The New Jet Entrants Versus the Regional Partners?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Community Outreach

Truckee Tahoe Airport District COMMUNITY OUTREACH Neighborhood Meetings October 2016 Draft Acknowledgements We wish to thank our supportive community who provided their insight and thoughtful feedback. TRUCKEE TAHOE AIRPORT DISTRICT BOARD AIRPORT COMMUNITY ADVISORY TEAM Lisa Wallace, President Kathryn Rohlf, Community Member/Chair James W. Morrison, Vice President Joe Polverari, Pilot Member/Vice Chair Mary Hetherington Christopher Gage, Pilot Member John B. Jones, Jr. Leigh Golden, Pilot Member J. Thomas Van Berkem Kent Hoopingarner, Community Member/Treasurer Lisa Krueger, Community Member AIRPORT STAFF Kevin Smith, General Manager BRIDGENET INTERNATIONAL Hardy Bullock, Director of Aviation Cindy Gibbs, Airspace Study Project Manager and Community Services Marc R. Lamb, Aviation and FRESHTRACKS COMMUNICATIONS Community Services Manager Seana Doherty, Owner/Founder Michael Cooke, Aviation and Phebe Bell, Facilitator Community Services Manager Amanda Wiebush, Associate Jill McClendon, Aviation and Community Greyson Howard,Mead &Associate Hunt, Inc. M & H Architecture, Inc. Services Program Coordinator 133 Aviation Boulevard, Suite 100 Lauren C. Tapia, District Clerk MEAD & HUNT,Santa INC. Rosa, California 95403 Mitchell Hooper,707-526-5010 West Coast Aviation meadhunt.com Planning Manager Brad Musinski, Aviation Planner Maranda Thompson, Aviation Planner TABLE OF CONTENTS 1 INTRODUCTION AND PROGRAM DESIGN .............................................. 1 2 NEIGHBORHOOD FEEDBACK ..................................................................... 5 APPENDICES A. Meeting Materials B. Public Comments C. Advertising and Marketing Efforts Introduction and ProgramMead & Hunt, Inc. Design M & H Architecture, Inc. 133 Aviation Boulevard, Suite 100 Santa Rosa, California 95403 707-526-5010 meadhunt.com INTRODUCTION Purpose The Truckee Tahoe Airport District (TTAD) understands that community input is incredibly valuable in developing good policies and making sound decisions about Truckee Tahoe Airport (TRK). -

United States Court of Appeals for the DISTRICT of COLUMBIA CIRCUIT

USCA Case #11-1018 Document #1351383 Filed: 01/06/2012 Page 1 of 12 United States Court of Appeals FOR THE DISTRICT OF COLUMBIA CIRCUIT Argued November 8, 2011 Decided January 6, 2012 No. 11-1018 REPUBLIC AIRLINE INC., PETITIONER v. UNITED STATES DEPARTMENT OF TRANSPORTATION, RESPONDENT On Petition for Review of an Order of the Department of Transportation Christopher T. Handman argued the cause for the petitioner. Robert E. Cohn, Patrick R. Rizzi and Dominic F. Perella were on brief. Timothy H. Goodman, Senior Trial Attorney, United States Department of Transportation, argued the cause for the respondent. Robert B. Nicholson and Finnuala K. Tessier, Attorneys, United States Department of Justice, Paul M. Geier, Assistant General Counsel for Litigation, and Peter J. Plocki, Deputy Assistant General Counsel for Litigation, were on brief. Joy Park, Trial Attorney, United States Department of Transportation, entered an appearance. USCA Case #11-1018 Document #1351383 Filed: 01/06/2012 Page 2 of 12 2 Before: HENDERSON, Circuit Judge, and WILLIAMS and RANDOLPH, Senior Circuit Judges. Opinion for the Court filed by Circuit Judge HENDERSON. KAREN LECRAFT HENDERSON, Circuit Judge: Republic Airline Inc. (Republic) challenges an order of the Department of Transportation (DOT) withdrawing two Republic “slot exemptions” at Ronald Reagan Washington National Airport (Reagan National) and reallocating those exemptions to Sun Country Airlines (Sun Country). In both an informal letter to Republic dated November 25, 2009 and its final order, DOT held that Republic’s parent company, Republic Airways Holdings, Inc. (Republic Holdings), engaged in an impermissible slot-exemption transfer with Midwest Airlines, Inc. (Midwest). -

