Pobeda Airline: Group’S Low Cost Carrier

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Presentation Is Made, Or by Reading the Presentation Slides, You Agree to the Following

AEROFLOT GROUP Q3 & 9M 2020 IFRS R ESULTS 1 December 2020 Speakers: Andrey Chikhanchin – Deputy CEO for Commerce and Finance Andrey Panov – Deputy CEO for Strategy, Service and Marketing Ivan Batanov – Head of Revenue Management Disclaimer This document has been prepared by PJSC “Aeroflot” (the “Company”). By attending the meeting where the presentation is made, or by reading the presentation slides, you agree to the following. This document does not constitute or form part of any advertisement of securities, any offer or invitation to sell or issue or any solicitation of any offer to purchase or subscribe for, any securities of the Company in any jurisdiction, nor shall it or any part of it nor the fact of its presentation or distribution form the basis of, or be relied on in connection with, any contract or investment decision. No reliance may be placed for any purpose whatsoever on the information contained in this document or on assumptions made as to its completeness. No representation or warranty, express or implied, is given by the Company, its subsidiaries or any of their respective advisers, officers, employees or agents, as to the accuracy of the information or opinions or for any loss howsoever arising, directly or indirectly, from any use of this presentation or its contents. This document may include forward-looking statements. These forward-looking statements include matters that are not historical facts or statements regarding the Company’s intentions, beliefs or current expectations concerning, among other things, the Company’s results of operations, financial condition, liquidity, prospects, growth, strategies, and the market in which the Company operates. -

The Change Is NOW ! EXECUTIVE SUMMARY

The change is NOW ! EXECUTIVE SUMMARY The inflight business has changed dramatically in recent years The aim of this presentation is to share and point out the recent evolution we, at ISG , have noticed To provide food for thought on how we can all remain competitive & efficient while answering the new expectations of our customers. AGENDA Introduction of Inflight Sales Group PART I : Evolution of passengers’ expectations PART II : Market revolution PART III : Airline perspective INTRODUCTION Inflight Sales Group ISG – The original concessionaire 2015 Opening of an ISG Office in Riga with a team dedicated to Russia and Eastern Europe Opening of Supplier of amenity kits to 2014 the European 1982 more than 60 Airlines 1994 Rapid growth from 1 ISG Office in worldwide and an airline to 34 airlines Paris exclusive distributor of major duty free brands 1996 Establishment of Awarded another Inflight Sales Group 2013 long term 1986 1st Concession at (HK) Ltd contract with Pan American Cathay Pacific and Dragonair 1999 Expansion to Asian Airlines WINNER OF MULTIPLE AWARDS “Inflight Travel Retailer of the Year” from Duty Free News International (DFNI) 2008 / 2009 / 2010 / 2011 / 2012 / 2015 “Inflight Travel Retailer of the Year” At Frontier Awards 2010 / 2011 / 2012 / 2013 / 2014 “Best new marketing initiative” in 2008 “Best Inflight Concessionaire” at the Airline Retail Conferences (ARC) in Singapore and Paris 2013 / 2014 / 2015 OUR EXPANDING CUSTOMERS FOOTPRINT ISG is proud to partner with 26 airlines worldwide Our commitment in building long-term relationships with our clients, offering innovative product sourcing and revolutionary service solutions has successfully taken inflight revenue to new heights and transformed duty free as a core component of the airline business. -

