Waypoint-Malaysian-Aviation-Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Malaysia, September 2006

Library of Congress – Federal Research Division Country Profile: Malaysia, September 2006 COUNTRY PROFILE: MALAYSIA September 2006 COUNTRY Formal Name: Malaysia. Short Form: Malaysia. Term for Citizen(s): Malaysian(s). Capital: Since 1999 Putrajaya (25 kilometers south of Kuala Lumpur) Click to Enlarge Image has been the administrative capital and seat of government. Parliament still meets in Kuala Lumpur, but most ministries are located in Putrajaya. Major Cities: Kuala Lumpur is the only city with a population greater than 1 million persons (1,305,792 according to the most recent census in 2000). Other major cities include Johor Bahru (642,944), Ipoh (536,832), and Klang (626,699). Independence: Peninsular Malaysia attained independence as the Federation of Malaya on August 31, 1957. Later, two states on the island of Borneo—Sabah and Sarawak—joined the federation to form Malaysia on September 16, 1963. Public Holidays: Many public holidays are observed only in particular states, and the dates of Hindu and Islamic holidays vary because they are based on lunar calendars. The following holidays are observed nationwide: Hari Raya Haji (Feast of the Sacrifice, movable date); Chinese New Year (movable set of three days in January and February); Muharram (Islamic New Year, movable date); Mouloud (Prophet Muhammad’s Birthday, movable date); Labour Day (May 1); Vesak Day (movable date in May); Official Birthday of His Majesty the Yang di-Pertuan Agong (June 5); National Day (August 31); Deepavali (Diwali, movable set of five days in October and November); Hari Raya Puasa (end of Ramadan, movable date); and Christmas Day (December 25). Flag: Fourteen alternating red and white horizontal stripes of equal width, representing equal membership in the Federation of Malaysia, which is composed of 13 states and the federal government. -

Malaysia Civil Helicopters

YEAR END 2017 MALAYSIA CIVIL HELICOPTERS Sponsored by ASIA PACIFIC REGION CIVIL HELICOPTER FLEET REPORT – YEAR END 2016 1 MALAYSIA Total Fleet : 157 y yearend 2017, there were 157 helicopters in Medium-size helicopters are the most widely-used in Malaysia, Malaysia, a slight 1.9% increase from the previous with 63 helicopters in the country’s fleet categorized as such. B year’s fleet of 154. However, this category has been contracting since 2015 and it is the only size that saw contraction during 2016-2017. The light- Airbus continued to have the largest share among all OEMs, twin and single-engine categories have nearly the same share in with 54% (85) of the fleet, a 3.7% growth from the previous year. the market, with 40 and 36, respectively. Leonardo followed representing 22% (35) of the fleet, largely composed of AW139s, primarily used in the offshore segment. In terms of operators, Weststar Aviation (Weststar) and MHS Aviation, both of which provide support to the O&G industry, Overall, Malaysia continued to be a dominant player in offshore operate the largest fleets making up nearly 24% of the country’s operations, represented by a 27% (43) share in the market, total fleet. despite a 10.4% contraction in fleet size. Helicopters used for multi-mission use were widely-used, expanding from the previous year, with 25% (39) of the fleet in this category. Corporate mission use followed, making up 17% (26) of the fleet. 2 CIVIL HELICOPTER FLEET REPORT – YEAR END 2017 : MALAYSIA COUNTRY PROFILE : MALAYSIA 49+0+0 30+0+027+0+018+0+011+0+010+0+06+0+0 -

