Company Flash Note

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SUNAC CHINA HOLDINGS LIMITED 融創中國控股有限公司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 01918)

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt about any aspect of this circular or as to the action to be taken, you should consult your licensed securities dealer or registered institution in securities, bank manager, solicitor, professional accountant or other professional advisers. If you have sold or transferred all your shares in Sunac China Holdings Limited, you should at once hand this circular together with the enclosed form of proxy to the purchaser(s) or transferee(s) or to the bank, licensed securities dealer or registered institution in securities or other agent through whom the sale or transfer was effected for transmission to the purchaser(s) or transferee(s). Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. This circular appears for information purposes only and does not constitute an invitation or offer to acquire, purchase or subscribe for any securities. SUNAC CHINA HOLDINGS LIMITED 融創中國控股有限公司 (incorporated in the Cayman Islands with limited liability) (Stock Code: 01918) (1) CONNECTED TRANSACTION — PROPOSED SHARE ISSUANCE UNDER SPECIFIC MANDATE AND (2) APPLICATION FOR WHITEWASH WAIVER Independent Financial Adviser to the Independent Board Committee and the Independent Shareholders Capitalised terms used on this cover shall have the same meanings as those defined in the section headed “Definition” in this circular, unless the context requires otherwise. -

Three Red Lines” Policy

Real Estate Developers with High Leverage to See Inventory Quality Tested Under Broader “Three Red Lines” Policy October 28, 2020 In our view, the widening of regulations aimed at controlling real estate developers’ interest- ANALYSTS bearing debt would further reduce the industry’s overall credit risk in the long term. However, the nearer term may see less headroom for highly leveraged developers to finance in the capital Xiaoliang Liu, CFA market, pushing them to sell off inventory to ease liquidity pressure. Beijing +86-10-6516-6040 The People’s Bank of China said in September that measures aimed at monitoring the funding [email protected] and financial management of key real estate developers will steadily be expanded. Media reports suggest that the new regulations would see a cap of 15% on annual growth of interest-bearing Jin Wang debt for all property developers. Developers will be assessed against three indicators, which are Beijing called “red lines”: whether asset liability ratios (excluding advance) exceeded 70%; whether net +86-10-6516-6034 gearing ratio exceeded 100%; whether cash to short-term debt ratios went below 1.0. Developers [email protected] which breached all three red lines won’t be allowed to increase their debt. If only one or two of the red lines are breached, such developers would have their interest-bearing debt growth capped at 5% and 10% respectively. The first half of the year saw debt grow rapidly among developers. In a sample of 87 real estate developers that we are monitoring, more than 40% saw their interest-bearing debt grow at a faster rate than 15% year over year as of the end of June (see the chart below). -

STOXX Hong Kong All Shares 180 Last Updated: 01.05.2015

STOXX Hong Kong All Shares 180 Last Updated: 01.05.2015 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) KYG875721634 BMMV2K8 0700.HK B01CT3 Tencent Holdings Ltd. CN HKD Y 97.0 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 71.8 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 69.5 3 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 67.4 4 3 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 59.3 5 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 46.7 6 6 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 37.7 7 10 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 32.3 8 7 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 28.9 9 9 HK0013000119 6448068 0013.HK 644806 Hutchison Whampoa Ltd. HK HKD Y 26.7 10 8 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 25.5 11 11 CNE1000003W8 6226576 0857.HK CN0065 PetroChina Co Ltd 'H' CN HKD Y 24.2 12 12 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 24.0 13 13 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 21.6 14 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 21.3 15 16 CNE100000205 B0B8Z29 3328.HK CN0054 Bank of Communications Co 'H' CN HKD Y 20.2 16 17 HK0004000045 6435576 0004.HK 643557 Wharf (Holdings) Ltd. -

