Keurig Dr Pepper Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2016 Social Ceo Report

2016 SOCIAL CEO REPORT Are Fortune 500 CEOs as digitally engaged as they should be? #socialceo SPONSORED BY: EXECUTIVE SUMMARY / 03 MAJOR FINDINGS / 04 LINKEDIN / 07 TWITTER / 08 FACEBOOK / 09 INSTAGRAM / 10 YOUTUBE AND GOOGLE+ / 11 YEAR-OVER-YEAR ANALYSIS / 12 ABOUT THE RESEARCH / 13 THE CHALLENGE / 14 A WORD FROM OUR SPONSOR / 15 HOW WE DID IT We identifed the social profles of every CEO on the Fortune 500 list across the six most popular networks: Twitter, Facebook, LinkedIn, Google+, Instagram, and YouTube. We weighed the legitimacy of these social profles against a strict set of criteria to ensure consistency in reporting. You can read more about our methodology at the end of the report. EXECUTIVE SUMMARY 2016 has been an interesting year Despite calls from many social media for the leading social media channels evangelists for CEOs to increase their as they vie for subscribers and use of social media, not much has infuencers, to grow advertising changed since 2015. While LinkedIn’s revenues. The past year has seen Infuencer program seems to be the strategic acquisition of LinkedIn gaining traction with CEOs, and by Microsoft. Meanwhile, YouTube Twitter use is also on the rise, continued to evolve and grow as a Facebook, Google+, Instagram, and streaming video platform, with YouTube remain the top choices for potential competitors—Facebook Live, corporate marketing teams to present LinkedIn Infuencer videos, Twitter’s corporate messaging. Periscope—vying to capture users. LinkedIn remains the frst channel CEOs adopt, followed by Twitter. 60% of Fortune 500 CEOs have LinkedIn’s Infuencer program no social media presence at all, features some of the most active compared to 61% in 2015. -

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

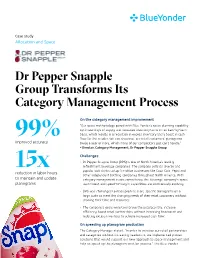

Dr Pepper Snapple Group Transforms Its Category Management Process

Case study Allocation and Space Dr Pepper Snapple Group Transforms Its Category Management Process On the category management improvement “Our space methodology paired with Blue Yonder’s space planning capability optimizes days of supply and increases inventory turns on an item-by-item basis, which results in a reduction in excess inventory and a boost in cash 99% flow for the retailer. We can also reset our retail customers’ planograms improved accuracy twice a year or more, which many of our competitors just can’t handle.” - Director, Category Management, Dr Pepper Snapple Group Challenges • Dr Pepper Snapple Group (DPS) is one of North America’s leading refreshment beverage companies. The company sells its diverse and 15x popular soft drinks to top franchise businesses like Coca-Cola, Pepsi and reduction in labor hours other independent bottling companies throughout North America. With to maintain and update category management a core competency, the beverage company’s space, planograms assortment and speed-to-insight capabilities are continuously evolving. • DPS was challenged to mass produce store-specific planograms on a large scale to meet the changing needs of their retail customers without draining their time and resources. • The company’s goals were to improve the accuracy rate, increase efficiency, boost retail partnerships without increasing headcount and reducing excess inventory to achieve increased cash flow. On speeding up planogram production The Category Manager stated, “In order to increase our retail partnerships and categories without increasing headcount, we implemented proven solutions that would support our new approach to space management and help us speed up the planogram creation process.” The Blue Yonder solution automated the large-scale production of Blue Yonder’s expertise optimized, store-specific planograms, increasing Dr Pepper Snapple Group’s accuracy rate to 99 percent. -

Fund Holdings As of 6/30/2021 Massmutual Balanced Fund Invesco Prior to 5/1/2021, the Fund Name Was Massmutual Premier Balanced Fund