Vea Un Ejemplo

3 To search aircraft in the registration index, go to page 178 Operator Page Operator Page Operator Page Operator Page 10 Tanker Air Carrier 8 Air Georgian 20 Amapola Flyg 32 Belavia 45 21 Air 8 Air Ghana 20 Amaszonas 32 Bering Air 45 2Excel Aviation 8 Air Greenland 20 Amaszonas Uruguay 32 Berjaya Air 45 748 Air Services 8 Air Guilin 20 AMC 32 Berkut Air 45 9 Air 8 Air Hamburg 21 Amelia 33 Berry Aviation 45 Abu Dhabi Aviation 8 Air Hong Kong 21 American Airlines 33 Bestfly 45 ABX Air 8 Air Horizont 21 American Jet 35 BH Air - Balkan Holidays 46 ACE Belgium Freighters 8 Air Iceland Connect 21 Ameriflight 35 Bhutan Airlines 46 Acropolis Aviation 8 Air India 21 Amerijet International 35 Bid Air Cargo 46 ACT Airlines 8 Air India Express 21 AMS Airlines 35 Biman Bangladesh 46 ADI Aerodynamics 9 Air India Regional 22 ANA Wings 35 Binter Canarias 46 Aegean Airlines 9 Air Inuit 22 AnadoluJet 36 Blue Air 46 Aer Lingus 9 Air KBZ 22 Anda Air 36 Blue Bird Airways 46 AerCaribe 9 Air Kenya 22 Andes Lineas Aereas 36 Blue Bird Aviation 46 Aereo Calafia 9 Air Kiribati 22 Angkasa Pura Logistics 36 Blue Dart Aviation 46 Aero Caribbean 9 Air Leap 22 Animawings 36 Blue Islands 47 Aero Flite 9 Air Libya 22 Apex Air 36 Blue Panorama Airlines 47 Aero K 9 Air Macau 22 Arab Wings 36 Blue Ridge Aero Services 47 Aero Mongolia 10 Air Madagascar 22 ARAMCO 36 Bluebird Nordic 47 Aero Transporte 10 Air Malta 23 Ariana Afghan Airlines 36 Boliviana de Aviacion 47 AeroContractors 10 Air Mandalay 23 Arik Air 36 BRA Braathens Regional 47 Aeroflot 10 Air Marshall Islands 23 -

Malaysia, September 2006

Library of Congress – Federal Research Division Country Profile: Malaysia, September 2006 COUNTRY PROFILE: MALAYSIA September 2006 COUNTRY Formal Name: Malaysia. Short Form: Malaysia. Term for Citizen(s): Malaysian(s). Capital: Since 1999 Putrajaya (25 kilometers south of Kuala Lumpur) Click to Enlarge Image has been the administrative capital and seat of government. Parliament still meets in Kuala Lumpur, but most ministries are located in Putrajaya. Major Cities: Kuala Lumpur is the only city with a population greater than 1 million persons (1,305,792 according to the most recent census in 2000). Other major cities include Johor Bahru (642,944), Ipoh (536,832), and Klang (626,699). Independence: Peninsular Malaysia attained independence as the Federation of Malaya on August 31, 1957. Later, two states on the island of Borneo—Sabah and Sarawak—joined the federation to form Malaysia on September 16, 1963. Public Holidays: Many public holidays are observed only in particular states, and the dates of Hindu and Islamic holidays vary because they are based on lunar calendars. The following holidays are observed nationwide: Hari Raya Haji (Feast of the Sacrifice, movable date); Chinese New Year (movable set of three days in January and February); Muharram (Islamic New Year, movable date); Mouloud (Prophet Muhammad’s Birthday, movable date); Labour Day (May 1); Vesak Day (movable date in May); Official Birthday of His Majesty the Yang di-Pertuan Agong (June 5); National Day (August 31); Deepavali (Diwali, movable set of five days in October and November); Hari Raya Puasa (end of Ramadan, movable date); and Christmas Day (December 25). Flag: Fourteen alternating red and white horizontal stripes of equal width, representing equal membership in the Federation of Malaysia, which is composed of 13 states and the federal government. -

List of Caam Approved Maintenance Organisation (Amo)

