Written Evidence Submitted by Airlines UK (PEG0191)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

UK Office December 2018 TDC Report Prepared By

UK Office December 2018 TDC Report Prepared by: Venessa Alexander UK Director Tour Operators • Virgin Holidays – We visited their office to provide Christmas cakes and branded giveaways to their Florida sales agents ahead of peak booking season. The items were very well received from the staff. • Funway Holidays - We visited their office to provide Christmas treats and branded giveaways to their sales agents ahead of the peak booking season. We got the chance to speak to the reservations team as well as the reservations manager and the treats and giveaways were gratefully received. • USAirtours/TravelPlanners - We had the chance to visit the USAirtours / TravelPlanners office to provide Christmas treats and branded giveaways to their sales agents. We had the chance to talk to the sales agents if they were not busy on the phones and then held a lunch meeting with both the product and marketing teams to discuss the proposed co-op marketing proposal that we have now received. The proposal is currently being assessed and once activity has been finalised, we will get final sign off from Brand USA. Meetings/Training/Events • SeaWorld Parks – We met with Simon Parry and Ruth Roseweir to further discuss our joint event and fam trip for next year. We will follow up in the New Year to begin sourcing a venue for the event and to work with Norwegian to secure seats for the trip. • Norwegian – We met with Nicole Richards, Marketing Manager, alongside Kenneth Strickland, Tampa Airport and Becky Fairlie-Clarke, Tampa Bay. All partners provided an update on the destination and recent and upcoming marketing activity. -

Annual Report 2017 Contents & Financial Highlights

ANNUAL REPORT 2017 CONTENTS & FINANCIAL HIGHLIGHTS TUI GroupFinancial 2017 in numbers highlights Formats The Annual Report and 2017 2016 Var. % Var. % at the Magazine are also available online € 18.5 bn € 1,102.1restated m constant € million currency Turnover 18,535.0 17,153.9 + 8.1 + 11.7 Underlying EBITA1 1 1 + 11.7Hotels & %Resorts + 12.0356.5 % 303.8 + 17.3 + 19.2 Cruises 255.6 190.9 + 33.9 + 38.0 Online turnoverSource Markets underlying526.5 554.3 – 5.0 – 4.0 Northern Region 345.8 383.1 – 9.7 – 8.4 year-on-year Central Region 71.5 85.1 – 16.0 – 15.8 Western Region EBITA109.2 86.1 + 26.8 + 27.0 Other Tourism year-on-year13.4 7.9 + 69.6 + 124.6 Tourism 1,152.0 1,056.9 + 9.0 + 11.2 All other segments – 49.9 – 56.4 + 11.5 + 3.4 Mobile TUI Group 1,102.1 1,000.5 + 10.2 + 12.0 Discontinued operations – 1.2 92.9 n. a. Total 1,100.9 1,093.4 + 0.7 http://annualreport2017. tuigroup.com EBITA 2, 4 1,026.5 898.1 + 14.3 Underlying EBITDA4 1,541.7 1,379.6 + 11.7 56 %EBITDA2 4 23.61,490.9 % ROIC1,305.1 + 14.2 Net profi t for the period 910.9 464.9 + 95.9 fromEarnings hotels per share4 & € 6.751.36 % WACC0.61 + 123.0 Equity ratio (30 Sept.)3 % 24.9 22.5 + 2.4 cruisesNet capex and contentinvestments (30 Sept.) 1,071.9 634.8 + 68.9 comparedNet with cash 30 %(302 at Sept.) time 4of merger 583.0 31.8 n. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Appendix 25 Box 31/3 Airline Codes

