Dr Pepper Snapple Group, Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Top 5G Stock to Buy in 2019 the 5G Stock We Love for 2019 Is Canada-Based Telus Corp

Contents INTRODUCTION Page i 2019 Will Bring Unprecedented Moneymaking Opportunities CHAPTER 1 Page 1 The Seven “No-Brainer” Stocks to Buy in 2019 – Plus Our “Wild Card” Pick CHAPTER 2 Page 12 The Only Stock to Own Ahead of the $1.3 Trillion 5G Revolution CHAPTER 3 Page 17 How to Turn Water Scarcity into a 40% – Plus Gain CHAPTER 4 Page 22 The Secret Way to Profit from the 11 “Unicorn” IPOs Slated for 2019 CHAPTER 5 Page 35 The Cryptocurrency with 1,000% Growth Potential CHAPTER 6 Page 40 Five Income Stocks with Double-Digit Growth Ahead CHAPTER 7 Page 47 Bank 145% Gains in the Biggest Year Yet for Cannabis Investors CHAPTER 8 Page 52 The Three Trendy Stocks to Avoid in 2019 MONEY MORNING THE ULTIMATE MONEY MAKING GUIDE FOR 2019 Introduction: 2019 Will Bring Unprecedented Moneymaking Opportunities Here at Money Morning, we have one goal: to make investing profitable. In 2018 alone, our readers had the chance to book gains of 333%, 440%, and even 478% on stock trades that came from our research. We also kept our readers at the forefront of the hottest investing trends, like cannabis legalization. After we told Money Morning subscribers about top cannabis pick Tilray Inc., the stock soared 262%. But you wouldn’t know these opportunities were out there from listening to mainstream financial news… Cable news focused on the trade war as major indexes struggled to stay in the black. And Wall Street pundits couldn’t stop talking about the evils of Facebook as it slid 24% this year. -

400 Refreshing Punch Recipes

TABLE OF CONTENTS 1. Yellow Fruit Punch 2. Zesty Punch Sipper 3. Wassail Punch 4. Watermelon Punch 5. What Hit Me Punch 6. Whisky Punch 7. White Grape~ Tangerine~ & Asti-Spumante Punch 8. White House Pink Fruit Punch (En) 9. White Sangria Punch (Nonalcholic) 10. "No Punch" Champagne 11. "Sting-Like-A-Bee" Punch 12. 1, 2, 3, Punch 13. 4-Fruit Wedding Punch 14. 7-Up Punch 15. Alkoholfreier Planter`s Punch 16. Aloha Fruit Punch 17. Amber Cider Punch 18. Amelia Island Punch 19. Angelfrost Punch 20. Annie's Rosemary Fruit Punch 21. Apple Orchard Punch 22. Apple Slush Punch 23. Apricot Punch 24. Apricot Mist Punch 25. Artillery Punch 26. Artillerymen's Punch 27. Atlanta Coffee Ice Cream Punch 28. Aunt Cindy's Punch 29. Aunt Louise's Wassail Punch 30. Autumn Apple Punch 31. Autumn Punch 32. Aztec Punch 33. Banana Punch 34. Banana-Orange-Pineapple Punch 35. Becky's Wedding Punch 36. Bernice's Holiday Punch 37. Berry Colada Punch 38. Billy Clude Punch 39. Brandy Milk Punch 40. Bridal Fruit Punch (Non-Alcholic) 41. Bridal Sweet Punch 42. Brides Lunch Punch 43. Brown Cow Punch 44. Bubbling Jade Punch 45. Canadian Punch 46. Caribbean Guava Punch 47. Champagne Fruit Punch 48. Champagne Punch 49. Chatham Artillery Punch 50. Cheery Cherry Punch 51. Cherry Tea Punch 52. Chocolate Punch 53. Christmas Cherry Berry Punch 54. Christmas Cranberry Punch 55. Christmas Party Punch 56. Christmas Rum Punch 57. Christmas Snow Punch 58. Cider And Brandy Punch 59. Cider Fruit Punch A La Normande 60. Cider Punch 61. -

