Suntory Beverage & Food (2587)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

Dr Pepper Snapple Group Transforms Its Category Management Process

Case study Allocation and Space Dr Pepper Snapple Group Transforms Its Category Management Process On the category management improvement “Our space methodology paired with Blue Yonder’s space planning capability optimizes days of supply and increases inventory turns on an item-by-item basis, which results in a reduction in excess inventory and a boost in cash 99% flow for the retailer. We can also reset our retail customers’ planograms improved accuracy twice a year or more, which many of our competitors just can’t handle.” - Director, Category Management, Dr Pepper Snapple Group Challenges • Dr Pepper Snapple Group (DPS) is one of North America’s leading refreshment beverage companies. The company sells its diverse and 15x popular soft drinks to top franchise businesses like Coca-Cola, Pepsi and reduction in labor hours other independent bottling companies throughout North America. With to maintain and update category management a core competency, the beverage company’s space, planograms assortment and speed-to-insight capabilities are continuously evolving. • DPS was challenged to mass produce store-specific planograms on a large scale to meet the changing needs of their retail customers without draining their time and resources. • The company’s goals were to improve the accuracy rate, increase efficiency, boost retail partnerships without increasing headcount and reducing excess inventory to achieve increased cash flow. On speeding up planogram production The Category Manager stated, “In order to increase our retail partnerships and categories without increasing headcount, we implemented proven solutions that would support our new approach to space management and help us speed up the planogram creation process.” The Blue Yonder solution automated the large-scale production of Blue Yonder’s expertise optimized, store-specific planograms, increasing Dr Pepper Snapple Group’s accuracy rate to 99 percent. -

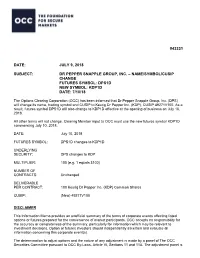

Dr Pepper Snapple Group, Inc. – Name/Symbol/Cusip Change Futures Symbol: Dps1d New Symbol: Kdp1d Date: 7/10/18

#43331 DATE: JULY 9, 2018 SUBJECT: DR PEPPER SNAPPLE GROUP, INC. – NAME/SYMBOL/CUSIP CHANGE FUTURES SYMBOL: DPS1D NEW SYMBOL: KDP1D DATE: 7/10/18 The Options Clearing Corporation (OCC) has been informed that Dr Pepper Snapple Group, Inc. (DPS) will change its name, trading symbol and CUSIP to Keurig Dr Pepper Inc. (KDP), CUSIP 49271V100. As a result, futures symbol DPS1D will also change to KDP1D effective at the opening of business on July 10, 2018. All other terms will not change. Clearing Member input to OCC must use the new futures symbol KDP1D commencing July 10, 2018. DATE: July 10, 2018 FUTURES SYMBOL: DPS1D changes to KDP1D UNDERLYING SECURITY: DPS changes to KDP MULTIPLIER: 100 (e.g. 1 equals $100) NUMBER OF CONTRACTS: Unchanged DELIVERABLE PER CONTRACT: 100 Keurig Dr Pepper Inc. (KDP) Common Shares CUSIP: (New) 49271V100 DISCLAIMER This Information Memo provides an unofficial summary of the terms of corporate events affecting listed options or futures prepared for the convenience of market participants. OCC accepts no responsibility for the accuracy or completeness of the summary, particularly for information which may be relevant to investment decisions. Option or futures investors should independently ascertain and evaluate all information concerning this corporate event(s). The determination to adjust options and the nature of any adjustment is made by a panel of The OCC Securities Committee pursuant to OCC By-Laws, Article VI, Sections 11 and 11A. The adjustment panel is comprised of representatives from OCC and each exchange which trades the affected option. The determination to adjust futures and the nature of any adjustment is made by OCC pursuant to OCC By- Laws, Article XII, Sections 3, 4, or 4A, as applicable. -

