Waste 2020 Market Intelligence Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Survey of Race Relations in South Africa: 1968

A survey of race relations in South Africa: 1968 http://www.aluka.org/action/showMetadata?doi=10.5555/AL.SFF.DOCUMENT.BOO19690000.042.000 Use of the Aluka digital library is subject to Aluka’s Terms and Conditions, available at http://www.aluka.org/page/about/termsConditions.jsp. By using Aluka, you agree that you have read and will abide by the Terms and Conditions. Among other things, the Terms and Conditions provide that the content in the Aluka digital library is only for personal, non-commercial use by authorized users of Aluka in connection with research, scholarship, and education. The content in the Aluka digital library is subject to copyright, with the exception of certain governmental works and very old materials that may be in the public domain under applicable law. Permission must be sought from Aluka and/or the applicable copyright holder in connection with any duplication or distribution of these materials where required by applicable law. Aluka is a not-for-profit initiative dedicated to creating and preserving a digital archive of materials about and from the developing world. For more information about Aluka, please see http://www.aluka.org A survey of race relations in South Africa: 1968 Author/Creator Horrell, Muriel Publisher South African Institute of Race Relations, Johannesburg Date 1969-01 Resource type Reports Language English Subject Coverage (spatial) South Africa, South Africa, South Africa, South Africa, South Africa, Namibia Coverage (temporal) 1968 Source EG Malherbe Library Description A survey of race -

Rates 2017.Xlsx

Facilities with Scales - Schedule of Charges March 2017 Description Charges GENERAL Basic Gate Fee $50 per ton Minimum Gate Fee Charge for Waste $5.00 Recyclable Materials Drop Off No Charge TYPE OF MATERIAL HOUSEHOLD TRASH Up to 200 lbs. minimum Gate Fee $5.00 $0.50 each additional 20 lb. increment or fraction CONSTRUCTION AND DEMOLITION (C&D) C&D with no concrete, recyclables, green waste or chipable wood $50 per ton minimum $5.00 Separated Concrete $25 per ton minimum $5.00 Separated chipable wood $25 per ton minimum $5.00 Mixed C&D (household trash, recyclables, green waste and/or concrete in the load) $175 per ton minimum $5.00 GREEN WASTE Lawn Clippings/Leaves, Up to 400lbs. Minimum Gate Fee $5.00 yard waste, brush, shrubs, $.0.50 each additional 40lb. Increment or fraction trees, branches, woodchips. Tree Stumps $4.00 less than 24" plus Gate Fee $5.00 $12.00 greater than 24" plus Gate Fee $5.00 Mixed Debris (Green waste, household trash,recyclables and/or concrete in the load) $175 per ton minimum $5.00 ANIMALS Small (less than 25 lbs.) $5.00 each + $5.00 Gate Fee Medium (25-200 lbs.) $10.00 each + $5.00 Gate Fee Large (more than 200lbs.) $30.00 each + $5.00 Gate Fee FURNITURE $5.00 minimum Gate Fee plus $4.00 per item ELECTRONIC WASTE No Charge UNIVERSAL WASTE No Charge RESIDENTIAL HOUSEHOLD HAZARDOUS WASTE No Charge COMMERCIAL HAZARDOUS WASTE Not accepted SEPTAGE Inyo $65.00 first 3,000 gallons $42.00 per additional 1,000 gallons or increment Out of County $130.00 first $3,000 gallons $84.00 per addional 1,000 gallons or increment Facilities with Scales - Schedule of Charges March 2017 Description Charges TIRES Auto & light truck $4.00 for 19" rim or less + $5.00 Gate Fee $8.00 for 20" - 24.5" rim + $5.00 Gate Fee Tractor/Heavy Equipment Tire $30 For Up to 100 lbs + $5.00 Gate Fee $40 over 100 lbs. -