Fund Holdings As of 6/30/2021 MassMutual Balanced Fund Invesco Prior to 5/1/2021, the Fund name was MassMutual Premier Balanced Fund. Fund Shares or Par Position Market Security Name Ticker CUSIP Weighting % Amount Value Apple Inc AAPL 037833100 3.91 48,433 6,633,384 Microsoft Corp MSFT 594918104 3.45 21,552 5,838,437 USTREAS T-Bill Auction Ave 3 Mon 1.69 2,862,977 JPMorgan Chase & Co JPM 46625H100 1.56 16,948 2,636,092 Verizon Communications Inc VZ 92343V104 1.45 43,768 2,452,321 The Home Depot Inc HD 437076102 1.42 7,556 2,409,533 Intel Corp INTC 458140100 1.29 38,961 2,187,271 Procter & Gamble Co PG 742718109 1.04 13,105 1,768,258 Cisco Systems Inc CSCO 17275R102 1.03 32,830 1,739,990 UnitedHealth Group Inc UNH 91324P102 1.00 4,215 1,687,855 Comcast Corp Class A CMCSA 20030N101 0.94 28,021 1,597,757 AT&T Inc T 00206R102 0.91 53,587 1,542,234 Oracle Corp ORCL 68389X105 0.83 18,031 1,403,533 Deere & Co DE 244199105 0.76 3,635 1,282,101 Accenture PLC Class A ACN G1151C101 0.74 4,237 1,249,025 Johnson Controls International PLC JCI G51502105 0.74 18,185 1,248,037 Visa Inc Class A V 92826C839 0.71 5,152 1,204,641 Texas Instruments Inc TXN 882508104 0.70 6,128 1,178,414 Costco Wholesale Corp COST 22160K105 0.67 2,850 1,127,660 Bank of America Corp BAC 060505104 0.64 26,192 1,079,896 Broadcom Inc AVGO 11135F101 0.63 2,223 1,060,015 Abbott Laboratories ABT 002824100 0.57 8,348 967,784 Target Corp TGT 87612E106 0.56 3,949 954,631 Honeywell International Inc HON 438516106 0.56 4,324 948,469 Goldman Sachs Group Inc GS 38141G104 0.53 2,374 901,004 -

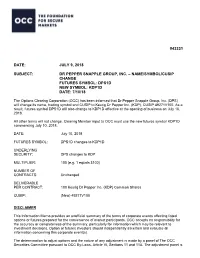

Dr Pepper Snapple Group, Inc. – Name/Symbol/Cusip Change Futures Symbol: Dps1d New Symbol: Kdp1d Date: 7/10/18

#43331 DATE: JULY 9, 2018 SUBJECT: DR PEPPER SNAPPLE GROUP, INC. – NAME/SYMBOL/CUSIP CHANGE FUTURES SYMBOL: DPS1D NEW SYMBOL: KDP1D DATE: 7/10/18 The Options Clearing Corporation (OCC) has been informed that Dr Pepper Snapple Group, Inc. (DPS) will change its name, trading symbol and CUSIP to Keurig Dr Pepper Inc. (KDP), CUSIP 49271V100. As a result, futures symbol DPS1D will also change to KDP1D effective at the opening of business on July 10, 2018. All other terms will not change. Clearing Member input to OCC must use the new futures symbol KDP1D commencing July 10, 2018. DATE: July 10, 2018 FUTURES SYMBOL: DPS1D changes to KDP1D UNDERLYING SECURITY: DPS changes to KDP MULTIPLIER: 100 (e.g. 1 equals $100) NUMBER OF CONTRACTS: Unchanged DELIVERABLE PER CONTRACT: 100 Keurig Dr Pepper Inc. (KDP) Common Shares CUSIP: (New) 49271V100 DISCLAIMER This Information Memo provides an unofficial summary of the terms of corporate events affecting listed options or futures prepared for the convenience of market participants. OCC accepts no responsibility for the accuracy or completeness of the summary, particularly for information which may be relevant to investment decisions. Option or futures investors should independently ascertain and evaluate all information concerning this corporate event(s). The determination to adjust options and the nature of any adjustment is made by a panel of The OCC Securities Committee pursuant to OCC By-Laws, Article VI, Sections 11 and 11A. The adjustment panel is comprised of representatives from OCC and each exchange which trades the affected option. The determination to adjust futures and the nature of any adjustment is made by OCC pursuant to OCC By- Laws, Article XII, Sections 3, 4, or 4A, as applicable. -