China Reits Property Landlords to Shine 19

SECTOR BRIEFING number DBS Asian Insights DBS Group59 Research • May 2018 China REITs Property Landlords to Shine 19 DBS Asian Insights SECTOR BRIEFING 59 02 China REITs Property Landlords to Shine Ken HE Equity Analyst DBS (Hong Kong) [email protected] Carol WU Head of Greater China Research DBS (Hong Kong) [email protected] Danielle WANG CFA Equity Analyst DBS (Hong Kong) [email protected] Derek TAN Equity Analyst DBS Group Research [email protected] Jason LAM Equity Analyst DBS (Hong Kong) [email protected] Produced by: Asian Insights Office • DBS Group Research go.dbs.com/research @dbsinsights [email protected] Goh Chien Yen Editor-in-Chief Jean Chua Managing Editor Martin Tacchi Art Director 19 DBS Asian Insights SECTOR BRIEFING 59 03 04 Executive Summary 08 China REITs Are Lagging Edging Towards Onshore REITs Major Obstacles in Fostering 18 an Onshore REIT Regime CMBS/CMBNs Are Growing Faster C-REITs Are Imminent Which Asset Type Will Benefit 28 More? Modern Logistics Properties The Rise of Active Property Asset Management Which Developer Will Benefit From the Establishment of C-REITs? 49 Appendix DBS Asian Insights SECTOR BRIEFING 59 04 Executive Summary No REIT regime yet he real estate investment trust (REIT) has become an important investment vehicle as evidenced by its separation from the financial sector in the Global Industry Classification Standard as a sector on its own. Major Asian countries/regions have joined western countries to kickstart local versions of REITs, leaving China the last Tbig economy that has yet to have such an investment vehicle. Two major technical In our view, removing legislative obstacles (publicly traded funds are not allowed to obstacles hold commercial properties) is the first step that the government needs to take towards establishing a modern REIT regime. -

Real Estate and Construction-210204-EN

Real Estate and Construction Beijing Guangzhou Hong Kong Shanghai Shenzhen 27/F, North Tower 17/F, International Finance 26/F, One Exchange Square 24/F, HKRI Centre Two, 17/F, Tower One, Kerry Plaza Beijing Kerry Centre Place, 8 Huaxia Road, 8 Connaught Place, Central HKRI Taikoo Hui 1 Zhong Xin Si Road 1 Guanghua Road Zhujiang New Town Hong Kong 288 Shi Men Yi Road Futian District Chaoyang District Guangzhou 510623, China Shanghai 200041, China Shenzhen 518048, China Beijing 100020, China Tel: +86 10 5769 5600 Tel: +86 20 3225 3888 Tel: +852 3976 8888 Tel: +86 21 2208 1166 Tel: +86 755 8159 3999 Fax:+86 10 5769 5788 Fax:+86 20 3225 3899 Fax:+852 2110 4285 Fax:+86 21 5298 5599 Fax:+86 755 8159 3900 www.fangdalaw.com Real Estate and Construction 01 Real Estate and Construction Practice Fangda’s Real Estate and Construction Practice Team excels at providing one-stop and full-scale services to leading real estate market players, including real estate developers, real estate private equity sponsors, institutional investors, financial institutions and other corporations and individuals in complicated domestic and cross-border real estate transactions. Our lawyers are frequently appointed as arbitrators in real estate and construction-related disputes. Our strength in this area includes a combination of understanding the traditions of the Chinese market and practice and our abundant experience in serving international clients, complemented by services for non-contentious and contentious cases. We are one of the few firms based in China that can provide integrated real estate and construction related legal services, and present practical advice based on our knowledge and experience in the local market. -

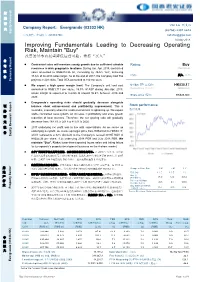

Improving Fundamentals Leading to Decreasing Operating Risk, Maintain "Buy"

股 票 研 [Table_Title] Van Liu 刘斐凡 Company Report: Evergrande (03333 HK) 究 (86755) 2397 6672 Equity Research 公司报告: 中国恒大 (03333 HK) [email protected] 14 May 2018 Improving[Table_Summary Fundamental] s Leading to Decreasing Operating Risk, Maintain "Buy" 改善的基本面展望降低运营风险,维持“买入” 公 Contracted sales will maintain steady growth due to sufficient saleable [Table_Rank] 司 Rating: Buy resources in wide geographic locations. During Jan.-Apr. 2018, contracted Maintained 报 sales amounted to RMB212.26 bn, increasing by 46.6% YoY, achieving 评级: 买入 (维持) 告 38.6% of its 2018 sales target. As at the end of 2017, the Company had 766 Company Report projects in 228 cities. Total GFA amounted to 312 mn sq.m. We expect a high gross margin level. The Company's unit land cost 6[Table_Price]-18m TP 目标价 : HK$30.17 amounted to RMB1,711 per sq.m., 16.5% of ASP during Jan.-Apr. 2018. Revised from 原目标价: HK$29.60 Gross margin is expected to remain at around 36.8% between 2018 and Share price 股价: HK$25.350 2020. 告 Evergrande’s operating risks should gradually decrease alongside 证 balance sheet enhancement and profitability improvement. This is Stock performance 报 股价表现 券 favorable, especially when the credit environment is tightening up. We expect 究 stable contracted sales growth, an increase in profitability and scale growth [Table_QuotePic] 研 reduction of land reserves. Therefore, the net gearing ratio will gradually 研 究 decrease from 183.7% in 2017 to 81.6% in 2020. 券 报 2017 underlying net profit was in line with expectations. -

