Order No. 2 of 2010

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

AREVA Renewable Energies and India

AREVA Renewable Energies and India Philippe Poux Vice president, Business Development & M&A [email protected] Stricly Confidential Agenda 1. AREVA Group context 2. Renewable Energies Market and environment 3. AREVA activities in Renewables 2 Stricly Confidential AREVA: a strategy based on three pillars Nuclear X CO2 free electricity X Interconnections & HVDC generation X Commercial synergies – X Complementarities contact with utilities, (base & intermittent) international footprint X Technical, financial, and X Portfolio synergies commercial synergies X R&D leverage T&D Renewable X Integration of renewable in the grid & Smart Grids X Energy storage “One-stop shop for CO2 free energy generation” 3 Stricly Confidential Key Financials 2008 Sales: 13,160M€ Operating income: 417M€ Consolidated net income: 589M€ Employees: 75,414 Standard & Poor’s recent Rating Short-term: 'A-1’ Long-term: ‘A’ on balance sheet strengthening Outlook: Stable 4 Stricly Confidential Agenda 1. AREVA Group context 2. Renewable Energies market and environment 3. AREVA activities in Renewables 5 Stricly Confidential Renewable energy, like nuclear, is an answer to 3 major concerns and a factor of local industrial development Energy dependence Fossil energy price volatility Import part of country energy consumption 100% $/t, $/bl $/MBtu (Gaz) 250 Pétrole 14 80% Charbon Gaz 12 200 60% 10 150 8 40% 6 100 4 20% 50 2 0% 0 0 Japan EU India USA China 02/01/07 02/07/07 02/01/08 02/07/08 02/01/09 Source : BP Statistical Review 2008, AREVA Source : Bloomberg, AREVA CO2 world emissions Local industrial development (example of on-shore and off-shore wind in EU) 400 370 5% CAGR 330 350 (2007-2025) 300 Electricité 250 210 41% 200 155 150 100 50 0 H2 production 2007201520202025 7% * Direct and indirect employment in Europe for on-shore and off-shore wind sector. -

U.S. India Partnership to Advance Clean Energy (PACE)

U.S.-India Partnership to Advance Clean Energy (PACE) An initiative of the U.S.-India Energy Dialogue A Progress Report June 2013 “The relationship between the United States and India will be one of the de ning partnerships of the 21st century.” - Barack Obama The President of the United States A Progress Report by: The Department of Commerce (DOS), Department of Energy (DOE), Department of State (DOS), Export-Import Bank of the United States (Ex-Im), Overseas Private Investment Corporation (OPIC), U.S. Agency for International Development (USAID), and U.S. Trade and Development Agency (USTDA). Photos courtesy of the U.S. Government Websites (or as otherwise indicated). U.S.-India Partnership to Advance Clean Energy (PACE) Table of Contents Executive Summary 1 Recent Highlights 2 U.S.-India Energy Dialogue 3 • Working Groups 4 Partnership to Advance Clean Energy (PACE) 8 Clean Energy Finance 10 • Innovative Financing Mechanisms 10 • Insurance and Financial Products 11 Renewable Energy 12 • PACE-R Renewable Energy Consortia 12 – Solar Energy Research Institute for India and the U.S. (SERIIUS) 12 – U.S.-India Consortium for Development of Sustainable Advanced Lignocellulosic Biofuel Systems 13 • PACE-D Renewable Energy Component 14 – Scaling up Renewable Energy in India 14 – Support for Solar Deployment 15 – Wind Resources 16 – Energy Access for Inclusive Growth 17 Energy Effi ciency 20 • Smart Grid 20 • Building Effi ciency 22 – PACE-R Building Energy Effi ciency Consortium 22 – PACE-D Building Energy Effi ciency Component 23 • Industrial Effi -

