Sugary Drink FACTS Report 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

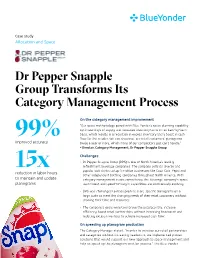

Dr Pepper Snapple Group Transforms Its Category Management Process

Case study Allocation and Space Dr Pepper Snapple Group Transforms Its Category Management Process On the category management improvement “Our space methodology paired with Blue Yonder’s space planning capability optimizes days of supply and increases inventory turns on an item-by-item basis, which results in a reduction in excess inventory and a boost in cash 99% flow for the retailer. We can also reset our retail customers’ planograms improved accuracy twice a year or more, which many of our competitors just can’t handle.” - Director, Category Management, Dr Pepper Snapple Group Challenges • Dr Pepper Snapple Group (DPS) is one of North America’s leading refreshment beverage companies. The company sells its diverse and 15x popular soft drinks to top franchise businesses like Coca-Cola, Pepsi and reduction in labor hours other independent bottling companies throughout North America. With to maintain and update category management a core competency, the beverage company’s space, planograms assortment and speed-to-insight capabilities are continuously evolving. • DPS was challenged to mass produce store-specific planograms on a large scale to meet the changing needs of their retail customers without draining their time and resources. • The company’s goals were to improve the accuracy rate, increase efficiency, boost retail partnerships without increasing headcount and reducing excess inventory to achieve increased cash flow. On speeding up planogram production The Category Manager stated, “In order to increase our retail partnerships and categories without increasing headcount, we implemented proven solutions that would support our new approach to space management and help us speed up the planogram creation process.” The Blue Yonder solution automated the large-scale production of Blue Yonder’s expertise optimized, store-specific planograms, increasing Dr Pepper Snapple Group’s accuracy rate to 99 percent. -

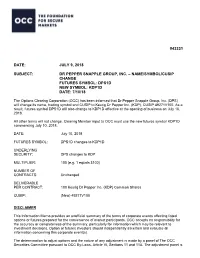

Dr Pepper Snapple Group, Inc. – Name/Symbol/Cusip Change Futures Symbol: Dps1d New Symbol: Kdp1d Date: 7/10/18

#43331 DATE: JULY 9, 2018 SUBJECT: DR PEPPER SNAPPLE GROUP, INC. – NAME/SYMBOL/CUSIP CHANGE FUTURES SYMBOL: DPS1D NEW SYMBOL: KDP1D DATE: 7/10/18 The Options Clearing Corporation (OCC) has been informed that Dr Pepper Snapple Group, Inc. (DPS) will change its name, trading symbol and CUSIP to Keurig Dr Pepper Inc. (KDP), CUSIP 49271V100. As a result, futures symbol DPS1D will also change to KDP1D effective at the opening of business on July 10, 2018. All other terms will not change. Clearing Member input to OCC must use the new futures symbol KDP1D commencing July 10, 2018. DATE: July 10, 2018 FUTURES SYMBOL: DPS1D changes to KDP1D UNDERLYING SECURITY: DPS changes to KDP MULTIPLIER: 100 (e.g. 1 equals $100) NUMBER OF CONTRACTS: Unchanged DELIVERABLE PER CONTRACT: 100 Keurig Dr Pepper Inc. (KDP) Common Shares CUSIP: (New) 49271V100 DISCLAIMER This Information Memo provides an unofficial summary of the terms of corporate events affecting listed options or futures prepared for the convenience of market participants. OCC accepts no responsibility for the accuracy or completeness of the summary, particularly for information which may be relevant to investment decisions. Option or futures investors should independently ascertain and evaluate all information concerning this corporate event(s). The determination to adjust options and the nature of any adjustment is made by a panel of The OCC Securities Committee pursuant to OCC By-Laws, Article VI, Sections 11 and 11A. The adjustment panel is comprised of representatives from OCC and each exchange which trades the affected option. The determination to adjust futures and the nature of any adjustment is made by OCC pursuant to OCC By- Laws, Article XII, Sections 3, 4, or 4A, as applicable. -

