23-4 0104 Ç¥Áö.Eps

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

OSB Representative Participant List by Industry

OSB Representative Participant List by Industry Aerospace • KAWASAKI • VOLVO • CATERPILLAR • ADVANCED COATING • KEDDEG COMPANY • XI'AN AIRCRAFT INDUSTRY • CHINA FAW GROUP TECHNOLOGIES GROUP • KOREAN AIRLINES • CHINA INTERNATIONAL Agriculture • AIRBUS MARINE CONTAINERS • L3 COMMUNICATIONS • AIRCELLE • AGRICOLA FORNACE • CHRYSLER • LOCKHEED MARTIN • ALLIANT TECHSYSTEMS • CARGILL • COMMERCIAL VEHICLE • M7 AEROSPACE GROUP • AVICHINA • E. RITTER & COMPANY • • MESSIER-BUGATTI- CONTINENTAL AIRLINES • BAE SYSTEMS • EXOPLAST DOWTY • CONTINENTAL • BE AEROSPACE • MITSUBISHI HEAVY • JOHN DEERE AUTOMOTIVE INDUSTRIES • • BELL HELICOPTER • MAUI PINEAPPLE CONTINENTAL • NASA COMPANY AUTOMOTIVE SYSTEMS • BOMBARDIER • • NGC INTEGRATED • USDA COOPER-STANDARD • CAE SYSTEMS AUTOMOTIVE Automotive • • CORNING • CESSNA AIRCRAFT NORTHROP GRUMMAN • AGCO • COMPANY • PRECISION CASTPARTS COSMA INDUSTRIAL DO • COBHAM CORP. • ALLIED SPECIALTY BRASIL • VEHICLES • CRP INDUSTRIES • COMAC RAYTHEON • AMSTED INDUSTRIES • • CUMMINS • DANAHER RAYTHEON E-SYSTEMS • ANHUI JIANGHUAI • • DAF TRUCKS • DASSAULT AVIATION RAYTHEON MISSLE AUTOMOBILE SYSTEMS COMPANY • • ARVINMERITOR DAIHATSU MOTOR • EATON • RAYTHEON NCS • • ASHOK LEYLAND DAIMLER • EMBRAER • RAYTHEON RMS • • ATC LOGISTICS & DALPHI METAL ESPANA • EUROPEAN AERONAUTIC • ROLLS-ROYCE DEFENCE AND SPACE ELECTRONICS • DANA HOLDING COMPANY • ROTORCRAFT • AUDI CORPORATION • FINMECCANICA ENTERPRISES • • AUTOZONE DANA INDÚSTRIAS • SAAB • FLIR SYSTEMS • • BAE SYSTEMS DELPHI • SMITH'S DETECTION • FUJI • • BECK/ARNLEY DENSO CORPORATION -

The Drivers Behind Outward Foreign Direct Investment in the Chinese Telecommunication Sector: a Case-Based Analysis

UNIVERSITE CATHOLIQUE DE LOUVAIN LOUVAIN SCHOOL OF MANAGEMENT The drivers behind outward foreign direct investment in the Chinese telecommunication sector: A case-based analysis. Supervisor : Prof. Dr. Jean-Christophe Defraigne Project (Research) Master Thesis submitted by Midas De Bondt With a view of getting the degree Master in Management ACADEMIC YEAR 2014-2015 Foreword This thesis was motivated by my sincere interest in emerging economies the different management challenges rising from these economies. The mere fact that the world of management and especially the world of international management has changed so significantly since I started my studies, was a never ending motivation. Even though this interest had always been present, it was not until the first year of my master’s degree that this interest really surfaced during a course called “European Economic Policy” at the Louvain School of Management. It can thus hardly be called a surprise that I was delighted that Professor Jean- Christophe Defraigne accepted to be my thesis promotor. I want to start by thanking him for the excellent support and trust that he has given me to throughout the year and a bit leading up to the completion of this thesis. To continue I would like to thank all the other academics that have influenced me – and thus the content of this thesis - throughout my academic curriculum. Obviously the Louvain School of Management has played the most important role in this aspect, but I would not do justice to plenty of others by not naming them. I therefore want to thank all the professors that have taught, supported and challenged me at the KULeuven, The London School of Economics and Political Sciences and the Wharton School. -