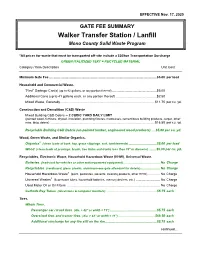

00 Gate Fee Schedule

EFFECTIVE Nov. 17, 2020 GATE FEE SUMMARY Walker Transfer Station / Lanfill Mono County Solid Waste Program *All prices for waste that must be transported off-site include a $20/ton Transportation Surcharge GREEN ITALICIZED TEXT = RECYCLED MATERIAL Category / Item Description Unit Cost Minimum Gate Fee ....................................................................................................................... $5.00 per load Household and Commercial Waste. “First” Garbage Can(s) (up to 82 gallons, or any portion thereof) .................................................. $5.00 Additional Cans (up to 41 gallons each, or any portion thereof) ............................................. $2.50 Mixed Waste, Generally ......................................................................................................... $11.75 per cu. yd. Construction and Demolition (C&D) Waste Mixed Building C&D Debris -- 2 CUBIC YARD DAILY LIMIT (painted wood, furniture, drywall, insulation, plumbing fixtures, mattresses, cementitious building products, carpet, other misc. bldg. debris) ..................................................................................................................... $16.50 per cu. yd. Recyclable Building C&D Debris (un-painted lumber, engineered wood products) …$5.00 per cu. yd. Wood, Green Waste, and Similar Organics. Organics8 (clean loads of bark, hay, grass clippings, sod, tumbleweeds) ............................... $5.00 per load Wood (clean loads of prunings, brush, tree limbs and trunks less than 18” -

Chapter 14 the Economics of Marine Litter

Chapter 14 The Economics of Marine Litter Stephanie Newman, Emma Watkins, Andrew Farmer, Patrick ten Brink and Jean-Pierre Schweitzer Abstract This chapter aims to provide an overview of research into quantifying the economic impacts of marine litter. From an environmental economics perspec- tive it introduces the difficulties in measuring the economic costs of marine litter; reviews those sectors where these costs are notable; and considers policy instru- ments, which can reduce these costs. Marine litter is underpinned by dynamic and complex processes, the drivers and impacts of which are multi-scalar, trans- boundary, and play out in both marine and terrestrial environments. These impacts include economic costs to expenditure, welfare and lost revenue. In most cases, these are not borne by the producers or the polluters. In industries such as fisher- ies and tourism the costs of marine litter are beginning to be quantified and are considerable. In other areas such as impacts on human health, or more intangible costs related to reduced ecosystem services, more research is evidently needed. As the costs of marine litter are most often used to cover removing debris or recov- ering from the damage which they have caused, this expenditure represents treat- ment rather than cure, and although probably cheaper than inaction do not present a strategy for cost reduction. Economic instruments, such as taxes and charges addressing the drivers of waste, for instance those being developed for plastic bags, could be used to reduce the production of marine litter and minimise its impacts. In any case, there remain big gaps in our understanding of the harm caused by marine litter, which presents difficulties when attempting to both quantify its economic costs, and develop effective and efficient instruments to reduce them. -

Nat Onal Directory 01- Nuc Ear Services Atomic Energy Board

.1.'. NAT ONAL DIRECTORY 01- NUC EAR SERVICES ATOMIC ENERGY BOARD Pelindaba PRETORIA Republic of South Africa SEPTEMBER 1974 i i • • i -th"_ S J"!!!, NATIONAL DIRECTORY OF NUCLEAR SERVICES IHKA1A I.-, tin I ,!.n HI !'..• >•> f-'-1 '.!• f'.f('i.jisul'ipt"-.. tt^1 U>l'i i^-viMn nil1, sh .iDpi-.it unini'didli'ly uder linlnim ' I l 1. 'im :'. CJ'I.I'JII1" Genecjl enqumes/fuither copies. The Administrative Officer: Chemistry, Atomic Energy Board. Private Bag X256, PRETORIA 0001 Tel. 79-4441 extension 263 FOREWORD Smilh Afiu\! hjs aheady leached imikHtant milestones in tin' iphrie uf uiu u\i> lei hnn',M;\ Ol'vr l 1 UeveluptMents arc, however, takiny placi which, though nut (is sprLhuulai, aif ni'pu'i.int ,tn<! j\.r I* <',o wtih the dpplicalion of iiULltMr nidtetiu!.. 4uul trclwiK|ut"> 11) nit.'dii-iui , . mills try, . UJI IL'LJ I tin r 1 I'SI ,n 1 !• tU Mindful if thcbc di>vi:lopmi't\ts, the isotopes ,itul R.idiiitinn Cominitlrf nt thr Atumn- Eiii'ni\ Bo.iul on which iii 1.' tupn.'Senh'd all niturustcil parties 111 '.he spheit' nf nuclr.n .ippliCiilon. h.w dividrd U1 I-.MII .1 directory nf nuch;ar scruicns which cun In1 provided. The Committee is fully awnre that the Dnecloiy h..s \\\ liniit.Huni, luasnuiih .l^ it IMH-IS jnuii held and hunce cloes not contain detailed paiticulais wlm'h would luunijlly he loun.l m j i.it.tUiHU/ Ihi- public.iliun of one 01 moie i,f)L'cidli/ed cataku|ues is thus a task fci tlw- liituic. -