March 2021 APPENDIX 25 BOX 31/3 AIRLINE CODES The information in this document is provided as a guide only and is not professional advice, including legal advice. It should not be assumed that the guidance is comprehensive or that it provides a definitive answer in every case. Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 000 ANTONOV DESIGN BUREAU 001 AMERICAN AIRLINES 005 CONTINENTAL AIRLINES 006 DELTA AIR LINES 012 NORTHWEST AIRLINES 014 AIR CANADA 015 TRANS WORLD AIRLINES 016 UNITED AIRLINES 018 CANADIAN AIRLINES INT 020 LUFTHANSA 023 FEDERAL EXPRESS CORP. (CARGO) 027 ALASKA AIRLINES 029 LINEAS AER DEL CARIBE (CARGO) 034 MILLON AIR (CARGO) 037 USAIR 042 VARIG BRAZILIAN AIRLINES 043 DRAGONAIR 044 AEROLINEAS ARGENTINAS 045 LAN-CHILE 046 LAV LINEA AERO VENEZOLANA 047 TAP AIR PORTUGAL 048 CYPRUS AIRWAYS 049 CRUZEIRO DO SUL 050 OLYMPIC AIRWAYS 051 LLOYD AEREO BOLIVIANO 053 AER LINGUS 055 ALITALIA 056 CYPRUS TURKISH AIRLINES 057 AIR FRANCE 058 INDIAN AIRLINES 060 FLIGHT WEST AIRLINES 061 AIR SEYCHELLES 062 DAN-AIR SERVICES 063 AIR CALEDONIE INTERNATIONAL 064 CSA CZECHOSLOVAK AIRLINES 065 SAUDI ARABIAN 066 NORONTAIR 067 AIR MOOREA 068 LAM-LINHAS AEREAS MOCAMBIQUE Page 2 of 19 Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 069 LAPA 070 SYRIAN ARAB AIRLINES 071 ETHIOPIAN AIRLINES 072 GULF AIR 073 IRAQI AIRWAYS 074 KLM ROYAL DUTCH AIRLINES 075 IBERIA 076 MIDDLE EAST AIRLINES 077 EGYPTAIR 078 AERO CALIFORNIA 079 PHILIPPINE AIRLINES 080 LOT POLISH AIRLINES 081 QANTAS AIRWAYS -

Global Leaders in Innovative Full Service Airline Training

Global Leaders in Innovative Full Service Airline Training committed to excellence Welcome At CTC we are proud of the reputation that we have built over time as worldwide providers of innovative training solutions. This reputation is founded on the delivery of our core values: expertise, quality, innovation and flexibility. With our state-of-the-art Crew Training Centres across the globe and specialist training personnel, we are able to provide our client airlines with every element of airline crew training. We offer a wide range of training options from basic CPL/IR licence through to Type Rating on the most popular commercial aircraft today including Boeing and Airbus, and onwards to training airline instructors and examiners. From crew selection through to crew supply and from CRM courses to Command Training, CTC can deliver all your needs; we are truly a ‘full service’ airline training specialist. To do this we enjoy comprehensive Joint Aviation Authority approvals as a Type-Rating Training Organisation and Flight Training Organisation and we have received approvals from many other regulatory authorities around the world. Equally as important, we enjoy the trust and loyalty of many of the world’s leading airlines – whether it be for the supply of a standalone training course, or for the outsourcing of all of their crew training needs. These factors make CTC your first choice partner to provide specialist aviation training and support – worldwide – for all your aircrew requirements. We look forward to being of service to you. Captain Chris Clarke Group Chairman CTC Aviation Group plc 1 WELCOME ‘CTC has supported us throughout our growth. -

