Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Aurora Airlines to Launch New Charter Service Between Narita and Yuzhno-Sakhalinsk!

[Joint Press Release] Aurora Airlines (UTS Air Service Inc.) Narita International Airport Corporation Aurora Airlines to Launch New Charter Service between Narita and Yuzhno-Sakhalinsk! Tokyo, 15 April 2014: We are delighted to announce the launch of a new charter service between Narita and Yuzhno-Sakhalinsk to be operated by Aurora Airlines (IATA Code: HZ) from Thursday, 1 May 2014. Aurora Airlines was established in September 2013 by amalgamating SAT Airlines and Vladivostok Air. It operates domestic services within Russia between Yuzhno-Sakhalinsk and major cities in the Russian Far East, while operating international services from Yuzhno-Sakhalinsk to 3 countries including the Narita route. Yuzhno-Sakhalinsk, the capital of the state of Sakhalin in Russia is located two and a half hours away from Narita by air, and is a key economic and cultural center and as the base for large-scale underground resource development projects by joint ventures comprising firms from Japan, Russia, Europe and the US. The launch of this new Aurora Airlines service will stimulate greater exchanges between Japan and the Russian Far East region. Flight Schedule: 2 flights/week (Tue, Thu) from 1 May 2014 Flight Departure STD Arrival STA Outbound HZ9234 Narita 16:30 Y-Sakhalinsk 21:00 Inbound HZ9233 Y-Sakhalinsk 13:05 Narita 13:50 * All times local Terminal: Terminal 1, North Wing Aircraft: Boeing B737-500 Seating Capacity: 108 in total (8 Business Class, 100 Economy Class) * Conditional upon approval by the relevant governments. Schedule and other details are subject to change without notice. *Courtesy of Aurora Airlines . -

Air Transport in Russia and Its Impact on the Economy

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Tomsk State University Repository Вестник Томского государственного университета. Экономика. 2019. № 48 МИРОВАЯ ЭКОНОМИКА UDC 330.5, 338.4 DOI: 10.17223/19988648/48/20 V.S. Chsherbakov, O.A. Gerasimov AIR TRANSPORT IN RUSSIA AND ITS IMPACT ON THE ECONOMY The study aims to collect and analyse statistics of Russian air transport, show the in- fluence of air transport on the national economy over the period from 2007 to 2016, compare the sector’s role in Russia with the one in other countries. The study reveals the significance of air transport for Russian economy by comparing airlines’ and air- ports’ monetary output to the gross domestic product. On the basis of the research, the policies in the aviation sector can be adjusted by government authorities. Ключевые слова: Russia, aviation, GDP, economic impact, air transport, statistics. Introduction According to Air Transport Action Group, the air transport industry supports 62.7 million jobs globally and aviation’s total global economic impact is $2.7 trillion (approximately 3.5% of the Gross World Product) [1]. Aviation transported 4 billion passengers in 2017, which is more than a half of world population, according to the International Civil Aviation Organization [2]. It makes the industry one of the most important ones in the world. It has a consid- erable effect on national economies by providing a huge number of employment opportunities both directly and indirectly in such spheres as tourism, retail, manufacturing, agriculture, and so on. Air transport is a driving force behind economic connection between different regions because it may entail economic, political, and social effects. -

Aviation Week & Space Technology

STARTS AFTER PAGE 34 How Air Trvel New Momentum for My Return Smll Nrrowbodies? ™ $14.95 APRIL 20-MAY 3, 2020 SUSTAINABLY Digital Edition Copyright Notice The content contained in this digital edition (“Digital Material”), as well as its selection and arrangement, is owned by Informa. and its affiliated companies, licensors, and suppliers, and is protected by their respective copyright, trademark and other proprietary rights. Upon payment of the subscription price, if applicable, you are hereby authorized to view, download, copy, and print Digital Material solely for your own personal, non-commercial use, provided that by doing any of the foregoing, you acknowledge that (i) you do not and will not acquire any ownership rights of any kind in the Digital Material or any portion thereof, (ii) you must preserve all copyright and other proprietary notices included in any downloaded Digital Material, and (iii) you must comply in all respects with the use restrictions set forth below and in the Informa Privacy Policy and the Informa Terms of Use (the “Use Restrictions”), each of which is hereby incorporated by reference. Any use not in accordance with, and any failure to comply fully with, the Use Restrictions is expressly prohibited by law, and may result in severe civil and criminal penalties. Violators will be prosecuted to the maximum possible extent. You may not modify, publish, license, transmit (including by way of email, facsimile or other electronic means), transfer, sell, reproduce (including by copying or posting on any network computer), create derivative works from, display, store, or in any way exploit, broadcast, disseminate or distribute, in any format or media of any kind, any of the Digital Material, in whole or in part, without the express prior written consent of Informa. -