Case Study Cerebos Australia – 2016 Outstanding Achievement in Design

Case Study Cerebos Australia - 2016 Outstanding Achievement in Design Case Study Cerebos Australia – 2016 Outstanding Achievement in Design Overview In 2016, Cerebos Australia won the Australian Packaging Covenant award for Outstanding Achievement in Design. This award recognises the organisation’s success in integrating the Sustainable Packaging Guidelines (SPGs) into their design and procurement processes, and implementing the opportunities identified. Taking advantage of an extensive factory modernisation, the Cerebos design team has been able to use the outcomes of the SPG reviews to redesign and rethink packaging as production lines were upgraded. A consistently high performing signatory, Cerebos also works actively with its supply chain to identify and implement design changes. Background Cerebos Australia Cerebos is a successful and innovative sauce, spice and coffee manufacturing organisation that develop and manufacture their own products across both Australia and New Zealand. They have a wide range of well- known brands including Fountain, Gravox, Saxa and Gregg’s. Cerebos Australia and New Zealand is a trans- Tasman integration of two companies. The parent company, Cerebos Pacific Limited, is based in Singapore and is wholly owned by Suntory Limited, a Japanese global food and beverage group. Commitment to Sustainable Design Since joining the Covenant in mid-2000, Cerebos has progressively improved its packaging decision-making processes in order to reduce environmental impacts and create business efficiencies. Cerebos has an ongoing commitment to minimise the environmental impact arising from packaging by continuing to pursue their specific performance goals of Design, Recycling and Product Stewardship. Environmental issues are considered in the product development process through a packaging decision checklist based on the SPGs. -

Chicken Essence for Cognitive Function Improvement: a Systematic Review and Meta-Analysis

nutrients Review Chicken Essence for Cognitive Function Improvement: A Systematic Review and Meta-Analysis Siew Li Teoh 1, Suthinee Sudfangsai 2, Pisake Lumbiganon 3, Malinee Laopaiboon 4, Nai Ming Lai 5 and Nathorn Chaiyakunapruk 1,6,7,8,* Received: 3 November 2015; Accepted: 11 January 2016; Published: 20 January 2016 1 School of Pharmacy, Monash University Malaysia, Selangor 47500, Malaysia; [email protected] 2 Faculty of Pharmaceutical Sciences, Naresuan University, Phitsanulok 65000, Thailand; [email protected] 3 Department of Obstetrics and Gynaecology, Faculty of Medicine, Khon Kaen University, Khon Kaen 40002, Thailand; [email protected] 4 Department of Biostatistics and Demography, Faculty of Public Health, Khon Kaen University, Khon Kaen 40002, Thailand; [email protected] 5 School of Medicine, Taylor’s University Malaysia, Selangor 47500, Malaysia; [email protected] 6 Center of Pharmaceutical Outcomes Research (CPOR), Department of Pharmacy Practice, Faculty of Pharmaceutical Sciences, Naresuan University, Phitsanulok 65000, Thailand 7 School of Pharmacy, University of Wisconsin, Madison, WI 53705-2222, USA 8 School of Population Health, University of Queensland, Brisbane, Herston QLD 4006, Australia * Correspondence: [email protected]; Tel.: +603-5514-4413; Fax: +603-5514-6326 Abstract: Chicken essence (CE) is a popular traditional remedy in Asia, which is believed to improve cognitive functions. CE company claimed that the health benefits were proven with research studies. A systematic review was conducted to determine the cognitive-enhancing effects of CE. We systematically searched a number of databases for randomized controlled trials with human subjects consuming CE and cognitive tests involved. Cochrane’s Risk of Bias (ROB) tool was used to assess the quality of trials and meta-analysis was performed. -

Introducing Keurig Dr Pepper

Introducing Keurig Dr Pepper Investor Presentation Creating a New Challenger In the Beverage Industry Highly Confidential January 2018 Forward Looking Statements Certain statements contained herein are “forward-looking statements” within the meaning of applicable securities laws and regulations. These forward-looking statements can generally be identified by the use of words such as “anticipate,” “expect,” “believe,” “could,” “estimate,” “feel,” “forecast,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will,” “would,” and similar words, phrases or expressions and variations or negatives of these words, although not all forward-looking statements contain these identifying words. Forward-looking statements by their nature address matters that are, to different degrees, uncertain, such as statements regarding the estimated or anticipated future results of the combined company following the proposed merger, the anticipated benefits of the proposed merger, including estimated synergies, the expected timing of completion of the proposed merger and related transactions and other statements that are not historical facts. These statements are based on the current expectations of Keurig Green Mountain Parent Holdings Corp. and Dr Pepper Snapple Group, Inc. management and are not predictions of actual performance. These forward-looking statements are subject to a number of risks and uncertainties regarding the combined company’s business and the proposed merger and actual results may differ materially. These risks and uncertainties -