Official Statement

NEW ISSUE—BOOK ENTRY ONLY RATING: See “Rating” In the opinion of Orrick, Herrington & Sutcliffe LLP, Bond Counsel, based upon an analysis of existing laws, regulations, rulings and court decisions and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the Series Twenty-One C Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, except that no opinion is expressed as to the status of interest on any Series Twenty-One C Bond for any period that such Series Twenty-One C Bond is held by a “substantial user” of the facilities refinanced by the Series Twenty- One C Bonds or by a “related person” within the meaning of Section 147(a) of the Internal Revenue Code of 1986. Bond Counsel observes, however, that interest on the Series Twenty-One C Bonds is a specific preference item for purposes of the federal individual and corporate alternative minimum taxes. In the further opinion of Bond Counsel, interest on the Series Twenty-One C Bonds is exempt from personal income taxation by the State of Oregon. Bond Counsel expresses no opinion regarding any other tax consequences related to the ownership or disposition of, or the accrual or receipt of interest on, the Series Twenty-One C Bonds. See “Tax MaTTers.” $27,685,000 THE PORT OF PORTLAND, OREGON Portland International Airport Refunding Revenue Bonds Series Twenty-One C (AMT) Dated: Date of initial delivery Base CUSIP No.: 735240 Due: July 1, as shown on inside cover The Port of Portland (the “Port”) is issuing its Portland International Airport Refunding Revenue Bonds, Series Twenty-One C (AMT) (the “Series Twenty-One C Bonds”) to refund the Port’s outstanding Portland International Airport Refunding Revenue Bonds, Series Fifteen D, to make a deposit to the SLB Reserve Account and to pay costs of issuing the Series Twenty-One C Bonds, all as described herein. -

July/August 2000 Volume 26, No

Irfc/I0 vfa£ /1 \ 4* Limited Edition Collectables/Role Model Calendars at home or in the office - these photo montages make a statement about who we are and what we can be... 2000 1999 Cmdr. Patricia L. Beckman Willa Brown Marcia Buckingham Jerrie Cobb Lt. Col. Eileen M. Collins Amelia Earhart Wally Funk julie Mikula Maj. lacquelyn S. Parker Harriet Quimby Bobbi Trout Captain Emily Howell Warner Lt. Col. Betty Jane Williams, Ret. 2000 Barbara McConnell Barrett Colonel Eileen M. Collins Jacqueline "lackie" Cochran Vicky Doering Anne Morrow Lindbergh Elizabeth Matarese Col. Sally D. Woolfolk Murphy Terry London Rinehart Jacqueline L. “lacque" Smith Patty Wagstaff Florene Miller Watson Fay Cillis Wells While They Last! Ship to: QUANTITY Name _ Women in Aviation 1999 ($12.50 each) ___________ Address Women in Aviation 2000 $12.50 each) ___________ Tax (CA Residents add 8.25%) ___________ Shipping/Handling ($4 each) ___________ City ________________________________________________ T O TA L ___________ S ta te ___________________________________________ Zip Make Checks Payable to: Aviation Archives Phone _______________________________Email_______ 2464 El Camino Real, #99, Santa Clara, CA 95051 [email protected] INTERNATIONAL WOMEN PILOTS (ISSN 0273-608X) 99 NEWS INTERNATIONAL Published by THE NINETV-NINES* INC. International Organization of Women Pilots A Delaware Nonprofit Corporation Organized November 2, 1929 WOMEN PILOTS INTERNATIONAL HEADQUARTERS Box 965, 7100 Terminal Drive OFFICIAL PUBLICATION OFTHE NINETY-NINES® INC. Oklahoma City, -