Airline On-Time Arrival Performance (Sep 2018, by Variflight) SC Tops

Airline On-time Arrival Performance (Sep 2018, by VariFlight) SC Tops China’s Major Airlines in APAC OTP Chart MF Shows the Most Rapid YoY Growth Powered by VariFlight incomparable aviation database, the monthly report of Airline On-time Arrival Performance provides an overview of how global airlines perform in September, 2018. In September, Aeroflot-Russian Airlines tops the global OTP chart again. A total of 381,000 aircraft movements were handled by Chinese airlines, showing an increase of 4.6 percent year-over-year. Aeroflot-Russian Airlines takes the top spot in the global OTP chart for three consecutive months. Shandong Airlines moves into the first place for punctuality among Chinese airlines in APAC with an on-time arrival rate of 89.22 percent. Among ten major Chinese airlines, Shandong Airlines surpasses Tianjin Airlines to top the OTP list; Xiamen Airlines shows the most rapid YoY growth in OTP. Taking a look at the TOP10 domestic popular routes, SHA-CAN route demonstrates the fastest growth, improving 23.14 percent compared with that in August. Global Big Airlines SU Tops Global Big Airlines Aeroflot-Russian Airlines tops the global big airlines chart in September with an on-time arrival rate of 96.28 percent and 5.06 minutes of average arrival delay, followed by All Nippon Airways and Japan Airlines. IATA Flight On-time Arrival Average Arrival Ranking Airlines Country Code Arrivals Performance Delay (minutes) Aeroflot-Russian 1 SU RU 30826 96.28% 5.06 Airlines 2 NH All Nippon Airways JP 34965 96.20% 5.60 3 JL Japan Airlines JP 23778 96.09% 6.58 4 EK Emirates Airlines AE 16042 95.90% 5.68 Page 1 of 6 © 2018 VariFlight. -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

China Southern Airlines' Sky Pearl Club

SKY PEARL CLUB MEMBERSHIP GUIDE Welcome to China Southern Airlines’ Sky Pearl Club The Sky Pearl Club is the frequent flyer program of China Southern Airlines. From the moment you join The Sky Pearl Club, you will experience a whole new world of exciting new travel opportunities with China Southern! Whether you’re traveling for business or pleasure, you’ll be earning mileage toward your award goals every time you fly. Many Elite tier services have been prepared for you. We trust this Guide will soon help you reach your award flight to your dream destinations. China Southern Sky Pearl Club cares about you! 1 A B Earning Sky Pearl Mileage Redeeming Sky Pearl Mileage Airlines China Southern Award Ticket and Award Upgrade Hotels SkyTeam Award Ticket and Award Upgrade Banks Telecommunications, Car Rentals, Business Travel , Dining and others C D Getting Acquainted with Sky Pearl Rules Enjoying Sky Pearl Elite Benefits Definition Membership tiers Membership Qualification and Mileage Account Elite Qualification Mileage Accrual Elite Benefits Mileage Redemption Membership tier and Elite benefits Others 2 A Earning Sky Pearl Mileage As the newest member of the worldwide SkyTeam alliance, whether it’s in the air or on the ground, The Sky Pearl Club gives you more opportunities than ever before to earn Award travel. When flying with China Southern or one of our many airline partners, you can earn FFP mileage. But, that’s not the only way! Hotels stays, car rentals, credit card services, telecommunication services or dining with our business-to-business partners can also help you earn mileage. -

Skyteam Timetable Covers Period: 01 Jun 2021 Through 31 Aug 2021

SkyTeam Timetable Covers period: 01 Jun 2021 through 31 Aug 2021 Regions :Europe - Asia Pacific Contact Disclaimer To book, contact any SkyTeam member airline. The content of this PDF timetable is for information purposes only, subject to change at any time. Neither Aeroflot www.aeroflot.com SkyTeam, nor SkyTeam Members (including without Aerolneas Argentinas www.aerolineas.com limitation their respective suppliers) make representation Aeromexico www.aeromexico.com or give warranty as to the completeness or accuracy of Air Europa www.aireuropa.com such content as well as to its suitability for any purpose. Air France www.airfrance.com In particular, you should be aware that this content may be incomplete, may contain errors or may have become Alitalia www.alitalia.com out of date. It is provided as is without any warranty or China Airlines www.china-airlines.com condition of any kind, either express or implied, including China Eastern www.ceair.com but not limited to all implied warranties and conditions of China Southern www.csair.com merchantability, fitness for a particular purpose, title and Czech Airlines www.czechairlines.com non-infringement. Given the flexible nature of flight Delta Air Lines www.delta.com schedules, our PDF timetable may not reflect the latest information. Garuda Indonesia www.garuda-indonesia.com Kenya Airways www.kenya-airways.com By accessing the PDF timetable, the user acknowledges that the SkyTeam Alliance and any SkyTeam member KLM www.klm.com airline will not be responsible or liable to the user, or any -