Quaker Sees an ROI of Over 6X by Reaching Amazon Shoppers on Amazon and Across the Web1

Case Study Amazon.com | Amazon Advertising Platform (AAP) Quaker sees an ROI of over 6X by reaching Amazon shoppers on Amazon and across the web1 The Quaker Oats company, a leading manufacturer of packaged grocery The AMG Solution foods and subsidiary of PepsiCo, Inc., worked with Amazon Media Quaker and AMG launched a campaign using custom Group (AMG) to drive purchase considerations and sales of Quaker coupon ads that ran on Amazon.com and amplified Oatmeal Squares Cereal. They assumed the AMG campaign would campaign reach with the Amazon Advertising Platform deliver on their objectives on Amazon, but they were also interested (AAP). The AMG campaign also revealed exact groups in learning what effect the campaign would have on offline sales in of Amazon customers who were who were most likely traditional brick and mortar stores. Through a mix of standard AMG to take action after exposure to their ads such as those post-campaign measurements and AMG’s partnership with Nielsen who were in-market for other grocery products. With HomeScan, Quaker was able to better understand the effect of their carefully targeted ads served across Amazon and campaign on key success metrics – both on and offline. AAP, Quaker maximized exposure among groups that mattered most, yielding a strong ROI. Online Success Metrics Total Campaign ROI For every $1 spent on advertising with Amazon, Quaker recognized over $6 in incremental sales Offline Sales Boost ¡ 26% lift in offline sales as a result of the on-Amazon portion of the campaign ¡ 29% lift in offline sales as a result of the AAP portion of the campaign On-Amazon Success Metrics On average, users who were exposed to Quaker ads were: ¡ 5x more likely to consider Quaker Oatmeal Squares versus those who weren’t ¡ Almost 2x more likely to purchase Quaker Oatmeal Squares versus those who weren’t About The Quaker Oats Company: The Quaker Oats Company, headquartered in Chicago, is a Methodology unit of PepsiCo, Inc., one of the world’s largest consumer packaged goods companies. -

Jaimesen Heins Keurig Dr Pepper Waterbury, Vermont As Senior

Jaimesen Heins Keurig Dr Pepper Waterbury, Vermont As Senior Counsel – Operations & Commercial Litigation to Keurig Dr Pepper, Mr. Heins supports global commercial operations matters for the business, with a focus on commercial litigation, contract negotiation and advisory responsibilities. Mr. Heins provides strategic business advice and partners with company leaders to meet the needs of Keurig Dr Pepper’s business. Mr. Heins previously served as General Counsel to Burton Snowboards, overseeing all legal affairs of the company, including corporate governance, commercial transactions, intellectual property, brand licensing, real estate, employment, regulatory and litigation matters. Keurig Dr Pepper (NYSE: KDP) is a leading coffee and beverage company in North America, with annual revenue in excess of $11 billion. Formed in 2018 with the merger of Keurig Green Mountain and Dr Pepper Snapple Group, we have leadership positions in soft drinks, specialty coffee and tea, water, juice and juice drinks and mixers, and we market the #1 single serve coffee brewing system in the U.S. We have an unrivaled distribution system that enables our portfolio of more than 125 owned, licensed and partner brands to be available nearly everywhere people shop and consume beverages. With a wide range of hot and cold beverages that meet virtually any consumer need, KDP key brands include Keurig®, Dr Pepper®, Green Mountain Coffee Roasters®, Canada Dry®, Snapple®, Bai®, Mott’s® and The Original Donut Shop®. We have more than 25,000 employees and more than 120 offices, manufacturing plants, warehouses and distribution centers across North America. . -