Energy Recovery from Sewage Sludge: the Case Study of Croatia

energies Article Energy Recovery from Sewage Sludge: The Case Study of Croatia Dinko Đurđevi´c 1,* , Paolo Blecich 2 and Željko Juri´c 1 1 Energy Institute Hrvoje Požar, 10000 Zagreb, Croatia; [email protected] 2 Faculty of Engineering, University of Rijeka, 51000 Rijeka, Croatia; [email protected] * Correspondence: [email protected] Received: 26 April 2019; Accepted: 16 May 2019; Published: 20 May 2019 Abstract: Croatia produced 21,366 tonnes of dry matter (DM) sewage sludge (SS) in 2016, a quantity expected to surpass 100,000 tonnes DM by 2024. Annual production rates for future wastewater treatment plants (WWTP) in Croatia are estimated at 5.8–7.3 Nm3/people equivalent (PE) for biogas and 20–25 kgDM/PE of sewage sludge. Biogas can be converted into 12–16 kWhel/PE of electricity and 19–24 kWhth/PE of heat, which is sufficient for 30–40% of electrical and 80–100% of thermal autonomy. The WWTP autonomy can be increased using energy recovery from sewage sludge incineration by 60% for electricity and 100% of thermal energy (10–13 kWhel/PE and 30–38 kWhth/PE). However, energy for sewage sludge drying exceeds energy recovery, unless solar drying is performed. 2 The annual solar drying potential is estimated between 450–750 kgDM/m of solar drying surface. The lower heating value of dried sewage sludge is 2–3 kWh/kgDM and this energy can be used for assisting sludge drying or for energy generation and supply to WWTPs. Sewage sludge can be considered a renewable energy source and its incineration generates substantially lower greenhouse gases emissions than energy generation from fossil fuels. -

Overview of Anaerobic Digestion for Municipal Solid Waste

Global Methane Initiative Overview of Anaerobic Digestion for Municipal Solid Waste Updated: October 2016 1 About This Presentation . Introduces the process of anaerobic digestion (AD) for municipal solid waste (MSW) . Provides an overview of anaerobic digestion microbiology . Helps you understand how you might benefit from AD . Guides you through the key areas to consider when developing an AD project . Reviews the status of AD globally and provides selected case studies Using Bookmarks to Navigate This presentation contains bookmarks to help you navigate. Using the panel on the left, click the bookmark to jump to the slide. For Chrome users, the bookmarks can be viewed by clicking on the bookmark icon ( ) at the top right of the screen. 2 Global Methane Initiative GMI is a voluntary, multilateral partnership that aims to reduce global methane emissions and to advance the abatement, recovery and use of methane as a valuable clean energy source. OBJECTIVES BENEFITS . Reduce anthropogenic methane . Decline in methane concentrations emissions and advance the and methane utilization will result recovery and use of methane in: while: – Sustainability – Enhancing economic growth – Energy security – Promoting energy security – Health and safety – Improving local air quality – Profitability and public health. 3 GMI Partners . Grew from 14 to 42 Partner governments, plus the European Commission . Accounts for nearly 70% of global anthropogenic methane emissions 4 Main Menu 1. Introduction – what is AD and why should it interest me? Click here for an introduction to AD 2. Is AD suitable for me? Click here for more info about the potential for AD 3. Step-by-step guide Click here for detailed information about the key issues to consider when developing an AD project 4. -

Biowaste Management in Europe Results of a Pre-Feasibility Report for a Facility for Organic Waste Recycling in South Backa Waste Management District - Serbia

