Presentation Is Made, Or by Reading the 182 Presentation Slides, You Agree to the Following

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

Air Transport in Russia and Its Impact on the Economy

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Tomsk State University Repository Вестник Томского государственного университета. Экономика. 2019. № 48 МИРОВАЯ ЭКОНОМИКА UDC 330.5, 338.4 DOI: 10.17223/19988648/48/20 V.S. Chsherbakov, O.A. Gerasimov AIR TRANSPORT IN RUSSIA AND ITS IMPACT ON THE ECONOMY The study aims to collect and analyse statistics of Russian air transport, show the in- fluence of air transport on the national economy over the period from 2007 to 2016, compare the sector’s role in Russia with the one in other countries. The study reveals the significance of air transport for Russian economy by comparing airlines’ and air- ports’ monetary output to the gross domestic product. On the basis of the research, the policies in the aviation sector can be adjusted by government authorities. Ключевые слова: Russia, aviation, GDP, economic impact, air transport, statistics. Introduction According to Air Transport Action Group, the air transport industry supports 62.7 million jobs globally and aviation’s total global economic impact is $2.7 trillion (approximately 3.5% of the Gross World Product) [1]. Aviation transported 4 billion passengers in 2017, which is more than a half of world population, according to the International Civil Aviation Organization [2]. It makes the industry one of the most important ones in the world. It has a consid- erable effect on national economies by providing a huge number of employment opportunities both directly and indirectly in such spheres as tourism, retail, manufacturing, agriculture, and so on. Air transport is a driving force behind economic connection between different regions because it may entail economic, political, and social effects. -

Presentation

Aeroflot Group Consolidated financials (IFRS) 9M2012 Moscow December 21, 2012 Speaker: Shamil Kurmashov Deputy Director General Finance and investments Table of contents 1.Introduction 2.Market position of the Group 3.Operating highlights 4.Financial results 5.Conclusions 6.Appendix 2 Awards and ratings AEROFLOT GROUP WAS RECOGNIZED AS ONE OF THE LEADING CARRIERS IN EUROPEAN AVIATION SECTOR BY FINANCIAL RESULTS FOR 2011. According to the authoritative international trade magazine Airline Business rating, Aeroflot Group is the third carrier in Europe by net income and among TOP 10 carriers in Europe by revenue. Aeroflot Group is in the 32nd place in 2011 world rankings having moved up two places from 2010. Among 50 most successful global carriers by revenue Aeroflot is the only Russian company. AEROFLOT CONFIRMED STATUS OF THE BEST RUSSIAN AIRLINE FOR BUSINESS-PASSENGERS. Aeroflot once again became a prize winner of Russian Business Travel and MICE awards in nomination “The best airline for business travelers”. Improving service and introducing the most modern technologies to serve our passengers, Aeroflot is rightly seen on the list of the best premium companies of business travelling market. AEROFLOT GAINED LEADING POSITION AMONG SKYTEAM COMPANIES FOR PASSENGER SERVICE. According to InSites Consulting research Aeroflot received the highest passenger appraisal in “Ground service (check-in)” and “On-board service”. The survey was conducted from October 2011 to March 2012 with more than 20 thousand participants – passengers of SkyTeam Alliance airlines. 70% of passengers rated Aeroflot check-in service with excellent marks, 57% rated on-board service with “9” and “10” marks. Passengers’ recognition led Aeroflot to the first place among 15 companies of SkyTeam alliance. -

