Current Status of the Telecommunications Business In

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Softbank Corp. Annual Report 2019 Softbank Corp

SoftBank Corp. Annual Report 2019 SoftBank Corp. We don’t just dream. We make things happen. We’re going beyond just being a carrier — we’re transforming into a visionary platformer. We don’t just dream up things. We take the world’s advanced ideas, and turn them into reality with our drive to make things happen. We do this so tomorrow’s people will be the happiest in human history. SoftBank Corp. ANNUAL REPORT 2019 1 Introducing Our First Annual Report SoftBank Group Corporate Philosophy Ken Miyauchi President & CEO Information Revolution SoftBank Corp. — Happiness for Everyone In December 2018, SoftBank Corp. (the “Company” or “SoftBank”) of this technological evolution, SoftBank has expanded its business listed its shares on the First Section of the Tokyo Stock Exchange. scale in step with society’s growth. The second is our ability to grow I would like to begin by expressing my sincere gratitude to our businesses. We have expanded our business operations by bringing shareholders, investors, and other stakeholders for their support together and regenerating companies in crisis, including JAPAN to date. TELECOM CO., LTD., Vodafone K.K., WILLCOM, Inc., and eAccess Ltd. The third is our ability to overcome adverse environments. In its role as a strategic holding company, our parent company Sometimes, we have faced headwinds, but we have always taken SoftBank Group Corp. (“SoftBank Group”). is accelerating the pace on adverse situations directly, focused on self-improvement, and of global investment in accordance with the Cluster of No. 1 AI thereby achieved further growth. Strategy. Meanwhile, as the primary operating company in Japan With a view to communicating our growth strategy and related and with the telecommunications business at its core, SoftBank is initiatives more clearly, we have issued our first annual report, Since our founding, the SoftBank Group has sought to use the engaging in a wide range of businesses. -

Recent Development of Net Neutrality Conditions in Japan: Impact of Fiber Wholesale and Long-Term Evolution (LTE)

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Jitsuzumi, Toshiya Conference Paper Recent Development of Net Neutrality Conditions in Japan: Impact of Fiber Wholesale and Long-term Evolution (LTE) 26th European Regional Conference of the International Telecommunications Society (ITS): "What Next for European Telecommunications?", Madrid, Spain, 24th-27th June, 2015 Provided in Cooperation with: International Telecommunications Society (ITS) Suggested Citation: Jitsuzumi, Toshiya (2015) : Recent Development of Net Neutrality Conditions in Japan: Impact of Fiber Wholesale and Long-term Evolution (LTE), 26th European Regional Conference of the International Telecommunications Society (ITS): "What Next for European Telecommunications?", Madrid, Spain, 24th-27th June, 2015, International Telecommunications Society (ITS), Calgary This Version is available at: http://hdl.handle.net/10419/127152 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. -

The United States-Japan Negotiations on Interconnection Pricing

Volume 43, Number 2, Spring 2002 Exporting Telecommunications Regulation: The United States-Japan Negotiations on Interconnection Pricing Jeffrey H. Rohlfs∗ J. Gregory Sidak∗∗ I. Introduction On February 15, 1997, seventy countries working within the framework of the World Trade Organization (WTO) agreed on a multilateral reduction of regulatory barriers to competition in international telecommunications services.1 At the time, the signatory nations to the WTO agreement on tele- communications services represented markets generating ninety-five percent of the $600 billion in global telecommunications revenues.2 Beginning January 1, 1998, those nations started a phased process to open their tele- communications markets to competition. Since 1997, the U.S. government has attempted to use the WTO agreement on telecommunications services as a vehicle for “exporting” American principles of telecommunications regula- tion to other nations. Part II of this Article explains how in 1997 the United States took the position that the WTO agreement on telecommunications services requires ∗ A.B., Amherst College, 1965; Ph.D., Massachusetts Institute of Technology, 1969. Principal, Strate- gic Policy Research, Inc., Bethesda, Maryland. ∗∗ A.B. Stanford University, 1977; A.M., J.D., Stanford University, 1981. F. K. Weyerhaeuser Fellow in Law and Economics Emeritus, American Enterprise Institute for Public Policy Research, Washington, D.C. The views expressed here are solely our own, and not those of the American Enterprise Institute, which does not take institutional positions on speciªc legislative or regulatory matters. We thank Martin Cave, Robert W. Crandall, Gary Epstein, Harold Furchtgott-Roth, Edward M. Graham, William Lake, Herbert Marks, Mark S. McConnell, John Thorne, and Masayoshi Yamashita for helpful comments. -