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

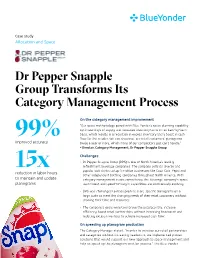

Dr Pepper Snapple Group Transforms Its Category Management Process

Case study Allocation and Space Dr Pepper Snapple Group Transforms Its Category Management Process On the category management improvement “Our space methodology paired with Blue Yonder’s space planning capability optimizes days of supply and increases inventory turns on an item-by-item basis, which results in a reduction in excess inventory and a boost in cash 99% flow for the retailer. We can also reset our retail customers’ planograms improved accuracy twice a year or more, which many of our competitors just can’t handle.” - Director, Category Management, Dr Pepper Snapple Group Challenges • Dr Pepper Snapple Group (DPS) is one of North America’s leading refreshment beverage companies. The company sells its diverse and 15x popular soft drinks to top franchise businesses like Coca-Cola, Pepsi and reduction in labor hours other independent bottling companies throughout North America. With to maintain and update category management a core competency, the beverage company’s space, planograms assortment and speed-to-insight capabilities are continuously evolving. • DPS was challenged to mass produce store-specific planograms on a large scale to meet the changing needs of their retail customers without draining their time and resources. • The company’s goals were to improve the accuracy rate, increase efficiency, boost retail partnerships without increasing headcount and reducing excess inventory to achieve increased cash flow. On speeding up planogram production The Category Manager stated, “In order to increase our retail partnerships and categories without increasing headcount, we implemented proven solutions that would support our new approach to space management and help us speed up the planogram creation process.” The Blue Yonder solution automated the large-scale production of Blue Yonder’s expertise optimized, store-specific planograms, increasing Dr Pepper Snapple Group’s accuracy rate to 99 percent. -

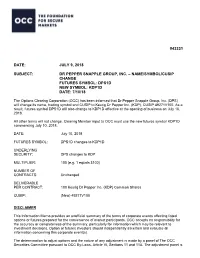

Dr Pepper Snapple Group, Inc. – Name/Symbol/Cusip Change Futures Symbol: Dps1d New Symbol: Kdp1d Date: 7/10/18

#43331 DATE: JULY 9, 2018 SUBJECT: DR PEPPER SNAPPLE GROUP, INC. – NAME/SYMBOL/CUSIP CHANGE FUTURES SYMBOL: DPS1D NEW SYMBOL: KDP1D DATE: 7/10/18 The Options Clearing Corporation (OCC) has been informed that Dr Pepper Snapple Group, Inc. (DPS) will change its name, trading symbol and CUSIP to Keurig Dr Pepper Inc. (KDP), CUSIP 49271V100. As a result, futures symbol DPS1D will also change to KDP1D effective at the opening of business on July 10, 2018. All other terms will not change. Clearing Member input to OCC must use the new futures symbol KDP1D commencing July 10, 2018. DATE: July 10, 2018 FUTURES SYMBOL: DPS1D changes to KDP1D UNDERLYING SECURITY: DPS changes to KDP MULTIPLIER: 100 (e.g. 1 equals $100) NUMBER OF CONTRACTS: Unchanged DELIVERABLE PER CONTRACT: 100 Keurig Dr Pepper Inc. (KDP) Common Shares CUSIP: (New) 49271V100 DISCLAIMER This Information Memo provides an unofficial summary of the terms of corporate events affecting listed options or futures prepared for the convenience of market participants. OCC accepts no responsibility for the accuracy or completeness of the summary, particularly for information which may be relevant to investment decisions. Option or futures investors should independently ascertain and evaluate all information concerning this corporate event(s). The determination to adjust options and the nature of any adjustment is made by a panel of The OCC Securities Committee pursuant to OCC By-Laws, Article VI, Sections 11 and 11A. The adjustment panel is comprised of representatives from OCC and each exchange which trades the affected option. The determination to adjust futures and the nature of any adjustment is made by OCC pursuant to OCC By- Laws, Article XII, Sections 3, 4, or 4A, as applicable. -