STOXX Hong Kong All Shares 180 Last Updated: 01.04.2015

STOXX Hong Kong All Shares 180 Last Updated: 01.04.2015 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) KYG875721634 BMMV2K8 0700.HK B01CT3 Tencent Holdings Ltd. CN HKD Y 92.5 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 70.6 2 3 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 64.3 3 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 61.8 4 4 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 52.5 5 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 40.9 6 6 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 30.3 7 7 HK0013000119 6448068 0013.HK 644806 Hutchison Whampoa Ltd. HK HKD Y 26.2 8 8 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 25.3 9 16 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 25.2 10 10 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 25.0 11 9 CNE1000003W8 6226576 0857.HK CN0065 PetroChina Co Ltd 'H' CN HKD Y 21.7 12 11 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 20.9 13 12 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.9 14 13 HK0004000045 6435576 0004.HK 643557 Wharf (Holdings) Ltd. HK HKD Y 19.7 15 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 18.9 16 15 CNE100000205 B0B8Z29 3328.HK CN0054 Bank of Communications Co 'H' CN HKD Y 17.6 17 17 HK0003000038 6436557 0003.HK 643655 Hong Kong & China Gas Co. -

China Vanke (A-1)

9-314-104 REV: MAY 9, 2014 L Y N N S . P A I N E JOHN MACOMBER K E I T H C H I - H O W O N G China Vanke (A-1) For me, long term is five to ten years. For Wang Shi it’s way out there—beyond imagination. Twenty years ago when Vanke was still a very small company, he already had a very grand vision that I thought was impossible to achieve. Twelve years ago when I became the general manager, we were only a two billion RMB company. He was thinking what Vanke might look like if it's a 100 billion company. I couldn’t have imagined that we’d achieve that goal in less than 10 years. — Yu Liang, President, China Vanke China Vanke president Yu Liang surveyed the densely developed expanse of land below as his plane touched down in the southern city of Shenzhen in November 2011. Yu was eager to get back to the company’s headquarters in the suburbs of Shenzhen after several days on the road meeting with subsidiary heads, construction partners, and government officials across China. Under the leadership of its founder Wang Shi, China Vanke Co. Ltd. (Vanke) had grown from a small trading firm to China’s largest homebuilder, successfully navigating the tumultuous mix of volatile markets and ever-changing government policies that characterized China’s real estate market. For 2011, Vanke expected to sell some 10.7 million square meters of floor area, or more than 120,000 homes valued at over 120 billion RMB (about US $20 billion).1 Nonetheless, the year had been a slow one for the industry, as the central government introduced successive waves of austerity measures to bring down skyrocketing prices. -

Concessions on Land Premium Yet to Come, Initiate with “Neutral”

股 票 Research 研 究 Company Report: Henderson Land (00012 HK) Johnny Wong 王俊浩 Equity 公司报告:恒基地产 (00012 HK) +852 2509 5348 [email protected] 29 January 2018 Concessions on Land Premium Yet to Come, Initiate with “Neutral” 补地价优惠尚未来临,首予“中性”评级 公 司 HLD is a leading property developer with businesses in Hong Kong and Rating: Neutral throughout mainland China. In addition to property development and Initial 报 property investment, HLD also has department store operations, hotel 评级: 中性 (首次研究) 告 operations, ferry operations and a utility business through 4 listed companies. HLD has a wide variety in its land bank in Hong Kong including agricultural Company Report land in New Territories (44.9 million sq.ft.), old buildings acquired for 6-18m TP 目标价: HK$54.08 redevelopment and land purchased through government land auctions (24.2 million sq.ft.). Share price 股价: HK$55.200 We estimate underlying net profit to be HKD15,282 million, HKD9,929 million and HKD10,432 million in 2017-2019, respectively. Since we expect that HLD’s property development revenue recognized in 2018 will Stock performance 股价表现 decrease, the reduction will drive down the underlying net profit in that year. Underlying net margins are expected to be 57.2%, 51.0% and 44.0% in % of return 50.0 2017-2019, respectively. 40.0 Initiate with “Neutral” rating and a TP of HKD54.08, which represents a 证 32.0% discount of our 2018 NAV estimate. HLD has secured its project 30.0 券 告 pipelines in the next few years through the redevelopment of old buildings and 20.0 研 报 the conversion of agricultural land into residential development. -