Federal Register/Vol. 85, No. 79/Thursday, April 23, 2020/Rules

22804 Federal Register / Vol. 85, No. 79 / Thursday, April 23, 2020 / Rules and Regulations FEDERAL COMMUNICATIONS FOR FURTHER INFORMATION CONTACT: Flexibility Analysis (FRFA) conforms to COMMISSION Anna Gentry of the Wireless the RFA. Telecommunications Bureau, Mobility Paperwork Reduction Act 47 CFR Parts 1, 2, 25, 27, and 101 Division, at (202) 418–7769 or [email protected]. For information The requirements in §§ 25.138(a) and [GN Docket No. 18–122; FCC 20–22; FRS (b); 25.147(a) through (c); 27.14(w)(1) 16548] regarding the PRA information collection requirements contained in through (4); 27.1412(b)(3)(i), (c) Expanding Flexible Use of the 3.7 to this PRA, contact Cathy Williams, Office introductory text, (c)(2), (d)(1) through 4.2 GHz Band of Managing Director, at (202) 418–2918 (2), and (f) through (h); 27.1413(a)(2) or [email protected]. and (3), (b), and (c)(3) and (7); AGENCY: Federal Communications 27.1414(b)(3), (b)(4)(i) and (iii), and SUPPLEMENTARY INFORMATION: This is a Commission. (c)(1) through (3) and (6) and (7); summary of the Commission’s Report 27.1415; 27.1416(a); 27.1417; 27.1419; ACTION: Final rule. and Order and Order of Proposed 27.1421; 27.1422(c); 27.1424; and SUMMARY: In this document, the Federal Modification in GN Docket No. 18–122, 101.101, Note (2) constitute new or Communications Commission FCC 20–22 adopted February 28, 2020 modified collections subject to the (Commission) adopts rules to reform the and released March 3, 2020. -

2820 October 1994

Telecommunications Equipment USITC Publication 2820 October 1994 OFFICE OF INDUSTRIES U.S. International Trade Commission Washington, DC 20436 UNITED STATES INTERNATIONAL TRADE COMMISSION COMMISSIONERS Peter S. Watson, Chairman Janet A. Nuzum, Vice Chairman David B. Rohr Don E. Newquist Carol T. Crawford Lynn M. Bragg Robert A. Rogowsky Director of Operations Vern Simpson Director of Industries This report was prepared principally by Lori Hylton Brown Electronic Technology and Equipment Branch Services and Electronics Division Address all communications to Secretary to the Commission United States International Trade Commission Washington, DC 20436 PREFACE In 1991 the United States International Trade Commission initiated its current Industry and Trade Summary series of informational reports on the thousands of products imported into and exported from the United States. Each summary addresses a different commodity/industry area and contains information on product uses, U.S. and foreign producers, and customs treatment. Also included is an analysis of the basic factors affecting trends in consumption, production, and trade of the commodity, as well as those bearing on the competitiveness of U.S. industries in domestic and foreign markets. 1 This report on telecommunications equipment covers the period 1989 through 1993 and represents one of approximately 250 to 300 individual reports to be produced in this series during the first half of the 1990s. Listed below are the individual summary reports published to date on the electronic equipment and technology sector. USITC publication Publication number date Title 2445 January 1992 .......... Television receivers and video monitors 2648 July 1993 ............. Measuring, testing, controlling, and analyzing instruments 2674 September 1993 ....... Medical goods 2708 December 1993 ....... -

