Forecasting Implied Volatility in a Risk Management Problem

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Here We Go Again

2015, 2016 MDDC News Organization of the Year! Celebrating 161 years of service! Vol. 163, No. 3 • 50¢ SINCE 1855 July 13 - July 19, 2017 TODAY’S GAS Here we go again . PRICE Rockville political differences rise to the surface in routine commission appointment $2.28 per gallon Last Week pointee to the City’s Historic District the three members of “Team him from serving on the HDC. $2.26 per gallon By Neal Earley @neal_earley Commission turned into a heated de- Rockville,” a Rockville political- The HDC is responsible for re- bate highlighting the City’s main po- block made up of Council members viewing applications for modification A month ago ROCKVILLE – In most jurisdic- litical division. Julie Palakovich Carr, Mark Pierzcha- to the exteriors of historic buildings, $2.36 per gallon tions, board and commission appoint- Mayor Bridget Donnell Newton la and Virginia Onley who ran on the as well as recommending boundaries A year ago ments are usually toward the bottom called the City Council’s rejection of same platform with mayoral candi- for the City’s historic districts. If ap- $2.28 per gallon of the list in terms of public interest her pick for Historic District Commis- date Sima Osdoby and city council proved Giammo, would have re- and controversy -- but not in sion – former three-term Rockville candidate Clark Reed. placed Matthew Goguen, whose term AVERAGE PRICE PER GALLON OF Rockville. UNLEADED REGULAR GAS IN Mayor Larry Giammo – political. While Onley and Palakovich expired in May. MARYLAND/D.C. METRO AREA For many municipalities, may- “I find it absolutely disappoint- Carr said they opposed Giammo’s ap- Giammo previously endorsed ACCORDING TO AAA oral appointments are a formality of- ing that politics has entered into the pointment based on his lack of qualifi- Newton in her campaign against ten given rubberstamped approval by boards and commission nomination cations, Giammo said it was his polit- INSIDE the city council, but in Rockville what process once again,” Newton said. -

Machine Learning Based Intraday Calibration of End of Day Implied Volatility Surfaces

DEGREE PROJECT IN MATHEMATICS, SECOND CYCLE, 30 CREDITS STOCKHOLM, SWEDEN 2020 Machine Learning Based Intraday Calibration of End of Day Implied Volatility Surfaces CHRISTOPHER HERRON ANDRÉ ZACHRISSON KTH ROYAL INSTITUTE OF TECHNOLOGY SCHOOL OF ENGINEERING SCIENCES Machine Learning Based Intraday Calibration of End of Day Implied Volatility Surfaces CHRISTOPHER HERRON ANDRÉ ZACHRISSON Degree Projects in Mathematical Statistics (30 ECTS credits) Master's Programme in Applied and Computational Mathematics (120 credits) KTH Royal Institute of Technology year 2020 Supervisor at Nasdaq Technology AB: Sebastian Lindberg Supervisor at KTH: Fredrik Viklund Examiner at KTH: Fredrik Viklund TRITA-SCI-GRU 2020:081 MAT-E 2020:044 Royal Institute of Technology School of Engineering Sciences KTH SCI SE-100 44 Stockholm, Sweden URL: www.kth.se/sci Abstract The implied volatility surface plays an important role for Front office and Risk Manage- ment functions at Nasdaq and other financial institutions which require mark-to-market of derivative books intraday in order to properly value their instruments and measure risk in trading activities. Based on the aforementioned business needs, being able to calibrate an end of day implied volatility surface based on new market information is a sought after trait. In this thesis a statistical learning approach is used to calibrate the implied volatility surface intraday. This is done by using OMXS30-2019 implied volatil- ity surface data in combination with market information from close to at the money options and feeding it into 3 Machine Learning models. The models, including Feed For- ward Neural Network, Recurrent Neural Network and Gaussian Process, were compared based on optimal input and data preprocessing steps. -

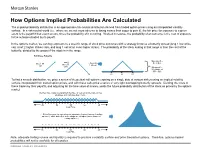

How Options Implied Probabilities Are Calculated

No content left No content right of this line of this line How Options Implied Probabilities Are Calculated The implied probability distribution is an approximate risk-neutral distribution derived from traded option prices using an interpolated volatility surface. In a risk-neutral world (i.e., where we are not more adverse to losing money than eager to gain it), the fair price for exposure to a given event is the payoff if that event occurs, times the probability of it occurring. Worked in reverse, the probability of an outcome is the cost of exposure Place content to the outcome divided by its payoff. Place content below this line below this line In the options market, we can buy exposure to a specific range of stock price outcomes with a strategy know as a butterfly spread (long 1 low strike call, short 2 higher strikes calls, and long 1 call at an even higher strike). The probability of the stock ending in that range is then the cost of the butterfly, divided by the payout if the stock is in the range. Building a Butterfly: Max payoff = …add 2 …then Buy $5 at $55 Buy 1 50 short 55 call 1 60 call calls Min payoff = $0 outside of $50 - $60 50 55 60 To find a smooth distribution, we price a series of theoretical call options expiring on a single date at various strikes using an implied volatility surface interpolated from traded option prices, and with these calls price a series of very tight overlapping butterfly spreads. Dividing the costs of these trades by their payoffs, and adjusting for the time value of money, yields the future probability distribution of the stock as priced by the options market. -