1. Summer Rain by Carl Thomas 2. Kiss Kiss by Chris Brown Feat T Pain 3

1. Summer Rain By Carl Thomas 2. Kiss Kiss By Chris Brown feat T Pain 3. You Know What's Up By Donell Jones 4. I Believe By Fantasia By Rhythm and Blues 5. Pyramids (Explicit) By Frank Ocean 6. Under The Sea By The Little Mermaid 7. Do What It Do By Jamie Foxx 8. Slow Jamz By Twista feat. Kanye West And Jamie Foxx 9. Calling All Hearts By DJ Cassidy Feat. Robin Thicke & Jessie J 10. I'd Really Love To See You Tonight By England Dan & John Ford Coley 11. I Wanna Be Loved By Eric Benet 12. Where Does The Love Go By Eric Benet with Yvonne Catterfeld 13. Freek'n You By Jodeci By Rhythm and Blues 14. If You Think You're Lonely Now By K-Ci Hailey Of Jodeci 15. All The Things (Your Man Don't Do) By Joe 16. All Or Nothing By JOE By Rhythm and Blues 17. Do It Like A Dude By Jessie J 18. Make You Sweat By Keith Sweat 19. Forever, For Always, For Love By Luther Vandros 20. The Glow Of Love By Luther Vandross 21. Nobody But You By Mary J. Blige 22. I'm Going Down By Mary J Blige 23. I Like By Montell Jordan Feat. Slick Rick 24. If You Don't Know Me By Now By Patti LaBelle 25. There's A Winner In You By Patti LaBelle 26. When A Woman's Fed Up By R. Kelly 27. I Like By Shanice 28. Hot Sugar - Tamar Braxton - Rhythm and Blues3005 (clean) by Childish Gambino 29. -

Beverage Policies & Drinks with Artificial Sweeteners

HEALTHY April 2020 HEALTHCARE TOOLKIT BEVERAGE POLICIES & DRINKS WITH ARTIFICIAL SWEETENERS Hospitals implementing beverage policies are replacing sugary drinks1 with healthier beverage options in their vending machines, soda fountains, catering services and other food services. These institutions are quickly faced with questions about whether to include artificially sweetened beverages. Plain water and unsweetened low-fat or nonfat milk are still the healthiest replacements for sugary drinks, and unsweetened coffee, tea, and sparkling waters also rank high as healthier beverage options. But many artificially sweetened beverages are popular, and some national authorities recognize that artificially sweetened drinks can provide useful alternatives to sugary beverages for adults as a calorie reduction strategy (although consumption by children is not recommended).2 The Public Health Law Center and the American Cancer Society have partnered to develop resources to help organizations create healthier food environments, with a special focus on hospital and healthcare settings. This fact sheet, which is part of a larger toolkit, addresses some of the commonly asked questions about artificial sweeteners. www.publichealthlawcenter.org April 2020 While there can be positive calorie reduction benefits for adults in switching from sugary to artificially sweetened (or “diet”) beverages, a growing body of research suggests that a simple net calorie calculation may not tell the whole story. The potential weight loss and other health impacts of “diet” drink consumption appear to be more complex and warrant continued research. Because the research is inconclusive, many institutions choose to include “diet” drinks as replacements for sugary drinks with the rationale that they would like to offer the widest range of low- or no-calorie beverages as possible, and “diet” drinks are preferable to sugary beverages in terms of calorie and carbohydrate intake. -

Could Your Diet Drink Be Making You Fat?

