AEGON N.V. (Exact Name of Registrant As Specified in Its Charter)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Outlook for the Global Economy, Interest Rates and the Impact on the Re/Insurance Industry Astrid Frey, Swiss Re Economic Research & Consulting

Outlook for the global economy, interest rates and the impact on the re/insurance industry Astrid Frey, Swiss Re Economic Research & Consulting The economic environment in 2009… Real GDP growth (%) Source: Swiss Re Economic Research & Consulting Astrid Frey | Swiss Re Economic Research & Consulting 2 … and in 2014 Real GDP growth (%) Source: Swiss Re Economic Research & Consulting Astrid Frey | Swiss Re Economic Research & Consulting 3 Table of Contents / Agenda • Outlook for the global economy, inflation and interest rates • How do interest rates affect re/insurers? • How can insurers manage interest rate risk? • Conclusions Astrid Frey | Swiss Re Economic Research & Consulting 4 Outlook for the global economy, inflation and interest rates Astrid Frey | Swiss Re Economic Research & Consulting 5 Economic indicators imply global growth acceleration Purchasing Managers Indices, monthly data PMIs are survey based indicators. Values above 50 indicate economic expansion, Sources: Datastream, values below 50 contraction Bloomberg Astrid Frey | Swiss Re Economic Research & Consulting 6 Economic recovery at different speeds Real GDP of selected euro area countries (indexed Q1 2008 = 100) Source: Datastream Astrid Frey | Swiss Re Economic Research & Consulting 7 Global economic outlook and key risks . The US expansion is expected to strengthen into 2014, driven by consumer spending, business investment and housing construction . Europe is growing again and will continue to improve – a huge improvement for global growth prospects, but growth is hampered by fiscal austerity, private deleveraging and tight credit conditions . Chinese growth will stay close to 7.5% for next several years. Some EM economies have been unsettled by Fed "tapering" discussions, but a strengthening global economy will alleviate the downside risks. -

Aegon N.V. Aegon N.V

Insurance Life Insurance Netherlands Ratings Aegon N.V. Aegon N.V. Long-Term IDR A- And Core Subsidiaries Short-Term IDR F2 Scottish Equitable Plc Insurer Financial Strength Rating A+ Transamerica Financial Life Insurance Company Key Rating Drivers Insurer Financial Strength Rating A+ Short-Term Insurer Financial WD Very Strong Business Profile: Fitch Ratings ranks Aegon N.V.’s business profile as ‘favourable’ Strength Rating compared to other Dutch insurance companies. Geographic diversification is broad; non- Transamerica Life Insurance Company Dutch assets account for about 80% of the group’s assets. Aegon has a substantial life Insurer Financial Strength Rating A+ insurance franchise in the Netherlands focusing on retirement services and savings, where it Short-Term Insurer Financial F1+ has top three market positions. It also has significant life and pension operations in the US and Strength Rating the UK. Transamerica Premier Life Insurance ‘Very Strong’ Capitalisation and Leverage: Aegon’s end-2019 Prism Factor-Based Capital Company Model (Prism FBM) score was unchanged at ‘Very Strong’ and the group’s Solvency II (S2) ratio Insurer Financial Strength Rating A+ was 201%. The S2 ratio improved to 208% in 1Q20 due to the increase of the S2 volatility Short-Term Insurer Financial WD adjuster (VA), although this was partly offset by adverse market movements in the US. The Strength Rating financial leverage ratio (FLR) decreased to 25% in 2019 on the successful issuance of Note: See additional ratings on page 8. restricted Tier 1 (RT1) notes during the year. Good Financial Performance: Aegon’s underlying earnings could weaken in 2020 due to the Outlooks impact of the coronavirus pandemic on US operations, while earnings in Europe are expected Negative to remain more resilient. -

Area Companies Offering Matching Gifts Below Is a Partial List of Area Companies Offering Matching Gifts

