Introducing Keurig Dr Pepper

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

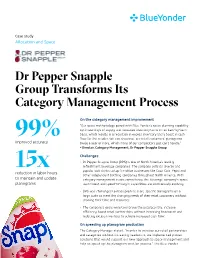

Dr Pepper Snapple Group Transforms Its Category Management Process

Case study Allocation and Space Dr Pepper Snapple Group Transforms Its Category Management Process On the category management improvement “Our space methodology paired with Blue Yonder’s space planning capability optimizes days of supply and increases inventory turns on an item-by-item basis, which results in a reduction in excess inventory and a boost in cash 99% flow for the retailer. We can also reset our retail customers’ planograms improved accuracy twice a year or more, which many of our competitors just can’t handle.” - Director, Category Management, Dr Pepper Snapple Group Challenges • Dr Pepper Snapple Group (DPS) is one of North America’s leading refreshment beverage companies. The company sells its diverse and 15x popular soft drinks to top franchise businesses like Coca-Cola, Pepsi and reduction in labor hours other independent bottling companies throughout North America. With to maintain and update category management a core competency, the beverage company’s space, planograms assortment and speed-to-insight capabilities are continuously evolving. • DPS was challenged to mass produce store-specific planograms on a large scale to meet the changing needs of their retail customers without draining their time and resources. • The company’s goals were to improve the accuracy rate, increase efficiency, boost retail partnerships without increasing headcount and reducing excess inventory to achieve increased cash flow. On speeding up planogram production The Category Manager stated, “In order to increase our retail partnerships and categories without increasing headcount, we implemented proven solutions that would support our new approach to space management and help us speed up the planogram creation process.” The Blue Yonder solution automated the large-scale production of Blue Yonder’s expertise optimized, store-specific planograms, increasing Dr Pepper Snapple Group’s accuracy rate to 99 percent. -

Fund Holdings As of 6/30/2021 Massmutual Balanced Fund Invesco Prior to 5/1/2021, the Fund Name Was Massmutual Premier Balanced Fund

Fund Holdings As of 6/30/2021 MassMutual Balanced Fund Invesco Prior to 5/1/2021, the Fund name was MassMutual Premier Balanced Fund. Fund Shares or Par Position Market Security Name Ticker CUSIP Weighting % Amount Value Apple Inc AAPL 037833100 3.91 48,433 6,633,384 Microsoft Corp MSFT 594918104 3.45 21,552 5,838,437 USTREAS T-Bill Auction Ave 3 Mon 1.69 2,862,977 JPMorgan Chase & Co JPM 46625H100 1.56 16,948 2,636,092 Verizon Communications Inc VZ 92343V104 1.45 43,768 2,452,321 The Home Depot Inc HD 437076102 1.42 7,556 2,409,533 Intel Corp INTC 458140100 1.29 38,961 2,187,271 Procter & Gamble Co PG 742718109 1.04 13,105 1,768,258 Cisco Systems Inc CSCO 17275R102 1.03 32,830 1,739,990 UnitedHealth Group Inc UNH 91324P102 1.00 4,215 1,687,855 Comcast Corp Class A CMCSA 20030N101 0.94 28,021 1,597,757 AT&T Inc T 00206R102 0.91 53,587 1,542,234 Oracle Corp ORCL 68389X105 0.83 18,031 1,403,533 Deere & Co DE 244199105 0.76 3,635 1,282,101 Accenture PLC Class A ACN G1151C101 0.74 4,237 1,249,025 Johnson Controls International PLC JCI G51502105 0.74 18,185 1,248,037 Visa Inc Class A V 92826C839 0.71 5,152 1,204,641 Texas Instruments Inc TXN 882508104 0.70 6,128 1,178,414 Costco Wholesale Corp COST 22160K105 0.67 2,850 1,127,660 Bank of America Corp BAC 060505104 0.64 26,192 1,079,896 Broadcom Inc AVGO 11135F101 0.63 2,223 1,060,015 Abbott Laboratories ABT 002824100 0.57 8,348 967,784 Target Corp TGT 87612E106 0.56 3,949 954,631 Honeywell International Inc HON 438516106 0.56 4,324 948,469 Goldman Sachs Group Inc GS 38141G104 0.53 2,374 901,004 -