1 LONDON SOUTHEND AIRPORT Minutes of Meeting No. 98 of The

LONDON SOUTHEND AIRPORT Minutes of meeting No. 98 of the Consultative Committee held on Wednesday, 9 May 2018 at 2pm at Southend Airport Present: Stuart Greengrass Chairman Jon Horne (JH) COO, LSA Jo Marchetti (JM) Community Affairs Co-ordinator, LSA David Osborn Deputy Chairman, Councillor Ray Howard, MBE Castle Point Borough Council Councillor Valerie Morgan Leigh Town Council Councillor Mike Lucas-Gill Rochford District Council Dan Kudla (Officer) Rochford District Council Councillor Meg Davidson Southend-on-Sea Borough Council Ron Smithson Southend Flying Clubs Mike Sessions Jota Aviation Emma McDonnell (EM) Minutes 1. APOLOGIES FOR ABSENCE Apologies for absence were received from Councillor Reeves, Councillor Steptoe, Councillor Riley, Councillor Elliott, Councillor Williams, Councillor Partridge, Mark Evershed, Martin Howlett, Paula Chapman, Andrew Lewis, Heidi Turnbull, David Burrows, Denise Rossiter, David Burch, Les Sawyer and Derry Thorpe. 2. MEMBERSHIP AND CHAIRMAN’S OPENING REMARKS The Chairman welcomed JH who, although he should have semi-retired in April, had been asked by the Airport to continue in his position for a further three months, ie to the end of July, until a replacement COO had been found. JH was delighted to be able to attend another LSACC. The Chairman asked those members and representatives attending for the first time to introduce themselves – Dan Kudla, Regeneration Officer, was attending on behalf of Planning Policy for Rochford District Council. 2.1 EM requested that as a result of the recent local elections, could all Councils notify ALL her in writing of any membership changes as soon as possible. 25/05/18 3. ADOPTION OF MINUTES FROM LAST MEETING 14 FEBRUARY 2018 3.1 The minutes of 14th February 2018 were agreed and adopted with no amendments required. -

Norwegian Air Shuttle ASA (A Public Limited Liability Company Incorporated Under the Laws of Norway)

REGISTRATION DOCUMENT Norwegian Air Shuttle ASA (a public limited liability company incorporated under the laws of Norway) For the definitions of capitalised terms used throughout this Registration Document, see Section 13 “Definitions and Glossary”. Investing in the Shares involves risks; see Section 1 “Risk Factors” beginning on page 5. Investing in the Shares, including the Offer Shares, and other securities issued by the Issuer involves a particularly high degree of risk. Prospective investors should read the entire Prospectus, comprising of this Registration Document, the Securities Note dated 6 May 2021 and the Summary dated 6 May 2021, and, in particular, consider the risk factors set out in this Registration Document and the Securities Note when considering an investment in the Company. The Company has been severely impacted by the current outbreak of COVID-19. In a very short time period, the Company has lost most of its revenues and is in adverse financial distress. This has adversely and materially affected the Group’s contracts, rights and obligations, including financing arrangements, and the Group is not capable of complying with its ongoing obligations and is currently subject to event of default. On 18 November 2020, the Company and certain of its subsidiaries applied for Examinership in Ireland (and were accepted into Examinership on 7 December 2020), and on 8 December 2020 the Company applied for and was accepted into Reconstruction in Norway. These processes were sanctioned by the Irish and Norwegian courts on 26 March 2021 and 12 April 2021 respectively, however remain subject to potential appeals in Norway (until 12 May 2021) and certain other conditions precedent, including but not limited to the successful completion of a capital raise in the amount of at least NOK 4,500 million (including the Rights Issue, the Private Placement and issuance of certain convertible hybrid instruments as described further herein). -