Project Research “Application of Information and Communication Technology in Developing Countries”

Project Research “Application of Information and Communication Technology in Developing Countries” Final Report October 2015 Infrastructure and Peacebuilding Department Japan International Cooperation Agency Entrusted to International Development Center of Japan Foreword Japan International Cooperation Agency (JICA) has been assisting policy-making, human resource development, infrastructure development and utilization promotion in the field of Information and Communication Technology (ICT), including broadcasting, in developing countries around the world. Rapid change in the communication environment, represented by the explosive spread of mobile phones in Africa, is positively influencing the traditional assistance approach and bringing forth unique, innovative problem-solving methods across the globe. Academics report that these methods often contribute to the effective and efficient maximization of the development assistance effect, and the international development assistance organizations, such as the World Bank, are accelerating the utilization of ICT in assistance projects in various sectors. Concurrently many of the goals in “The 2030 Agenda for Sustainable Development” (commonly known as SDGs), officially adopted in September 2015, specified the importance of promoting the utilization of ICT from different perspectives. Therefore, JICA conducted this research with the aim to sort out and analyze its numerous past surveys and projects, collect and analyze cases of other organizations, and to organize basic information for the planning of strategies on mid- and long-term utilization of ICT. The research team of International Development Center of Japan (IDCJ), led by Dr. Joji Terahara, collected and analyzed enormous domestic and international resources for this research. Related departments at JICA, as well as domestic and international ICT-related companies and organizations, were also interviewed. -

ECC REPORT 143 Electronic Communications Committee

ECC REPORT 143 Electronic Communications Committee (ECC) within the European Conference of Postal and Telecommunications Administrations (CEPT) PRACTICAL IMPROVEMENTS IN HANDLING 112 EMERGENCY CALLS: CALLER LOCATION INFORMATION Lisbon, April 2010 ECC REPORT 143 Page 2 0 EXECUTIVE SUMMARY Each year in the European Union several millions of citizens dial the emergency call number to access emergency services. Due to increasing penetration of mobile telephony in the society, the share of emergency calls emanating from mobile networks is rapidly outgrowing emergency calls for fixed networks; this causes that an emergency situation mobile callers are increasingly not able to indicate the precise location for an optimum response. Similarly, VoIP services are substituting voice calls over traditional networks, customers increasingly use VoIP for emergency calls and expecting the same reliability and completeness of the emergency calls service. Location information is normally represented by data indicating the geographic position of the terminal equipment of a user. These data vary in range, indicating in a general way where the user is or very precise, pinpointing the user’s whereabouts to within a few meters. Some location data are effectively a subset of signalling data as they are necessary for setting up a telephone connection. In the framework of Enhanced emergency call services, the availability of location information must serve three main goals: Route the calls to the right emergency call centre; Locate the caller and/or the incident site. Dispatch the most appropriate emergency response team(s); The Report identify the most relevant regulatory principles applicable to caller location requirements in the context of emergency calls and analyses the location information standards produced by ETSI as a Standard Development Organization for fixed, mobile and IP communications networks. -