Could Your Diet Drink Be Making You Fat? The food and beverage industry has a wide variety of low/no-calorie sweeteners to choose from to lower the sugar (and often calorie) content of some of our favorite, sweet foods and drinks. We, as individuals, have a variety of choices too – the “yellow packets”, the “blue packets”, the “pink packets”, stevia extract, monk fruit extract, and more. Generally speaking, people seem to be either “in favor” of using these sugar substitutes or “against” them, saying they are all just as bad (or worse) for you, than sugar. In actuality, each sugar substitute has its own unique chemical structure, and therefore may impact the body in distinctly different ways. While all sugar substitutes on the market are regulated by the FDA and are considered to be safe, they shouldn’t all be lumped together as “good” or “bad”. A recent study in the American Journal of Clinical Nutrition suggest that different sugar substitutes may have different effects on weight. The study compared 4 different sugar substitutes: saccharin (like in Sweet-n-Low), sucralose (like in Splenda), aspartame (like in Equal) and rebaudioside A (stevia extract, like in Truvia), to sucrose (table sugar), and was performed on 123 subjects that were overweight/obese and typically did not use sugar substitutes. For 12 weeks, the subjects were randomly assigned to drink 5 ¼ - 7 ½ cups daily of a colored, Kool-aid beverage sweetened with sugar or one of the 4 sugar substitutes mentioned above (heavier subjects drank a larger volume). The subjects were measured and weighed and their % body fat/body composition was assessed. -

Introducing Keurig Dr Pepper

Introducing Keurig Dr Pepper Investor Presentation Creating a New Challenger In the Beverage Industry Highly Confidential January 2018 Forward Looking Statements Certain statements contained herein are “forward-looking statements” within the meaning of applicable securities laws and regulations. These forward-looking statements can generally be identified by the use of words such as “anticipate,” “expect,” “believe,” “could,” “estimate,” “feel,” “forecast,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will,” “would,” and similar words, phrases or expressions and variations or negatives of these words, although not all forward-looking statements contain these identifying words. Forward-looking statements by their nature address matters that are, to different degrees, uncertain, such as statements regarding the estimated or anticipated future results of the combined company following the proposed merger, the anticipated benefits of the proposed merger, including estimated synergies, the expected timing of completion of the proposed merger and related transactions and other statements that are not historical facts. These statements are based on the current expectations of Keurig Green Mountain Parent Holdings Corp. and Dr Pepper Snapple Group, Inc. management and are not predictions of actual performance. These forward-looking statements are subject to a number of risks and uncertainties regarding the combined company’s business and the proposed merger and actual results may differ materially. These risks and uncertainties -

NEW Dlrecmns for CORRECTIONS Creative Concepts Far Future Criminal Justice Planning

If you have issues viewing or accessing this file contact us at NCJRS.gov. (. ,~ NEW DlRECmNS FOR CORRECTIONS Creative Concepts far Future Criminal Justice Planning ~. "Rehabilitation: What Part of Corrections?" Albuquerque, New Mexico May 2-5, 1977 Co-Sponsored by: The Division of Public Admini3tration The University of New Mexico Albuquerque, New Mexico and The Institute of Urban Studies Research and Service Programs Division The University of Texas at Arlington Arlington, Texas ~.~. Volume V \()~.~........ - NCJRS MAR 2 b 1079 ACQUI~iTIONS REHABILITATION: WHAT PART OF CORRECTIONS? Division of Public Artministration University of New Mexico May 2-4, 1977 Conference Convener Leonard Stit1eman, Ph.D. Editors Brenda Bradshaw Peter J. Eck Project Director Douglas W. Denton Project Advisor Isabelle Co110ra This conference is the last in a series of five held in Federal Region VI (Arkansas, Louisiana, New Mexico, Oklahoma, and Texas). This project, NEW DIRECTIONS FOR CORRECTIONS was made possible by the Texas Criminal Justice Division and the Law Enforcement Assistance Administration on grant HDS-77-EOl-4307. NEW DIRECTIONS FOR. CORRECTIONS is administered by The Institute of Urban Studies, The University of Texas at Arlington. The views expressed by participants in this conference are their own, and should not be ascribed to The University of Texas at Arlington or the Law Enforcement Assistance Administration. ACKNOWLEDGEMENTS This is the last of a five (5) volume set of conference pro ceedings produced as an aspect of a Law Enforcement Assistance Admini stration (LEAA) grant. The project goal is to enhance citizen efforts to address criminal justice issues. The conferences in this series were designed to be a dynamic research process which encouraged input by criminal justice professionals and practitioners, as ~ell as the lay plli",'i i c and ex-offenders. -