Area Companies Offering Matching Gifts Below is a partial list of area companies offering matching gifts. Please check to see if your employer is on the list and/or check with your company if they offer the program. If your employer offers a matching gift program, please request a matching gift form from your employer or fill out their online form. Matching gifts can be made to the Tredyffrin Township Libraries, Paoli Library or Tredyffrin Public Library. Aetna FMC Corporation PNC Financial Services AIG GATX PPG Industries Air Products and Chemicals, Inc. GE Foundation PQ Corporation Allstate Foundation GlaxoSmithKline Procter & Gamble Altria Group, Inc. Glenmede Prudential Financial American Express Company Hillman Company PVR Partners, L.P. American International Group, Inc. Houghton Mifflin Quaker Chemical Corporation AmeriGas Propane, Inc. IBM Corporation Quest Diagnostics AON J.P. Morgan Chase Ross Arkema Inc. John Hancock Saint-Gobain Corporation Automatic Data Processing Johnson & Johnson Sandmeyer Steel Company AXA Foundation, Inc. JP Morgan Chase SAP Matching Gift Program Axiom Data, Inc. Kaplan Inc. Schering-Plough Foundation Bank of America Kellogg Schroder Investment Management Bemis Company Foundation KPMG LLP Shell Oil Company Berwind Corporation Liberty Mutual State Farm Companies Foundation BlackRock Lincoln Financial Group Subaru of America Boeing Company May Department Stores Sun Life Financial BP McDonald's Sun Microsystems, Inc Bristol-Myers Squibb Company McKesson Foundation Sunoco, Inc. C. R. Bard, Inc. Merck & Co., Inc. Tenet Healthcare Foundation CertainTeed Merrill Lynch Texas Instruments Charles Schwab Merrill Lynch ACE INA Foundation Chevron Corporation Microsoft AXA Foundation Chubb Group of Insurance Companies Minerals Technologies Inc. Dow Chemical Company CIGNA Foundation Mobil Foundation Inc. -

Cross-Border Financial Institutions in the EU: Analysis of Total Assets and Ultimate Ownership

Directorate-General for Internal Policies Directorate A - Economic and Scientific Policy Policy Department A.: Economic and Scientific Policy and Quality of Life Unit Cross-Border Financial Institutions in the EU: Analysis of Total Assets and Ultimate Ownership Briefing Note IP/A/ECON/NT/2008-10 PE 408.550 Only published in English. Author: Josina KAMERLING Policy Department Economy and Science DG Internal Policies European Parliament Rue Wiertz 60 - ATR 00L046 B-1047 Brussels Tel: +32 (0)2 283 27 86 Fax: +32(0)2 284 69 29 E-mail: [email protected] Arttu MAKIPAA Policy Department Economy and Science DG Internal Policies European Parliament Rue Wiertz 60 - ATR 00L042 B-1047 Brussels Tel: +32 (0)2 283 26 20 Fax: +32(0)2 284 69 29 E-mail: [email protected] Manuscript completed in August 2008. The opinions expressed in this document do not necessarily represent the official position of the European Parliament. Reproduction and translation for non-commercial purposes are authorised provided the source is acknowledged and the publisher is given prior notice and receives a copy. Rue Wiertz – B-1047 Bruxelles - 32/2.284.43.74 Fax: 32/2.284.68.05 Palais de l‘Europe – F-67000 Strasbourg - 33/3.88.17.25.56 Fax: 33/3.88.36.92.14 E-mail: [email protected] IP/A/ECON/NT/2008-10 PE 408.550 Table of Contents 1. The Data on Financial Institutions in EU27 ......................................................................1 2. Largest Financial Institutions in Europe (Tables 1-5) .......................................................2 -