Global Pay TV Operator Forecasts

Global Pay TV Operator Forecasts Table of Contents Published in October 2016, this 190-page electronically-delivered report comes in two parts: A 190-page PDF giving a global executive summary and forecasts. An excel workbook giving comparison tables and country-by-country forecasts in detail for 400 operators with 585 platforms [125 digital cable, 112 analog cable, 208 satellite, 109 IPTV and 31 DTT] across 100 territories for every year from 2010 to 2021. Forecasts (2010-2021) contain the following detail for each country: By country: TV households Digital cable subs Analog cable subs Pay IPTV subscribers Pay digital satellite TV subs Pay DTT homes Total pay TV subscribers Pay TV revenues By operator (and by platform by operator): Pay TV subscribers Share of pay TV subscribers by operator Subscription & VOD revenues Share of pay TV revenues by operator ARPU Countries and operators covered: Country No of ops Operators Algeria 4 beIN, OSN, ART, Algerie Telecom Angola 5 ZAP TV, DStv, Canal Plus, Angola Telecom, TV Cabo Argentina 3 Cablevision; Supercanal; DirecTV Australia 1 Foxtel Austria 3 Telekom Austria; UPC; Sky Bahrain 4 beIN, OSN, ART, Batelco Belarus 2 MTIS, Zala Belgium 5 Belgacom; Numericable; Telenet; VOO; Telesat/TV Vlaanderen Bolivia 3 DirecTV, Tigo, Entel Bosnia 3 Telemach, M:Tel; Total TV Brazil 5 Claro; GVT; Vivo; Sky; Oi Bulgaria 5 Blizoo, Bulsatcom, Vivacom, M:Tel, Mobitel Canada 9 Rogers Cable; Videotron; Cogeco; Shaw Communications; Shaw Direct; Bell TV; Telus TV; MTS; Max TV Chile 6 VTR; Telefonica; Claro; DirecTV; -

Monthly Industry Overview

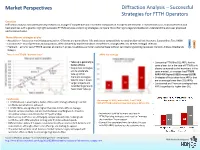

Market Perspectives Diffraction Analysis – Successful Strategies for FTTH Operators Overview Diffraction Analysis conducted primary research on a range of competitive and incumbent companies in Europe to benchmark FTTH/B services so as to analyse trends and best practices with a goal to: highlight successful FTTH/B services and pricing strategies; compare fibre offerings to legacy broadband; understand the end-user proposed and perceived value. Three different strategies at play ARPU • Acquisition – focuses on maximising penetration. Offerings are generally no frills and priced competitively to existing alternatives: Networx; Superonline; Teo; HKBN TAKE • Constrained – mix of premium and acquisition, often dictated by market condition: Rostelecom; Orange; KPN; Izzi; M-Net; Portugal Telecom - UP • Premium – aims for sexy FTTH/B services at premium prices, to address a smaller customer base without cannibalising existing revenues: Verizon; Altibox; Bredbands Bolaget There is no FTTH/B “demand issue” ARPU by strategy • Take-up is generally a • Comparing FTTH/B to DSL ARPU for the factor of time same player (or in the case of FTTH/B only • Acquisition strategies players compared to the incumbent in the aim to accelerate same market), on average has FTTH/B take-up while ARPU 46% higher (US$55 versus US$38) Premium strategies • Strategies of Acquisition have ARPUs that tend to slow it down are on average lower than DSL ARPUs • Larger projects and • Constrained and Premium strategies have incumbents generally ARPUs significantly higher than DSL -

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16

Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 1 of 137 Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 2 of 137 Exhibit A Case 20-32299-KLP Doc 208 Filed 06/01/20 Entered 06/01/20 16:57:32 Desc Main Document Page 3 of 137 Exhibit A1 Served via Overnight Mail Name Attention Address 1 Address 2 City State Zip Country Aastha Broadcasting Network Limited Attn: Legal Unit213 MezzanineFl Morya LandMark1 Off Link Road, Andheri (West) Mumbai 400053 IN Abs Global LTD Attn: Legal O'Hara House 3 Bermudiana Road Hamilton HM08 BM Abs-Cbn Global Limited Attn: Legal Mother Ignacia Quezon City Manila PH Aditya Jain S/O Sudhir Kumar Jain Attn: Legal 12, Printing Press Area behind Punjab Kesari Wazirpur Delhi 110035 IN AdminNacinl TelecomunicacionUruguay Complejo Torre De Telecomuniciones Guatemala 1075. Nivel 22 HojaDeEntrada 1000007292 5000009660 Montevideo CP 11800 UY Advert Bereau Company Limited Attn: Legal East Legon Ars Obojo Road Asafoatse Accra GH Africa Digital Network Limited c/o Nation Media Group Nation Centre 7th Floor Kimathi St PO Box 28753-00100 Nairobi KE Africa Media Group Limited Attn: Legal Jamhuri/Zaramo Streets Dar Es Salaam TZ Africa Mobile Network Communication Attn: Legal 2 Jide Close, Idimu Council Alimosho Lagos NG Africa Mobile Networks Cameroon Attn: Legal 131Rue1221 Entree Des Hydrocarbures Derriere Star Land Hotel Bonapriso-Douala Douala CM Africa Mobile Networks Cameroon Attn: Legal BP12153 Bonapriso Douala CM Africa Mobile Networks Gb, -