Monthly OTP July 2019

Monthly OTP July 2019 ON-TIME PERFORMANCE AIRLINES Contents On-Time is percentage of flights that depart or arrive within 15 minutes of schedule. Global OTP rankings are only assigned to all Airlines/Airports where OAG has status coverage for at least 80% of the scheduled flights. Regional Airlines Status coverage will only be based on actual gate times rather than estimated times. This July result in some airlines / airports being excluded from this report. If you would like to review your flight status feed with OAG pleas [email protected] MAKE SMARTER MOVES Airline Monthly OTP – July 2019 Page 1 of 1 Home GLOBAL AIRLINES – TOP 50 AND BOTTOM 50 TOP AIRLINE ON-TIME FLIGHTS On-time performance BOTTOM AIRLINE ON-TIME FLIGHTS On-time performance Airline Arrivals Rank No. flights Size Airline Arrivals Rank No. flights Size SATA International-Azores GA Garuda Indonesia 93.9% 1 13,798 52 S4 30.8% 160 833 253 Airlines S.A. XL LATAM Airlines Ecuador 92.0% 2 954 246 ZI Aigle Azur 47.8% 159 1,431 215 HD AirDo 90.2% 3 1,806 200 OA Olympic Air 50.6% 158 7,338 92 3K Jetstar Asia 90.0% 4 2,514 168 JU Air Serbia 51.6% 157 3,302 152 CM Copa Airlines 90.0% 5 10,869 66 SP SATA Air Acores 51.8% 156 1,876 196 7G Star Flyer 89.8% 6 1,987 193 A3 Aegean Airlines 52.1% 155 5,446 114 BC Skymark Airlines 88.9% 7 4,917 122 WG Sunwing Airlines Inc. -

Is the Low-Cost Long-Haul Business Model a Threat to European Major Airlines?

Pierre Rolland Is the low-cost long-haul business model a threat to European major airlines? Metropolia University of Applied Sciences Bachelor of Business Administration European Business Administration Bachelor’s Thesis 28/04/2021 Abstract Author Pierre Rolland Title Is the low-cost long-haul business model a threat to European major airlines? Number of Pages 40 pages + 5 appendices Date 28th April 2021 Degree Bachelor of Business Administration Degree Programme European Business Administration Instructor/Tutor Daryl Chapman, Senior Lecturer The objective of this thesis is to understand the low-cost air market in Europe and identify the differences to explain to what extent the low-cost long-haul business is a threat to the European major airlines. This thesis consists of an explanation of the different low-cost long-haul air-market strategies in Europe, observe their development, successes and failures, and analyse their impact on the major airlines. The result of this research shows us that the low-cost model has affected the traditional model, and that major airlines have to adapt their offers to retain their clients. We also find out that the low-cost strategy that applies to the long-haul is not and cannot be the same as the short and medium-haul strategy. Keywords Low-Cost Airlines, Norwegian Air Shuttle, Business Model, Europe, Long-haul, COVID-19 Contents Glossary 1 Introduction 1 2 Current state of the air transport market 3 2.1 Air transport in Europe 4 2.1.1 The medium-haul 6 2.1.2 The long-haul 7 2.2 Low-cost companies 8 -