Biowaste Management in Europe Results of a Pre-feasibility report for a facility for organic waste recycling in South Backa Waste Management District - Serbia Marco Ricci - Jürgensen Altereko sas on behalf Abt associates About myself • 20 years of experience in planning MSW management, designing and up¬grading of collection and transport schemes, assessing recycling facilities (focus on composting), planning comunication and participation initiatives, chairing multi-linguistic, multi-tasking working groups or projects. • 15 year foreign working experience as consulting expert focusing on issues related to solid waste management. Extensive consultancy experience in the Solid Waste Sector – on Strategy and Policy, Fees&Taxes, Separate collection schemes - , both in ´advanced´ and ´low to middle income’ countries in Europe, Latin America and Asia. • 10 years experience cooperating with international organisation/agencies (as ECN-European Compost Network, ACRR, EEA- European Environment Agency, Sweepnet-GIZ, SCOW). About myself About myself CIC Italian Composting and Biogas Association Senior Expert www.compost.it ISWA International Solid Waste Association Chair of the Working Group on Biological Treatment of Waste www.iswa.org Ecomondo International Fair Ambassador en.ecomondo.com Activities (outside Italy) Bulgaria Czech Republic Slovak Republic UK Spain Tunisia/Sweep-Net Brazil Cambodia Chile Overview • What is biowaste? • Biological treatment options • From City Assessment to Pre-feasibility investigations • South Backa WMR – scenarios -

Full Scale Co-Digestion of Wastewater Sludge and Food Waste: Bottlenecks and Possibilities

University of Wollongong Research Online Faculty of Engineering and Information Faculty of Engineering and Information Sciences - Papers: Part A Sciences 1-1-2017 Full scale co-digestion of wastewater sludge and food waste: bottlenecks and possibilities Long D. Nghiem University of Wollongong, Technical University of Munich, [email protected] Konrad Koch Technische Universitat Munchen, [email protected] David Bolzonella University of Verona Jörg E. Drewes Technical University of Munich, [email protected] Follow this and additional works at: https://ro.uow.edu.au/eispapers Part of the Engineering Commons, and the Science and Technology Studies Commons Recommended Citation Nghiem, Long D.; Koch, Konrad; Bolzonella, David; and Drewes, Jörg E., "Full scale co-digestion of wastewater sludge and food waste: bottlenecks and possibilities" (2017). Faculty of Engineering and Information Sciences - Papers: Part A. 6423. https://ro.uow.edu.au/eispapers/6423 Research Online is the open access institutional repository for the University of Wollongong. For further information contact the UOW Library: [email protected] Full scale co-digestion of wastewater sludge and food waste: bottlenecks and possibilities Abstract Wastewater treatment plants in many countries use anaerobic digesters for biosolids management and biogas generation. Opportunities exist to utilise the spare capacity of these digesters to co-digest food waste and sludge for energy recovery and a range of other economic and environmental benefits. This paper provides a critical perspective for full-scale implementation of co-digestion of food waste and wastewater sludge. Data compiled from full-scale facilities and the peer-reviewed literature revealed several key bottlenecks hindering full-scale implementation of co-digestion. -

Annexure 1: Restructuring Zones

ANNEXURE 1: RESTRUCTURING ZONES The City has identified 8 restructuring zones. The various zones are constituted by the following areas ZONE A Size Boundaries Suburbs included in the zone 19 085 530 m² Witwatersberg mountain range Sunnyside D.F Malan Drive Pretoria Staatsartillerie Road Salvokop Quagga Road Arcadia Southbound railway line including Salvokop area Pretoria West Elandspoort/Walker Streets to Sunnyside and Arcadia Marabastad boundary line ZONE B Size Boundaries Suburbs included in the zone 40 946 235 N1 highway Silverton m² Stormvoël/Tsamaya Roads Jan Niemand Park N4 highway Weavind Park Simon Vermooten Road Moretele View Nellmapius boundary line Nellmapius Waltloo Silvertondale Lindo Park Bellevue Koedoespoort Eersterust Derdepoort ZONE C Size Boundaries Suburbs included in the zone 43 405 094 Atteridgeville boundary line Atteridgeville m² N4 highway Elandspoort Lotus Gardens boundary line Lotus Gardens Acridian/Kalafong Road Danville Pretoria industrial Proclamation Hill Kwaggasrand Wespark ZONE D Size Boundaries Suburbs included in the zone 32 881 951 Magaliesberg mountain range Capital Park m² DF Malan Drive Roseville Les Marais Witwatersberg mountain range Daspoort Soutpansberg Road Parktown Estate Villeria/Rietondale boundary Mayville Wonderboom South Gezina Villeria Rietfontein Rietondale ZONE E Size Boundaries Suburbs included in the zone 19 880 491 R80/Mabopane Highway Rosslyn m² R566 road Soshanguve South Rosslyn boundary line Klip/Kruisfontein M20 -