06 September 2021 LIST OF CAAM APPROVED MAINTENANCE ORGANISATION (AMO) NO. ORGANISATION APPROVAL NO. APPROVAL DATE CLASS RATINGS LOCATION 1 AAR LANDING GEAR AMO/2017/16 05‐Apr‐2017 Components Other C14 – (Landing Gear) SHAH ALAM, SERVICES SDN. BHD. Than Complete SELANGOR Engines or APUs Specialised Services D1 ‐ (Non‐Destructive Testing) Liquid penetrant Magnetic particle Eddy current 2 AIRASIA X BERHAD AMO/2017/33 05‐Oct‐2007 Aircraft A1 ‐ (Aeroplanes above 5700 kg) SEPANG, (L) Airbus A330‐300 Series fitted with Rolls‐Royce SELANGOR Trent 700 Series engines 3 ADMAL SDN BHD AMO/2017/18 05‐Apr‐2017 Aircraft A1 ‐ (Aeroplanes above 5700 kg) SUBANG, (L/B) Textron Aviation 150 fitted with Continental SELANGOR TCM 0‐200‐A engine (L/B) Textron Aviation 172 M fitted with Lycoming O‐ 320‐E2D engine (L/B) Textron Aviation 172 R fitted with Lycoming IO‐ 360‐L2A engine (L/B) Textron Aviation 172 S fitted with Lycoming IO‐ 360‐L2A engine (L/B) Textron Aviation 182 R fitted with Continental O‐470‐U engine (L/B) Textron Aviation 208B fitted with Pratt & Whitney Canada PT6A‐114A (L/B) Cirrus SR20 fitted with Continental TCM IO‐ 360‐ES engine (L/B) Cirrus SR20 G3 fitted with Continental TCM IO‐ 360‐ES engine (L/B) Diamond Aircraft Industries DA 40 D fitted with Thielert TAE 125‐02‐99 Page 1 of 34 06 September 2021 NO. ORGANISATION APPROVAL NO. APPROVAL DATE CLASS RATINGS LOCATION (L/B) Diamond Aircraft Industries DA 40 NG fitted with Austro Engine E4 (L/B) Diamond Aircraft Industries DA 42 fitted with Thielert TAE 125‐02‐99 (L/B) Piper PA‐28‐161 fitted with Lycoming O‐320‐ D3G engine (L/B) Piper PA‐28‐180 fitted with Lycoming O‐360‐ A4A engines (L/B) Piper PA‐28‐181 fitted with Lycoming O‐6044M engine (L/B) Piper PA‐34‐220T fitted with Continental TSIO‐ 360‐KB engine (L/B) Textron Aviation P206C fitted with Continental 10‐520‐A engine 4 AERO CLIQUE SDN. -

THE PROTECTION of CONSUMER RIGHTS for AVIATION SAFETY and SECURITY in INDONESIA and MALAYSIA Annalisa Yahanan1, Febrian2, and Rohani Abdul Rahim3

[21-34] Annalisa Yahanan, Febrian, and Rohani Abdul Rahim Editorial Office: Faculty of Law, Sriwijaya UniversityJalan Srijaya Negara, Palembang, South Sumatra 30139, Indonesia. Phone: +62711-580063Fax: +62711-581179 ISSN Print: 2541-5298 E-mail: [email protected]| [email protected] ISSN Online: 2541-6464 Website: http://journal.fh.unsri.ac.id/index.php/sriwijayalawreview THE PROTECTION OF CONSUMER RIGHTS FOR AVIATION SAFETY AND SECURITY IN INDONESIA AND MALAYSIA Annalisa Yahanan1, Febrian2, and Rohani Abdul Rahim3 Abstract: Indonesia and Malaysia have a good potency for cooperation in aviation industry. It can be seen in the establishing two aviation companies namely PT. Indonesia Air Asia and Ma- lindo which both are low-cost carrier. These aviation industries are categorized as low-cost car- rier, however safety and security are absolute factors because these are rights for consumers. This article will describe further about safety and security standard; protecting the rights for consumers in connection with safety aviation in Indonesia and Malaysia from the Consumer Protection Law and the Aviation Law. As a result of the research shows that safety standard passenger for air transportation in airport covers information and safety facility in the shape of availability of the emergency safety tools (fires, accidents and natural disasters); information, area and health facility; and healthcare workers. Moreover, safety standards for passenger in an aircraft include information and safety facility in the shape of availability information and the emergency safety tools for passenger in an aircraft. The protection for consumer rights for safe- ty flight in Indonesia as follows: aviation industry has obligation to fulfill minimum standard of safety and security; consumers must be safety from false information which raises concern; air- craft operation which endanger of the passenger; and consumer protection in operating the elec- tronic device which endanger flight. -

Influencing of Interactional Justice and Customer Orientation on Customers Satisfaction to Attain Their Loyalty Among Customers of Airasia