Antojitos (Appetizers)

EAT IN TAKE OUT OPEN 7 DAYS A WEEK FROM 11AM HAPPY HOUR MON-FRI 4–6PM IN A HURRY? CALL AHEAD AND PLACE YOUR TO GO ORDER AND WE’LL HAVE IT READY AND WAITING WHEN YOU ARRIVE. DINING IN? 207·494·1000 FEEL FREE TO CALL ONE HOUR AHEAD TO GET YOUR www.elrayotaqueria.com NAME ON OUR WAITING LIST. ANTOJITOS (APPETIZERS) GOLDEN PAPAS FRITAS – 3.95 CHIPS – 1.25 JET PINEAPPLE – 3.95 fried Maine potatoes drizzled with w/ salsa – 3.75 on a stick dusted with chile powder, garlic aioli† w/ guacamole – 5.75 salt & lime w/ salsa & guacamole – 8.25 FRIED PLANTAINS – 4.95 FUNDIDO – 6.95 with chipotle mayo CHEESE NACHOS – 4.25 warm cheese dip with cilantro, rajas & with chorizo, shredded pork, grilled your choice of mushrooms or SWEET & SPICY chicken, ground beef, or organic black housemade chorizo PEPITAS – 2.95 beans & grilled veggies – 5.95 Served with corn chips pumpkin seeds roasted with chile pepper, toasted cumin, cinnamon & sugar MEXICO CITY STYLE CORN Turn your nachos into a GRANDE ON THE COB – 4.95 CORN-JALAPEÑO meal by adding guacamole, shredded basted with chipotle mayonnaise & FRITTERS – 5.95 lettuce, housemade crema, radishes, dusted with cotija cheese with jalapeño jelly pickled jalapeños, cilantro & taquerera salsa add 4.95 CHILE FRITAS – 7.95 DAILY SOUP– 4.95 an El Rayo favorite! Fried shishito peppers dusted with sea salt SALSAS SMALL 1.25 LARGE 2.50 PICO DE GALLO SALSA CORN SALSA *SALSA VERDE TAQUERERA SALSA *RANCHERO SAUCE OUR FAMOUS CHIPOTLE DIPPING SAUCE GRILLED PINEAPPLE *SMOKEY CHIPOTLE-TOMATO SALSITA SAUCE *Served warm FRESH LOCAL SUSTAINABLE We source locally grown and raised ingredients whenever possible and cook with sustainable seafood, naturally raised meats and organic black beans. -

Drinks & Beverages

Drinks & Beverages Cocktails BEVERAGES Pepsi / Diet Pepsi/ Mist 3 Americano ................................................ 10 Sierra Mist 3 One of Italy’s favorite cocktail: Campari, Vermouth Rosso, club soda Ginger Ale 3 Aperol Spritz ........................................... 10 Milk 3 Orangina (bottle) 4 Aperol, Prosecco (Italian champagne), club soda Orange Juice 4 Montecatini Cosmopolitan ........................ 12 Grapefruit Juice 4 Cranberry Juice 4 Grey Goose vodka, triple sec, fresh lime, cranberry juice Pineapple Juice 4 Monte’s Wallbanger .................................. 12 San Pellegrino (bottle) 4 Tito’s Vodka, Italian Galliano liqueur, orange juice Angry Orchard Hard Cider (Alcoholic) 5 Ginger Beer (Non‐Alcoholic) 4 Flaming B-52 ............................................ 15 Three layers: Grand Marnier, Irish Bailey Cream, Kahlua; Set on Fire! COFFEE AND HOT DRINKS Godiva Chocolate Martini .......................... 10 American Coffee 3 Hot Tea 3 Godiva dark chocolate liqueur, Smirnoff vodka, fresh cream Café Latte 5 Toasted Almond Martini ............................ 10 Café Mocha 5 Amareo Di Sarronno, Kahlua, Smirnoff vodka, fresh cream Expresso 4 Expresso Double 6 Cappuccino 5 Mocktails Hot Chocolate 5 Tuscan Cooler ......................................... 6 BOTTLE BEER Montecani combinaon of juices, sodas, fresh fruits, rosemary Anchor Steam 5 Budweiser 4 No-Jitos ................................................... 5 Coors Light 4 Fresh mint leaves, fresh lemon, fresh lime, club soda Corona (Mexico) 6 Shirley Temple -