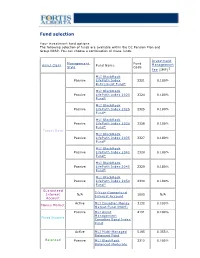

Fund Selection

Fund selection Y our investment fund options The following selection of funds are available within the DC Pension Plan and Group RRSP. You can choose a combination of these funds. Investment Management Fund Asset Class Fund Name Management Style Code Fee (IMF)1 MLI BlackRock Passive LifeP ath Index 2321 0.180% Retirement Fund* MLI BlackRock Passive LifeP ath Index 2020 2324 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2025 2325 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2030 2326 0.180% Fund* Target Date MLI BlackRock Passive LifeP ath Index 2035 2327 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2040 2328 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2045 2329 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2050 2330 0.180% Fund* Guaranteed 5-Y ear Guaranteed Interest N/A 1005 N/A Interest Account Account Active MLI Canadian Money 3132 0.100% Money Market Market Fund (MAM) Passive MLI Asset 4191 0.100% Management Fixed Income Canadian Bond Index Fund Active MLI Multi-Managed 5195 0.355% Balanced Fund Balanced Passive MLI BlackRock 2312 0.105% Balanced Moderate Index Fund Active MLI Canadian Equity 7011 0.210% Fund Canadian Passive MLI Asset 7132 0.100% Equity Management Canadian Equity Index Fund Active MLI U.S. Diversified 8196 0.375% Grow th Equity (Wellington) Fund U.S. Equity Passive MLI BlackRock U.S. 8322 0.090% Equity Index Fund* Active MLI MFS MB 8162 0.280% International Equity International Fund Equity Passive MLI BlackRock 8321 0.160% International Equity Index Fund* 1 IMFs shown do not include applicable taxes. -

NP Key Contacts.Pdf

IGP Network Partners: Key Contacts Region: Americas Country / Territory IGP Network Partner IGP Contact Email Type IGP Regional Coordinator Mr. Michael Spincemaille [email protected] Argentina SMG LIFE Mr. Nicolas Passet [email protected] Partner Brazil MAPFRE Vida S.A. Ms. Débora Nunes Santos [email protected] Partner Canada Manulife Financial Corporation Mr. Kajan Ramanathan [email protected] Partner Chile MAPFRE Chile Ms. Nathalie Gonzalez [email protected] Partner Colombia MAPFRE Colombia Ms. Ingrid Olarte Pérez [email protected] Partner Costa Rica MAPFRE Costa Rica Mr. Armando Sevilla [email protected] Partner Dominican Republic (Life) MAPFRE BHD Mrs. Alejandra Quirico [email protected] Partner Dominican Republic (Health) MAPFRE Salud ARS, S. A. Mr. Christian Wazar [email protected] Partner Ecuador MAPFRE Atlas * Mr. Carlos Zambrano [email protected] Correspondent El Salvador MAPFRE Seguros El Salvador S.A. Mr. Daniel Acosta González [email protected] Partner French Guiana Refer to France - - Partner Guadeloupe Refer to France - - Partner Guatemala MAPFRE Guatemala Mr. Luis Pedro Chavarría [email protected] Partner Honduras MAPFRE Honduras Mr. Carlos Ordoñez [email protected] Partner Martinique Refer to France - - Partner Mexico Seguros Monterrey New York Life Ms. Paola De Uriarte [email protected] Partner Nicaragua MAPFRE Nicaragua Mr. Dany Lanuza Flores [email protected] Partner Panama MAPFRE Panama Mr. Manuel Rodriguez [email protected] Partner Paraguay MAPFRE Paraguay Mr. Sergio Alvarenga [email protected] Partner Peru MAPFRE Peru Mr. Ramón Acuña Huerta [email protected] Partner Saint Martin Refer to France - - Partner Saint Barthélemy Refer to France - - Partner Saint Pierre & Miquelon Refer to France - - Partner United States Prudential Insurance Company of America Mr. -

Part VII Transfers Pursuant to the UK Financial Services and Markets Act 2000

PART VII TRANSFERS EFFECTED PURSUANT TO THE UK FINANCIAL SERVICES AND MARKETS ACT 2000 www.sidley.com/partvii Sidley Austin LLP, London is able to provide legal advice in relation to insurance business transfer schemes under Part VII of the UK Financial Services and Markets Act 2000 (“FSMA”). This service extends to advising upon the applicability of FSMA to particular transfers (including transfers involving insurance business domiciled outside the UK), advising parties to transfers as well as those affected by them including reinsurers, liaising with the FSA and policyholders, and obtaining sanction of the transfer in the English High Court. For more information on Part VII transfers, please contact: Martin Membery at [email protected] or telephone + 44 (0) 20 7360 3614. If you would like details of a Part VII transfer added to this website, please email Martin Membery at the address above. Disclaimer for Part VII Transfers Web Page The information contained in the following tables contained in this webpage (the “Information”) has been collated by Sidley Austin LLP, London (together with Sidley Austin LLP, the “Firm”) using publicly-available sources. The Information is not intended to be, and does not constitute, legal advice. The posting of the Information onto the Firm's website is not intended by the Firm as an offer to provide legal advice or any other services to any person accessing the Firm's website; nor does it constitute an offer by the Firm to enter into any contractual relationship. The accessing of the Information by any person will not give rise to any lawyer-client relationship, or any contractual relationship, between that person and the Firm. -