Ara Ara Ara Ara

,, SCHEDULE 1 (CONT'D) -AIRCRAfT AFFECTED BY THIS AGREEMENT AEROFLOT RUSSIAN AIRLINES- ARA (CONT'D) ARA Airbus A320-214 VP-BWF 2144 ARA Airbus A320-214 VP-BWH 2151 ARA Airbus A320-214 VP-BWI 2163 ARA Airbus A319-111 VP-BWJ 2179 ARA Airbus A320-214 VP-BWM 2233 ARA Airbus A321-211 VP-BWN 2330 ARA Airbus A321-211 VP-BWO 2337 ARA Airbus A321-211 VP-BWP 2342 ARA Airbus A320-214 VP-BQP 2875 ARA Airbus A320-214 VP-BQV 2920 ARA Airbus A320-214 VP-BQW 2947 ARA Airbus A321-211 VP-BQR 2903 ARA Airbus A321-211 VP-BQS 2912 ARA Airbus A321-211 VP-BQT 2965 ARA AirbusA321-211 VP-BQX 2957 ARA Airbus A321-211 VP-BRW 3191 ARA Airbus A321-211 VP-BOC 5720 ARA AirbusA321-211 VP-BOE 5755 ARA Airbus A321-211 VP-BTG 5790 ARA Airbus A321-211 VP-BTL 5881 ARA AirbusA321-211 VP-BTR 5913 Date: 20 March 2014 Page2 SCHEDULE 1 (CONT'D) .. AIRCRAFT AFFECTED BY THIS AGREEMENT "AURORA Airlines" JSC AURORA Airbus A319-111 VP-BWK 2222 AURORA Airbus A319-111 VP-BWL 2243 AURORA Airbus A319-111 VP-BUK 3281 AURORA Airbus A319-111 VP-BUN 3298 AURORA Airbus A319-111 VP-BUO 3336 Date: 20 March 2014 Page41 SCHEDULE 1 (CONT'D) -AIRCRAFT AFFECTED BY THIS AGREEMENT YAKUTIAAIR YAKUTIA Boeing 757-256 VP-BFG 26244 YAKUTIA Boeing 757 -23N VQ-BCF 27874 YAKUTIA Boeing 757-256 VQ-BCK 26245 YAKUTIA Boeing 737-76Q VQ-BEO 30293 YAKUTIA Boeing 757 -23N VQ-BMW 29330 YAKUTIA Boeing 737 -85F VQ-BOY 28825 YAKUTIA Boeing 737-86N VQ-BMP 28617 YAKUTIA Boeing 757 -23APF VQ-BOX 24868 YAKUTIA Boeing 737-700 VQ-BLS 30277 YAKUTIA Boeing 737-76Q VQ-BLT 30271 YAKUTIA Boeing 737-8Q8 VP-BEP 32797 YAKUTIA Boeing 737-7Q8 VP-BIB 30642 YAKUTIA Boeing 737 -7L9 VP-BSP 28009 YAKUTIA Bombardier DHG-8-402 VP-BKD 4162 YAKUTIA Bombardier DHG-8-402 VP-BNU 4171 YAKUTIA Bombardier DHC-8-402 VP-BOS 4159 YAKUTIA Bombardier DHC-8-402 VP-BOV 4017. -

Tupolev TU-204-100/ -300/ TU-214 Sorting: Serial Nr

Tupolev TU-204-100/ -300/ TU-214 Sorting: Serial Nr. 15.07.2021 Ser.Nr. Type F/F Status Immatr. Operator Last Operator in service Engines Owner Rem. @airlinefleet.info M/Y until 1450741064019 TU-204-100 1993 stored RA-64019 none Red Wings 03-2014 Perm PS-90A 1450741164004 TU-204-100 1991 broken up RA-64004 none Producer/Prototype 08-2005 Perm PS-90A broken up by 12-2010 1450741264007 TU-204-100C 1991 perm_wfu RA-64007 none Aeroflot Russian Airlines 08-2001 Perm PS-90A 1450741364011 TU-204-100 1993 accidented RA-64011 none Sibir Airlines 03-2010 Perm PS-90A crashed on landing Moscow-Domodedov 1450741364024 TU-204-120C 1999 in service RA-64024 Aviastar - TU Air 07-2005 Perm PS-90A 1450741464015 TU-204-100 1993 stored RA-64015 none Rossiya GTK 08-2001 Perm PS-90A to Aviastar for re-work/modernisation 1450741564039 TU-204-300 2005 stored RA-64039 none Vladivostok Air 10-2013 Perm PS-90A VIP-configurated 1450741864044 TU-204-300 2008 in service RA-64044 Roskosmos 05-2019 Perm PS-90A RKK Energy 1450741964018 TU-204-100 1993 perm_wfu RA-64018 none Red Wings 10-2017 Perm PS-90A 1450741964048 TU-204-100 2009 in service P-633 Air Koryo 03-2010 Perm PS-90A 1450741964050 TU-204-100 2009 stored RA-64050 none Red Wings 11-2018 Perm PS-90A 1450742064022 TU-204-100 1999 stored RA-64022 none Red Wings 09-2013 Perm PS-90A 1450742264032 TU-204-120C 2001 in service RA-64032 Aviastar - TU Air 07-2008 Perm PS-90A 1450742364012 TU-204-300 1993 in service P-632 Air Koryo 12-2007 Perm PS-90A conv.from vers.100 in vers.300 2007 1450742564017 TU-204-100 1993 in -

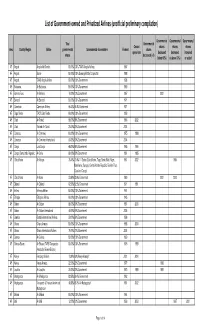

List of Government-Owned and Privatized Airlines (Unofficial Preliminary Compilation)