Adaptive Connected.Xlsx

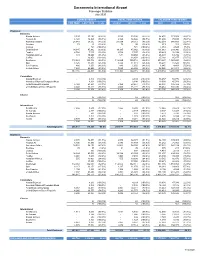

Sacramento International Airport Passenger Statistics July 2020 CURRENT MONTH FISCAL YEAR TO DATE CALENDAR YEAR TO DATE THIS YEAR LAST YEAR % +/(-) 2020/21 2019/20 % +/(-) 2020 2019 % +/(-) Enplaned Domestic Alaska Airlines 3,593 33,186 (89.2%) 3,593 33,186 (89.2%) 54,432 173,858 (68.7%) Horizon Air 6,120 14,826 (58.7%) 6,120 14,826 (58.7%) 31,298 75,723 (58.7%) American Airlines 28,089 54,512 (48.5%) 28,089 54,512 (48.5%) 162,319 348,689 (53.4%) Boutique 79 95 (16.8%) 79 95 (16.8%) 613 201 205.0% Contour - 721 (100.0%) - 721 (100.0%) 4,461 2,528 76.5% Delta Airlines 14,185 45,962 (69.1%) 14,185 45,962 (69.1%) 111,063 233,946 (52.5%) Frontier 4,768 7,107 (32.9%) 4,768 7,107 (32.9%) 25,423 38,194 (33.4%) Hawaiian Airlines 531 10,660 (95.0%) 531 10,660 (95.0%) 26,393 64,786 (59.3%) Jet Blue - 16,858 (100.0%) - 16,858 (100.0%) 25,168 85,877 (70.7%) Southwest 112,869 300,716 (62.5%) 112,869 300,716 (62.5%) 899,647 1,963,253 (54.2%) Spirit 8,425 11,318 (25.6%) 8,425 11,318 (25.6%) 38,294 15,526 146.6% Sun Country 886 1,650 (46.3%) 886 1,650 (46.3%) 1,945 4,401 (55.8%) United Airlines 7,620 46,405 (83.6%) 7,620 46,405 (83.6%) 98,028 281,911 (65.2%) 187,165 544,016 (65.6%) 187,165 544,016 (65.6%) 1,479,084 3,288,893 (55.0%) Commuters Alaska/Skywest - 4,304 (100.0%) - 4,304 (100.0%) 36,457 50,776 (28.2%) American/Skywest/Compass/Mesa - 8,198 (100.0%) - 8,198 (100.0%) 18,030 45,781 (60.6%) Delta/Skywest/Compass 5,168 23,651 (78.1%) 5,168 23,651 (78.1%) 62,894 146,422 (57.0%) United/Skywest/GoJet/Republic 4,040 16,221 (75.1%) 4,040 16,221 (75.1%) -

Southwest Airlines Corporation: a Domestic Industry Analysis & Recommendation for Expansion

University of Tennessee, Knoxville TRACE: Tennessee Research and Creative Exchange Supervised Undergraduate Student Research Chancellor’s Honors Program Projects and Creative Work 5-2006 Southwest Airlines Corporation: A Domestic Industry Analysis & Recommendation for Expansion Joel LaSharon Thomas University of Tennessee-Knoxville Follow this and additional works at: https://trace.tennessee.edu/utk_chanhonoproj Part of the Marketing Commons Recommended Citation Thomas, Joel LaSharon, "Southwest Airlines Corporation: A Domestic Industry Analysis & Recommendation for Expansion" (2006). Chancellor’s Honors Program Projects. https://trace.tennessee.edu/utk_chanhonoproj/1019 This is brought to you for free and open access by the Supervised Undergraduate Student Research and Creative Work at TRACE: Tennessee Research and Creative Exchange. It has been accepted for inclusion in Chancellor’s Honors Program Projects by an authorized administrator of TRACE: Tennessee Research and Creative Exchange. For more information, please contact [email protected]. Southwest Airlines Corporation: A Domestic Industry Analysis & Recommendation for Expansion Joel L. Thomas Chancellor's Honors Program University of Tennessee Senior Project May 2,2006 Joel L. Thomas Senior Honors Project Southwest Airlines May 2, 2006 2 Executive Summary After almost thirty years of service, Southwest Airlines has emerged as one of the world's premier airlines. The Southwest approach to business and the industry at large have enabled the company to continue to grow at profit in times of true economic downturn. Presently, the market for air carriers is saturated and highly fragmented. Overcapacity has led the major United States airlines to compete with Southwest's low fare pricing strategy. However, due to the company's brand image of efficient and effective low fare service, Southwest has been able to ward off its competitors (e.g. -