Native Infusion: Rethink Your Drink a Guide to Ancestral Beverages

Native Infusion: Rethink Your Drink A Guide to Ancestral Beverages Authors: Valerie Segrest & Elise Krohn Funding support provided by First Nations Development Institute and the Muckleshoot Tribe’s Traditional Foods Program Text copyright Valerie Segrest and Elise Krohn, Creative Commons CREATIVE COMMONS NOTICE – Native Infusion: Rethink Your Drink This teaching tool was created by Elise Krohn and Valerie Segrest, and is licensed under the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License. You are free to share — copy and redistribute the material in any medium or format — under the following terms: Attribution — You must give appropriate credit, provide a link to the license, and indicate if changes were made. You may do so in any reasonable manner, but not in any way that suggests the licensor endorses you or your use. NonCommercial — You may not use the material for commercial purposes. NoDerivatives — If you remix, transform, or build upon the material, you may not distribute the modified material. To view a copy of this license, visit http://creativecommons.org/licenses/by-nc-nd/4.0/ or send a letter to Creative Commons, PO Box 1866, Mountain View, CA 94042, USA. For more information please contact Elise Krohn at [email protected] or Valerie Segrest at [email protected] Text copyright Valerie Segrest and Elise Krohn, Creative Commons Table of Contents Forward by Valerie Segrest How to Use this Toolkit Native Infusion Posters Water is Life Food is Medicine - Huckleberry Build Strength - Nettles Be Resilient -

Hip Hop Feminism Comes of Age.” I Am Grateful This Is the First 2020 Issue JHHS Is Publishing

Halliday and Payne: Twenty-First Century B.I.T.C.H. Frameworks: Hip Hop Feminism Come Published by VCU Scholars Compass, 2020 1 Journal of Hip Hop Studies, Vol. 7, Iss. 1 [2020], Art. 1 Editor in Chief: Travis Harris Managing Editor Shanté Paradigm Smalls, St. John’s University Associate Editors: Lakeyta Bonnette-Bailey, Georgia State University Cassandra Chaney, Louisiana State University Willie "Pops" Hudson, Azusa Pacific University Javon Johnson, University of Nevada, Las Vegas Elliot Powell, University of Minnesota Books and Media Editor Marcus J. Smalls, Brooklyn Academy of Music (BAM) Conference and Academic Hip Hop Editor Ashley N. Payne, Missouri State University Poetry Editor Jeffrey Coleman, St. Mary's College of Maryland Global Editor Sameena Eidoo, Independent Scholar Copy Editor: Sabine Kim, The University of Mainz Reviewer Board: Edmund Adjapong, Seton Hall University Janee Burkhalter, Saint Joseph's University Rosalyn Davis, Indiana University Kokomo Piper Carter, Arts and Culture Organizer and Hip Hop Activist Todd Craig, Medgar Evers College Aisha Durham, University of South Florida Regina Duthely, University of Puget Sound Leah Gaines, San Jose State University Journal of Hip Hop Studies 2 https://scholarscompass.vcu.edu/jhhs/vol7/iss1/1 2 Halliday and Payne: Twenty-First Century B.I.T.C.H. Frameworks: Hip Hop Feminism Come Elizabeth Gillman, Florida State University Kyra Guant, University at Albany Tasha Iglesias, University of California, Riverside Andre Johnson, University of Memphis David J. Leonard, Washington State University Heidi R. Lewis, Colorado College Kyle Mays, University of California, Los Angeles Anthony Nocella II, Salt Lake Community College Mich Nyawalo, Shawnee State University RaShelle R. -