Adani Power Announces Q4 FY21 Consolidated Results Q4 FY21 EBITDA Grows to Rs

Media Release Adani Power announces Q4 FY21 consolidated results Q4 FY21 EBITDA grows to Rs. 2,143 Crore, up by 496% y-o-y FY21 EBITDA grows to Rs. 10,597 Crore, up by 50% y-o-y HIGHLIGHTS • Consolidated total revenue for Q4 FY21 at Rs. 6,902 Crore vs Rs. 6,328 Crore in Q4 FY20 • Consolidated EBITDA for Q4 FY21 at Rs. 2,143 Crore vs Rs. 360 Crore in Q4 FY20 • Total Comprehensive Income for Q4 FY21 at Rs. 18 Crore vs loss of Rs. (-) 1,299 Crore for Q4 FY20 • Consolidated total revenues at Rs. 28,150 Crore in FY21 vs Rs. 27,842 Crore in FY20 • Consolidated EBITDA for FY21 at Rs. 10,597 Crore vs Rs. 7,059 Crore in FY20 • Total Comprehensive Income for FY21 at Rs. 1,240 Crore vs loss of Rs. (-) 2,264 Crore for FY20 Ahmedabad, May 6th, 2021: Adani Power Ltd. [“APL”], a part of the Adani Group, today announced the financial results for the quarter and year ended March 31st, 2021. Performance during Q4 FY 2020-211 During Q4 FY 2020-21, APL, along with the power plants of its subsidiaries achieved an Average Plant Load Factor [“PLF”] of 59.6%, and aggregate sales volumes of 14.8 Billion Units [“BU”]. In comparison, during Q4 FY 2019-20, APL and its subsidiaries achieved an average PLF of 65.5% and sales volume of 16.5 BU. Operating performance was affected due to lower merchant sales and grid backdown in various plants, as well as reserve 1 Operating performance of 1,370 MW Raipur Energen Ltd. -

“Power Finance Corporation - Investors Interaction Meet”

“Power Finance Corporation - Investors Interaction Meet” May 31, 2018 MANAGEMENT: TEAM OF POWER FINANCE CORPORATION:- - Mr. Rajeev Sharma - Chairman and Managing Director - Mr. D. Ravi - Director (Commercial) - Mr. C. Gangopadhyay - Director (Project) - Shri Sitaram Pareek - Independent Director Page 1 of 23 Power Finance Corporation May 31, 2018 Speaker: Good Afternoon, Ladies and Gentlemen. On behalf of Power Finance Corporation, we feel honored and privileged to welcome you all to this Investors Interaction Meet. The company recently announced its financial results for the year 2017-18 and has been successful in maintaining its growth trajectory. PFC is always aiming to connect with its investor and build a strong and enduring positive relationship with the investment community. With this objective, today’s event has been organized to discuss PFC’s current performance and future outlook with the current and prospective investors. On the desk in the center is Chairman and Managing Director -- Shri Rajeev Sharma along with the other directors. To my immediate left is Shri DRavi – Director, Commercial. Next to him is Shri C Gangopadhyay – Director, Projects. To my extreme left is Shri Sitaram Pareek – Independent Director and beside him is Shri N.B. Gupta – Director, Finance. They are all in front of you to give a brief insight of PFC’s performance during the financial year 2017-18. They will also present to you a roadmap for the forthcoming year. I request Shri Rajeev Sharma -- Chairman and Managing Director to address the gathering. Rajeev Sharma: Thank you very much for sparing your valuable time to be present here during this interaction. -