DR PEPPER SNAPPLE GROUP ANNUAL REPORT DPS at a Glance

DR PEPPER SNAPPLE GROUP ANNUAL REPORT DPS at a Glance NORTH AMERICA’S LEADING FLAVORED BEVERAGE COMPANY More than 50 brands of juices, teas and carbonated soft drinks with a heritage of more than 200 years NINE OF OUR 12 LEADING BRANDS ARE NO. 1 IN THEIR FLAVOR CATEGORIES Named Company of the Year in 2010 by Beverage World magazine CEO LARRY D. YOUNG NAMED 2010 BEVERAGE EXECUTIVE OF THE YEAR BY BEVERAGE INDUSTRY MAGAZINE OUR VISION: Be the Best Beverage Business in the Americas STOCK PRICE PERFORMANCE PRIMARY SOURCES & USES OF CASH VS. S&P 500 TWO-YEAR CUMULATIVE TOTAL ’09–’10 JAN ’10 MAR JUN SEP DEC ’10 $3.4B $3.3B 40% DPS Pepsi/Coke 30% Share Repurchases S&P Licensing Agreements 20% Dividends Net Repayment 10% of Credit Facility Operations & Notes 0% Capital Spending -10% SOURCES USES 2010 FINANCIAL SNAPSHOT (MILLIONS, EXCEPT EARNINGS PER SHARE) CONTENTS 2010 $5,636 NET SALES +2% 2009 $5,531 $ 1, 3 21 SEGMENT +1% Letter to Stockholders 1 OPERATING PROFIT $ 1, 310 Build Our Brands 4 $2.40 DILUTED EARNINGS +22% PER SHARE* $1.97 Grow Per Caps 7 Rapid Continuous Improvement 10 *2010 diluted earnings per share (EPS) excludes a loss on early extinguishment of debt and certain tax-related items, which totaled Innovation Spotlight 23 cents per share. 2009 diluted EPS excludes a net gain on certain 12 distribution agreement changes and tax-related items, which totaled 20 cents per share. See page 13 for a detailed reconciliation of the Stockholder Information 12 7 excluded items and the rationale for the exclusion. -

Vaughan, Ontario L4H 5A1 | 905.673.9880 | Email: Info@Allmart .Ca | Allmart.Ca Customer