Product Differentiation and Mergers in the Carbonated Soft Drink Industry

Product Differentiation and Mergers in the Carbonated Soft Drink Industry JEAN-PIERRE DUBE´ University of Chicago Graduate School of Business Chicago, IL 60637 [email protected] I simulate the competitive impact of several soft drink mergers from the 1980s on equilibrium prices and quantities. An unusual feature of soft drink demand is that, at the individual purchase level, households regularly select a variety of soft drink products. Specifically, on a given trip households may select multiple soft drink products and multiple units of each. A concern is that using a standard discrete choice model that assumes single unit purchases may understate the price elasticity of demand. Tomodel the sophisticated choice behavior generating this multiple discreteness,Iuse a household-level scanner data set. Market demand is then computed by aggregating the household estimates. Combining the aggregate demand estimates with a model of static oligopoly, I then run the merger simulations. Despite moderate price increases, I find substantial welfare losses from the proposed merger between Coca-Cola and Dr. Pepper. I also find large price increases and corresponding welfare losses from the proposed merger between Pepsi and 7 UP and, more notably, between Coca-Cola and Pepsi. 1. Introduction With the advent of aggregate brand-level data collected at supermarket checkout scanners, researchers have begun to use structural econo- metric models for policy analysis. The rich content of scanner data enables the estimation of demand systems and their corresponding cross-price elasticities. The areas of merger and antitrust policy have been strong beneficiaries of these improved data. Recent advances in structural approaches to empirical merger analysis consist of combining Iamvery grateful to my thesis committee: David Besanko, Tim Conley, Sachin Gupta, and Rob Porter. -

OLSTEIN ALL CAP VALUE FUND SCHEDULE of INVESTMENTS March 31, 2021 (Unaudited) COMMON STOCKS - 84.7% Shares Value Advertising Agencies - 1.4% Omnicom Group, Inc

OLSTEIN ALL CAP VALUE FUND SCHEDULE OF INVESTMENTS March 31, 2021 (Unaudited) COMMON STOCKS - 84.7% Shares Value Advertising Agencies - 1.4% Omnicom Group, Inc. 140,000 $ 10,381,000 Aerospace & Defense - 1.9% L3Harris Technologies, Inc. 39,000 7,904,520 Raytheon Technologies Corporation 77,000 5,949,790 13,854,310 Air Delivery & Freight Services - 2.4% FedEx Corporation 35,000 9,941,400 United Parcel Service, Inc. - Class B 45,000 7,649,550 17,590,950 Airlines - 2.1% Delta Air Lines, Inc. (a) 158,000 7,628,240 JetBlue Airways Corporation (a) 353,000 7,180,020 14,808,260 Auto Manufacturers - 1.0% General Motors Company (a) 129,000 7,412,340 Beverages - 0.6% Keurig Dr Pepper, Inc. (b) 124,000 4,261,880 Building Products - 1.2% Carrier Global Corporation 198,000 8,359,560 Capital Markets - 1.4% Goldman Sachs Group, Inc. 31,500 10,300,500 Chemicals - 1.8% Corteva, Inc. 201,000 9,370,620 Eastman Chemical Company 31,000 3,413,720 12,784,340 Commercial Banks - 5.8% Citizens Financial Group, Inc. 154,000 6,799,100 Fifth Third Bancorp 228,000 8,538,600 Prosperity Bancshares, Inc. 68,000 5,092,520 U.S. Bancorp 181,000 10,011,110 Wells Fargo & Company 280,000 10,939,600 41,380,930 Commercial Services - 1.6% Moody's Corporation 18,500 5,524,285 S&P Global, Inc. 17,000 5,998,790 11,523,075 Communications Equipment - 1.9% Cisco Systems, Inc. 266,000 13,754,860 Computers - 1.9% Apple, Inc. -

Why Keurig Is Acquiring Dr. Pepper (Rabobank)