2011-2012 Sustainability Report

2011-2012 Sustainability Report Revised September 19, 2012 to correct tables on page 32 On the cover: Nature and its resources are critical to our business. Lake Tahoe, one of the world’s most pristine crystal blue alpine lakes, is just 15 minutes from The Ritz-Carlton®, Lake Tahoe (California), a LEED® Silver certified hotel (shown here). Contents Executive Letter 1 Marriott Business Values 12 Marriott and the Environment 30 About This Report 2 Workforce 13 Energy/Water/Waste/Carbon 32 Determining Materiality 2 Global Diversity and Inclusion 18 Supply Chain 37 Stakeholders 2 Human Rights 21 Green Buildings 40 Areas of Stakeholder Collaboration 3 Guest Satisfaction 22 Educating and Inspiring Associates and Guests 41 The Way We Do Business 6 Marriott Economic Hotel Development 23 Innovative Conservation Initiatives 43 Our Company 7 Marriott and Society 24 Awards and Recognition 45 Our Business Model 7 Shelter and Food/Poverty Alleviation 26 GRI Report Parameters 46 Global Growth 8 Vitality of Children 27 GRI Content Index 47 Governance 10 Readiness for Hotel Careers 28 Ethics 10 MARPAC Disbursements 11 1 To Our Stakeholders We are investing in sustainable development and innovative conservation initiatives, such as the following, that will provide long-term solutions to critical social and environmental issues. z In 2011, we announced our plan to open our first hotel in Port-au-Prince, Haiti, an area devastated by the 2010 earthquake. The tireless fundraising and volunteerism of our associates, hundreds with family connections in Haiti, inspired us personally to consider ways to help tourism return to the country. The hotel is scheduled to open in 2014, creating jobs and much-needed hotel and meeting space as Haiti recovers. -

PDF Product Guide

05/24/21 To Place an Order, Call (207)947-0321 Fax: (207)947-0323 ITEM # DESCRIPTION PACK ITEM # DESCRIPTION PACK COCKTAIL MIXES COFFEE FLAVORED 14678 ROLAND OLIVE JUICE DIRTY*MARTIN 12/25.4OZ 10927 MAINE'S BEST COFFEE JAMAICAN ME CRAZY 2 24/2.25OZ 2008 OCEAN SPRAY DRINK MIX BLOODY MARY 12/32 OZ 11282 MAINE'S BEST COFFEE VACATIONLND VANILLA 24/2.25OZ 26628 MAYSON'S MARGARITA MIX ON THE ROCKS 4/1 GAL 11516 MAINE'S BEST COFFEE HARBORSIDE HAZELNUT 24/2.25OZ 26633 MAYSON'S MARGARITA MIX FOR FROZEN 4/1 GAL 83931 NewEngland COFFEE REG FRNCH VAN CRAZE 24/2.5OZ 26634 MAYSON'S MARGARITA STRAWBERRY PUREE 4/1 GAL 83933 NewEngland COFFEE REG HAZELNUT CRAZE 24/2.5OZ 26637 MAYSON'S MARGARITA RASPBERRY PUREE 4/1 GAL 83939 NewEngland COFFEE REG PUMPKIN SPICE 24/2.5OZ 26639 MAYSON'S MARGARITA PEACH PUREE 4/1 GAL 83940 NewEngland COFFEE REG CINNAMON STICKY B 24/2.5OZ 26640 MAYSON'S MARGARITA WATERMELON PUREE 4/1 GAL 26724 MAYSON'S MARGARITA MANGO PUREE 4/1 GAL 83831 Packer DRINK MIX LEMON POWDER 12/1GAL COFFEE REGULAR 83890 COCO LOPEZ DRINK MIX CREAM COCONUT 24/15oz 10444 MAXWELL HOUSE COFFEE HOTEL & REST 112/1.6OZ 84011 Rose's SYRUP GRENADINE 12/1LTR 10479 Folgers COFFEE LIQ 100% COLOMBIAN 2/1.25L 10923 MAINE'S BEST COFFEE REG ACADIA BLEND 2O 42/2OZ 10924 MAINE'S BEST COFFEE REG COUNTY BLEND 1. 42/1.5OZ CAPPUCCINO 10930 MAINE'S BEST COFFEE REG DWNEAST DARK 2. 24/2.25OZ 90343 Int Coffee CAPPUCCINO FRENCH VAN 6/2LB 1410 Maxwellhse COFFEE REGULAR MASTERBLEND 64/3.75 OZ 23529 MAINE'S BEST COFFEE SEBAGO BLEND 42/2.25OZ 23531 NEW ENGLAND COFFEE EXTREME KAFFEINE -