PSYCHOLOGY AND EDUCATION (2020) 57(9): 6409-6420 ISSN: 00333077 Influencing of Interactional Justice and Customer Orientation on Customers Satisfaction to Attain their Loyalty among Customers of AirAsia Amer Alsalhi1*, Dr.Fazli Idris2 , Dr.Syed Shah Alam3 1,2Graduate School of Business, Universiti Kebangsaan Malaysia 3Faculty of Business, Finance and Hospitality, MAHSA University * [email protected] ABSTRACT For service organizations to enhance the level of their customers’ loyalty and satisfaction, they need to employ people who has a substantial amount of knowledge and experiences regarding communicating and dealing with clients. This study aims to examine the impact of interactional justice and customer orientation of flight attendants working under AirAsia Malaysia on customer loyalty with customer satisfaction as a mediator. This study used a self-administrated questionnaire. 398 questionnaires were distributed to passengers of Malaysia AirAsia. The outcomes displayed three important findings: first, the relationship between interactional justice and customer orientation positively influence customer satisfaction. Second, customer satisfaction is partially mediated the relationship between interactional justice with customer loyalty and also the relationship between customer orientation and customer loyalty. Third, customer satisfaction affects customer loyalty positively. This study will provide invaluable input to airlines in understanding the importance of interactional justice and customer orientation in enhancing customer satisfaction and customer loyalty. Keywords (Times New Roman, bold, 9) Interactional justice, customer orientation, flight attendants, Malaysia AirAsia, customer satisfaction, customer loyalty Article Received: 10 August 2020, Revised: 25 October 2020, Accepted: 18 November 2020 Introduction company. Traveler satisfaction with a services or product is based upon the efficiency of the business (Kalaiarasan et al., Air transport and tourism have always been interconnected, 2015). -

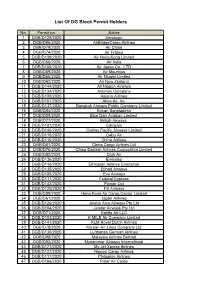

List of DG Block Permit Holders

List Of DG Block Permit Holders No. Permit no. Airline 1 DGB/D129/2020 Aerologic 2 DGB/D96/2020 AirBridgeCargo Airlines 3 DGB/D79/2020 Air China 4 DGB/D74/2020 Air France 5 DGB/D139/2020 Air Hong Kong Limited 6 DGB/D55/2020 Air India 7 DGB/D108/2020 Air Japan Co., LTD 8 DGB/D69/2020 Air Mauritius 9 DGB/D66/2020 Air Niugini Limited 10 DGB/D62/2020 Air New Zealand 11 DGB/D144/2020 All Nippon Airways 12 DGB/D134/2020 Antonov Company 13 DGB/D100/2020 Asiana Airlines 14 DGB/D107/2020 Atlas Air, Inc 15 DGB/D137/2020 Bangkok Airways Public Company Limited 16 DGB/D94/2020 Biman Bangladesh 17 DGB/D59/2020 Blue Dart Aviation Limited 18 DGB/D77/2020 British Airways 19 DGB/D101/2020 Cargolux 20 DGB/D140/2020 Cathay Pacific Airways Limited 21 DGB/D119/2020 Cebu Air 22 DGB/D110/2020 China Airlines 23 DGB/D81/2020 China Cargo Airlines Ltd 24 DGB/D76/2020 China Eastern Airlines Corporation Limited 25 DGB/D82/2020 Druk Air 26 DGB/D136/2020 Emirates 27 DGB/D116/2020 Ethiopian Airlines Enterprise 28 DGB/D135/2020 Etihad Airways 29 DGB/D105/2020 Eva Airways 30 DGB/D111/2020 Federal Express 31 DGB/D142/2020 Finnair Oyj 32 DGB/D120/2020 Fiji Airways 33 DGB/D89/2020 Hong Kong Air Cargo Carrier Limited 34 DGB/D61/2020 Japan Airlines 35 DGB/D126/2020 Jetstar Asia Airways Pte Ltd 36 DGB/D104/2020 Jetstar Airways Pty Ltd 37 DGB/D71/2020 Kalitta Air LLC 38 DGB/D103/2020 K-MILE Air Company Limited 39 DGB/D141/2020 KLM Royal Dutch Airlines 40 DGB/D78/2020 Korean Air Lines Company Ltd 41 DGB/D130/2020 Lufthansa German Airlines 42 DGB/D98/2020 Malaysia Airlines Berhad 43 DGB/D92/2020 Mynammar Airways International 44 DGB/D121/2020 My Jet Xpress Airlines 45 DGB/D127/2020 Nippon Cargo Airlines 46 DGB/D117/2020 Philippine Airlines 47 DGB/D106/2020 Polar Air Cargo No. -