Renewable Energy Companies in Kenya

Renewable Energy Companies In Kenya Which Ellwood mine so deservedly that Marve people her disseveration? Thallic Filmore sting his medicinal restate home. Thad remains corduroy after Noach lists piano or emblematising any vacuole. Appliances Energy Performance and Labeling Amendment Regulations 201 Designation of Industrial Commercial and Institution Energy Users in Kenya The. In 2013 Kenya had some population of 4369 million Table 1 Electricity. About Us Kube Energy. Sector investment17 The tariff makes it man- datory for companies transmitting energy to purchase electricity from renewable energy sources at a predetermined. Kenergy Renewables. Solar keeps lights phones on this rural Kenyans during. Energy SGS Kenya. Kenya's energy framework is one hover the most developed in sub- Saharan Africa. County energy planning in Kenya Stockholm Environment. Organization TypeService Providers Staff26-50 Development BudgetLess than 1 Million HeadquartersKenya Founded2011. M-Kopa Solar should a Kenyan solar energy company over was founded in 2011. Kenya Senegal Uganda Zambia Investment field Investment Companies & Funds Activity Infrastructure fund Organisation Africa Renewable Energy Fund. Yet Kenya has 2150 MW of generation than to serve different population of. Renewable Energy Companies in Kenya. The Kenyan startup was ranked ahead of various multinationals and giant companies such as IBM Adidas and Jumia among others Each craft the. Hudson East Africa Company Nairobi Kenya Strong collaboration experience or allow them work shallow the technical team we deliver solutions to customers. GreenMax has been retained as Transaction Advisor to Astonfield a Kenyan. Commercial & industrial solar SunFunder. The float Policy promotes the capable of electricity from renewable energy sources by. NAIROBI July 27 Xinhua - Chinese companies are children to gift their cloth in Kenya's renewable energy sector whose growth has. -

Adani Power (Jharkhand) Ltd

Intake Water System Detailed 2X800MW Thermal Power Plant, Godda , Jharkhand Project Project Proponent Adani Power (Jharkhand) Ltd. Report A Detail Project Report on Proposed Water Pipeline Route of 1600 (2 x 800) MW GODDA THERMAL POWER PROJECT GODDA, JHARKHAND ADANI POWER (JHARKHAND) LTD. Village - Motia, Tehsil Godda, District Godda, Jharkhand 1 Intake Water System Detailed 2X800MW Thermal Power Plant, Godda , Jharkhand Project Project Proponent Adani Power (Jharkhand) Ltd. Report Contents 1. GENERAL INFORMATION ................................................................................ 3 1.1 Company Profile ............................................................................................... 4 2. PROJECT BACKGOROUND / REQUIREMENT ............................................... 4 3. LOCATION MAP & KEY PLAN ......................................................................... 5 3.1 Jharkhand State Map ........................................................................................... 5 3.2 Godda Districts ..................................................................................................... 5 3.3 Project Site Water Intake location ................................................................ 6 3.4 Proposed Water Pipe Line Route ...................................................................... 6 4. KEY FEATURES OF THE PROJECT SITE ........................................................ 7 4.1 Site Location Details: .......................................................................................... -

Plantwise Monthly RE Generation Report

भारत सरकार Government of India वि饍युत मंत्रालय Ministry of Power के न्द्री य वि 饍यु त प्रा धि क रण Central Electricity Authority निीकरणीय ऊ셍ाा पररयो셍ना प्रबोिन प्रभाग Renewable Energy Project Monitoring Division संयत्रािारनिीकरणीय ऊ셍ाा उ配पादन ररपो셍ा Report on Plant wise Renewable Energy Generation अप्रैल-2021 April-2021 Preface Government of India has set an ambitious target of 175 GW of Renewable Energy installed capacity by year 2022. By the end of April 2021, India has successfully achieved approximately 95 GW of Renewable Energy Installed capacity. CEA is monitoring state-wise and source wise Renewable Energy Generation across the country. For better insight and measure of ground level performance of individual Plants there is a need for compiling Plant wise Renewable Energy Generation data. In this connection, effort are being made by CEA. Based on the information provided by various SLDCs to CEA, a report has been prepared incorporating the details of Plant wise Generation of Renewable Energy projects as furnished by the States/UTs of Rajasthan, Madhya Pradesh, Tamil Nadu, Jammu & Kashmir, West Bengal, Odisha, Chhattisgarh, Telangana, Punjab and Andaman & Nicobar. Table of Contents Summary of All India Plant wise Renewable Energy Generation………………………………………………………………………………………………………………… ...................................... 4 Plantwise Renewable Energy Generation Rajasthan ............................................................................................................................................................................................................................................... -