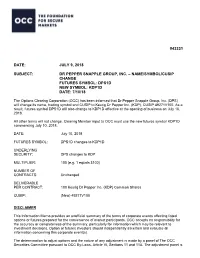

Dr Pepper Snapple Group, Inc. – Name/Symbol/Cusip Change Futures Symbol: Dps1d New Symbol: Kdp1d Date: 7/10/18

#43331 DATE: JULY 9, 2018 SUBJECT: DR PEPPER SNAPPLE GROUP, INC. – NAME/SYMBOL/CUSIP CHANGE FUTURES SYMBOL: DPS1D NEW SYMBOL: KDP1D DATE: 7/10/18 The Options Clearing Corporation (OCC) has been informed that Dr Pepper Snapple Group, Inc. (DPS) will change its name, trading symbol and CUSIP to Keurig Dr Pepper Inc. (KDP), CUSIP 49271V100. As a result, futures symbol DPS1D will also change to KDP1D effective at the opening of business on July 10, 2018. All other terms will not change. Clearing Member input to OCC must use the new futures symbol KDP1D commencing July 10, 2018. DATE: July 10, 2018 FUTURES SYMBOL: DPS1D changes to KDP1D UNDERLYING SECURITY: DPS changes to KDP MULTIPLIER: 100 (e.g. 1 equals $100) NUMBER OF CONTRACTS: Unchanged DELIVERABLE PER CONTRACT: 100 Keurig Dr Pepper Inc. (KDP) Common Shares CUSIP: (New) 49271V100 DISCLAIMER This Information Memo provides an unofficial summary of the terms of corporate events affecting listed options or futures prepared for the convenience of market participants. OCC accepts no responsibility for the accuracy or completeness of the summary, particularly for information which may be relevant to investment decisions. Option or futures investors should independently ascertain and evaluate all information concerning this corporate event(s). The determination to adjust options and the nature of any adjustment is made by a panel of The OCC Securities Committee pursuant to OCC By-Laws, Article VI, Sections 11 and 11A. The adjustment panel is comprised of representatives from OCC and each exchange which trades the affected option. The determination to adjust futures and the nature of any adjustment is made by OCC pursuant to OCC By- Laws, Article XII, Sections 3, 4, or 4A, as applicable. -

Jaimesen Heins Keurig Dr Pepper Waterbury, Vermont As Senior

Jaimesen Heins Keurig Dr Pepper Waterbury, Vermont As Senior Counsel – Operations & Commercial Litigation to Keurig Dr Pepper, Mr. Heins supports global commercial operations matters for the business, with a focus on commercial litigation, contract negotiation and advisory responsibilities. Mr. Heins provides strategic business advice and partners with company leaders to meet the needs of Keurig Dr Pepper’s business. Mr. Heins previously served as General Counsel to Burton Snowboards, overseeing all legal affairs of the company, including corporate governance, commercial transactions, intellectual property, brand licensing, real estate, employment, regulatory and litigation matters. Keurig Dr Pepper (NYSE: KDP) is a leading coffee and beverage company in North America, with annual revenue in excess of $11 billion. Formed in 2018 with the merger of Keurig Green Mountain and Dr Pepper Snapple Group, we have leadership positions in soft drinks, specialty coffee and tea, water, juice and juice drinks and mixers, and we market the #1 single serve coffee brewing system in the U.S. We have an unrivaled distribution system that enables our portfolio of more than 125 owned, licensed and partner brands to be available nearly everywhere people shop and consume beverages. With a wide range of hot and cold beverages that meet virtually any consumer need, KDP key brands include Keurig®, Dr Pepper®, Green Mountain Coffee Roasters®, Canada Dry®, Snapple®, Bai®, Mott’s® and The Original Donut Shop®. We have more than 25,000 employees and more than 120 offices, manufacturing plants, warehouses and distribution centers across North America. . -

OLSTEIN ALL CAP VALUE FUND SCHEDULE of INVESTMENTS March 31, 2021 (Unaudited) COMMON STOCKS - 84.7% Shares Value Advertising Agencies - 1.4% Omnicom Group, Inc