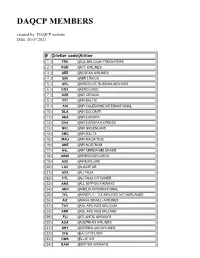

DAQCP MEMBERS Created By: DAQCP Website Date: 20.07.2021

DAQCP MEMBERS created by: DAQCP website Date: 20.07.2021 # 3-letter code Airline 1 FRH ACE BELGIUM FREIGHTERS 2 RUN ACT AIRLINES 3 AEE AEGEAN AIRLINES 4 EIN AER LINGUS 5 AFL AEROFLOT RUSSIAN AIRLINES 6 BOX AEROLOGIC 7 KZR AIR ASTANA 8 BTI AIR BALTIC 9 ACI AIR CALEDONIE INTERNATIONAL 10 DLA AIR DOLOMITI 11 AEA AIR EUROPA 12 OVA AIR EUROPA EXPRESS 13 GRL AIR GREENLAND 14 AMC AIR MALTA 15 MAU AIR MAURITIUS 16 ANE AIR NOSTRUM 17 ASL AIR SERBIA BELGRADE 18 ABW AIRBRIDGECARGO 19 AXE AIREXPLORE 20 LAV ALBASTAR 21 AZA ALITALIA 22 CYL ALITALIA CITYLINER 23 ANA ALL NIPPON AIRWAYS 24 AEH AMELIA INTERNATIONAL 25 TFL ARKEFLY - TUI AIRLINES NETHERLANDS 26 AIZ ARKIA ISRAELI AIRLINES 27 TAY ASL AIRLINES BELGIUM 28 ABR ASL AIRLINES IRELAND 29 FLI ATLANTIC AIRWAYS 30 AUA AUSTRIAN AIRLINES 31 AHY AZERBAIJAN AIRLINES 32 CFE BA CITYFLYER 33 BMS BLUE AIR 34 BAW BRITISH AIRWAYS 35 BEL BRUSSELS AIRLINES 36 GNE BUSINESS AVIATION SERVICES GUERNSEY LTD 37 CLU CARGOLOGICAIR 38 CLX CARGOLUX AIRLINES INTERNATIONAL S.A 39 ICV CARGOLUX ITALIA 40 CEB CEBU PACIFIC 41 BCY CITYJET 42 CFG CONDOR FLUGDIENST GMBH 43 CTN CROATIA AIRLINES 44 CSA CZECH AIRLINES 45 DLH DEUTSCHE LUFTHANSA 46 DHK DHL AIR LTD. 47 EZE EASTERN AIRWAYS 48 EJU EASYJET EUROPE 49 EZS EASYJET SWITZERLAND 50 EZY EASYJET UK 51 EDW EDELWEISS AIR 52 ELY EL AL 53 UAE EMIRATES 54 ETH ETHIOPIAN AIRLINES 55 ETD ETIHAD AIRWAYS 56 MMZ EUROATLANTIC 57 BCS EUROPEAN AIR TRANSPORT 58 EWG EUROWINGS 59 OCN EUROWINGS DISCOVER 60 EWE EUROWINGS EUROPE 61 EVE EVELOP AIRLINES 62 FIN FINNAIR 63 FHY FREEBIRD AIRLINES 64 GJT GETJET AIRLINES 65 GFA GULF AIR 66 OAW HELVETIC AIRWAYS 67 HFY HI FLY 68 HBN HIBERNIAN AIRLINES 69 HOP HOP! 70 IBE IBERIA 71 ICE ICELANDAIR 72 ISR ISRAIR AIRLINES 73 JAL JAPAN AIRLINES CO. -

U.S. Department of Transportation Federal

U.S. DEPARTMENT OF ORDER TRANSPORTATION JO 7340.2E FEDERAL AVIATION Effective Date: ADMINISTRATION July 24, 2014 Air Traffic Organization Policy Subject: Contractions Includes Change 1 dated 11/13/14 https://www.faa.gov/air_traffic/publications/atpubs/CNT/3-3.HTM A 3- Company Country Telephony Ltr AAA AVICON AVIATION CONSULTANTS & AGENTS PAKISTAN AAB ABELAG AVIATION BELGIUM ABG AAC ARMY AIR CORPS UNITED KINGDOM ARMYAIR AAD MANN AIR LTD (T/A AMBASSADOR) UNITED KINGDOM AMBASSADOR AAE EXPRESS AIR, INC. (PHOENIX, AZ) UNITED STATES ARIZONA AAF AIGLE AZUR FRANCE AIGLE AZUR AAG ATLANTIC FLIGHT TRAINING LTD. UNITED KINGDOM ATLANTIC AAH AEKO KULA, INC D/B/A ALOHA AIR CARGO (HONOLULU, UNITED STATES ALOHA HI) AAI AIR AURORA, INC. (SUGAR GROVE, IL) UNITED STATES BOREALIS AAJ ALFA AIRLINES CO., LTD SUDAN ALFA SUDAN AAK ALASKA ISLAND AIR, INC. (ANCHORAGE, AK) UNITED STATES ALASKA ISLAND AAL AMERICAN AIRLINES INC. UNITED STATES AMERICAN AAM AIM AIR REPUBLIC OF MOLDOVA AIM AIR AAN AMSTERDAM AIRLINES B.V. NETHERLANDS AMSTEL AAO ADMINISTRACION AERONAUTICA INTERNACIONAL, S.A. MEXICO AEROINTER DE C.V. AAP ARABASCO AIR SERVICES SAUDI ARABIA ARABASCO AAQ ASIA ATLANTIC AIRLINES CO., LTD THAILAND ASIA ATLANTIC AAR ASIANA AIRLINES REPUBLIC OF KOREA ASIANA AAS ASKARI AVIATION (PVT) LTD PAKISTAN AL-AAS AAT AIR CENTRAL ASIA KYRGYZSTAN AAU AEROPA S.R.L. ITALY AAV ASTRO AIR INTERNATIONAL, INC. PHILIPPINES ASTRO-PHIL AAW AFRICAN AIRLINES CORPORATION LIBYA AFRIQIYAH AAX ADVANCE AVIATION CO., LTD THAILAND ADVANCE AVIATION AAY ALLEGIANT AIR, INC. (FRESNO, CA) UNITED STATES ALLEGIANT AAZ AEOLUS AIR LIMITED GAMBIA AEOLUS ABA AERO-BETA GMBH & CO., STUTTGART GERMANY AEROBETA ABB AFRICAN BUSINESS AND TRANSPORTATIONS DEMOCRATIC REPUBLIC OF AFRICAN BUSINESS THE CONGO ABC ABC WORLD AIRWAYS GUIDE ABD AIR ATLANTA ICELANDIC ICELAND ATLANTA ABE ABAN AIR IRAN (ISLAMIC REPUBLIC ABAN OF) ABF SCANWINGS OY, FINLAND FINLAND SKYWINGS ABG ABAKAN-AVIA RUSSIAN FEDERATION ABAKAN-AVIA ABH HOKURIKU-KOUKUU CO., LTD JAPAN ABI ALBA-AIR AVIACION, S.L. -

