DR. PEPPER SNAPPLE GROUP, Inc. (NYSE: DPS)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

Dr Pepper Snapple Group Transforms Its Category Management Process

Case study Allocation and Space Dr Pepper Snapple Group Transforms Its Category Management Process On the category management improvement “Our space methodology paired with Blue Yonder’s space planning capability optimizes days of supply and increases inventory turns on an item-by-item basis, which results in a reduction in excess inventory and a boost in cash 99% flow for the retailer. We can also reset our retail customers’ planograms improved accuracy twice a year or more, which many of our competitors just can’t handle.” - Director, Category Management, Dr Pepper Snapple Group Challenges • Dr Pepper Snapple Group (DPS) is one of North America’s leading refreshment beverage companies. The company sells its diverse and 15x popular soft drinks to top franchise businesses like Coca-Cola, Pepsi and reduction in labor hours other independent bottling companies throughout North America. With to maintain and update category management a core competency, the beverage company’s space, planograms assortment and speed-to-insight capabilities are continuously evolving. • DPS was challenged to mass produce store-specific planograms on a large scale to meet the changing needs of their retail customers without draining their time and resources. • The company’s goals were to improve the accuracy rate, increase efficiency, boost retail partnerships without increasing headcount and reducing excess inventory to achieve increased cash flow. On speeding up planogram production The Category Manager stated, “In order to increase our retail partnerships and categories without increasing headcount, we implemented proven solutions that would support our new approach to space management and help us speed up the planogram creation process.” The Blue Yonder solution automated the large-scale production of Blue Yonder’s expertise optimized, store-specific planograms, increasing Dr Pepper Snapple Group’s accuracy rate to 99 percent. -

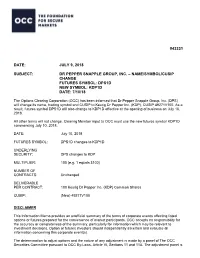

Dr Pepper Snapple Group, Inc. – Name/Symbol/Cusip Change Futures Symbol: Dps1d New Symbol: Kdp1d Date: 7/10/18

#43331 DATE: JULY 9, 2018 SUBJECT: DR PEPPER SNAPPLE GROUP, INC. – NAME/SYMBOL/CUSIP CHANGE FUTURES SYMBOL: DPS1D NEW SYMBOL: KDP1D DATE: 7/10/18 The Options Clearing Corporation (OCC) has been informed that Dr Pepper Snapple Group, Inc. (DPS) will change its name, trading symbol and CUSIP to Keurig Dr Pepper Inc. (KDP), CUSIP 49271V100. As a result, futures symbol DPS1D will also change to KDP1D effective at the opening of business on July 10, 2018. All other terms will not change. Clearing Member input to OCC must use the new futures symbol KDP1D commencing July 10, 2018. DATE: July 10, 2018 FUTURES SYMBOL: DPS1D changes to KDP1D UNDERLYING SECURITY: DPS changes to KDP MULTIPLIER: 100 (e.g. 1 equals $100) NUMBER OF CONTRACTS: Unchanged DELIVERABLE PER CONTRACT: 100 Keurig Dr Pepper Inc. (KDP) Common Shares CUSIP: (New) 49271V100 DISCLAIMER This Information Memo provides an unofficial summary of the terms of corporate events affecting listed options or futures prepared for the convenience of market participants. OCC accepts no responsibility for the accuracy or completeness of the summary, particularly for information which may be relevant to investment decisions. Option or futures investors should independently ascertain and evaluate all information concerning this corporate event(s). The determination to adjust options and the nature of any adjustment is made by a panel of The OCC Securities Committee pursuant to OCC By-Laws, Article VI, Sections 11 and 11A. The adjustment panel is comprised of representatives from OCC and each exchange which trades the affected option. The determination to adjust futures and the nature of any adjustment is made by OCC pursuant to OCC By- Laws, Article XII, Sections 3, 4, or 4A, as applicable. -

Introducing Keurig Dr Pepper

Introducing Keurig Dr Pepper Investor Presentation Creating a New Challenger In the Beverage Industry Highly Confidential January 2018 Forward Looking Statements Certain statements contained herein are “forward-looking statements” within the meaning of applicable securities laws and regulations. These forward-looking statements can generally be identified by the use of words such as “anticipate,” “expect,” “believe,” “could,” “estimate,” “feel,” “forecast,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will,” “would,” and similar words, phrases or expressions and variations or negatives of these words, although not all forward-looking statements contain these identifying words. Forward-looking statements by their nature address matters that are, to different degrees, uncertain, such as statements regarding the estimated or anticipated future results of the combined company following the proposed merger, the anticipated benefits of the proposed merger, including estimated synergies, the expected timing of completion of the proposed merger and related transactions and other statements that are not historical facts. These statements are based on the current expectations of Keurig Green Mountain Parent Holdings Corp. and Dr Pepper Snapple Group, Inc. management and are not predictions of actual performance. These forward-looking statements are subject to a number of risks and uncertainties regarding the combined company’s business and the proposed merger and actual results may differ materially. These risks and uncertainties -