OLSTEIN ALL CAP VALUE FUND SCHEDULE OF INVESTMENTS March 31, 2021 (Unaudited) COMMON STOCKS - 84.7% Shares Value Advertising Agencies - 1.4% Omnicom Group, Inc. 140,000 $ 10,381,000 Aerospace & Defense - 1.9% L3Harris Technologies, Inc. 39,000 7,904,520 Raytheon Technologies Corporation 77,000 5,949,790 13,854,310 Air Delivery & Freight Services - 2.4% FedEx Corporation 35,000 9,941,400 United Parcel Service, Inc. - Class B 45,000 7,649,550 17,590,950 Airlines - 2.1% Delta Air Lines, Inc. (a) 158,000 7,628,240 JetBlue Airways Corporation (a) 353,000 7,180,020 14,808,260 Auto Manufacturers - 1.0% General Motors Company (a) 129,000 7,412,340 Beverages - 0.6% Keurig Dr Pepper, Inc. (b) 124,000 4,261,880 Building Products - 1.2% Carrier Global Corporation 198,000 8,359,560 Capital Markets - 1.4% Goldman Sachs Group, Inc. 31,500 10,300,500 Chemicals - 1.8% Corteva, Inc. 201,000 9,370,620 Eastman Chemical Company 31,000 3,413,720 12,784,340 Commercial Banks - 5.8% Citizens Financial Group, Inc. 154,000 6,799,100 Fifth Third Bancorp 228,000 8,538,600 Prosperity Bancshares, Inc. 68,000 5,092,520 U.S. Bancorp 181,000 10,011,110 Wells Fargo & Company 280,000 10,939,600 41,380,930 Commercial Services - 1.6% Moody's Corporation 18,500 5,524,285 S&P Global, Inc. 17,000 5,998,790 11,523,075 Communications Equipment - 1.9% Cisco Systems, Inc. 266,000 13,754,860 Computers - 1.9% Apple, Inc. -

Why Keurig Is Acquiring Dr. Pepper (Rabobank)

January 2018 Why Keurig Is Acquiring Dr Pepper Breaking Down the Walls Between Coffee and Soft Drinks RaboResearch Food & Agribusiness far.rabobank.com Summary The strategic basis for the Keurig – DPS combination is clear: to create a company that Jim Watson combines hot/cold beverages and retail/office/e-commerce distribution in order to match the Senior Analyst - Beverages +1 212 916 7943 way its consumers experience the beverage world. The strategic side of the combination will take significant execution skill, while the financial side (creating synergies and an exit strategy) looks to be more straightforward. Details of the acquisition On January 29, 2018 Keurig agreed to a merger with Dr Pepper Snapple to form Keurig Dr Pepper (KDP). Dr Pepper Snapple shareholders will receive USD 103.75 per share (for a total cash value of USD 19 billion) and retain a 13% stake in the new public company. The total value to DPS shareholders represents an EV/EBITDA multiple of 17.6x. JAB, together with its partners, will make an equity investment of USD 9 billion to help finance this transaction. Coffee + soft drink opportunities and challenges KDP integrates hot and cold beverages to a degree we haven’t seen before, but we see this as a step towards a more combined coffee and soft-drink world. The most concrete example presented by the company of top-line synergies is the ability to increase distribution of ready-to- drink coffee products, with access to the broader JAB coffee portfolio. We wrote about the blurring lines between coffee and soft drinks in our note Coffee Joins the Beverage Party: What Happens when a Can of Coffee Looks Just Like a Can of Soda? We are bullish on the potential for ready-to-drink coffee in North America – and believe the new KDP could build a real challenger to Starbucks/Pepsi in this space. -

Carbonated Soft Drinks in the US Through 2025

Carbonated Soft Drinks in the U.S. through 2025: Market Essentials 2021 Edition (To be published September 2021. Data through 2020. Market projections through 2025.) More than 120 Excel tables plus an executive summary detailing trends and comprehensive profiles of leading companies, their brands and their strategies. his comprehensive market research report on the number-two T beverage category examines trends and top companies' For A Full strategies. It provides up-to-date statistics on leading brands, Catalog of packaging, quarterly growth and channels of distribution. It also Reports and offers data on regional markets, pricing, demographics, Databases, advertising, five-year growth projections and more. Go To The report presents the data in Excel spreadsheets, which it supplements with a concise executive summary highlighting key bmcreports.com developments including the impact of the coronavirus pandemic as well as a detailed discussion of the leading carbonated soft drink (CSD) companies. INSIDE: REPORT OVERVIEW A brief discussion of key AVAILABLE FORMAT & features of this report. 2 PRICING TABLE OF CONTENTS Direct Download A detailed outline of this Excel sheets, PDF, PowerPoint & Word report’s contents and data tables. 7 $4,395 To learn more, to place an advance order or to inquire about SAMPLE TEXT AND additional user licenses call: Charlene Harvey +1 212.688.7640 INFOGRAPHICS ext. 1962 [email protected] A few examples of this report’s text, data content layout and style. 13 HAVE Contact Charlene Harvey: 212-688-7640 x 1962 QUESTIONS? [email protected] Beverage Marketing Corporation 850 Third Avenue, 13th Floor, New York, NY 10022 Tel: 212-688-7640 Fax: 212-826-1255 The answers you need Carbonated Soft Drinks in the U.S. -