Organic Waste Economic Values Analysis Summary Report

Environment Protection Authority Consultancy report: Organic waste economic values analysis Summary report This report has been prepared by consultants for the Environment Protection Authority (EPA) and the views expressed do not necessarily reflect those of the EPA. The EPA cannot guarantee the accuracy of the report, and does not accept liability for any loss or damage incurred as a result of relying on its accuracy. Department of Industry and Trade Environment Protection Agency ORGANIC WASTE ECONOMIC VALUES ANALYSIS SUMMARY REPORT January, 2002 Prepared in association with Access Economics Ref: 3091-01 NOLAN-ITU Pty Ltd ACN 067 785 853 ABN 23 359 240 890 P.O. Box 393 Level 1, 625 High St, East Kew Victoria 3102 Telephone: (03) 9859 3344 Facsimile: (03) 9859 3411 NOLAN-ITU PTY LTD ACN 067 785 853 ABN 23 359 240 890 Melbourne PO Box 393 Level 1, 625 High Street East Kew VIC 3102 Tel: (03) 9859 3344 Fax: (03) 9859 3411 Copyright © Nolan-ITU Pty Ltd 2002 This document is and shall remain the property of Nolan-ITU Pty Ltd. The document may only be used for the purpose for which it was commissioned and in accordance with the terms of engagement for the commission. Unauthorised use of this document in any form whatsoever is prohibited.© Printed on Recycled Paper REF: 3091-01 Document Issue and Status Rev. Status Date Project Manager Reviewer 1-0 Preliminary Draft 18 July 2001 John Nolan Bruno Schacher 1-1 Internal Draft 19 July 2001 John Nolan Sam Bateman 1-2 Draft 10 August 2001 John Nolan Sam Bateman 1-4 Final Draft 13 November 2001 John Nolan Sam Bateman 1-5 Final Draft No. -

INTEGRATED SOLID WASTE MANAGEMENT for LOCAL GOVERNMENTS a Practical Guide

INTEGRATED SOLID WASTE MANAGEMENT FOR LOCAL GOVERNMENTS A Practical Guide Improving solid waste management is crucial for countering public health impacts of uncollected waste and environmental impacts of open dumping and burning. This practical reference guide introduces key concepts of integrated solid waste management and identifi es crosscutting issues in the sector, derived mainly from fi eld experience in the technical assistance project Mainstreaming Integrated Solid Waste Management in Asia. This guide contains over 40 practice briefs covering solid waste management planning, waste categories, waste containers and collection, waste processing and diversion, landfi ll development, landfi ll operations, and contract issues. About the Asian Development Bank ADB’s vision is an Asia and Pacifi c region free of poverty. Its mission is to help its developing member countries reduce poverty and improve the quality of life of their people. Despite the region’s many successes, it remains home to a large share of the world’s poor. ADB is committed to reducing poverty through inclusive economic growth, environmentally sustainable growth, and regional integration. Based in Manila, ADB is owned by members, including from the region. Its main instruments for helping its developing member countries are policy dialogue, loans, equity investments, guarantees, grants, and technical assistance. INTEGRATED SOLID WASTE MANAGEMENT FOR LOCAL GOVERNMENTS A Practical Guide ASIAN DEVELOPMENT BANK 6 ADB Avenue, Mandaluyong City 1550 Metro Manila, Philippines 9 789292 578374 ASIAN DEVELOPMENT BANK www.adb.org Tool Kit for Solid Waste Management in Asian_COVER.indd 1 6/1/2017 5:14:11 PM INTEGRATED SOLID WASTE MANAGEMENT FOR LOCAL GOVERNMENTS A Practical Guide Improving solid waste management is crucial for countering the public health impacts of uncollected waste as well as the environmental impacts of open dumping and burning.