DR PEPPER SNAPPLE GROUP ANNUAL REPORT DPS at a Glance

DR PEPPER SNAPPLE GROUP ANNUAL REPORT DPS at a Glance NORTH AMERICA’S LEADING FLAVORED BEVERAGE COMPANY More than 50 brands of juices, teas and carbonated soft drinks with a heritage of more than 200 years NINE OF OUR 12 LEADING BRANDS ARE NO. 1 IN THEIR FLAVOR CATEGORIES Named Company of the Year in 2010 by Beverage World magazine CEO LARRY D. YOUNG NAMED 2010 BEVERAGE EXECUTIVE OF THE YEAR BY BEVERAGE INDUSTRY MAGAZINE OUR VISION: Be the Best Beverage Business in the Americas STOCK PRICE PERFORMANCE PRIMARY SOURCES & USES OF CASH VS. S&P 500 TWO-YEAR CUMULATIVE TOTAL ’09–’10 JAN ’10 MAR JUN SEP DEC ’10 $3.4B $3.3B 40% DPS Pepsi/Coke 30% Share Repurchases S&P Licensing Agreements 20% Dividends Net Repayment 10% of Credit Facility Operations & Notes 0% Capital Spending -10% SOURCES USES 2010 FINANCIAL SNAPSHOT (MILLIONS, EXCEPT EARNINGS PER SHARE) CONTENTS 2010 $5,636 NET SALES +2% 2009 $5,531 $ 1, 3 21 SEGMENT +1% Letter to Stockholders 1 OPERATING PROFIT $ 1, 310 Build Our Brands 4 $2.40 DILUTED EARNINGS +22% PER SHARE* $1.97 Grow Per Caps 7 Rapid Continuous Improvement 10 *2010 diluted earnings per share (EPS) excludes a loss on early extinguishment of debt and certain tax-related items, which totaled Innovation Spotlight 23 cents per share. 2009 diluted EPS excludes a net gain on certain 12 distribution agreement changes and tax-related items, which totaled 20 cents per share. See page 13 for a detailed reconciliation of the Stockholder Information 12 7 excluded items and the rationale for the exclusion. -

Dr Pepper Snapple Group Inc DPS (XNYS)

Morningstar Equity Analyst Report | Report as of 24 Oct 2014 | Page 1 of 8 Dr Pepper Snapple Group Inc DPS (XNYS) Morningstar Rating Last Price Fair Value Estimate Price/Fair Value Dividend Yield % Market Cap (Bil) Industry Stewardship QQ 66.69 USD 52.00 USD 1.39 2.40 13.06 Beverages - Soft Drinks Standard 24 Oct 2014 24 Oct 2014 24 Oct 2014 24 Oct 2014 Morningstar Pillars Analyst Quantitative Economic Moat Narrow Wide Dr Pepper's continued productivity initiatives should help offset end- Valuation QQ Overvalued Uncertainty Medium Medium market headwinds. Financial Health BBB+ Strong Adam Fleck, CFA, 24 October 2014 repurchases. Source: Morningstar Equity Research Investment Thesis Quantitative Valuation Dr Pepper Snapple’s (DPS) brands enjoy solid positions Adam Fleck, CFA, 23 October 2014 DPS USA s within their particular markets, but limited geographic Analyst Note reach, partial reliance on competitors for bottling and After reviewing narrow-moat Dr Pepper Snapple's Undervalued Fairly Valued Overvalued distribution, and an overall trailing position constrain our third-quarter results, we will probably raise our $48 per Current 5-Yr Avg Sector Country moat rating to narrow. share fair value estimate 5% to 10% to account for Price/Quant Fair Value 1.18 1.05 0.94 0.86 continued solid execution. Cost control remained strong Price/Earnings 18.5 14.9 19.3 20.0 Following its split from parent company Cadbury in the quarter. Core operating margins rose 70 basis points Forward P/E 17.7 — 16.9 15.0 Price/Cash Flow 13.3 11.0 12.0 12.0 Schweppes in 2008, DPS retained the U.S., Canadian, year over year to 20.1%, and combined with a slightly Price/Free Cash Flow 16.1 16.8 20.5 20.4 Mexican, and Caribbean rights to its core brands; outside lower expected tax rate and a beneficial raw material cost Dividend Yield % 2.40 2.47 1.97 2.08 these regions, competitors such as Coca-Cola and PepsiCo environment, management raised its full-year earnings Source: Morningstar own the rights. -