Overview and Trends

9310-01 Chapter 1 10/12/99 14:48 Page 15 1 M Overview and Trends The Transportation Research Board (TRB) study committee that pro- duced Winds of Change held its final meeting in the spring of 1991. The committee had reviewed the general experience of the U.S. airline in- dustry during the more than a dozen years since legislation ended gov- ernment economic regulation of entry, pricing, and ticket distribution in the domestic market.1 The committee examined issues ranging from passenger fares and service in small communities to aviation safety and the federal government’s performance in accommodating the escalating demands on air traffic control. At the time, it was still being debated whether airline deregulation was favorable to consumers. Once viewed as contrary to the public interest,2 the vigorous airline competition 1 The Airline Deregulation Act of 1978 was preceded by market-oriented administra- tive reforms adopted by the Civil Aeronautics Board (CAB) beginning in 1975. 2 Congress adopted the public utility form of regulation for the airline industry when it created CAB, partly out of concern that the small scale of the industry and number of willing entrants would lead to excessive competition and capacity, ultimately having neg- ative effects on service and perhaps leading to monopolies and having adverse effects on consumers in the end (Levine 1965; Meyer et al. 1959). 15 9310-01 Chapter 1 10/12/99 14:48 Page 16 16 ENTRY AND COMPETITION IN THE U.S. AIRLINE INDUSTRY spurred by deregulation now is commonly credited with generating large and lasting public benefits. -

Appendix C Informal Complaints to DOT by New Entrant Airlines About Unfair Exclusionary Practices March 1993 to May 1999

9310-08 App C 10/12/99 13:40 Page 171 Appendix C Informal Complaints to DOT by New Entrant Airlines About Unfair Exclusionary Practices March 1993 to May 1999 UNFAIR PRICING AND CAPACITY RESPONSES 1. Date Raised: May 1999 Complaining Party: AccessAir Complained Against: Northwest Airlines Description: AccessAir, a new airline headquartered in Des Moines, Iowa, began service in the New York–LaGuardia and Los Angeles to Mo- line/Quad Cities/Peoria, Illinois, markets. Northwest offers connecting service in these markets. AccessAir alleged that Northwest was offering fares in these markets that were substantially below Northwest’s costs. 171 9310-08 App C 10/12/99 13:40 Page 172 172 ENTRY AND COMPETITION IN THE U.S. AIRLINE INDUSTRY 2. Date Raised: March 1999 Complaining Party: AccessAir Complained Against: Delta, Northwest, and TWA Description: AccessAir was a new entrant air carrier, headquartered in Des Moines, Iowa. In February 1999, AccessAir began service to New York–LaGuardia and Los Angeles from Des Moines, Iowa, and Moline/ Quad Cities/Peoria, Illinois. AccessAir offered direct service (nonstop or single-plane) between these points, while competitors generally offered connecting service. In the Des Moines/Moline–Los Angeles market, Ac- cessAir offered an introductory roundtrip fare of $198 during the first month of operation and then planned to raise the fare to $298 after March 5, 1999. AccessAir pointed out that its lowest fare of $298 was substantially below the major airlines’ normal 14- to 21-day advance pur- chase fares of $380 to $480 per roundtrip and was less than half of the major airlines’ normal 7-day advance purchase fare of $680. -

RESOURCE Air Travel 2001

RESOURCE SYSTEMS GROUP INCORPORATED Air Travel 2001 What do they tell us about the future of US air travel? An Industry Report by Resource Systems Group, Inc. December 2001 331 Olcott Drive, White River Junction, Vermont 05001 802.295.4999 www.rsginc.com www.surveycafe.com TABLE OF CONTENTS INTRODUCTION..........................................................................................................................................2 THE SURVEY SAMPLE ..............................................................................................................................2 TRIP CHARACTERISTICS..........................................................................................................................2 RESERVATIONS AND TICKETING............................................................................................................3 CHOICE OF TICKETING LOCATIONS ....................................................................................................3 SATISFACTION WITH TICKETING OPTIONS ........................................................................................4 TICKETING SEGMENTS .........................................................................................................................7 AIRPORTS ..................................................................................................................................................7 AIRLINE RANKINGS.................................................................................................................................12 -