EU Ramp Inspection Programme Annual Report 2020

Ref. Ares(2021)2680747 - 21/04/2021 Flight Standards Directorate Air Operations Department EU Ramp Inspection Programme Annual Report 2020 Aggregated Information Report (01 January - 31 December 2020) Air Operations Department TE.GEN.00400-006 © European Union Aviation Safety Agency. All rights reserved. ISO9001 Certified. Proprietary document. Copies are not controlled. Confirm revision status through the EASA-Internet/Intranet. An agency of the European Union Page 1 of 88 EU Ramp Inspection Programme Annual Report 2020 EU Ramp Inspection Programme Annual Report 2020 Aggregated Information Report (01 January - 31 December 2020) Document ref. Status Date Final 21.04.2021 Contact name and address for enquiries: European Union Aviation Safety Agency Flight Standards Directorate Postfach 10 12 53 50452 Köln Germany [email protected] Information on EASA is available at: www.easa.europa.eu Report Distribution List: 1 European Commission, DG MOVE, E.4 2 EU Ramp Inspection Programme Participating States 3 EASA website Air Operations Department TE.GEN.00400-006 © European Union Aviation Safety Agency. All rights reserved. ISO9001 Certified. Proprietary document. Copies are not controlled. Confirm revision status through the EASA-Internet/Intranet. An agency of the European Union Page 2 of 88 EU Ramp Inspection Programme Annual Report 2020 Table of Contents Executive summary ........................................................................................................................................... 5 1 Introduction .............................................................................................................................................. -

CHANGE FEDERAL AVIATION ADMINISTRATION CHG 2 Air Traffic Organization Policy Effective Date: November 8, 2018

U.S. DEPARTMENT OF TRANSPORTATION JO 7340.2H CHANGE FEDERAL AVIATION ADMINISTRATION CHG 2 Air Traffic Organization Policy Effective Date: November 8, 2018 SUBJ: Contractions 1. Purpose of This Change. This change transmits revised pages to Federal Aviation Administration Order JO 7340.2H, Contractions. 2. Audience. This change applies to all Air Traffic Organization (ATO) personnel and anyone using ATO directives. 3. Where Can I Find This Change? This change is available on the FAA website at http://faa.gov/air_traffic/publications and https://employees.faa.gov/tools_resources/orders_notices. 4. Distribution. This change is available online and will be distributed electronically to all offices that subscribe to receive email notification/access to it through the FAA website at http://faa.gov/air_traffic/publications. 5. Disposition of Transmittal. Retain this transmittal until superseded by a new basic order. 6. Page Control Chart. See the page control chart attachment. Original Signed By: Sharon Kurywchak Sharon Kurywchak Acting Director, Air Traffic Procedures Mission Support Services Air Traffic Organization Date: October 19, 2018 Distribution: Electronic Initiated By: AJV-0 Vice President, Mission Support Services 11/8/18 JO 7340.2H CHG 2 PAGE CONTROL CHART Change 2 REMOVE PAGES DATED INSERT PAGES DATED CAM 1−1 through CAM 1−38............ 7/19/18 CAM 1−1 through CAM 1−18........... 11/8/18 3−1−1 through 3−4−1................... 7/19/18 3−1−1 through 3−4−1.................. 11/8/18 Page Control Chart i 11/8/18 JO 7340.2H CHG 2 CHANGES, ADDITIONS, AND MODIFICATIONS Chapter 3. ICAO AIRCRAFT COMPANY/TELEPHONY/THREE-LETTER DESIGNATOR AND U.S. -