Volte Launches

VoLTE launches Country Operator VoLTE Status VoLTE Launched Algeria Mobilis (Algerie Telecom) VoLTE Launched 01-Aug-16 Argentina Movistar (Telefónica) VoLTE Launched 25-Nov-16 Australia Telstra VoLTE Launched 16-Sep-15 Australia Vodafone (Vodafone Hutchison) VoLTE Launched 11-Jan-16 Australia Optus (Singtel) VoLTE Launched 09-May-16 Austria A1 Telekom (Telekom Austria) VoLTE Launched 30-Nov-15 Bahrain Batelco VoLTE Launched 04-May-16 Belgium Proximus VoLTE Launched 22-Nov-16 Brazil TIM (Telecom Italia) VoLTE Launched 02-Aug-16 Cambodia SEATEL (Southeast Asia Telecom) VoLTE Launched 01-Jul-15 Canada Rogers VoLTE Launched 01-Mar-15 Canada Bell (BCE) VoLTE Launched 01-Feb-16 Canada Telus VoLTE Launched 18-Apr-16 Canada EastLink (Bragg Communications) VoLTE Launched 01-Jun-16 China China Mobile VoLTE Launched 01-Aug-15 China China Unicom VoLTE Launched 12-Jan-16 Colombia Movistar (Telefónica) VoLTE Launched 01-Sep-16 Czech Republic T-Mobile (Deutsche Telekom) VoLTE Launched 01-May-15 Czech Republic Vodafone VoLTE Launched 18-Jul-16 Denmark Telenor VoLTE Launched 30-Nov-15 Estonia Telia VoLTE Launched 15-Jul-16 Finland Elisa VoLTE Launched 29-Nov-16 France Bouygues Telecom VoLTE Launched 25-Nov-15 France Orange VoLTE Launched 25-Jan-16 Germany O2 (Telefónica) VoLTE Launched 01-Apr-15 Germany Vodafone VoLTE Launched 01-May-15 Germany Telekom (Deutsche Telekom) VoLTE Launched 11-Jan-16 Hong Kong SmarTone VoLTE Launched 01-May-14 Hong Kong CSL (HKT) VoLTE Launched 01-Jul-14 Hong Kong 3 (CK Hutchison) VoLTE Launched 01-Mar-15 Hong Kong China Mobile -

Thailand Telecom Brief by Ken Zita

Thailand Telecom Brief By Ken Zita hailand has ambitions to challenge its Southeast Asian neighbors as a regional Internet and Tn ew media services hub. The economy rebounded strongly from the Asian financial crisis and the resulting consumer affluence is driving fast expansion of mobile services. The mobile penetration Political and Economic Brief 2 rate leapt spectacularly to about 42.5 percent in 2004, Economy 3 up from only 6 percent in 2000 and forms the basis for Telecom Policy Environment 4 a range of new data and content services likely to spur ICT Promotion 8 innovation in the years to come. Network operators Telecom Market Environment 11 Mobile Market 12 are posting record financial performance even as retail Other Technologies 15 prices for services continue to fall. The government is Internet 15 meanwhile forging ahead with a new high-profile tsunami warning system and ambitious e-government initiatives. Despite justly deserved optimism, Thailand faces a number of keen challenges. It has one of the most complex markets environments in the world, characterized by a maze of interlocking investment structures, lease-based infrastructure concessions and government intervention in the commercial marketplace. To circumvent a constitutional mandate requiring state ownership of “strategic” sectors such as telecom, Thailand introduced build-transfer-operate arrangements, or concessions, in the early 1990s with the two licensed monopolies, TOT and CAT. The concessions were negotiated at different times and with different terms, and some companies enjoy considerable advantages over their competitors. Thailand’s commitments to the WTO and to a bilateral trade agreement with the U.S. -

24573 Thrive APAC Post Event Report

3-5 November, 2020 122 GSMA THRIVE COUNTRIES 28 ASIA PACIFIC & TERRITORIES SESSIONS WHERE THE OVER 1,572 FUTURE OF PARTICIPATING 7,527 COMPANIES ASIA PACIFIC 12% MOBILE NETWORK SESSION ATTENDEES CONNECTS OPERATORS 5.6 JOB LEVEL ATTENDED PER ATTENDEE BREAKDOWN 293 Total connections made 51% 13% 2,938 198 Director level C-Level Total meetings arranged ATTENDEES & above #GSMAThrive // gsmathrive.com/asiapacific TOP AREAS CULTURE GROUP OF INTEREST: PARTNERSHIP SESSIONS Creating new dialogue with platform leaders including Twitter, Twitch and Go Play, these 5G sessions focused on the new frontier of music, lifestyle and shopping and examined their IOT impact on mobile networks. Artificial Intelligence Big Data/Analytics ONLINE ENGAGEMENT: Cloud Services Network Infrastructure APP/Mobile Services TOTAL VIDEO Industry 4.0/Manufacturing CLICKS Digital Commerce/Finance REACH VIEWS Digital Identity/Authentication Culture Group Partner Sessions 2,953,631 603,385 44,617 2,618,248 589,407 44,056 OF ATTENDEES WOULD ATTEND 283, 267 6,425 176 93% A FUTURE VIRTUAL EVENT 53,116 7,553 385 We have not only seen a shift in our approach to life During the special days with pandemic, GSMA Thrive Asia Pacific created great and business, but importantly, online summit experience on different topics and let us accelerate digital an opportunity to leverage the power transformation and bring more opportunities to economy growth together. “of technology to help us stay ahead in Huawei is particularly proud to be Theme & Summit Headline Sponsor and make it a great everything that we do. Our critical role is “event together. Governments in Asia Pacific are actively applying ICT technologies in to bring together the best of technologies policies to prepare for digitalization in various industries. -