Tax Treatment of Derivatives

United States Viva Hammer* Tax Treatment of Derivatives 1. Introduction instruments, as well as principles of general applicability. Often, the nature of the derivative instrument will dictate The US federal income taxation of derivative instruments whether it is taxed as a capital asset or an ordinary asset is determined under numerous tax rules set forth in the US (see discussion of section 1256 contracts, below). In other tax code, the regulations thereunder (and supplemented instances, the nature of the taxpayer will dictate whether it by various forms of published and unpublished guidance is taxed as a capital asset or an ordinary asset (see discus- from the US tax authorities and by the case law).1 These tax sion of dealers versus traders, below). rules dictate the US federal income taxation of derivative instruments without regard to applicable accounting rules. Generally, the starting point will be to determine whether the instrument is a “capital asset” or an “ordinary asset” The tax rules applicable to derivative instruments have in the hands of the taxpayer. Section 1221 defines “capital developed over time in piecemeal fashion. There are no assets” by exclusion – unless an asset falls within one of general principles governing the taxation of derivatives eight enumerated exceptions, it is viewed as a capital asset. in the United States. Every transaction must be examined Exceptions to capital asset treatment relevant to taxpayers in light of these piecemeal rules. Key considerations for transacting in derivative instruments include the excep- issuers and holders of derivative instruments under US tions for (1) hedging transactions3 and (2) “commodities tax principles will include the character of income, gain, derivative financial instruments” held by a “commodities loss and deduction related to the instrument (ordinary derivatives dealer”.4 vs. -

Bond Futures Calendar Spread Trading

Black Algo Technologies Bond Futures Calendar Spread Trading Part 2 – Understanding the Fundamentals Strategy Overview Asset to be traded: Three-month Canadian Bankers' Acceptance Futures (BAX) Price chart of BAXH20 Strategy idea: Create a duration neutral (i.e. market neutral) synthetic asset and trade the mean reversion The general idea is straightforward to most professional futures traders. This is not some market secret. The success of this strategy lies in the execution. Understanding Our Asset and Synthetic Asset These are the prices and volume data of BAX as seen in the Interactive Brokers platform. blackalgotechnologies.com Black Algo Technologies Notice that the volume decreases as we move to the far month contracts What is BAX BAX is a future whose underlying asset is a group of short-term (30, 60, 90 days, 6 months or 1 year) loans that major Canadian banks make to each other. BAX futures reflect the Canadian Dollar Offered Rate (CDOR) (the overnight interest rate that Canadian banks charge each other) for a three-month loan period. Settlement: It is cash-settled. This means that no physical products are transferred at the futures’ expiry. Minimum price fluctuation: 0.005, which equates to C$12.50 per contract. This means that for every 0.005 move in price, you make or lose $12.50 Canadian dollar. Link to full specification details: • https://m-x.ca/produits_taux_int_bax_en.php (Note that the minimum price fluctuation is 0.01 for contracts further out from the first 10 expiries. Not too important as we won’t trade contracts that are that far out.) • https://www.m-x.ca/f_publications_en/bax_en.pdf Other STIR Futures BAX are just one type of short-term interest rate (STIR) future. -

VERTICAL SPREADS: Taking Advantage of Intrinsic Option Value

Advanced Option Trading Strategies: Lecture 1 Vertical Spreads – The simplest spread consists of buying one option and selling another to reduce the cost of the trade and participate in the directional movement of an underlying security. These trades are considered to be the easiest to implement and monitor. A vertical spread is intended to offer an improved opportunity to profit with reduced risk to the options trader. A vertical spread may be one of two basic types: (1) a debit vertical spread or (2) a credit vertical spread. Each of these two basic types can be written as either bullish or bearish positions. A debit spread is written when you expect the stock movement to occur over an intermediate or long- term period [60 to 120 days], whereas a credit spread is typically used when you want to take advantage of a short term stock price movement [60 days or less]. VERTICAL SPREADS: Taking Advantage of Intrinsic Option Value Debit Vertical Spreads Bull Call Spread During March, you decide that PFE is going to make a large up move over the next four months going into the Summer. This position is due to your research on the portfolio of drugs now in the pipeline and recent phase 3 trials that are going through FDA approval. PFE is currently trading at $27.92 [on March 12, 2013] per share, and you believe it will be at least $30 by June 21st, 2013. The following is the option chain listing on March 12th for PFE. View By Expiration: Mar 13 | Apr 13 | May 13 | Jun 13 | Sep 13 | Dec 13 | Jan 14 | Jan 15 Call Options Expire at close Friday, -