Change 3, FAA Order 7340.2A Contractions

U.S. DEPARTMENT OF TRANSPORTATION CHANGE FEDERAL AVIATION ADMINISTRATION 7340.2A CHG 3 SUBJ: CONTRACTIONS 1. PURPOSE. This change transmits revised pages to Order JO 7340.2A, Contractions. 2. DISTRIBUTION. This change is distributed to select offices in Washington and regional headquarters, the William J. Hughes Technical Center, and the Mike Monroney Aeronautical Center; to all air traffic field offices and field facilities; to all airway facilities field offices; to all international aviation field offices, airport district offices, and flight standards district offices; and to the interested aviation public. 3. EFFECTIVE DATE. July 29, 2010. 4. EXPLANATION OF CHANGES. Changes, additions, and modifications (CAM) are listed in the CAM section of this change. Changes within sections are indicated by a vertical bar. 5. DISPOSITION OF TRANSMITTAL. Retain this transmittal until superseded by a new basic order. 6. PAGE CONTROL CHART. See the page control chart attachment. Y[fa\.Uj-Koef p^/2, Nancy B. Kalinowski Vice President, System Operations Services Air Traffic Organization Date: k/^///V/<+///0 Distribution: ZAT-734, ZAT-464 Initiated by: AJR-0 Vice President, System Operations Services 7/29/10 JO 7340.2A CHG 3 PAGE CONTROL CHART REMOVE PAGES DATED INSERT PAGES DATED CAM−1−1 through CAM−1−2 . 4/8/10 CAM−1−1 through CAM−1−2 . 7/29/10 1−1−1 . 8/27/09 1−1−1 . 7/29/10 2−1−23 through 2−1−27 . 4/8/10 2−1−23 through 2−1−27 . 7/29/10 2−2−28 . 4/8/10 2−2−28 . 4/8/10 2−2−23 . -

Ara Ara Ara Ara

,, SCHEDULE 1 (CONT'D) -AIRCRAfT AFFECTED BY THIS AGREEMENT AEROFLOT RUSSIAN AIRLINES- ARA (CONT'D) ARA Airbus A320-214 VP-BWF 2144 ARA Airbus A320-214 VP-BWH 2151 ARA Airbus A320-214 VP-BWI 2163 ARA Airbus A319-111 VP-BWJ 2179 ARA Airbus A320-214 VP-BWM 2233 ARA Airbus A321-211 VP-BWN 2330 ARA Airbus A321-211 VP-BWO 2337 ARA Airbus A321-211 VP-BWP 2342 ARA Airbus A320-214 VP-BQP 2875 ARA Airbus A320-214 VP-BQV 2920 ARA Airbus A320-214 VP-BQW 2947 ARA Airbus A321-211 VP-BQR 2903 ARA Airbus A321-211 VP-BQS 2912 ARA Airbus A321-211 VP-BQT 2965 ARA AirbusA321-211 VP-BQX 2957 ARA Airbus A321-211 VP-BRW 3191 ARA Airbus A321-211 VP-BOC 5720 ARA AirbusA321-211 VP-BOE 5755 ARA Airbus A321-211 VP-BTG 5790 ARA Airbus A321-211 VP-BTL 5881 ARA AirbusA321-211 VP-BTR 5913 Date: 20 March 2014 Page2 SCHEDULE 1 (CONT'D) .. AIRCRAFT AFFECTED BY THIS AGREEMENT "AURORA Airlines" JSC AURORA Airbus A319-111 VP-BWK 2222 AURORA Airbus A319-111 VP-BWL 2243 AURORA Airbus A319-111 VP-BUK 3281 AURORA Airbus A319-111 VP-BUN 3298 AURORA Airbus A319-111 VP-BUO 3336 Date: 20 March 2014 Page41 SCHEDULE 1 (CONT'D) -AIRCRAFT AFFECTED BY THIS AGREEMENT YAKUTIAAIR YAKUTIA Boeing 757-256 VP-BFG 26244 YAKUTIA Boeing 757 -23N VQ-BCF 27874 YAKUTIA Boeing 757-256 VQ-BCK 26245 YAKUTIA Boeing 737-76Q VQ-BEO 30293 YAKUTIA Boeing 757 -23N VQ-BMW 29330 YAKUTIA Boeing 737 -85F VQ-BOY 28825 YAKUTIA Boeing 737-86N VQ-BMP 28617 YAKUTIA Boeing 757 -23APF VQ-BOX 24868 YAKUTIA Boeing 737-700 VQ-BLS 30277 YAKUTIA Boeing 737-76Q VQ-BLT 30271 YAKUTIA Boeing 737-8Q8 VP-BEP 32797 YAKUTIA Boeing 737-7Q8 VP-BIB 30642 YAKUTIA Boeing 737 -7L9 VP-BSP 28009 YAKUTIA Bombardier DHG-8-402 VP-BKD 4162 YAKUTIA Bombardier DHG-8-402 VP-BNU 4171 YAKUTIA Bombardier DHC-8-402 VP-BOS 4159 YAKUTIA Bombardier DHC-8-402 VP-BOV 4017. -