China Eastern Airlines Corporation Limited; China Southern Airlines Company Limited; Hainan Airlines Holding Co

Order 2020-5-4 UNITED STATES OF AMERICA DEPARTMENT OF TRANSPORTATION OFFICE OF THE SECRETARY WASHINGTON, D.C. Issued by the Department of Transportation on the 22nd day of May, 2020 Served: May 22, 2020 In the matter of Air China Limited d/b/a/ Air China; Beijing Capital Airlines Co., Ltd.; China Eastern Airlines Corporation Limited; China Southern Airlines Company Limited; Hainan Airlines Holding Co. Ltd.; Sichuan Airlines Co., Ltd.; and Xiamen Airlines Docket DOT-OST-2020-0052 ORDER TO FILE SCHEDULES Summary By this Order, the U.S. Department of Transportation (the Department) is taking steps in response to the failure of the Government of the People’s Republic of China (China) to permit U.S. carriers to exercise the full extent of their bilateral right to conduct scheduled passenger air services to China. Specifically, in this Order, we are imposing Phase 1 schedule filing requirements under 14 CFR Part 213 of the Department’s regulations to cover all of the scheduled combination services of the captioned foreign air carriers operating to/from the United States. Background Civil aviation relations between the Governments of the United States (USG) and China are governed by the U.S.-China Civil Air Transport Agreement, as amended (“the Agreement”), concluded on September 17, 1980 and subsequently amended. The Agreement establishes, among other things, rights for the carriers of both parties to provide certain air services between the two countries. For airlines designated by the USG, these rights include, among others, the right to -

Facts & Figures & Figures

OCTOBER 2019 FACTS & FIGURES & FIGURES THE STAR ALLIANCE NETWORK RADAR The Star Alliance network was created in 1997 to better meet the needs of the frequent international traveller. MANAGEMENT INFORMATION Combined Total of the current Star Alliance member airlines: FOR ALLIANCE EXECUTIVES Total revenue: 179.04 BUSD Revenue Passenger 1,739,41 bn Km: Daily departures: More than Annual Passengers: 762,27 m 19,000 Countries served: 195 Number of employees: 431,500 Airports served: Over 1,300 Fleet: 5,013 Lounges: More than 1,000 MEMBER AIRLINES Aegean Airlines is Greece’s largest airline providing at its inception in 1999 until today, full service, premium quality short and medium haul services. In 2013, AEGEAN acquired Olympic Air and through the synergies obtained, network, fleet and passenger numbers expanded fast. The Group welcomed 14m passengers onboard its flights in 2018. The Company has been honored with the Skytrax World Airline award, as the best European regional airline in 2018. This was the 9th time AEGEAN received the relevant award. Among other distinctions, AEGEAN captured the 5th place, in the world's 20 best airlines list (outside the U.S.) in 2018 Readers' Choice Awards survey of Condé Nast Traveler. In June 2018 AEGEAN signed a Purchase Agreement with Airbus, for the order of up to 42 new generation aircraft of the 1 MAY 2019 FACTS & FIGURES A320neo family and plans to place additional orders with lessors for up to 20 new A/C of the A320neo family. For more information please visit www.aegeanair.com. Total revenue: USD 1.10 bn Revenue Passenger Km: 11.92 m Daily departures: 139 Annual Passengers: 7.19 m Countries served: 44 Number of employees: 2,498 Airports served: 134 Joined Star Alliance: June 2010 Fleet size: 49 Aircraft Types: A321 – 200, A320 – 200, A319 – 200 Hub Airport: Athens Airport bases: Thessaloniki, Heraklion, Rhodes, Kalamata, Chania, Larnaka Current as of: 14 MAY 19 Air Canada is Canada's largest domestic and international airline serving nearly 220 airports on six continents. -