Customer #: #REF! Phone #: Delivery Date: Contact: Customer Order #: ENERGY 473ml Can 24x680ml Can COKECOKE 24 24x355mlx355ml Can Can PEPSIPEPSI 24 24x355mlx355ml Can Can 24x340ml 24x330 Canml Can 24x330ml Cans Can (12x355ml) ENERGY 12x473ml Can 24x680ml Can 24x680ml 24x680 mlCan Can Coca-Cola Classic Pepsi SAN PELLEGRINO U.S. Import MONSTER ARIZONA $1.29 ARIZONA Diet Coke Diet Pepsi Aranciata Cherry Coke Assault Arnold Palmer ½+½ Import 99¢ Coke Zero 7-UP Aranciata Rossa Vanilla Coke Khaos Fruit Punch Georgia Peach Gr.Tea Sprite Crush Orange Clementina Cherry Vanilla Coke Original (Green) Green Tea Lemonade Canada Dry Ginger Ale Dr Pepper Limonata Orange Vanilla Coke Lo-Cal Grapeade Orangeade 12x355ml Mug Root Beer Melograno E Arancia Crush Peach Ultra Blue Kiwi Strawberry Red Apple Green Tea Zero Sugar Zero Caffeine Schweppes Ginger Ale Pompelmo Crush Strawberry Ultra Red Lemon Tea Import (Non-Priced) Diet Coke With Lime Crush Variety Pack Momenti Dr Pepper Cherry Ultra Violet Mucho Mango African Rooibos Red T. Coca-Cola Stevia 12x355ml Clementine & Peach Dr Pepper Cherry Vanilla Zero Ultra Peach Tea Cherry Lime Rickey Sprite Zero Crush Cream Soda Lemon & Raspberry Dr Pepper Vanilla Float Raspberry Tea Mango ½ & ½ Fresca Diet Crush Orange Pomeg. & Blackcurrant Fanta Berry RED BULL (24x250ml) Sweet Tea (South.Style) Tropical ½ & ½ Barq's Root Beer Diet Dr Pepper 250ml Fanta Peach Regular Watermelon Canada Dry Club Soda 7-UP Limone + Tea Fanta Strawberry Sugar Free Arnold Palmer ½+½ Canada Dry Diet Ale 7-UP Zero Pesca + Tea MTN Dew Major -

Comvita Limited 2011 Independent Adviser's Report

Comvita Limited Independent Adviser’s Report On the Full Takeover Offer from Cerebos New Zealand Limited November 2011 COMVITA LIMITED TARGET COMPANY STATEMENT 2011 29 Table of Contents Glossary..........................................................................................................................................................................................3 1. Terms of the Cerebos Offer .................................................................................................................................................4 1.1 Background..................................................................................................................................................................4 1.2 Details of the Cerebos Offer..........................................................................................................................................4 1.3 Requirements of the Takeovers Code ...........................................................................................................................5 1.4 Overview of Cerebos ....................................................................................................................................................6 2. Scope of the Report..............................................................................................................................................................7 2.1 Purpose of the Report ..................................................................................................................................................7 -

Teachers' Retirement System of Louisiana: Comprehensive Annual Financial Report--A Component Unit of the State of Louisiana for the Fiscal Year Ended June 30, 1996

DOCUMENT RESUME ED 405 307 SP 037 185 TITLE Teachers' Retirement System of Louisiana: Comprehensive Annual Financial Report--A Component Unit of the State of Louisiana for the Fiscal Year Ended June 30, 1996. INSTITUTION Teachers Retirement System of Louisiana, Baton Rouge. PUB DATE Oct 96 NOTE 138p. PUB TYPE Reports Descriptive (141) EDRS PRICE MF01/PC06 Plus Postage. DESCRIPTORS Elementary Secondary Education; Fringe Benefits; Higher Education; *Investment; Personnel Policy; *Retirement Benefits; *Teacher Employment Benefits; *Teacher Retirement IDENTIFIERS Financial Planning; Financial Reports; *Louisiana; *Retirement Planning ABSTRACT The annual Financial Report of the Teachers' Retirement System of Louisiana is divided into six main sections. The Introductory Section includes the letter of transmittal, names of the Board of Trustees, staff, and consultants; the organization chart; copy of certificate of achievement for excellence in financial reporting for 1995 financial report; summary of 1995-96 legislative acts; and a plan summary. The Financial Section includes the Independent Auditor's Report, General Purpose Finance Statements, Required Supplementary Information, and Supporting Schedules. The Investment Section includes reports on investment activity and policy, an Investment Summary, a list of investments, net earnings on investments and performance measures, annual rates of return, and Summary Schedule of Commissions Paid to Brokers. The Actuarial Section includes a summary of assumptions; Actuarial Valuation Balance Sheet; summary, reconciliation, and amortization of unfunded actuarial liabilities; and membership data. The Statistical Section provides data on vested and nonvested members, retirees, benefit recipients, benefit expenses, revenues, expenses, and participating employers. The final section outlines the Optional Retirement Plan, the Deferred Retirement Option Plan, and Option 5.