2020 Q1 Sawgrass FF

Investment Statement June 30, 2021 Ormond Beach Firefighters Pension Trust Fund Diversified Large Growth Equity Gregory S. Gosch, Institutional Client Services (904) 493-5506 1579 The Greens Way, Suite 20 Jacksonville Beach, FL 32250 www.saw-grass.com Portfolio Review Portfolio Market Values Portfolio Summary Change in Portfolio Market Value Asset Class Total Cost Market Value Percent of Assets Beginning Market Value on 03/31/2021 $4,321,633.21 Equity $2,683,259.40 $4,518,862.64 98.3% Additions $0.00 Cash & Equivs. $77,110.59 $77,110.59 1.7% Withdrawals -$30,353.69 TOTAL $2,760,369.99 $4,595,973.23 100% Investment Gain/Loss $310,432.01 Ending Market Value on 06/30/2021 $4,595,973.23 Asset Allocation Equity Cash & Equivs. 98% 2% STABILITY | CONSISTENCY | COMMITMENT 2 Portfolio Performance TOTAL RETURNS FOR SELECT PERIODS Ormond Beach Firefighters Pension Trust Fund 06/30/2021 Quarter Year Latest Latest Latest Latest Since To Date To Date One Year Three Year Five Year Ten Year Inception* Total Account 7.19 11.32 31.15 21.03 18.39 - 15.87 Russell 1000 Growth 11.93 12.99 42.50 25.14 23.66 - 18.44 Equities 7.25 11.43 31.54 21.71 19.07 - 16.52 Russell 1000 Growth 11.93 12.99 42.50 25.14 23.66 - 18.44 S&P 500 8.55 15.25 40.79 18.67 17.65 - 15.39 Fixed Income - - - - - - - Cash and Equiv. - - - 1.03 0.90 - 0.54 Other - - - - - - - *Since Inception 04/25/12 Performance is Gross of Fees unless otherwise noted Returns for periods of one year or longer are annualized STABILITY | CONSISTENCY | COMMITMENT 3 Portfolio Performance TOTAL RETURNS GROSS FOR SELECT PERIODS Ormond Beach Firefighters Pension Trust Fund 06/30/2021 45.0% 40.0% 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% QTD YTD 1 Year 3 Year 5 Year Since Inception Portfolio Russell 1000 Growth *Since Inception 04/25/12 Returns for periods of one year or longer are annualized STABILITY | CONSISTENCY | COMMITMENT 4 Portfolio Holdings Security Quantity Unit Cost Total Cost Price Market Value Pct of Assets Common Stock Consumer Discretionary TRACTOR SUPPLY CO COM 369.00 149.35 55,109.22 186.06 68,656.14 1.5 NIKE INC. -

Keurig Dr Pepper

Food and Beverage Benchmark COMPANY SCORECARD 2020 Keurig Dr Pepper TICKER MARKET CAPITALIZATION HEADQUARTERS NASDAQ: KDP US$35 billion United States DISCLOSURES TARGETS UK Modern Slavery Act: Yes Yes California Transparency in Supply Chains Act: Yes OVERALL RANKING OVERALL SCORE 17 out of 43 31 out of 100 SUMMARY Keurig Dr Pepper (KDP), an American producer of hot and cold beverages, ranks 17th out of 43 companies, disclosing more information on its forced labor policies and practices than its peers on all themes except Worker Voice, Monitoring, and Remedy. The company’s score is based on its strong performance on the theme of Commitment & Governance. The company is encouraged to improve its performance and disclosure on the themes of Purchasing Practices, Worker Voice, and Remedy. THEME-LEVEL SCORES 0 10 20 30 40 50 60 70 80 90 100 80 Commitment & Governance 55 50 Traceability & Risk Assessment 33 18 Purchasing Practices 17 30 Recruitment 21 7 Worker Voice 15 15 Monitoring 26 19 Remedy 28 Company score Industry average KEY DATA POINTS Research conducted through February 2020 or through May 2020, where companies provided additional disclosure or links. For more information, see the full dataset here. For information on a company’s positive and negative human rights impact, see the Business & Human Rights Resource Centre website. 1 Food and Beverage Benchmark COMPANY SCORECARD 2020 SUPPLIER LIST NO-FEE POLICY No Yes (Employer Pays Principle) SUPPORTS FREEDOM OF ASSOCIATION REMEDY FOR SUPPLY CHAIN WORKERS No No HIGH-RISK COMMODITIES Coffee, cocoa, and corn1 LEADING PRACTICES None. NOTABLE FINDINGS Commitment & Governance: The company discloses that it has trained 100% of its procurement staff on the supplier code of conduct, which prohibits forced labor. -