Pinnacle Airlines, Inc. CRJ200 124 CRJ900 16

Forward-Looking Statement The use of words, such as “may”, “might”, “will”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “intends”, “future”, “potential” or “continue”, the negative of these terms and other comparable terminology are intended to identify forward-looking statements. These statements are only predictions based on our current expectations and projections about future events. Because these forward-looking statements involve risks and uncertainties, there are important factors that could cause our actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by the forward-looking statements. In this regard, you should specifically consider the numerous risks outlined in our registration statement in the section entitled, “Risk Factors.” 1 Phil Trenary President and CEO 2 About Pinnacle Airlines Corp. Holding company with two operating subsidiaries: Pinnacle Airlines, Inc. and Colgan Air, Inc. Regional Airline Partnerships with Continental Airlines, Delta Air Lines, Northwest Airlines, United Airlines and US Airways Over 5,000 Employees Current fleet of 138 CRJ200 and 2 CRJ900 next generation regional jets, 42 Saab 340B and 7 Beech 1900D turboprop aircraft 14 additional CRJ900s on order for delivery by February 2009 15 Q-400 next generation turboprops on order. Deliveries start in December 2007, completed by June 30, 2008. 3 Guiding Principles – Pinnacle Airlines Never Compromise Safety Respect for All Pinnacle People We recognize safety as our highest We recognize the value of all People. priority in all aspects of the Airline. We will train our People in the areas of diversity and leadership, giving them the Commitment to Communications tools necessary to ensure relationships We will communicate timely and effectively any are based on the principle of mutual respect. -

Special Rates for Your Group

Special rates for your group. Group travel discounts include: 5% off the lowest applicable fare For reservations, call 1-800-433-1790, and refer to the authorization number below: AN# A8799AQ Now Book your Discount Fares Directly Online To take advantage of a 5% discount on AA, American Eagle and AmericanConnections. It's simple! After you have selected your flight(s) under the "Enter Passenger Details" tab, go to the "AA.com Promotion Code" field and enter in your Authorization Code without the leading “A”. Go directly to www.aa.com to book your flights. Discount Fares are valid for travel on American Airlines, American Eagle®, AmericanConnection®, oneworld Alliance, and codeshare partners from anywhere to your meeting destination. Reservations and Ticketing For reservations and ticketing information, call AmericanAirlines Meeting Services Desk, or have your travel professional call 1-800-433-1790 from anywhere in the United States or Canada, seven days a week, from 6:00 a.m. to 12:00 midnight (Central Time), and reference the authorization number shown above. Reservations for the hearing and speech impaired are also available at 1-800-543-1586. There is a $20.00USD reservations service fee for tickets issued through AA reservations, and a $30.00USD ticketing fee for tickets issued at the airport. Frequent Flyer Miles Earn AAdvantage® miles for your trip. The AAdvantage program was the first airline frequent traveler program, and for more than 20 years has offered members the most innovative ways to earn travel awards. Enroll online at www.aa.com. *Seats are limited. American Airlines, American Eagle, AmericanConnection, American Airlines Group & Meeting Travel and AAdvantage are marks of American Airlines, Inc. -

Flying the Line Flying the Line the First Half Century of the Air Line Pilots Association

Flying the Line Flying the Line The First Half Century of the Air Line Pilots Association By George E. Hopkins The Air Line Pilots Association Washington, DC International Standard Book Number: 0-9609708-1-9 Library of Congress Catalog Card Number: 82-073051 © 1982 by The Air Line Pilots Association, Int’l., Washington, DC 20036 All rights reserved Printed in the United States of America First Printing 1982 Second Printing 1986 Third Printing 1991 Fourth Printing 1996 Fifth Printing 2000 Sixth Printing 2007 Seventh Printing 2010 CONTENTS Chapter 1: What’s a Pilot Worth? ............................................................... 1 Chapter 2: Stepping on Toes ...................................................................... 9 Chapter 3: Pilot Pushing .......................................................................... 17 Chapter 4: The Airmail Pilots’ Strike of 1919 ........................................... 23 Chapter 5: The Livermore Affair .............................................................. 30 Chapter 6: The Trouble with E. L. Cord .................................................. 42 Chapter 7: The Perils of Washington ........................................................ 53 Chapter 8: Flying for a Rogue Airline ....................................................... 67 Chapter 9: The Rise and Fall of the TWA Pilots Association .................... 78 Chapter 10: Dave Behncke—An American Success Story ......................... 92 Chapter 11: Wartime.............................................................................