Shui on Land Limited 瑞安房地產有限公司* (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 272)

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your licensed securities dealer, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Shui On Land Limited, you should at once hand this 14.63(2)(b) circular to the purchaser(s) or the transferee(s) or to the bank manager, licensed securities dealer or registered institution in securities or other agent through whom the sale or transfer was effected for transmission to the purchaser(s) or the transferee(s). Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no 14.66(1) 14.88 responsibility for the contents of this circular, make no representation as to its accuracy or completeness 14.58(1) and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. Shui On Land Limited 14.66(1) App.1B-1 瑞安房地產有限公司* (Incorporated in the Cayman Islands with limited liability) 13.51A (Stock code: 272) (1) MAJOR TRANSACTION — DISPOSAL OF THE ENTIRE ISSUED SHARE CAPITAL OF INFOSHORE INTERNATIONAL LIMITED AND ASSIGNMENT OF THE INTERCOMPANY LOANS OF INFOSHORE INTERNATIONAL LIMITED (2) MAJOR TRANSACTION — GRANT OF THE PUT OPTION Sole Financial Advisor A letter from the Board is set out on pages 6 to 18 of this circular. * For identification purposes only 31 December 2015 CONTENTS Page Definitions .............................................................. -

Investment in Shui on Land Limited Very Substantial Acquisition and Connected Transactions

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Shui On Construction and Materials Limited, you should at once hand this circular and the accompanying form of proxy to the purchaser or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser or the transferee. The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this circular, makes no 14.40 representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. * (Incorporated in Bermuda with limited liability) INVESTMENT IN SHUI ON LAND LIMITED App. 1B VERY SUBSTANTIAL ACQUISITION AND CONNECTED TRANSACTIONS Independent Financial Adviser to the Independent Board Committee A letter from the Independent Board Committee is set out on page 30 of this circular. A letter from BNP Paribas Peregrine Capital Limited, the independent financial adviser to the Independent Board Committee is set out on pages 31 to 44 of this circular. A notice convening a special general meeting of Shui On Construction and Materials Limited to be held at Room 103, 1/F Shui On Centre, 6-8 Harbour Road, Wanchai, Hong Kong, 2:30 p.m. -

SHANGHAI ZENDAI PROPERTY LIMITED 上海証大房地產有限公司 (Incorporated in Bermuda with Limited Liability) (Stock Code: 755)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. SHANGHAI ZENDAI PROPERTY LIMITED 上海証大房地產有限公司 (Incorporated in Bermuda with limited liability) (Stock code: 755) CHANGE OF NON-EXECUTIVE DIRECTORS RESIGNATION OF NON-EXECUTIVE DIRECTORS The board (the “Board”) of directors (the “Directors”) of Shanghai Zendai Property Limited (the “Company”, and together with its subsidiaries, the “Group”) announces that, with effect from 23 April 2020: 1. Mr. Gong Ping has resigned as a non-executive Director of the Company due to internal management and work needs of the Fosun Group; and 2. Ms. Jiang Zhengyan has resigned as a non-executive Director of the Company due to her resignation from the Fosun Group. Each of Mr. Gong Ping and Ms. Jiang Zhengyan has confirmed that he/she has no disagreement with the Board and there is no matter relating to his/her resignation as described above that needs to be brought to the attention of the holders of securities of the Company or The Stock Exchange of Hong Kong Limited (“Stock Exchange”). The Board would like to take this opportunity to express its gratitude to each of Mr. Gong Ping and Ms. Jiang Zhengyan for his/her contributions to the Company during his/her term of office. APPOINTMENT OF NON-EXECUTIVE DIRECTORS The Board announces that, with effect from 23 April 2020: 1.