Broward County Public Schools Approved Smart Snacks Beverages

Updated October 25, 2019 Broward County Public Schools Approved Smart Snacks Beverages All Brands (water) MS/HS Unflavored water Any size Aquafina Flavor Splash (berry berry, Aquafina HS color me kiwi, really raspberry) 20 oz. Aquafina Flavor Splash sparkling Aquafina HS ( kiwi strawberry, orange citrus) 16.9 oz. Bubly HS Assorted Sparking Waters 12 oz. Campbell Soup Co. MS/HS V-8 Fusion 100 % Juice 8 oz. Canada Dry HS Canada Dry 10-Gingerale 12 oz. Canada Dry HS Diet Ginger Ale 12 oz. Sparkling Seltzer Water Canada Dry HS (Unflavored) 12 oz. Sparkling Seltzer Water (Raspberry, Canada Dry HS Strawberry) 12 oz. Clement Pappas & Co., Inc. MS/HS Fruit Punch-100% Juice 8 oz. Coca-Cola HS POWERADE ZERO Fruit Punch 12 oz. Coca-Cola HS Diet Barq's Beer 12 oz., 20 oz. Coca-Cola HS Cherry Zero, Vanilla Zero 12 oz., 20 oz. Coca-Cola HS Fresca-Original Citrus 12 oz., 20 oz. Coca-Cola HS Fanta Orange Zero 12 oz., 20 oz. Updated October 25, 2019 Broward County Public Schools Approved Smart Snacks Beverages Coca-Cola HS Coke Zero 12 oz., 20 oz. Coca-Cola HS Diet Coke 12 oz., 20 oz. Coca-Cola HS Glaceau vitaminwater 20 oz. Coca-Cola HS Glaceau smartwater 20 oz. Coca-Cola HS Mello-Yellow Zero 12 oz., 20 oz. Coca-Cola HS Pibb Zero 12 oz., 20 oz. Coca-Cola HS Sprite Zero 12 oz., 20 oz. Coca-Cola HS FRESCA 12 oz. Dasani HS Strawberry Dasani 20 oz. Dasani HS Lemon Dasani 20 oz. Dr. Pepper-Snapple HS A& W Root Beer 10 12 oz. -

Dr Pepper Snapple Group, Inc Annual Report 2018

Dr Pepper Snapple Group, Inc Annual Report 2018 Form 10-K (NYSE:DPS) Published: February 14th, 2018 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 Form 10-K x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2017 or o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to C ommission file number 001-33829 (Exact name of Registrant as specified in its charter) Delaware 98-0517725 (State or other jurisdiction of (I.R.S. employer incorporation or organization) identification number) 5301 Legacy Drive, Plano, Texas 75024 (Address of principal executive offices) (Zip code) Registrant's telephone number, including area code: (972) 673-7000 Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchange on Which Registered COMMON STOCK, $0.01 PAR VALUE NEW YORK STOCK EXCHANGE Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yesx No o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Beverages 2014 to Access the Full Report, Contact [email protected]

EXCERPT FROM THE DIGITAL IQ INDEX®: BEVERAGES 2014 TO ACCESS THE FULL REPORT, CONTACT [email protected] DIGITAL IQ INDEX® BEVERAGES September 29, 2014 EXCERPT FROM THE DIGITAL IQ INDEX®: BEVERAGES 2014 TO ACCESS THE FULL REPORT, CONTACT [email protected] DIGITAL IQ INDEX® BEVERAGES Fizzle Beverages: Annual Per Capita Consumption by Category The “sugar water” business is going from bad to worse. U.S., 1987–2013 In 1998, the average American drank more than 50 gallons of soda per year.1 Fifteen years later, consumption 50 is down nearly 20 percent—with “diet” drinks declining 42.2 faster than any other beverage category due to increased 40 Soft Drinks scrutiny of aspartame and other artificial sweeteners.2 Although cola conglomerates have attempted triage by 30 launching anti-obesity campaigns, testing stevia-based GALLONS PER CAPITA Bottled Water 22.1 reformulations (e.g., Coca-Cola Life, Pepsi NEXT), and 20 20.1 doubling down on marketing expenditures—nothing can Beer 3,4 stem the tide. Last April, Coca-Cola announced its 10 Juices first global dip in soda volume since 1999, signaling the 6.9 4.3 5 spread of the disease beyond the United States. 0 Sports Drinks 1990 2000 2010 Source: Beverages Digest, July 2014. Too Little, Too Late? As reality sets in, beverage titans are slowly rethinking business Beverages: Change in Per Capital Consumption by Category fundamentals. In 2007, Coca-Cola embarked on a diversification U.S., 2003–2013 binge (e.g., Glacéau, Honest Tea, Zico)—culminating in a $2 billion investment in Monster Energy last August.6,7 In 2013, the company Sports Drinks reversed course by selling costly distribution operations it acquired +40% Bottled as recently as 2010.8 In September, Coca-Cola experimented with its Water first exclusive distribution deal with Amazon (see page 48). -