January 2018 Why Keurig Is Acquiring Dr Pepper Breaking Down the Walls Between Coffee and Soft Drinks RaboResearch Food & Agribusiness far.rabobank.com Summary The strategic basis for the Keurig – DPS combination is clear: to create a company that Jim Watson combines hot/cold beverages and retail/office/e-commerce distribution in order to match the Senior Analyst - Beverages +1 212 916 7943 way its consumers experience the beverage world. The strategic side of the combination will take significant execution skill, while the financial side (creating synergies and an exit strategy) looks to be more straightforward. Details of the acquisition On January 29, 2018 Keurig agreed to a merger with Dr Pepper Snapple to form Keurig Dr Pepper (KDP). Dr Pepper Snapple shareholders will receive USD 103.75 per share (for a total cash value of USD 19 billion) and retain a 13% stake in the new public company. The total value to DPS shareholders represents an EV/EBITDA multiple of 17.6x. JAB, together with its partners, will make an equity investment of USD 9 billion to help finance this transaction. Coffee + soft drink opportunities and challenges KDP integrates hot and cold beverages to a degree we haven’t seen before, but we see this as a step towards a more combined coffee and soft-drink world. The most concrete example presented by the company of top-line synergies is the ability to increase distribution of ready-to- drink coffee products, with access to the broader JAB coffee portfolio. We wrote about the blurring lines between coffee and soft drinks in our note Coffee Joins the Beverage Party: What Happens when a Can of Coffee Looks Just Like a Can of Soda? We are bullish on the potential for ready-to-drink coffee in North America – and believe the new KDP could build a real challenger to Starbucks/Pepsi in this space. -

Carbonated Soft Drinks in the US Through 2025

Carbonated Soft Drinks in the U.S. through 2025: Market Essentials 2021 Edition (To be published September 2021. Data through 2020. Market projections through 2025.) More than 120 Excel tables plus an executive summary detailing trends and comprehensive profiles of leading companies, their brands and their strategies. his comprehensive market research report on the number-two T beverage category examines trends and top companies' For A Full strategies. It provides up-to-date statistics on leading brands, Catalog of packaging, quarterly growth and channels of distribution. It also Reports and offers data on regional markets, pricing, demographics, Databases, advertising, five-year growth projections and more. Go To The report presents the data in Excel spreadsheets, which it supplements with a concise executive summary highlighting key bmcreports.com developments including the impact of the coronavirus pandemic as well as a detailed discussion of the leading carbonated soft drink (CSD) companies. INSIDE: REPORT OVERVIEW A brief discussion of key AVAILABLE FORMAT & features of this report. 2 PRICING TABLE OF CONTENTS Direct Download A detailed outline of this Excel sheets, PDF, PowerPoint & Word report’s contents and data tables. 7 $4,395 To learn more, to place an advance order or to inquire about SAMPLE TEXT AND additional user licenses call: Charlene Harvey +1 212.688.7640 INFOGRAPHICS ext. 1962 [email protected] A few examples of this report’s text, data content layout and style. 13 HAVE Contact Charlene Harvey: 212-688-7640 x 1962 QUESTIONS? [email protected] Beverage Marketing Corporation 850 Third Avenue, 13th Floor, New York, NY 10022 Tel: 212-688-7640 Fax: 212-826-1255 The answers you need Carbonated Soft Drinks in the U.S. -

Employee Well-Being

Employee Well-being Healthy Living, PepsiCo’s employee well-being program, is designed to help employees and their families improve their physical, financial, and emotional health. The program is based on three pillars of well-being, offering employees a variety of programs to help them: • Be Well—Programs to get healthy, get moving, and be safe. • Find Balance—Programs to manage stress, build resilience, and improve their financial well-being and work/life quality. • Get Involved—Programs to foster community involvement and family and social connections, a critical component to well-being. To provide a sense of the scope and reach of Healthy Living, in the U.S. alone, we offer a variety of programs including: a wellness questionnaire and biometric screening to gauge health status; flu shots; telephonic wellness coaching; stress, resilience, and sleep management programs; weight management programs; and fitness and nutrition programs. Through a digital well-being platform launched in January 2018, participants earn points through engagement in these programs, which they can redeem for rewards such as gift cards, Health Savings Account contributions, and sweepstakes entries. Additionally, we offer a healthy pregnancy program; a tobacco-free program; a back care program; care management programs for chronic conditions (like diabetes); and Employee Assistance Program and preventive care coverage. These programs are available to all benefits- eligible employees, as well as spouses and partners who are already covered under the PepsiCo medical plan. In 2019, over 60,000 members registered on the digital well-being platform. Of those registered, two-thirds completed a wellness questionnaire and 85 percent earned points by participating in programs.