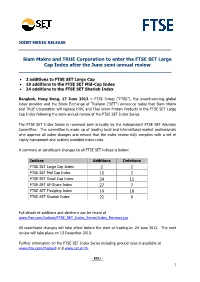

Siam Makro and TRUE Corporation to Enter the FTSE SET Large Cap Index After the June Semi-Annual Review ______

JOINT MEDIA RELEASE ___________________________________________________ Siam Makro and TRUE Corporation to enter the FTSE SET Large Cap Index after the June semi-annual review ___________________________________________________ 2 additions to FTSE SET Large Cap 10 additions to the FTSE SET Mid-Cap Index 24 additions to the FTSE SET Shariah Index Bangkok, Hong Kong, 17 June 2013 – FTSE Group (“FTSE”), the award-winning global index provider and the Stock Exchange of Thailand (“SET”) announce today that Siam Makro and TRUE Corporation will replace IRPC and Thai Union Frozen Products in the FTSE SET Large Cap Index following the semi-annual review of the FTSE SET Index Series. The FTSE SET Index Series is reviewed semi-annually by the independent FTSE SET Advisory Committee. The committee is made up of leading local and international market professionals who approve all index changes and ensure that the index review fully complies with a set of highly transparent and publicly available index rules. A summary of constituent changes to all FTSE SET indices is below: Indices Additions Deletions FTSE SET Large Cap Index 2 2 FTSE SET Mid Cap Index 10 3 FTSE SET Small Cap Index 24 11 FTSE SET All-Share Index 27 7 FTSE SET Fledgling Index 14 18 FTSE SET Shariah Index 22 9 Full details of additions and deletions can be found at www.ftse.com/Indices/FTSE_SET_Index_Series/Index_Reviews.jsp. All constituent changes will take effect before the start of trading on 24 June 2013. The next review will take place on 13 December 2013. Further information on the FTSE SET Index Series including ground rules is available at www.ftse.com/thailand and www.set.or.th. -

OSB Participant List by Research Area and Industry

OSB Participant List by Research Area and Industry Contact Centers (CC) • CPS Energy • Beijing Benz Automotive • Mack Trucks Consumer Products/Packaged • Direct Energy • Beiqi Foton Motor • Magna Goods Company • Louisville Water Company • Mazda Motor Corporation • Clarke American • BMW • Manila Electric Company • Navistar International • Newell Rubbermaid • Bosch Engineering Financial Management (FM) Solutions • Nissan Financial Services/Banking • Aerospace Brembo • Opel • Bank of America • • Advanced Coating Caterpillar • Paccar • Charles Schwab & Technologies • Company China FAW Group • Porsche Automobil • Airbus • Citigroup • China International • Proeza • Alliant Techsystems Marine Containers • Federal Reserve Bank of • • Proton Holdings Minneapolis • BE Aerospace Chrysler • John Deere • • PSA Peugeot Citroën • Bombardier Commercial Vehicle Group • Mellon Financial • PT Astra International • Cobham • Daihatsu Motor • Morgan Stanley • Rane Engine Valves • Dassault Aviation • Daimler • NetBank • Renault • European Aeronautic • Delphi • Sterling Bank Defence and Space • Robert Bosch Company • DENSO Corporation • TIAA-CREF • SAIC Motor • Finmeccanica • Denway Motors • Union National Bank • SG&G • Fuji • DGP Hinoday Industries • Washington Mutual • Sinotruk Group Jinan • General Dynamics • Eaton Commercial Vehicle • Wells Fargo • General Electric • FAW Jiefang Automotive • Ssangyong Motor Industrial Products Company • IHI Corporation • Fiat • Suzuki Motor • John Deere • Kawasaki • Ford Motor Company • Tenedora Nemark Insurance • Korean -