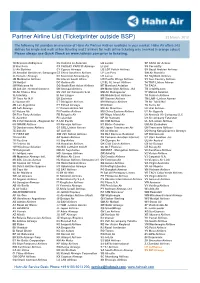

Airlines List in Outside

Partner Airline List (Ticketprinter outside BSP) 23 March, 2012 The following list provides an overview of Hahn Air Partner Airlines available in your market. Hahn Air offers 243 airlines for single and multi airline ticketing and 2 airlines for multi airline ticketing only (marked in orange colour). Please always use Quick Check on www.hahnair.com prior to ticketing. 1X Branson AirExpress CU Cubana de Aviacion LG Luxair SP SATA Air Acores 2I Star Perú CX CATHAY PACIFIC Airways LI Liat SS Corsairfly 2J Air Burkina CY Cyprus Airways LO LOT Polish Airlines SV Saudi Arabian Airlines 2K AeroGal Aerolineas Galapagos CZ China Southern Airlines LP Lan Peru SW Air Namibia 2L Helvetic Airways D2 Severstal Aircompany LR Lacsa SX SkyWork Airlines 2M Moldavian Airlines D6 Interair South Africa LW Pacific Wings Airlines SY Sun Country Airlines 2N Nextjet DC Golden Air LY EL AL Israel Airlines T4 TRIP Linhas Aéreas 2W Welcome Air DG South East Asian Airlines M7 Marsland Aviation TA TACA 3B Job Air - Central Connect DN Senegal Airlines M9 Motor Sich Airlines JSC TB Jetairfly.com 3E Air Choice One DV JSC Air Company Scat MD Air Madagascar TF Malmö Aviation 3L InterSky EI Aer Lingus ME Middle East Airlines TK Turkish Airlines 3P Tiara Air N.V. EK Emirates MF Xiamen Airlines TM LAM - Linhas Aereas 4J Somon Air ET Ethiopian Airlines MH Malaysia Airlines TN Air Tahiti Nui 4M Lan Argentina EY Etihad Airways MI SilkAir TU Tunis Air 4Q Safi Airways F7 Darwin Airline SA MK Air Mauritius U6 Ural Airlines 5C Nature Air F9 Frontier Airlines MU China Eastern Airlines -

Die Folgende Liste Zeigt Alle Fluggesellschaften, Die Über Den Flugvergleich Von Verivox Buchbar Sein Können