Operational Performance Reporting Manchester Airport January 2018

Operational Performance Reporting Manchester Airport January 2018 Departure Punctuality - Jan-18 Last Month Last Year % Change Target Var to Target First Wave 89.7% 85.2% 4.5% 85.0% 4.7% Not First Wave 77.7% 76.3% 1.4% 85.0% -7.3% Grand Total 80.2% 78.3% 1.8% 85.0% -4.8% Departure Punctuality - Last 12 Months This Year Prev Year % Change Target Var to Target First Wave 82.5% 84.3% (1.7%) 82.0% 0.5% Not First Wave 70.8% 75.0% (4.2%) 82.0% -11.2% Grand Total 73.3% 77.1% (3.8%) 82.0% -8.7% ATMs and Passenger Volumes MTD YTD Last Year Change Last Year Change Last Year Change Last Year Change Terminal Flight Passengers Passengers % Movements Movements % Passengers Passengers % Movements Movements % Arriving 413,069 372966 11% 2681 2505 7% 5,776,415 5129198 13% 34665 32205 8% Terminal 1 Departing 380,761 341712 11% 2675 2485 8% 5,734,288 5072183 13% 34618 32139 8% Terminal 1 793,830 714678 11% 5356 4990 7% 11,510,703 10201381 13% 69283 64344 8% Total Arriving 150,070 190197 -21% 703 985 -29% 2,697,622 2756734 -2% 13450 14019 -4% Terminal 2 Departing 141,257 169277 -17% 691 973 -29% 2,676,828 2708295 -1% 13306 13984 -5% Terminal 2 291,327 359474 -19% 1394 1958 -29% 5,374,450 5465029 -2% 26756 28003 -4% Total Arriving 296,088 306835 -4% 3070 3138 -2% 3,662,711 3502730 5% 35171 33713 4% Terminal 3 Departing 282,123 283528 -0% 3074 3131 -2% 3,644,398 3443729 6% 35170 33682 4% Terminal 3 578,211 590363 -2% 6144 6269 -2% 7,307,109 6946459 5% 70341 67395 4% Total Grand Total 1,663,368 1664515 -0% 12894 13217 -2% 24,192,262 22612869 7% 166380 159742