Dr Pepper Shareholders Denied Appraisal in $21B Keurig Deal by Vince Sullivan

Portfolio Media. Inc. | 111 West 19th Street, 5th Floor | New York, NY 10011 | www.law360.com Phone: +1 646 783 7100 | Fax: +1 646 783 7161 | [email protected] Dr Pepper Shareholders Denied Appraisal In $21B Keurig Deal By Vince Sullivan Law360 (June 1, 2018, 8:46 PM EDT) -- Shareholders of Dr Pepper Snapple Group Inc. do not have appraisal rights in the proposed $21 billion merger of the company with Keurig Green Mountain Inc., after a Delaware Chancery Court judge ruled Friday that Dr Pepper itself is not a party to the deal. In an opinion issued by Chancellor Andre G. Bouchard, the court ruled that appraisal rights afforded to shareholders of a company that is a party to a merger do not apply in this transaction because Dr Pepper is merely the parent of Salt Merger Sub Inc., a subsidiary created to merge with the parent company of Keurig. Section 262 of the Delaware General Corporation Law provides shareholders with a right to seek a court determination of the fair value of their shares in a company after a merger is announced. The court has the authority to award the petitioning shareholders the difference between the deal price and the appraised value under certain conditions. Chancellor Bouchard said that Section 262 requires a petitioning shareholder to hold stock in a constituent corporation, which requires the company to be one “actually being merged or combined.” “Based on that construction, the court concludes that Dr Pepper’s stockholders do not have a statutory right to appraisal under Section 262(b) because Dr Pepper is not a constituent corporation,” the opinion said. -

DR PEPPER SNAPPLE GROUP ANNUAL REPORT DPS at a Glance

DR PEPPER SNAPPLE GROUP ANNUAL REPORT DPS at a Glance NORTH AMERICA’S LEADING FLAVORED BEVERAGE COMPANY More than 50 brands of juices, teas and carbonated soft drinks with a heritage of more than 200 years NINE OF OUR 12 LEADING BRANDS ARE NO. 1 IN THEIR FLAVOR CATEGORIES Named Company of the Year in 2010 by Beverage World magazine CEO LARRY D. YOUNG NAMED 2010 BEVERAGE EXECUTIVE OF THE YEAR BY BEVERAGE INDUSTRY MAGAZINE OUR VISION: Be the Best Beverage Business in the Americas STOCK PRICE PERFORMANCE PRIMARY SOURCES & USES OF CASH VS. S&P 500 TWO-YEAR CUMULATIVE TOTAL ’09–’10 JAN ’10 MAR JUN SEP DEC ’10 $3.4B $3.3B 40% DPS Pepsi/Coke 30% Share Repurchases S&P Licensing Agreements 20% Dividends Net Repayment 10% of Credit Facility Operations & Notes 0% Capital Spending -10% SOURCES USES 2010 FINANCIAL SNAPSHOT (MILLIONS, EXCEPT EARNINGS PER SHARE) CONTENTS 2010 $5,636 NET SALES +2% 2009 $5,531 $ 1, 3 21 SEGMENT +1% Letter to Stockholders 1 OPERATING PROFIT $ 1, 310 Build Our Brands 4 $2.40 DILUTED EARNINGS +22% PER SHARE* $1.97 Grow Per Caps 7 Rapid Continuous Improvement 10 *2010 diluted earnings per share (EPS) excludes a loss on early extinguishment of debt and certain tax-related items, which totaled Innovation Spotlight 23 cents per share. 2009 diluted EPS excludes a net gain on certain 12 distribution agreement changes and tax-related items, which totaled 20 cents per share. See page 13 for a detailed reconciliation of the Stockholder Information 12 7 excluded items and the rationale for the exclusion.