Fritz-Handleiding-Ziggokpn-7490.Pdf

Handleiding: Hoe sluit je de FRITZ!Box aan achter een Ziggo of KPN modem Pagina | 1 Inhoudsopgave Pagina 1 - Voorblad Pagina 2 - Inhoudsopgave Pagina 3 - Voorwoord / Tips Pagina 4 - Instellen van de taal Pagina 5 - Instellen van het land Pagina 6 - Kiezen van de Annex verbinding Pagina 7 - Kiezen van het password Pagina 8 - 9 - Kiezen van de Internet Service Provider Pagina 9 - 10 - Set Up Internet Connection / Instellen snelheid DSL line Pagina 11 - 12 - Opslaan instellingen en testen internet connectie Pagina 13 - Einde van het instellen van de internetverbinding Pagina 14 - Instellen telefonie Ziggo via de FRITZ!Box Pagina 15 - Verbindingstype telefonie kiezen Pagina 16 - Ingeven telefoonnummer / Eind instellen telefonie Pagina 17 - Slotwoord / Tel.nr Helpdesk AVM / FAQ Pagina | 2 Het instellen van de FRITZ!Box als u een Ziggo of KPN modem/router heeft Allereerst bedankt voor de aanschaf van de FRITZ!Box. Wij wensen u er veel plezier mee! Via deze handleiding lopen we stap voor stap met u door wat u moet doen om de FRITZ!Box in de juiste instellingen te krijgen. Dit neemt enkele minuten in beslag. De handleiding is alleen om uw internet en telefonie in te stellen. Aan het TV signaal verandert niets en zal gewoon via uw Ziggo of KPN modem blijven gaan. Het is aan te raden om uw Ziggo of KPN modem in Bridge mode te zetten. Dit houdt in dat de Ziggo of KPN modem geen enkel signaal meer uitzendt wat storing kan geven. Hij geeft alleen nog via de LAN 1 poort internet door naar de FRITZ!Box. -

Cell Phone City Mobile Phone Use and the Hybridization of Space in Tokyo

Cell Phone City Mobile Phone Use and the Hybridization of Space in Tokyo PhD Thesis, Urban Studies Deirdre Aranka Lucia Sneep Universität Duisburg-Essen IN-EAST School of Advanced Studies Cell Phone City Mobile Phone Use and the Hybridization of Space in Tokyo Inaugural-Dissertation zur Erlangung des akademischen Grades Doktor der Philosophie (Dr. phil.) der Fakultät für Geisteswissenschaften der Universität Duisburg-Essen vorgelegt von Deirdre Aranka Lucia Sneep aus Mülheim (Ruhr) Gutachter/Betreuer: Prof. Dr. Jens Martin Gurr and Prof. Dr. Florian Coulmas, Universität Duisburg-Essen Duisburg, 8 September 2017 Disputation: Essen, den 12. Juni 2018 1 This PhD project has been a part of the ‘Urban Systems in East Asia’ cluster of the IN-EAST School of Advanced Studies, University of Duisburg-Essen. All photographs and images in this thesis belong to the author, unless otherwise stated in the caption. Do not reproduce without permission. Diese Dissertation wird über DuEPublico, dem Dokumenten- und Publikationsserver der Universität Duisburg-Essen, zur Verfügung gestellt und liegt auch als Print-Version vor. DOI: 10.17185/duepublico/71795 URN: urn:nbn:de:hbz:464-20200610-125905-4 Alle Rechte vorbehalten. 2 TABLE OF CONTENTS 1. Introduction ............................................................................................................................................................... 6 Smartphone Citizens................................................................................................................................................