List of Government-owned and Privatized Airlines (unofficial preliminary compilation) Governmental Governmental Governmental Total Governmental Ceased shares shares shares Area Country/Region Airline governmental Governmental shareholders Formed shares operations decreased decreased increased shares decreased (=0) (below 50%) (=/above 50%) or added AF Angola Angola Air Charter 100.00% 100% TAAG Angola Airlines 1987 AF Angola Sonair 100.00% 100% Sonangol State Corporation 1998 AF Angola TAAG Angola Airlines 100.00% 100% Government 1938 AF Botswana Air Botswana 100.00% 100% Government 1969 AF Burkina Faso Air Burkina 10.00% 10% Government 1967 2001 AF Burundi Air Burundi 100.00% 100% Government 1971 AF Cameroon Cameroon Airlines 96.43% 96.4% Government 1971 AF Cape Verde TACV Cabo Verde 100.00% 100% Government 1958 AF Chad Air Tchad 98.00% 98% Government 1966 2002 AF Chad Toumai Air Tchad 25.00% 25% Government 2004 AF Comoros Air Comores 100.00% 100% Government 1975 1998 AF Comoros Air Comores International 60.00% 60% Government 2004 AF Congo Lina Congo 66.00% 66% Government 1965 1999 AF Congo, Democratic Republic Air Zaire 80.00% 80% Government 1961 1995 AF Cofôte d'Ivoire Air Afrique 70.40% 70.4% 11 States (Cote d'Ivoire, Togo, Benin, Mali, Niger, 1961 2002 1994 Mauritania, Senegal, Central African Republic, Burkino Faso, Chad and Congo) AF Côte d'Ivoire Air Ivoire 23.60% 23.6% Government 1960 2001 2000 AF Djibouti Air Djibouti 62.50% 62.5% Government 1971 1991 AF Eritrea Eritrean Airlines 100.00% 100% Government 1991 AF Ethiopia Ethiopian -

Receipts Collected for the Quarter Ended September 30, 2019 (Application No

PFC Quarterly Report - Receipts Collected For the Quarter Ended September 30, 2019 (Application No. 2) Application #05-02-C-00-ANC $14,000,000.00 Application #05-02-C-01-ANC 71,000,000.00 Total Collection Authority $85,000,000.00 PFC Revenue Received Air Carriers Current Quarter Previous Quarters Cumulative Aer Lingus $ 132.94 $ 1,173.41 $ 1,306.35 Aeroflot - Russian Airline 80.26 1,584.96 1,665.22 Aerolane Lineas Aereas Nacionale - 135.83 135.83 AeroMexico 196.52 5,895.60 6,092.12 Aerovias De Mexico - 491.30 491.30 Air Canada 16,771.01 576,696.64 593,467.65 Air France 174.56 15,411.14 15,585.70 Air New Zealand 96.72 6,885.31 6,982.03 Air Pacific Limited DBA Fiji Airways - 1,442.11 1,442.11 Air Serbia, Inc. 11.56 23.12 34.68 Air Tahiti - 31.79 31.79 Alaska Airlines Inc 984,852.33 40,002,650.48 40,987,502.81 Alitalia Airlines 8.67 352.58 361.25 Alitalia Societa Aerea Italiana S.P.A. - 26.01 26.01 Allegiant Air, Inc. 4,392.80 5,340.72 9,733.52 All Nippon Airways Co Ltd 189.09 4,340.73 4,529.82 Aloha Airlines - 86.37 86.37 America West Airlines - 180,410.15 180,410.15 American Airlines 36,881.55 1,882,599.77 1,919,481.32 American Trans Air - 459.07 459.07 Asiana Airlines 1,259.85 47,577.28 48,837.13 Austrian Airlines AG 11.34 1,923.95 1,935.29 Aviacion Commercial Del America - 5.78 5.78 Avianca Inc 72.25 3,113.32 3,185.57 Big Sky Airlines - 20.23 20.23 British Airways 552.78 23,098.12 23,650.90 Brussels 14.45 170.51 184.96 Cape Air - 40.46 40.46 Cape Smythe Air Service, Inc - 8.67 8.67 Cathay Pacific Airways Ltd 554.77 12,396.54 12,951.31 Champion Air - 367.03 367.03 China Airlines 20.23 156,763.27 156,783.50 Compania Panamena DE Aviacion S.A. -

CHANGE FEDERAL AVIATION ADMINISTRATION CHG 2 Air Traffic Organization Policy Effective Date: November 8, 2018