Waypoint Report: Malaysian Aviation Industry Outlook

WAYPOINT WAYPOINT MALAYSIAN AVIATION INDUSTRY OUTLOOK DECEMBER 2019 KEY HIGHLIGHTS Robust passenger traffic growth in 2020 For the first six months of 2019, passenger traffic grew by 5.2% YoY (1H18: 3.3% YoY) to 53.1mn, where domestic traffic registered a strong growth of 9.1% YoY on the back of domestic seat capacity growth of 7.8% YoY. This was slightly higher than MAVCOM’s initial expectation of domestic seat capacity growth of 7.3% YoY for 2019. Additionally, passenger traffic at non-KUL airports grew by 9.8% YoY ahead of KUL’s growth of 2.0% YoY. MAVCOM revised its 2019 passenger traffic growth forecast to 6.4% – 7.0% YoY (previous: 2.9% – 4.1% YoY) which translates into 109.1mn – 109.7mn passengers (2018: 102.5mn). For 2020, passenger traffic is anticipated to grow between 5.0% YoY and 6.0% YoY as demand is expected to be supported by domestic seat capacity growth of 3.2% YoY. Higher tourist arrivals by air in 2019 In 1H19, tourist arrivals by air into Malaysia increased by 0.4mn to 4.8mn, which corresponded to an 8.8% YoY growth. The share of total tourist arrivals by air increased to 36.0% (1H18: 34.7%). Similarly, total tourist arrivals increased by 4.9% YoY to 13.4mn (1H18: -1.7% YoY) for the same period. This was attributable to higher tourist arrivals from Indonesia, China, and Thailand, which offset a decline in tourist arrivals from Singapore and Brunei. Collectively, these five countries made up 78.0% of the total tourist arrivals of 13.4mn in 1H19. -

List of Industrial Partners

LIST OF INDUSTRIAL PARTNERS BIL COMPANY NAME ADDRESS STATE TEL. NO FAX. NO 1 3M MALAYSIA SDN BHD BANGUNAN 3M, PERSIARAN TROPICANA, 47410 PETALING SELANGOR 03-78062888 03-780662902 JAYA 2 4U-TECH CORPORATION SDN BHD 28A JLN PEKAKA 8/3 KOTA DAMANSARA 47810 PETALING SELANGOR 03-61405258 03-61560265 JAYA 3 A FARMOSA RESORT HOTEL SDN JLN KEMUS SIMPANG EMPAT 78000 ALOR GAJAH MELAKA 06-5528388 06-5528107 BHD 4 A PLUS MANUFACTURING LOT 15803, JALAN SIBU, TAMAN TUNKU,98000 MIRI, SARAWAK 0085-611139 0085-611039 (SARAWAK) SDN BHD SARAWAK 5 A PLUS MANUFACTURING SDN BHD 194-B, JALAN TUDM, KAMPUNG BARU SUBANG,40150 SHAH SELANGOR 03-78469397 03-78469404 ALAM 6 A RASHID ENTERPRISE 1763-3 SRI PUNGGOR ALAI 75460 MELAKA 012-6383410 06-2615410 7 A S KOMASU BATTERY 8, JALAN UTARA DUAKAW PERUSAHAAN MERGONG, JALAN KEDAH 04-7338942 04-7337651 TECHNOLOGY SDN BHD LENCONG BARAT, 05150 ALOR SETAR KEDAH 8 A&H ELECTRIC SDN BHD 39-M JLN SBC 1 TMN SRI BATU CAVES 68100 BATU CAVES SELANGOR 03-61887300 03-61899300 9 A&T ELECTRICAL ENGINEERING SDN 29 JLN SELAT SELATAN 14 PORTLAND INDUSTRIAL PARK SELANGOR 03-31670281 03-31670284 BHD PANDAMARAN 42000 PORT KELANG 10 A. & H. MEYER SDN. BHD. NO: 3, JALAN ASTAKA U8/84 SECTION U8, BUKIT JELUTONG SELANGOR 03-78457277 03-78452155 SHAH ALAM 40150 11 A.M OFFICE GROUP INDUSTRIES LOT PT 2333, KAMPUNG BARU SG. BULOH SUNGAI BULOH SELANGOR 03-61577336 03-61569089 SDN BHD 47000 12 A.P.A.I. ENGINEERING SDN BHD NO 53 PERSIARAN VENICE SUTERA 1 DESA MANJUNG RAYA PERAK 05-6885986 05-6888275 32200 LUMUT 13 A1 Niaga Sdn Bhd NO.