Die folgende Liste zeigt alle Fluggesellschaften, die über den Flugvergleich von Verivox buchbar sein können. Aufgrund von laufenden Updates einzelner Tarife, technischen Problemen oder eingeschränkten Verfügbarkeiten kann es vorkommen, dass einzelne Airlines oder Tarife nicht berechnet oder angezeigt werden können. 1 Adria Airways 2 Aegean Airlines 3 Aer Arann 4 Aer Lingus 5 Aeroflot 6 Aerolan 7 Aerolíneas Argentinas 8 Aeroméxico 9 Air Algérie 10 Air Astana 11 Air Austral 12 Air Baltic 13 Air Berlin 14 Air Botswana 15 Air Canada 16 Air Caraibes 17 Air China 18 Air Corsica 19 Air Dolomiti 20 Air Europa 21 Air France 22 Air Guinee Express 23 Air India 24 Air Jamaica 25 Air Madagascar 26 Air Malta 27 Air Mauritius 28 Air Moldova 29 Air Namibia 30 Air New Zealand 31 Air One 32 Air Serbia 33 Air Transat 34 Air Asia 35 Alaska Airlines 36 Alitalia 37 All Nippon Airways 38 American Airlines 39 Arkefly 40 Arkia Israel Airlines 41 Asiana Airlines 42 Atlasglobal 43 Austrian Airlines 44 Avianca 45 B&H Airlines 46 Bahamasair 47 Bangkok Airways 48 Belair Airlines 49 Belavia Belarusian Airlines 50 Binter Canarias 51 Blue1 52 British Airways 53 British Midland International 54 Brussels Airlines 55 Bulgaria Air 56 Caribbean Airlines 57 Carpatair 58 Cathay Pacific 59 China Airlines 60 China Eastern 61 China Southern Airlines 62 Cimber Sterling 63 Condor 64 Continental Airlines 65 Corsair International 66 Croatia Airlines 67 Cubana de Aviacion 68 Cyprus Airways 69 Czech Airlines 70 Darwin Airline 71 Delta Airlines 72 Dragonair 73 EasyJet 74 EgyptAir 75 -

Tupolev TU-204-100/ -300/ TU-214 Sorting: Serial Nr

Tupolev TU-204-100/ -300/ TU-214 Sorting: Serial Nr. 15.07.2021 Ser.Nr. Type F/F Status Immatr. Operator Last Operator in service Engines Owner Rem. @airlinefleet.info M/Y until 1450741064019 TU-204-100 1993 stored RA-64019 none Red Wings 03-2014 Perm PS-90A 1450741164004 TU-204-100 1991 broken up RA-64004 none Producer/Prototype 08-2005 Perm PS-90A broken up by 12-2010 1450741264007 TU-204-100C 1991 perm_wfu RA-64007 none Aeroflot Russian Airlines 08-2001 Perm PS-90A 1450741364011 TU-204-100 1993 accidented RA-64011 none Sibir Airlines 03-2010 Perm PS-90A crashed on landing Moscow-Domodedov 1450741364024 TU-204-120C 1999 in service RA-64024 Aviastar - TU Air 07-2005 Perm PS-90A 1450741464015 TU-204-100 1993 stored RA-64015 none Rossiya GTK 08-2001 Perm PS-90A to Aviastar for re-work/modernisation 1450741564039 TU-204-300 2005 stored RA-64039 none Vladivostok Air 10-2013 Perm PS-90A VIP-configurated 1450741864044 TU-204-300 2008 in service RA-64044 Roskosmos 05-2019 Perm PS-90A RKK Energy 1450741964018 TU-204-100 1993 perm_wfu RA-64018 none Red Wings 10-2017 Perm PS-90A 1450741964048 TU-204-100 2009 in service P-633 Air Koryo 03-2010 Perm PS-90A 1450741964050 TU-204-100 2009 stored RA-64050 none Red Wings 11-2018 Perm PS-90A 1450742064022 TU-204-100 1999 stored RA-64022 none Red Wings 09-2013 Perm PS-90A 1450742264032 TU-204-120C 2001 in service RA-64032 Aviastar - TU Air 07-2008 Perm PS-90A 1450742364012 TU-204-300 1993 in service P-632 Air Koryo 12-2007 Perm PS-90A conv.from vers.100 in vers.300 2007 1450742564017 TU-204-100 1993 in -