U.S. DEPARTMENT OF TRANSPORTATION JO 7340.2H CHANGE FEDERAL AVIATION ADMINISTRATION CHG 2 Air Traffic Organization Policy Effective Date: November 8, 2018 SUBJ: Contractions 1. Purpose of This Change. This change transmits revised pages to Federal Aviation Administration Order JO 7340.2H, Contractions. 2. Audience. This change applies to all Air Traffic Organization (ATO) personnel and anyone using ATO directives. 3. Where Can I Find This Change? This change is available on the FAA website at http://faa.gov/air_traffic/publications and https://employees.faa.gov/tools_resources/orders_notices. 4. Distribution. This change is available online and will be distributed electronically to all offices that subscribe to receive email notification/access to it through the FAA website at http://faa.gov/air_traffic/publications. 5. Disposition of Transmittal. Retain this transmittal until superseded by a new basic order. 6. Page Control Chart. See the page control chart attachment. Original Signed By: Sharon Kurywchak Sharon Kurywchak Acting Director, Air Traffic Procedures Mission Support Services Air Traffic Organization Date: October 19, 2018 Distribution: Electronic Initiated By: AJV-0 Vice President, Mission Support Services 11/8/18 JO 7340.2H CHG 2 PAGE CONTROL CHART Change 2 REMOVE PAGES DATED INSERT PAGES DATED CAM 1−1 through CAM 1−38............ 7/19/18 CAM 1−1 through CAM 1−18........... 11/8/18 3−1−1 through 3−4−1................... 7/19/18 3−1−1 through 3−4−1.................. 11/8/18 Page Control Chart i 11/8/18 JO 7340.2H CHG 2 CHANGES, ADDITIONS, AND MODIFICATIONS Chapter 3. ICAO AIRCRAFT COMPANY/TELEPHONY/THREE-LETTER DESIGNATOR AND U.S. -

Anchorage, Alaska PFC Quarterly Report - Receipts Collected for the Quarter Ended September 30, 2010 (Application No

TED STEVENS ANCHORAGE INTERNATIONAL AIRPORT Anchorage, Alaska PFC Quarterly Report - Receipts Collected For the Quarter Ended September 30, 2010 (Application No. 1 ) Application #99-01-C-00-ANC & 99-01-C-01-ANC $22,000,000.00 0.00 Total Collection Authority $22,000,000.00 PFC Revenue Received Air Carriers Current Quarter Previous Quarters Cumulative Aces Airlines $ 32.12 $ 32.12 Aer Lingus 317.44 317.44 Aerovias De Mexico 122.58 122.58 Aero Mexico 98.53 98.53 Air Canada 136,476.21 136,476.21 Air France 1,764.99 1,764.99 Air New Zealand 2,094.33 2,094.33 Air Pacific 8.67 8.67 Airlines Services Corporation 37.96 37.96 Air Wisconsin Airlines 46.54 46.54 Alaska Airlines 11,024,874.06 11,024,874.06 Alitalia Airlines 1,051.51 1,051.51 All Nippon Airways Co 1,905.64 1,905.64 Aloha Airlines 7,152.82 7,152.82 America Central Corp 23.36 23.36 America West Airlines 228,474.04 228,474.04 American Airlines 509,508.22 509,508.22 American Trans Air 6,513.14 6,513.14 Asiana Airlines 2,125.95 2,125.95 Atlantic Coast Airline 96.36 96.36 Avianca 8.76 8.76 Big Sky Airlines 87.36 87.36 British Airways 12,272.36 12,272.36 Canada 3000 10,999.72 10,999.72 Cathay Pacific Airways 271.27 271.27 China Airlines 78,473.09 78,473.09 Condor Flugdienst, GMBH 63,889.95 63,889.95 Continental Airlines 1,380,859.31 1,380,859.31 Czech Airlines 348.36 348.36 Delta Airlines 1,673,182.33 1,673,182.33 Elal Israel Airlines 110.74 110.74 Emirates 14.57 14.57 Era Aviation, Inc. -

INVESTOR PRESENTATION June 2014

AEROFLOT – RUSSIAN AIRLINES INVESTOR PRESENTATION June 2014 \\IBLNS003VF\EAST2013\03 Presentations\Graphics\Template\01 Aeroflot Cover.psd Disclaimer 0/58/129 This communication has been prepared by and is the sole responsibility of the issuer that is the subject of this communication. This communication 148/190/224 is provided for information purposes only. Any offering of any security or other financial instrument that may be related to the subject matter of this communication (a “financial instrument”) will be made pursuant to separate and distinct documentation (an “offering circular”) and in such case the information contained herein will be superseded in its entirety by any such offering circular in its final form. In addition, because this communication is a summary only, it may not contain all material terms and this communication in and of itself should not form the basis for any investment decision. 119/119/119 The information and opinions herein is believed to be reliable and has been obtained from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to the fairness, correctness, accuracy reasonableness or completeness of the information and opinions. There is no obligation to update, modify or amend this communication or to otherwise notify the recipient if information, opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate. 79/115/160 The recipient is strongly advised to seek their own independent advice in relation to any investment, financial, legal, tax, accounting or regulatory issues discussed herein. Nothing contained herein shall constitute any representation or warranty as to future performance of any financial instrument, credit, currency, rate or other market or economic measure. -