A Glossary of Securities and Financial Terms

A Glossary of Securities and Financial Terms (English to Traditional Chinese) 9-times Restriction Rule 九倍限制規則 24-spread rule 24 個價位規則 1 A AAAC see Academic and Accreditation Advisory Committee【SFC】 ABS see asset-backed securities ACCA see Association of Chartered Certified Accountants, The ACG see Asia-Pacific Central Securities Depository Group ACIHK see ACI-The Financial Markets of Hong Kong ADB see Asian Development Bank ADR see American depositary receipt AFTA see ASEAN Free Trade Area AGM see annual general meeting AIB see Audit Investigation Board AIM see Alternative Investment Market【UK】 AIMR see Association for Investment Management and Research AMCHAM see American Chamber of Commerce AMEX see American Stock Exchange AMS see Automatic Order Matching and Execution System AMS/2 see Automatic Order Matching and Execution System / Second Generation AMS/3 see Automatic Order Matching and Execution System / Third Generation ANNA see Association of National Numbering Agencies AOI see All Ordinaries Index AOSEF see Asian and Oceanian Stock Exchanges Federation APEC see Asia Pacific Economic Cooperation API see Application Programming Interface APRC see Asia Pacific Regional Committee of IOSCO ARM see adjustable rate mortgage ASAC see Asian Securities' Analysts Council ASC see Accounting Society of China 2 ASEAN see Association of South-East Asian Nations ASIC see Australian Securities and Investments Commission AST system see automated screen trading system ASX see Australian Stock Exchange ATI see Account Transfer Instruction ABF Hong -

Volatility As Investment - Crash Protection with Calendar Spreads of Variance Swaps

Journal of Applied Operational Research (2014) 6(4), 243–254 © Tadbir Operational Research Group Ltd. All rights reserved. www.tadbir.ca ISSN 1735-8523 (Print), ISSN 1927-0089 (Online) Volatility as investment - crash protection with calendar spreads of variance swaps Uwe Wystup 1,* and Qixiang Zhou 2 1 MathFinance AG, Frankfurt, Germany 2 Frankfurt School of Finance & Management, Germany Abstract. Nowadays, volatility is not only a risk measure but can be also considered an individual asset class. Variance swaps, one of the main investment vehicles, can obtain pure exposure on realized volatility. In normal market phases, implied volatility is often higher than the realized volatility will turn out to be. We present a volatility investment strategy that can benefit from both negative risk premium and correlation of variance swaps to the underlying stock index. The empirical evidence demonstrates a significant diversification effect during the financial crisis by adding this strategy to an existing portfolio consisting of 70% stocks and 30% bonds. The back-testing analysis includes the last ten years of history of the S&P500 and the EUROSTOXX50. Keywords: volatility; investment strategy; stock index; crash protection; variance swap * Received July 2014. Accepted November 2014 Introduction Volatility is an important variable of the financial market. The accurate measurement of volatility is important not only for investment but also as an integral part of risk management. Generally, there are two methods used to assess volatility: The first one entails the application of time series methods in order to make statistical conclusions based on historical data. Examples of this method are ARCH/GARCH models. -

Spread Scanner Guide Spread Scanner Guide

Spread Scanner Guide Spread Scanner Guide ..................................................................................................................1 Introduction ...................................................................................................................................2 Structure of this document ...........................................................................................................2 The strategies coverage .................................................................................................................2 Spread Scanner interface..............................................................................................................3 Using the Spread Scanner............................................................................................................3 Profile pane..................................................................................................................................3 Position Selection pane................................................................................................................5 Stock Selection pane....................................................................................................................5 Position Criteria pane ..................................................................................................................7 Additional Parameters pane.........................................................................................................7 Results section .............................................................................................................................8 -