Volte Launches

VoLTE Launches Country Operator VoLTE Status VoLTE Launched Egypt Misr VoLTE Launched 01-Nov-18 United States of America Sprint (SoftBank) VoLTE Launched 07-Oct-18 Egypt Etisalat VoLTE Launched 25-Sep-18 South Africa MTN VoLTE Launched 13-Sep-18 Lebanon Alfa (OTMT) VoLTE Launched 12-Sep-18 Freedom Mobile (Shaw VoLTE Launched Canada Communications) 12-Aug-18 Bulgaria VIVACOM VoLTE Launched 07-Aug-18 Bulgaria Telenor (PPF) VoLTE Launched 31-Jul-18 Luxembourg Tango (Proximus) VoLTE Launched 22-Jul-18 Austria 3 (CK Hutchison) VoLTE Launched 10-Jul-18 Chile Movistar (Telefonica) VoLTE Launched 24-Jun-18 Russian Federation MTS (Sistema) VoLTE Launched 20-Jun-18 Belgium Orange VoLTE Launched 10-Jun-18 Austria T-Mobile (Deutsche Telekom) VoLTE Launched 23-May-18 Poland Play (P4) VoLTE Launched 20-May-18 Georgia MagtiCom VoLTE Launched 01-May-18 Ecuador Movistar (Telefonica) VoLTE Launched 10-Apr-18 Bahamas ALIV VoLTE Launched 31-Mar-18 India Vodafone Idea VoLTE Launched 28-Feb-18 IDC (Interdnestrkom), VoLTE Launched Moldova Transnistria 22-Dec-17 Luxembourg POST Luxembourg VoLTE Launched 13-Dec-17 Kenya Faiba (Jamii Telecom) VoLTE Launched 06-Dec-17 Armenia Ucom VoLTE Launched 04-Dec-17 Swaziland Swazi Mobile VoLTE Launched 15-Nov-17 Canada Videotron (Quebecor Media) VoLTE Launched 01-Nov-17 Bahrain Viva (STC) VoLTE Launched 22-Oct-17 Romania Digi Mobil (RCS & RDS) VoLTE Launched 19-Oct-17 Iran MTN Irancell VoLTE Launched 14-Oct-17 Iceland Nova VoLTE Launched 09-Oct-17 Mexico Telcel (America Movil) VoLTE Launched 29-Sep-17 India Airtel (Bharti -

Digital Journalism: Making News, Breaking News

MAPPING DIGITAL MEDIA: GLOBAL FINDINGS DIGITAL JOURNALISM: MAKING NEWS, BREAKING NEWS Mapping Digital Media is a project of the Open Society Program on Independent Journalism and the Open Society Information Program Th e project assesses the global opportunities and risks that are created for media by the switch- over from analog broadcasting to digital broadcasting; the growth of new media platforms as sources of news; and the convergence of traditional broadcasting with telecommunications. Th ese changes redefi ne the ways that media can operate sustainably while staying true to values of pluralism and diversity, transparency and accountability, editorial independence, freedom of expression and information, public service, and high professional standards. Th e project, which examines the changes in-depth, builds bridges between researchers and policymakers, activists, academics and standard-setters. It also builds policy capacity in countries where this is less developed, encouraging stakeholders to participate in and infl uence change. At the same time, this research creates a knowledge base, laying foundations for advocacy work, building capacity and enhancing debate. Covering 56 countries, the project examines how these changes aff ect the core democratic service that any media system should provide—news about political, economic and social aff airs. Th e MDM Country Reports are produced by local researchers and partner organizations in each country. Cumulatively, these reports provide a unique resource on the democratic role of digital media. In addition to the country reports, research papers on a range of topics related to digital media have been published as the MDM Reference Series. Th ese publications are all available at http://www.opensocietyfoundations.org/projects/mapping-digital-media. -

Company Research TRUE CORPORATION

Company Research March 3, 2020 TRUE CORPORATION BUY (TRUE TB/ TRUE.BK) Target price Bt4.90 (+49.4%) Price Bt3.28 Sharp correction is unjustified The sharp correction in the share price over the past six months suggest the negatives have been priced-in, including the core loss in 4Q19. We also expect TRUE to book losses this year, but the magnitude would be shallower than in 2019, underpinned by rising revenue. This could be a share price Phatipak NAVAWATANA catalyst. We continue to recommend a BUY rating with a TP of Bt4.9. Fundamental investment analyst on securities +662 659 7000 ext 5003 Minimal guidance for 2020 [email protected] At the analyst briefing yesterday, TRUE presented a recap of 4Q19 performance and earnings prospects for FY20 following its winning bids for 5G spectra in mid- February. We left the meeting with a neutral view as the message is in line with our view. The key takeaways were as follows: (1) TRUE gave a rough guidance Key data Unit for revenue, earnings and capex trend in 2020. Following successful marketing 12M high/ low (Bt) 6.8/ 3.2 strategies for both mobile and FBB implemented in 4Q19, the firm expects Market cap (Btm/ USDm) 109,448/ 3,484 services revenue to grow faster this year than +3.9% in 2019. TRUE also expects 3M avg. daily turnover (Btm/ USDm) 389.2/ 12.7 costs to rise at a slower pace than revenue because cost control remains a Free float (%) 67.0 Issued shares (m shares) 33,368 priority. -