AIR TRANSPORT in RUSSIA and ITS IMPACT on the ECONOMY © 2020 Oleg A, Gerasimov

AIR TRANSPORT IN RUSSIA AND ITS IMPACT ON THE ECONOMY © 2020 Oleg A, Gerasimov. All rights reserved. 1. INTRODUCTION 2 Global Aviation Industry in 2019 3 4.3 billion passengers That’s more than half of global population $2.7 trillion economic impact It is 3.6% of world GDP, equal to the United Kingdom economy. 65.5 million jobs supported 4 times more than total number of employed people in Canada Source: Aviation Benefits Report 2019 - Industry High Level Group on behalf of ICAO 4 Air transport impact on an economy United States of America China France ▷ 4.2% of GDP ▷ 0.93% of GDP ▷ 4.3% of GDP ▷ 6.5M jobs supported by air ▷ 6M jobs supported by air ▷ 1.1M jobs supported by air transport sector transport sector transport sector ▷ $779 billion GVA ▷ $104 billion GVA ▷ $105 billion GVA contribution to GDP contribution to GDP contribution to GDP What about Russia?... Note: GVA – Gross Value Added; GDP – Gross Domestic Product Source: Aviation Benefits Beyond Borders Reports 2018 5 The purpose is to estimate the influence of air transport industry on the economy of Russia so as to understand the importance of the aviation sphere for the country 6 The way to findings Review of literature Methodology Calculations Academic journals, On the basis of Oxford Data from official books, technical Economics and United financial reports, reports, working Nations ones pro.fira.ru, SPARK- papers Interfax, disclosure.ru, e-disclosure.ru 7 2. METHODOLOGY 8 What is implied by air transport sector? ▪ Airlines – Companies that provide transport for people and freight ▪ Ground-based infrastructure – Organizations that provide facilities for airlines and services for people and freight. -

ANC PFC 4Th Quarterly Report Ending Jun 30, 2019.Xlsx

PFC Quarterly Report - Receipts Collected For the Quarter Ended September 30, 2018 (Application No. 2) Application #05-02-C-00-ANC $14,000,000.00 Application #05-02-C-01-ANC 71,000,000.00 Total Collection Authority $85,000,000.00 PFC Revenue Received Air Carriers Current Quarter Previous Quarters Cumulative Aer Lingus 234.09 $ 312.19 $ 546.28 Aeroflot - Russian Airline 75.14 1,189.14 1,264.28 Aerolane Lineas Aereas Nacionale - 124.27 124.27 AeroMexico - 5,649.95 5,649.95 Aerovias De Mexico 135.83 355.47 491.30 Air Canada 15,634.96 507,376.34 523,011.30 Air France 370.78 14,341.19 14,711.97 Air New Zealand 48.58 6,233.24 6,281.82 Air Pacific Limited DBA Fiji Airways- 1,442.11 1,442.11 Air Serbia, Inc. 2.89 20.23 23.12 Air Tahiti - 31.79 31.79 Alaska Airlines Inc 951,280.44 35,846,266.88 36,797,547.32 Alitalia Airlines 8.67 343.91 352.58 Alitalia Societa Aerea Italiana S.P.A. - 23.12 23.12 Allegian Air, Inc. - 127.16 127.16 All Nippon Airways Co Ltd 129.72 3,363.77 3,493.49 Aloha Airlines - 86.37 86.37 America West Airlines - 180,410.15 180,410.15 American Airlines 39,826.07 1,719,992.50 1,759,818.57 American Trans Air - 459.07 459.07 Asiana Airlines 964.52 42,115.64 43,080.16 Austrian Airlines AG 2.89 1,897.94 1,900.83 Aviacion Commercial Del America - 5.78 5.78 Avianca Inc 156.06 2,541.10 2,697.16 Big Sky Airlines - 20.23 20.23 British Airways 432.68 20,992.66 21,425.34 Brussels 5.78 156.06 161.84 Cape Air - 40.46 40.46 Cape Smythe Air Service, Inc - 8.67 8.67 Cathay Pacific Airways Ltd 301.50 11,062.23 11,363.73 Champion Air - 367.03