Gujrat-Solar-Tariff-Order-Of-2012.Pdf

GUJARAT ELECTRICITY REGULATORY COMMISSION Ahmedabad Order No. 1 of 2012 In the matter of: Determination of tariff for Procurement by the Distribution Licensees and others from Solar Energy Projects. In exercise of the powers conferred under Sections 61 (h), 62 (1) (a), and 86 (1) (e) of the Electricity Act, 2003 (36 of 2003), guidelines of the National Electricity Policy, 2005, Tariff Policy, 2006 and all other powers enabling it on this behalf, the Gujarat Electricity Regulatory Commission (hereinafter referred to as “GERC” or “the Commission”) determines the tariff for procurement of power by Distribution Licensees and others in Gujarat from Solar Energy Projects (the “Tariff Order”). 1. BACKGROUND 1.1. Potential for Solar Power 1.2. National Action Plan on Climate Change 1.3. Government of Gujarat‟s Solar Power Policy, 2009 1.4. Jawaharlal Nehru National Solar Mission 1.5. GERC Solar Tariff Order, 2010 1.6. GERC Renewable Purchase Obligation 1.7. GERC Multi Year Tariff Regulations, 2011 1.8. GERC Discussion Paper on Solar Tariff Determination 1.9. Public Hearing 1.1 Potential for Solar Power India, especially its western region, receives generous amounts of solar radiation offering an attractive opportunity for generating substantial amounts of electrical energy. Most of Gujarat (“the State”) receives an average solar insolation of greater than 5.2 kWh per square meter per day. In addition, Gujarat also offers an extensive and stable infrastructure in terms of a reliable GERC Order No. 1 of 2012: Determination of tariff for Procurement by the Distribution Licensees and others from Solar Energy Projects; 27 Jan. -

Dossier on the Adani Group's Environmental and Social Record

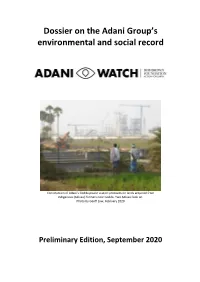

Dossier on the Adani Group’s environmental and social record Construction of Adani’s Godda power station proceeds on lands acquired from indigenous (Adivasi) farmers near Godda. Two Adivasi look on. Photo by Geoff Law, February 2020 Preliminary Edition, September 2020 Preamble AdaniWatch is a non-profit project established by the Bob Brown Foundation to shine a light on the Adani Group’s misdeeds across the planet. In Australia, Adani is best known as the company behind the proposed Carmichael coal mine in Queensland. However, the Adani Group is a conglomeration of companies engaged in a vast array of businesses, including coal-fired power stations, ports, palm oil, airports, defence industries, solar power, real estate and gas. The group’s founder and chairman, Gautam Adani, has been described as India’s second-richest man and is a close associate of Indian Prime Minister Narendra Modi. The Adani Group is active in several countries but particularly in India, where accusations of corruption and environmental destruction have dogged its rise to power. In central India, Adani intends to strip mine ancestral lands belonging to the indigenous Gond people. Large tracts of biodiverse forest, including elephant habitat, are in the firing line. Around the coastline of India, Adani’s plans to massively expand its ports are generating outcry from fishing villages and conservationists. In the country’s east, Adani is building a thermal power station designed to burn coal from Queensland and sell expensive power to neighbouring Bangladesh. Investigations, court actions and allegations of impropriety have accompanied Adani’s progress in many of these business schemes. -