Manulife Global Fund Unaudited Semi-Annual Report

Unaudited Semi-Annual Report Manulife Global Fund Société d'Investissement à Capital Variable for the six month period ended 31 December 2020 No subscription can be received on the basis of nancial reports. Subscriptions are only valid if made on the bases of the current prospectus, accompanied by the latest annual report and semi-annual report if published thereaer. SICAV R.C.S Luxembourg B 26 141 Contents Directors ..................................................................................................................................................... 1 Management and Administration ............................................................................................................. 2 Directors’ Report ........................................................................................................................................ 4 Statement of Net Assets ........................................................................................................................... 10 Statement of Changes in Net Assets ........................................................................................................ 15 Statement of Operations ........................................................................................................................... 20 Statistical Information ............................................................................................................................... 25 Statement of Changes in Shares ............................................................................................................. -

Q1 2020 Building Sustainable Shareholder Value Business Overview

Q1 2020 Building Sustainable Shareholder Value Business overview Update in light of COVID-19 Business group results & highlights Capital management Asset portfolio Sustainability 2 A $26.51 billion leading global financial services organization Offices in 40,600 Employees 125,900 advisors 27 markets 2 2 2 Operating through a balanced and diversified model and focused on creating shareholder value now and in the future SUN LIFE • Q1 2020 1 Market capitalization in C$ as at March 31, 2020 3 2 As at December 31, 2019. Includes Asia joint ventures The Sun Life story • A diversified business model, with four strong pillars that can each compete, win and grow in their respective sectors and which leverage each other • Bound together by a strong balance sheet and risk culture, including no U.S. Variable Annuity or U.S. Long-Term Care • Digital transformation that is deeply embedded throughout the organization • Building on momentum created by past organic investments and acquisitions that will help drive earnings growth SUN LIFE • Q1 2020 4 Executing on our ambition to be one of the best insurance and asset management companies globally A Leader in Insurance and A Leader in U.S. Wealth Solutions in our CAN US Group Benefits Canadian Home Market A Leader in Asia A Leader in Global AM ASIA through Distribution Asset Management Excellence in Higher Growth Markets Each pillar Top quartile Disproportionate Top quartile total viewed as a Client share of top shareholder leader experience talent return SUN LIFE • Q1 2020 5 Consistently delivering value to shareholders 5-year total shareholder return1 Progress on medium-term objectives March 31, 2020 Sun Life 6.9% Medium-term objective Q1 2020 TSX 0.9% Underlying ROE2 12-14% 14.2% Canadian lifecos 0.0% Underlying EPS growth2 9% Global lifecos (1.2)% 8-10% Dividend payout ratio2 U.S. -

Demystifying Negative Screens: the Full Implications of ESG Exclusions

Marketing material for professional investors or advisers only Demystifying negative screens: The full implications of ESG exclusions December 2017 Contents Demystifying negative screens: Appendix: A close look at the full implications of ESG different screening options exclusions 14 Alcohol 3 Executive summary 15 Fossil fuels 3 Screening remains very popular 16 Fur in general 17 Gambling 4 But some individual screens are more 18 Nuclear popular than others 19 Pornography 4 Our Global Investor Survey highlights 20 Sin changing attitudes towards 21 Tobacco negative screens 22 Weapons 5 Interest in fossil fuel and tobacco divestment is rising 7 Focusing narrowly on returns can be deeply misleading 9 Screens can have a heavy impact on specific investment strategies 11 Details matter when implementing screens 11 Screen definition decisions can significantly alter exclusion lists and investment results 12 Different data providers can produce very different exclusion lists 12 Active management can add more value than passive when applying screens Demystifying negative screens: the full implications of ESG exclusions Screening out investments that Alexander Monk Sustainable do not meet environmental, social Investment Analyst or governance (ESG) criteria is and the Sustainable superficially simple but fraught with Investment Team practical challenges. Understanding the complexities and biases screens create before they are implemented and appropriately assessing performance afterward is crucial for investors. In this paper, we investigate the pitfalls when implementing different screens. Executive summary The chart in Figure 1 shows the extent to which typical Negative screens that sieve investments on environmental, negative exclusions constrain managers. Implementing social and governance grounds remain critical to many screens may be mechanical, but assessing their impact on investors. -

