURISDICTION M/s.