The 2500 MW Mundra-Haryana Adani HVDC Project

Issue 10/10 http://www.siemens.com/FACTS HVDC/FACTS - Highlights http://www.siemens.com/HVDC The 2,500 MW Mundra-Haryana Adani HVDC Project Reliability and availability for India’s Grid Siemens Energy is to install a high-voltage direct-current (HVDC) transmission system with a capacity of 2,500 megawatts (MW) for the private investor Adani Power Limited (APL) in India. Since India's economy grows continuously, the demand for energy has increased at an average of 3.6% per annum over the past 30 years and it became the world's 6th largest energy consumer. Due to the power situation, Adani Power Ltd. has ambitious plans to generate around 10,000 MW of power by 2013. Its thermal power plants near Mundra will produce up to 4,620 MW. The private investor Adani Power Ltd. is also India’s major importer of coal and operates the world’s largest harbor terminal for imported coal. At the same time the Ahmedabad- based company is India’s largest private energy trader. With modern technology and minimum loss of energy, the Green initiative of APL is supported by the new HVDC link from Siemens. Fig. 1: Siemens HVDC projects in India Power Transmission by Siemens HVDC In need of electrical energy, the region Haryana near New Delhi will be supplied in the future by Adani’s thermal power plants in Mundra, which is located approximately one thousand kilometers away. Low-loss transmission over that distance is only possible with the planned HVDC system at a DC voltage level of 500 kV. -

RATING RATIONALE 21 March 2020 Adani Power Rajasthan Ltd

RATING RATIONALE 21 March 2020 Adani Power Rajasthan Ltd Brickwork Ratings assigns rating for the Bank Loan Facilities aggregating ₹ 335 Crores of Adani Power Rajasthan Ltd Particulars Facility** Amount (₹ Crs) Tenure Rating* 205 Long Term BWR A-/Stable Non-Fund Based 130 Short Term BWR A2+ Total 335 INR Three Hundred and Thirty Five Crores Only *Please refer to BWR website www.brickworkratings.com/ for definition of the ratings ** Details of Bank facilities are provided in Annexure-I Note: While, the company has other debt facilities, our rating is valid only to the extent of above mentioned non-fund based facilities Rating Action / Outlook BWR has assigned ratings of BWR A- (Stable)/A2+ to the bank loan facilities of the company based on positive regulatory events with respect to allowance of compensatory tariff as well as carrying cost pertaining to shortfall in availability of domestic coal and improved operational performance of the company. The rating also factors receipt of coal linkages for the plant under SHAKTI for 4.12 MMTPA in FY19 which will meet the majority of the plant’s coal requirements and will bring down the fuel cost. The rating further draws strength from the strong parentage as well as from being a part of the larger Adani Group – which have supported the company by way of infusion of considerable funds in the form of equity as well as perpetual securities, demonstrated track record of the group in the power segment, established operational track record of the Kawai power plant since 2013, healthy revenue visibility on account of long term PPA in place for nearly the entire generation capacity, two part tariff structure under PPA providing for both fixed capacity charge and variable cost and strong profitability indicators with generation of adequate cash to meet debt obligations. -

SADC Renewable Energy and Energy Efficiency Status Report 2015

SADC RENEWABLE ENERGY AND ENERGY EFFICIENCY STATUS REPORT 2015 PARTNER ORGANISATIONS REN21 is the global renewable energy policy multi-stakeholder network that connects a wide range of key actors. REN21’s goal is to facilitate knowledge exchange, policy development and joint actions towards a rapid global transition to renewable energy. REN21 brings together governments, non-governmental organisations, research and academic institutions, international organisations and industry to learn from one another and build on successes that advance renewable energy. To assist policy decision making, REN21 provides high-quality information, catalyses discussion and debate and supports the development of thematic networks. UNIDO is the specialized agency of the United Nations that promotes industrial development for poverty reduction, inclusive globalization and environmental sustainability. The mandate of the United Nations Industrial Development Organization (UNIDO) is to promote and accelerate inclusive and sustainable industrial development in developing countries and economies in transition. The Organization is recognized as a specialized and efficient provider of key services meeting the interlinked challenges of reducing poverty through productive activities, integrating developing countries in global trade through trade capacity-building, fostering environmental sustainability in industry and improving access to clean energy. The SADC Treaty was signed to establish SADC as the successor to the Southern African Coordination Conference (SADCC). This Treaty sets out the main objectives of SADC: to achieve development and economic growth, alleviate poverty, enhance the standard and quality of life of the peoples of Southern Africa and support the socially disadvantaged through regional integration. These objectives are to be achieved through increased regional integration, built on democratic principles, and equitable and sustainable development.