Keurig Dr Pepper Annual Report 2021

Keurig Dr Pepper Annual Report 2021 Form 10-K (NASDAQ:KDP) Published: February 25th, 2021 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED December 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO COMMISSION FILE NUMBER 001-33829 kdp-20201231_g1.jpg Keurig Dr Pepper Inc. (Exact name of registrant as specified in its charter) Delaware 98-0517725 (State or other jurisdiction of incorporation or organization) (I.R.S. employer identification number) 53 South Avenue Burlington, Massachusetts 01803 (Address of principal executive offices) (781) 418-7000 (Registrant's telephone number, including area code) Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). -

Dr Pepper Snapple Group, Inc

A NEW COMPANY with a heritage spanning centuries… Our brands have been synonymous with refreshment, revitalization, fun and fl avor for generations. In 2008, those 50-plus brands became Dr Pepper Snapple Group, the oldest new company traded on the New York Stock Exchange. We may be a new player in the equity markets, but the equity of our brands is unmistakably strong and growing. Th is report illustrates the power and potential of great brands and great people to produce great results. EXPERIENCED LEADERSHIP Dr Pepper Snapple Group is an integrated refreshment beverage business serving consumers across the U.S., Canada, Mexico and the Caribbean. Our business is led by an experienced management team that is focused on building capabilities to support growth and create shareholder value. With 200 years of collective food and beverage industry experience, this team has worked with top consumer brands, managed complex supply chains and developed strong relationships with key players in the industry. From left to right: Larry D. Young, President & Chief Executive Offi cer; Tina S. Barry, Senior Vice President, Corporate Affairs; John O. Stewart, Executive Vice President & Chief Financial Offi cer; James L. Baldwin, Jr., Executive Vice President, General Counsel; Rodger L. Collins, President, Packaged Beverages; Pedro Herrán Gacha, Executive Vice President, Strategy & President, Mexico & Caribbean; Derry L. Hobson, Executive Vice President, Supply Chain; James J. Johnston, Jr., President, Beverage Concentrates; Lawrence N. Solomon, Executive Vice President, Human Resources; David J. Thomas, Ph.D., Senior Vice President, Research & Development; Jim R. Trebilcock, Executive Vice President, Marketing Dr Pepper is served for Jean Jacob Schweppe Mott’s brand starts as the fi rst time at the Charles Grigg invents 7UP Peñafi el, Mexico’s oldest perfects a process for a line of apple cider and Old Corner Drug Store mineral water, is founded making carbonated water vinegar offerings in Waco, Texas in Puebla 1783 1842 1885 1929 1948 DPS at-a- GLANCE • No. -

Redefining the Rules of Engagement of the Cola Wars

FW University of Florida Warrington College of Business Administration HONORS THESIS Redefining the Rules of Engagement in the Cola Wars A comparative study of multi-point corporate social responsibility practices as part of an integrated strategy and source of competitive advantage in the soft drink manufacturing industry. Presented by: Frederique Whitaker UF ID: 4104 - 9853 Faculty Advisor: Jennifer Knippen ~ 1 ~ FW Abstract: The Cola Wars commenced over a century ago as Coca-Cola and Pepsi vigorously began fighting for market share in the soft drink manufacturing industry. Today the war continues but the battlefield has expanded beyond the storefront to all the firms’ stakeholders. This thesis seeks to explain the linkages between these two firms' corporate social responsibility (CSR) practices and their respective resources and capabilities, and suggests these linkages could help explain differentials in performance between the two rivals. This result will be achieved through both industry- and firm-level analyses, to identify sources of superior profitability and competitive advantage in The Coca-Cola Company and PepsiCo, before analyzing each firm's multi-faceted approach to CSR, the linkages between their practices and resources and capabilities and the implications for each firm’s respective performance. This analysis concludes with some future strategy recommendations for these two industry leaders. ~ 2 ~ FW Table of Contents Introduction ...................................................................................................................................................4