Download the Thrive Asia Pacific Post Event Report

3-5 November, 2020 122 GSMA THRIVE COUNTRIES 28 ASIA PACIFIC & TERRITORIES SESSIONS WHERE THE OVER 1,572 FUTURE OF PARTICIPATING 7,527 COMPANIES ASIA PACIFIC 12% MOBILE NETWORK SESSION ATTENDEES CONNECTS OPERATORS 5.6 JOB LEVEL ATTENDED PER ATTENDEE BREAKDOWN 293 Total connections made 51% 13% 2,938 198 Director level C-Level Total meetings arranged ATTENDEES & above #GSMAThrive // gsmathrive.com/asiapacific TOP AREAS CULTURE GROUP OF INTEREST: PARTNERSHIP SESSIONS Creating new dialogue with platform leaders including Twitter, Twitch and Go Play, these 5G sessions focused on the new frontier of music, lifestyle and shopping and examined their IOT impact on mobile networks. Artificial Intelligence Big Data/Analytics ONLINE ENGAGEMENT: Cloud Services Network Infrastructure APP/Mobile Services TOTAL VIDEO Industry 4.0/Manufacturing CLICKS Digital Commerce/Finance REACH VIEWS Digital Identity/Authentication Culture Group Partner Sessions 2,953,631 603,385 44,617 2,618,248 589,407 44,056 OF ATTENDEES WOULD ATTEND 283, 267 6,425 176 93% A FUTURE VIRTUAL EVENT 53,116 7,553 385 We have not only seen a shift in our approach to life During the special days with pandemic, GSMA Thrive Asia Pacific created great and business, but importantly, online summit experience on different topics and let us accelerate digital an opportunity to leverage the power transformation and bring more opportunities to economy growth together. “of technology to help us stay ahead in Huawei is particularly proud to be Theme & Summit Headline Sponsor and make it a great everything that we do. Our critical role is “event together. Governments in Asia Pacific are actively applying ICT technologies in to bring together the best of technologies policies to prepare for digitalization in various industries. -

Qos Priority

Protecting consumer interest in broadband services 21 - 23 March 2016 New Delhi, India Sameer Sharma, Senior Advisor ITU Regional Office for Asia and the Pacific 1 ITU: A Brief Overview A specialized agency of the UN with Founded in 1865 focus on Telecommunication / ICTs 193 Member States ITU‐R:ITU’sRadio‐communication Sector globally manages radio‐frequency spectrum and satellite orbits that ensure 567 Sector Members safety of life on land, at sea and in the skies. 159 Associates 100+ Academia ITU‐T: ITU's Telecommunication Standardization Sector enables global communications by ensuring that countries’ ICT networks and devices are speaking the same language. Headquartered in ITU‐D: ITU’s Development Sector fosters Geneva, international cooperation and solidarity in the 4 Regional Offices delivery of technical assistance and in the creation, development and improvement of 7 Area Offices. telecommunication/ICT equipment and networks in developing countries. ITU: Regional Office for Asia and the Pacific 38 Member States 134 Sector Members, Associates 20 Academia Least Developed Countries (12) Land Locked Developing Countries (5) Low‐Income States (10) The Rest (10) Afghanistan Kiribati Fiji Australia Bangladesh Solomon Is. Maldives PNG D.P.R. Korea Brunei Bhutan Tuvalu Marshall Islands Samoa India China/Hong Kong Vanuatu Micronesia Cambodia Indonesia Iran Nauru Lao, PDR Mongolia Japan Tonga Nepal Pakistan Malaysia Myanmar Philippines New Zealand Timor Leste Sri Lanka R.O. Korea Small Islands Developing States (12) Vietnam Singapore Thailand 3 ITU-D Sector & Associate Members: Asia-Pacific Region 1. Afghan Wireless Communication Co.- Afghanistan 39. Nippon Telegraph and Telephone East Corporation – Japan 2. Asia Pacific Network Information Centre – Australia 40.