Besluit in Zaak 7051

Openbare versie Nederlandse Mededingingsautoriteit BESLUIT Besluit van de Raad van Bestuur van de Nederlandse Mededingingsautoriteit als bedoeld in artikel 37, eerste lid, van de Mededingingswet. Nummer 7051 / 197 Betreft zaak: 7051/ Eureko B.V. - Coöperatie De Friesland U.A. I. MELDING 1. Op 15 oktober 2010 heeft de Raad van Bestuur van de Nederlandse Mededingingsautoriteit (hierna: de Raad) een melding ontvangen van een voorgenomen concentratie in de zin van artikel 34 van de Mededingingswet. Hierin is medegedeeld dat Eureko B.V. en Coöperatie De Friesland U.A. voornemens zijn een concentratie aan te gaan in de zin van artikel 27, eerste lid, van de Mededingingswet. 2. Van de melding is mededeling gedaan in Staatscourant nr. 16764 van 22 oktober 2010. Naar aanleiding van de mededeling in de Staatscourant zijn zienswijzen van derden naar voren gebracht. Deze zienswijzen worden, voor zover er overwegingen aan zijn ontleend die dragend zijn voor dit besluit, in het navolgende nader uiteengezet. Ambtshalve zijn vragen gesteld aan verschillende marktpartijen. In onderhavige zaak is een zienswijze ontvangen van de Nederlandse Zorgautoriteit (hierna: NZa); hierop wordt in de punten 54 en 55 ingegaan. II. PARTIJEN 3. Eureko B.V. (hierna: Eureko) is een besloten vennootschap naar Nederlands recht. Zij heeft als belangrijkste aandeelhouders Vereniging Achmea, die via Stichting Administratiekantoor Achmea circa 55% van de aandelen houdt en de Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A. (hierna: Rabobank) die circa 39% van de aandelen houdt, terwijl de overige aandelen in handen zijn van strategische investeerders. Vereniging Achmea en Rabobank hebben gezamenlijke zeggenschap over Eureko.1 Eureko houdt alle aandelen in Achmea Holding N.V., een naamloze vennootschap naar Nederlands recht, die aan het hoofd staat van de Achmea Groep. -

2018 Annual Report Fellow Shareholders, Governance and Shareholder Outreach

Manulife Financial Corporation Who Manulife Financial Corporation is Our five Portfolio Optimization we are a leading international financial strategic We are actively managing our priorities services group providing financial 1 legacy businesses to improve advice, insurance, as well as returns and cash generation while wealth and asset management reducing risk. solutions for individuals, groups, and institutions. We operate as John Hancock in the United States Expense Efficiency and Manulife elsewhere. We are getting our cost structure 2 into fighting shape and simplifying and digitizing our processes to position us for efficient growth. Accelerate Growth We are accelerating growth in our 3 highest-potential businesses. Our Digital, Customer Leader mission Decisions We are improving our customer 4 experiences, using digitization and made easierr. innovation to put customers first. Lives High-Performing Team made betterr. We are building a culture that 5 drives our priorities. Our Our Values represent how we Obsess Do the Values operate. They reflect our culture, about right thing inform our behaviours, and help define how we work together. customers Manulife Note: Growth in core earnings, assets under Core Earnings (C$ billions) management and administration (AUMA), and by the new business value are presented on a constant $5.6 billion exchange rate basis. numbers Total Company, Global Wealth and Asset Management (Global WAM), and Asia core earnings up 23%, 21%, and 20%, respectively, from 2017. 5.6 4.6 4.0 3.4 2.9 2014 2015 2016 2017 2018 Assets Under Management and Administration Net Income Attributed to Shareholders (C$ billions) (C$ billions) $1,084 billion $4.8 billion Over $1 trillion in AUMA.