Jaimesen Heins Keurig Dr Pepper Waterbury, Vermont As Senior

Jaimesen Heins Keurig Dr Pepper Waterbury, Vermont As Senior Counsel – Operations & Commercial Litigation to Keurig Dr Pepper, Mr. Heins supports global commercial operations matters for the business, with a focus on commercial litigation, contract negotiation and advisory responsibilities. Mr. Heins provides strategic business advice and partners with company leaders to meet the needs of Keurig Dr Pepper’s business. Mr. Heins previously served as General Counsel to Burton Snowboards, overseeing all legal affairs of the company, including corporate governance, commercial transactions, intellectual property, brand licensing, real estate, employment, regulatory and litigation matters. Keurig Dr Pepper (NYSE: KDP) is a leading coffee and beverage company in North America, with annual revenue in excess of $11 billion. Formed in 2018 with the merger of Keurig Green Mountain and Dr Pepper Snapple Group, we have leadership positions in soft drinks, specialty coffee and tea, water, juice and juice drinks and mixers, and we market the #1 single serve coffee brewing system in the U.S. We have an unrivaled distribution system that enables our portfolio of more than 125 owned, licensed and partner brands to be available nearly everywhere people shop and consume beverages. With a wide range of hot and cold beverages that meet virtually any consumer need, KDP key brands include Keurig®, Dr Pepper®, Green Mountain Coffee Roasters®, Canada Dry®, Snapple®, Bai®, Mott’s® and The Original Donut Shop®. We have more than 25,000 employees and more than 120 offices, manufacturing plants, warehouses and distribution centers across North America. . -

Introducing Keurig Dr Pepper

Introducing Keurig Dr Pepper Investor Presentation Creating a New Challenger In the Beverage Industry Highly Confidential January 2018 Forward Looking Statements Certain statements contained herein are “forward-looking statements” within the meaning of applicable securities laws and regulations. These forward-looking statements can generally be identified by the use of words such as “anticipate,” “expect,” “believe,” “could,” “estimate,” “feel,” “forecast,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will,” “would,” and similar words, phrases or expressions and variations or negatives of these words, although not all forward-looking statements contain these identifying words. Forward-looking statements by their nature address matters that are, to different degrees, uncertain, such as statements regarding the estimated or anticipated future results of the combined company following the proposed merger, the anticipated benefits of the proposed merger, including estimated synergies, the expected timing of completion of the proposed merger and related transactions and other statements that are not historical facts. These statements are based on the current expectations of Keurig Green Mountain Parent Holdings Corp. and Dr Pepper Snapple Group, Inc. management and are not predictions of actual performance. These forward-looking statements are subject to a number of risks and uncertainties regarding the combined company’s business and the proposed merger and actual results may differ materially. These risks and uncertainties -

Manitoba Liquor & Lotteries Category Price List Effective July 1, 2021

COMPUTER PRICE LIST BY BRAND CATEGORY Effective: July 1, 2021 LISTE DES PRIX PREPAREE PAR ORDINATEUR Entrée en vigueur le 1 juillet, 2021 TABLE OF CONTENTS MANITOBA LIQUOR & LOTTERIES PRICE LIST – BRAND CATEGORY - July 1, 2021 BEER WINE - CANADIAN Manitoba Liquor & Lotteries Distributed 136-143 Canadian Bulk Wine / Vin en Bloc 40 Canadian Flavoured Wine / Vins Aromatises 40 Canadian Fruit Wine / Vins de fruits-canadien 41 REFRESHMENT BEVERAGES Canadian Icewine / Vins de Glace 41-42 Cider / Cidres 123-126 Canadian Sparkling Wine / Vins Mousseaux-Canadien 43 Coolers - Wine and Spirit Based / à Base de Vin et D'Alcool 126-136 Canadian Red Wine / Vins Rouges-Canadien 43-49 Ready to Drink Non Alcohol/Prêt à boire non alcoolisée 136 Canadian Rosé Wine / Vin de Table-Rose Canadien 49-50 Canadian White Wine / Vins Blanc-Canadien 50-55 Canadian Miscellaneous Wine / Vins Divers-Canadien 42-43 LIQUEUR/LIQUOR (listed in alphabetical order by flavour) 5-12 WINE - IMPORTED SPIRITS Imported Bulk Wine / Vin en Bloc 55-56 Brandy / Eau-de Vie 1-2 Flavoured Wines / Vins Aromatises 56-57 Gin - Dry /Gin sec & Gin-Geneva/Gin geneve 2-4 Imported Fruit Wines / Vins de Fruits-Importes 57 Miscellaneous Spirits / Spiritueux divers 12-13 Imported Sparkling Wine /Vins Mousseaux-Importée 58-64 Rum / Rhum 13-17 Imported Red Table Wine /Vins Rouges-Importée 64-96 Tequila / Mezcal / Mezcal 17-20 Imported Rosé Wine / Vin de Table-Rose Importée 96-101 Vodka 20-26 Imported White Table Wine / Vins Blanc-Importée 101-118 Whiskey - Bourbon / Whiskey- bourbon 28-29 Imported -