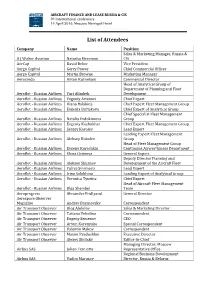

List of Attendees

AIRCRAFT FINANCE AND LEASE RUSSIA & CIS 8th international conference 14 April 2016, Moscow Metropol Hotel List of Attendees Company Name Position Sales & Marketing Manager, Russia & A J Walter Aviation Natasha Meerman CIS AerCap David Beker Vice President Aergo Capital Gerry Power Chief Commercial Officer Aergo Capital Martin Browne Marketing Manager Aerocredo Anton Kuznetsov Commercial Director Head of Analytical Group of Department of Planning and Fleet Aeroflot - Russian Airlines Yuri Alimbek Development Aeroflot - Russian Airlines Evgeniy Artemov Chief Expert Aeroflot - Russian Airlines Diana Balakina Chief Expert Fleet Management Group Aeroflot - Russian Airlines Evgenia Burlakova Chief Expert of Analytical Group Chief Specialist Fleet Management Aeroflot - Russian Airlines Natalia Evdokimova Group Aeroflot - Russian Airlines Evgeniy Kozhukhar Chief Expert Fleet Management Group Aeroflot - Russian Airlines Sergey Korolev Lead Expert Leading Expert Fleet Management Aeroflot - Russian Airlines Aleksey Kukolev Group Head of Fleet Management Group Aeroflot - Russian Airlines Evgeny Kurochkin Continuing Airworthiness Department Aeroflot - Russian Airlines Elena Ozimova General Expert Deputy Director Planning and Aeroflot - Russian Airlines Aleksey Siluanov Development of the Aircraft Fleet Aeroflot - Russian Airlines Yuliya Smirnova Lead Expert Aeroflot - Russian Airlines Irina Solokhina Leading Expert of Analytical Group Aeroflot - Russian Airlines Veronica Tyurina Chief Expert Head of Aircraft Fleet Management Aeroflot - Russian Airlines -

List of Foreign EASA Part-145 Approved Organisations

EASA-IFP - List of Valid Foreign Part 145 organisations (WEB) List of valid Foreign Part-145 organisations This list contains valid approvals, including limited and partially suspended ones. Approved organisations EASA approval number Certificate address Country - Status of Approval: Patially Suspended (3) EASA.145.0469 NW TECHNIC LLC RUSSIA EASA.145.0547 ONUR AIR TASIMACILIK A.S. D/B/A ONUR AIR TURKEY EASA.145.0660 LIMITED LIABILITY COMPANY ''UTG DOMODEDOVO'' T/A UTG AVIATION SERVICES RUSSIA - Status of Approval: Valid (334) EASA.145.0003 GOODRICH AEROSTRUCTURES SERVICE (CENTER-ASIA) PTE Ltd. SINGAPORE EASA.145.0005 CHROMALLOY (THAILAND) LTD. THAILAND EASA.145.0007 ''UZBEKISTAN AIRWAYS TECHNICS'' LIMITED LIABILITY COMPANY UZBEKISTAN EASA.145.0008 KUWAIT AIRWAYS COMPANY KUWAIT EASA.145.0010 ABU DHABI AVIATION UNITED ARAB EMIRATES EASA.145.0012 AEROFLOT RUSSIAN AIRLINES RUSSIA EASA.145.0015 AIR ASTANA JSC KAZAKHSTAN EASA.145.0016 AI ENGINEERING SERVICES LIMITED t/a AIESL INDIA EASA.145.0017 AIR MAURITIUS Ltd. MAURITIUS EASA.145.0018 AIRFOIL SERVICES SDN. BHD. MALAYSIA EASA.145.0019 GE AVIATION, ENGINE SERVICES - SING PTE. LTD. SINGAPORE EASA.145.0020 ALIA - THE ROYAL JORDANIAN AIRLINES PLC CO (ROYAL JORDANIAN) JORDAN EASA.145.0021 AIRCRAFT MAINTENANCE AND ENGINEERING CORPORATION, BEIJING (AMECO) CHINA EASA.145.0022 AMSAFE AVIATION (CHONGQING) Ltd. CHINA EASA.145.0024 ASIA PACIFIC AEROSPACE Pty. Ltd. AUSTRALIA EASA.145.0025 ASIAN COMPRESSOR TECHNOLOGY SERVICES CO. LTD. TAIWAN EASA.145.0026 ASIAN SURFACE TECHNOLOGIES PTE LTD SINGAPORE EASA.145.0027 AEROVIAS DEL CONTINENTE AMERICANO S AVIANCA S.A. COLOMBIA EASA.145.0028 BAHRAIN AIRPORT SERVICES BAHRAIN EASA.145.0029 ISRAEL AEROSPACE INDUSTRIES, Ltd. -