Airliner Census Western-Built Jet and Turboprop Airliners

World airliner census Western-built jet and turboprop airliners AEROSPATIALE (NORD) 262 7 Lufthansa (600R) 2 Biman Bangladesh Airlines (300) 4 Tarom (300) 2 Africa 3 MNG Airlines (B4) 2 China Eastern Airlines (200) 3 Turkish Airlines (THY) (200) 1 Equatorial Int’l Airlines (A) 1 MNG Airlines (B4 Freighter) 5 Emirates (300) 1 Turkish Airlines (THY) (300) 5 Int’l Trans Air Business (A) 1 MNG Airlines (F4) 3 Emirates (300F) 3 Turkish Airlines (THY) (300F) 1 Trans Service Airlift (B) 1 Monarch Airlines (600R) 4 Iran Air (200) 6 Uzbekistan Airways (300) 3 North/South America 4 Olympic Airlines (600R) 1 Iran Air (300) 2 White (300) 1 Aerolineas Sosa (A) 3 Onur Air (600R) 6 Iraqi Airways (300) (5) North/South America 81 RACSA (A) 1 Onur Air (B2) 1 Jordan Aviation (200) 1 Aerolineas Argentinas (300) 2 AEROSPATIALE (SUD) CARAVELLE 2 Onur Air (B4) 5 Jordan Aviation (300) 1 Air Transat (300) 11 Europe 2 Pan Air (B4 Freighter) 2 Kuwait Airways (300) 4 FedEx Express (200F) 49 WaltAir (10B) 1 Saga Airlines (B2) 1 Mahan Air (300) 2 FedEx Express (300) 7 WaltAir (11R) 1 TNT Airways (B4 Freighter) 4 Miat Mongolian Airlines (300) 1 FedEx Express (300F) 12 AIRBUS A300 408 (8) North/South America 166 (7) Pakistan Int’l Airlines (300) 12 AIRBUS A318-100 30 (48) Africa 14 Aero Union (B4 Freighter) 4 Royal Jordanian (300) 4 Europe 13 (9) Egyptair (600R) 1 American Airlines (600R) 34 Royal Jordanian (300F) 2 Air France 13 (5) Egyptair (600R Freighter) 1 ASTAR Air Cargo (B4 Freighter) 6 Yemenia (300) 4 Tarom (4) Egyptair (B4 Freighter) 2 Express.net Airlines -

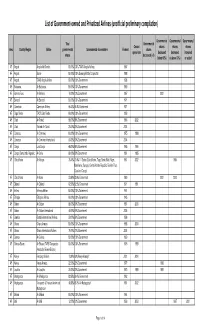

List of Government-Owned and Privatized Airlines (Unofficial Preliminary Compilation)

List of Government-owned and Privatized Airlines (unofficial preliminary compilation) Governmental Governmental Governmental Total Governmental Ceased shares shares shares Area Country/Region Airline governmental Governmental shareholders Formed shares operations decreased decreased increased shares decreased (=0) (below 50%) (=/above 50%) or added AF Angola Angola Air Charter 100.00% 100% TAAG Angola Airlines 1987 AF Angola Sonair 100.00% 100% Sonangol State Corporation 1998 AF Angola TAAG Angola Airlines 100.00% 100% Government 1938 AF Botswana Air Botswana 100.00% 100% Government 1969 AF Burkina Faso Air Burkina 10.00% 10% Government 1967 2001 AF Burundi Air Burundi 100.00% 100% Government 1971 AF Cameroon Cameroon Airlines 96.43% 96.4% Government 1971 AF Cape Verde TACV Cabo Verde 100.00% 100% Government 1958 AF Chad Air Tchad 98.00% 98% Government 1966 2002 AF Chad Toumai Air Tchad 25.00% 25% Government 2004 AF Comoros Air Comores 100.00% 100% Government 1975 1998 AF Comoros Air Comores International 60.00% 60% Government 2004 AF Congo Lina Congo 66.00% 66% Government 1965 1999 AF Congo, Democratic Republic Air Zaire 80.00% 80% Government 1961 1995 AF Cofôte d'Ivoire Air Afrique 70.40% 70.4% 11 States (Cote d'Ivoire, Togo, Benin, Mali, Niger, 1961 2002 1994 Mauritania, Senegal, Central African Republic, Burkino Faso, Chad and Congo) AF Côte d'Ivoire Air Ivoire 23.60% 23.6% Government 1960 2001 2000 AF Djibouti Air Djibouti 62.50% 62.5% Government 1971 1991 AF Eritrea Eritrean Airlines 100.00% 100% Government 1991 AF Ethiopia Ethiopian