Copyrighted Material

Index AA estimate, 68–69 At-the-money (ATM) SPX variance Affine jump diffusion (AJD), 15–16 levels/skews, 39f AJD. See Affine jump diffusion Avellaneda, Marco, 114, 163 Alfonsi, Aurelien,´ 163 American Airlines (AMR), negative book Bakshi, Gurdip, 66, 163 value, 84 Bakshi-Cao-Chen (BCC) parameters, 40, 66, American implied volatilities, 82 67f, 70f, 146, 152, 154f American options, 82 Barrier level, Amortizing options, 135 distribution, 86 Andersen, Leif, 24, 67, 68, 163 equal to strike, 108–109 Andreasen, Jesper, 67, 68, 163 Barrier options, 107, 114. See also Annualized Heston convexity adjustment, Out-of-the-money barrier options 145f applications, 120 Annualized Heston VXB convexity barrier window, 120 adjustment, 160f definitions, 107–108 Ansatz, 32–33 discrete monitoring, adjustment, 117–119 application, 34 knock-in options, 107 Arbitrage, 78–79. See also Capital structure knock-out options, 107, 108 arbitrage limiting cases, 108–109 avoidance, 26 live-out options, 116, 117f calendar spread arbitrage, 26 one-touch options, 110, 111f, 112f, 115 vertical spread arbitrage, 26, 78 out-of-the-money barrier, 114–115 Arrow-Debreu prices, 8–9 Parisian options, 120 Asymptotics, summary, 100 rebate, 108 Benaim, Shalom, 98, 163 At-the-money (ATM) implied volatility (or Berestycki, Henri, 26, 163 variance), 34, 37, 39, 79, 104 Bessel functions, 23, 151. See also Modified structure, computation, 60 Bessel function At-the-money (ATM) lookback (hindsight) weights, 149 option, 119 Bid/offer spread, 26 At-the-money (ATM) option, 70, 78, 126, minimization, -

Intraday Volatility Surface Calibration

INTRADAY VOLATILITY SURFACE CALIBRATION Master Thesis Tobias Blomé & Adam Törnqvist Master thesis, 30 credits Department of Mathematics and Mathematical Statistics Spring Term 2020 Intraday volatility surface calibration Adam T¨ornqvist,[email protected] Tobias Blom´e,[email protected] c Copyright by Adam T¨ornqvist and Tobias Blom´e,2020 Supervisors: Jonas Nyl´en Nasdaq Oskar Janson Nasdaq Xijia Liu Department of Mathematics and Mathematical Statistics Examiner: Natalya Pya Arnqvist Department of Mathematics and Mathematical Statistics Master of Science Thesis in Industrial Engineering and Management, 30 ECTS Department of Mathematics and Mathematical Statistics Ume˚aUniversity SE-901 87 Ume˚a,Sweden i Abstract On the financial markets, investors search to achieve their economical goals while simultaneously being exposed to minimal risk. Volatility surfaces are used for estimating options' implied volatilities and corresponding option prices, which are used for various risk calculations. Currently, volatility surfaces are constructed based on yesterday's market in- formation and are used for estimating options' implied volatilities today. Such a construction gets redundant very fast during periods of high volatility, which leads to inaccurate risk calculations. With an aim to reduce volatility surfaces' estimation errors, this thesis explores the possibilities of calibrating volatility surfaces intraday using incomplete mar- ket information. Through statistical analysis of the volatility surfaces' historical movements, characteristics are identified showing sections with resembling mo- tion patterns. These insights are used to adjust the volatility surfaces intraday. The results of this thesis show that calibrating the volatility surfaces intraday can reduce the estimation errors significantly during periods of both high and low volatility. -

Binomial Trees • Stochastic Calculus, Ito’S Rule, Brownian Motion • Black-Scholes Formula and Variations • Hedging • Fixed Income Derivatives

Pricing Options with Mathematical Models 1. OVERVIEW Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic and Fernando Zapatero. • What we want to accomplish: Learn the basics of option pricing so you can: - (i) continue learning on your own, or in more advanced courses; - (ii) prepare for graduate studies on this topic, or for work in industry, or your own business. • The prerequisites we need to know: - (i) Calculus based probability and statistics, for example computing probabilities and expected values related to normal distribution. - (ii) Basic knowledge of differential equations, for example solving a linear ordinary differential equation. - (iii) Basic programming or intermediate knowledge of Excel • A rough outline: - Basic securities: stocks, bonds - Derivative securities, options - Deterministic world: pricing fixed cash flows, spot interest rates, forward rates • A rough outline (continued): - Stochastic world, pricing options: • Pricing by no-arbitrage • Binomial trees • Stochastic Calculus, Ito’s rule, Brownian motion • Black-Scholes formula and variations • Hedging • Fixed income derivatives Pricing Options with Mathematical Models 2. Stocks, Bonds, Forwards Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic and Fernando Zapatero. A Classification of Financial Instruments SECURITIES AND CONTRACTS BASIC SECURITIES DERIVATIVES