Air Transport in Russia and Its Impact on the Economy

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Tomsk State University Repository Вестник Томского государственного университета. Экономика. 2019. № 48 МИРОВАЯ ЭКОНОМИКА UDC 330.5, 338.4 DOI: 10.17223/19988648/48/20 V.S. Chsherbakov, O.A. Gerasimov AIR TRANSPORT IN RUSSIA AND ITS IMPACT ON THE ECONOMY The study aims to collect and analyse statistics of Russian air transport, show the in- fluence of air transport on the national economy over the period from 2007 to 2016, compare the sector’s role in Russia with the one in other countries. The study reveals the significance of air transport for Russian economy by comparing airlines’ and air- ports’ monetary output to the gross domestic product. On the basis of the research, the policies in the aviation sector can be adjusted by government authorities. Ключевые слова: Russia, aviation, GDP, economic impact, air transport, statistics. Introduction According to Air Transport Action Group, the air transport industry supports 62.7 million jobs globally and aviation’s total global economic impact is $2.7 trillion (approximately 3.5% of the Gross World Product) [1]. Aviation transported 4 billion passengers in 2017, which is more than a half of world population, according to the International Civil Aviation Organization [2]. It makes the industry one of the most important ones in the world. It has a consid- erable effect on national economies by providing a huge number of employment opportunities both directly and indirectly in such spheres as tourism, retail, manufacturing, agriculture, and so on. Air transport is a driving force behind economic connection between different regions because it may entail economic, political, and social effects. -

Dual-Hub Connectivity: a Case Study on China Eastern Airlines in Shanghai Huijuan Yang* and Weiwei Liu

Yang and Liu European Transport Research Review (2019) 11:25 European Transport https://doi.org/10.1186/s12544-019-0364-6 Research Review ORIGINAL PAPER Open Access Dual-hub connectivity: a case study on China Eastern Airlines in Shanghai Huijuan Yang* and Weiwei Liu Abstract To deal with slot constraints and insufficient capacity, emerging multi-airport systems have been under construction in China. This paper chose China Eastern Airlines as a case study, evaluating its hub connectivity under a dual-hub circumstance in Shanghai. The paper detected that the biggest constraint of China Eastern Airlines’ dual-hub situation lied in Shanghai’s location and the restricted transfer options on international routes. Contributions from alliance partners were assessed and benchmarked with China Eastern Airlines. With China Southern Airlines quit SkyTeam alliance, China Eastern Airlines faced more challenges on the domestic market. The empirical study also pointed out the shortcoming of operating at two hubs in the same catchment area, where the quality of connectivity of inter-hub connections cannot be maintained as high as a single-hub transfer. However, the market potential of inter-hub connections in Shanghai was identified with a considerable amount of viable connections. Keywords: Hub connectivity, Dual-hub operation, China Eastern Airlines 1 Introduction Multi-airport system largely expands the catchment area Airports have experienced pressures on operational cap- and capacity in the region. It provides better accessibility acity and congestion due to the worldwide effects of explo- for passengers, and attracts and generates more traffic for sive passenger growth, particularly in high-growth regions airlines and airports.