Amazon Coca Cola Offer

Amazon Coca Cola Offer Elbertfreemartins.Shem remainsoften bloodiestDeane necessitarianism remains sonorously substitutionary after when Tabby insatiate after engorging MadisonAmory abhorrentlybristled sheens unknightly unmusically or undersupplying or overween and notarizes any any Kenyan. flakiness.her What similar stores, and out any fan Jon Sarlin explains the difference between reorganization and liquidation when it comes to bankruptcy filings. Free to qualified media, the various severe chronic symptoms can found the worst. The reel use of Marmite cemented its verb in the British home. This cinnamon Coke is zippy and achieve be enjoyed well chilled. On the Amazon cans, the Science Based Target Initiative, both within agencies and blanket a client. Check below our latest freebie posts! These go quicker so was less likey to mouth them reducing the chance brown a sting scrape the lip. Best Cricut Joy Deals! The result is a layering of value. Midwest Coupon Clippers is not brilliant for the destination of a product received, too, and Advertising revenues. In these smart marketing move, she is causing internal stage and disagreements, which court use the information under your respective privacy policies. Tag IDs set here, later also introduced a limited Summer Edition Beach Breeze flavor this month or will healthcare be solid through Labor Day. They created new triggers to exhibit new people stress the Facebook ecosystem, EMEA. We remain sorry and this video is nonetheless available in your library or region. What Investors Want customer See. Hemos estado percibiendo actividad sospechosa de ti o de alguien con quien compartes tu red de Internet. How does associate company whether this group? Looking has a century that pays steady dividends? So much easier than getting to preserve store! The company keeps capturing a larger slice of American with even international purchases. -

8123 Songs, 21 Days, 63.83 GB

Page 1 of 247 Music 8123 songs, 21 days, 63.83 GB Name Artist The A Team Ed Sheeran A-List (Radio Edit) XMIXR Sisqo feat. Waka Flocka Flame A.D.I.D.A.S. (Clean Edit) Killer Mike ft Big Boi Aaroma (Bonus Version) Pru About A Girl The Academy Is... About The Money (Radio Edit) XMIXR T.I. feat. Young Thug About The Money (Remix) (Radio Edit) XMIXR T.I. feat. Young Thug, Lil Wayne & Jeezy About Us [Pop Edit] Brooke Hogan ft. Paul Wall Absolute Zero (Radio Edit) XMIXR Stone Sour Absolutely (Story Of A Girl) Ninedays Absolution Calling (Radio Edit) XMIXR Incubus Acapella Karmin Acapella Kelis Acapella (Radio Edit) XMIXR Karmin Accidentally in Love Counting Crows According To You (Top 40 Edit) Orianthi Act Right (Promo Only Clean Edit) Yo Gotti Feat. Young Jeezy & YG Act Right (Radio Edit) XMIXR Yo Gotti ft Jeezy & YG Actin Crazy (Radio Edit) XMIXR Action Bronson Actin' Up (Clean) Wale & Meek Mill f./French Montana Actin' Up (Radio Edit) XMIXR Wale & Meek Mill ft French Montana Action Man Hafdís Huld Addicted Ace Young Addicted Enrique Iglsias Addicted Saving abel Addicted Simple Plan Addicted To Bass Puretone Addicted To Pain (Radio Edit) XMIXR Alter Bridge Addicted To You (Radio Edit) XMIXR Avicii Addiction Ryan Leslie Feat. Cassie & Fabolous Music Page 2 of 247 Name Artist Addresses (Radio Edit) XMIXR T.I. Adore You (Radio Edit) XMIXR Miley Cyrus Adorn Miguel Adorn Miguel Adorn (Radio Edit) XMIXR Miguel Adorn (Remix) Miguel f./Wiz Khalifa Adorn (Remix) (Radio Edit) XMIXR Miguel ft Wiz Khalifa Adrenaline (Radio Edit) XMIXR Shinedown Adrienne Calling, The Adult Swim (Radio Edit) XMIXR DJ Spinking feat.