SYSCO VANCOUVER PRODUCT LISTING GUIDE Updated: February 2019

SYSCO VANCOUVER PRODUCT LISTING GUIDE updated: February 2019 ARDENT MILLS - updated April 2018 ManufacturerSkuBrand Description PackSizeText DistributorSku StockingStatus 10030 Robin Hood All - O - Wheat Whole Wheat Flour 1/20 KG 6413045 A 10082 Robin Hood Bakers Hood All Purpose Flour UB 1/20 KG 6518496 A 10089 Robin Hood Bakers Hood Bleached All Purpose 1/20 KG 6416800 A 10090 Robin Hood Bakers Hood All Purpose Flour 2/10 KG 6417693 A 10092 Robin Hood Bakersource All Purpose Flour 1/20 KG 9665589 A 10134 Primo Mulino Neapolitan Style Pizza Flour 1/20 KG 1922867 A 10287 Robin Hood Wheatlets 2 Coarse Wheat Granules 1/20 KG 6416337 A 10450 Arrezzio Pizza Flour UB 1/20 KG 9665480 A 10472 Robin Hood Bakersource Classic Strong Bakers 1/20 KG 9665605 A 10496 Robin Hood Keynote 45 Strong Bakers UB 1/20 KG 6429821 A 11013 Robin Hood Brodie Self Rising Flour 1/20 KG 6416719 A 11066 Robin Hood Peach Pastry Cake & Pastry Flour 1/20 KG 6429835 A 11810 Robin Hood Red River Cereal Oats 1/10 KG 6429783 A 11895 Robin Hood Light Rye 1/20 KG 6426466 SO 13505 Robin Hood Classic Custard Mix 1/10 KG 3214196 A 13211 Robin Hood Classic Scone Mix 1/20 KG 6429801 A 13215 Robin Hood Scone Mix Reduced Sodium 1/20 KG 1206665 SO 13323 Robin Hood Bran Muffin Mix LFC Free 1/10 KG 6398271 A 13575 Robin Hood Tea Biscuit Mix 1/10 KG 6429817 A 13602 Robin Hood Corn Bread/Muffin Mix 1/10 KG 6403721 A 13614 Robin Hood Variety Cookie Base Mix 1/20 KG 6412680 SO 13626 Robin Hood Plain Muffin Mix 1/20 KG 6410569 A 13637 Robin Hood Deluxe Bran Muffin 1/20 KG 6410528 A 13788 -

Avril - April 2015 Conagra Maître Saladier Pogo À Table Saucisses Sur Bâtonnet Salade De Chou Wieners on a Stick ¢ Blanche Crémeuse 120 Un

SPÉCIMEN Snack-Bar Avril - April 2015 Conagra Maître Saladier Pogo À Table Saucisses sur bâtonnet Salade de chou Wieners on a stick ¢ blanche crémeuse 120 un. 50 Creamy white coleslaw ¢ 5 kg 20 Skoulakis Lanières de poulet précuit Parmalat assaisonnées Mozzabene Precooked seasoned Fromage râpé style pub chicken strips $ Pub-style grated cheese $ 2 x 2,5 kg 1 4 x 2,27 kg 1 Menu Original Philly Rondelles d’oignon Boeuf tranché Onion rings ¢ Sliced beef ¢ 4 kg 25 40 x 110 g 25 Nachos triangulaires Weston Triangular nachos ¢ Pepe’s 6 x 454 g 25 Tortillas 10” ¢ Burgers de boeuf 12 x 12 un. 35 Beef burgers ¢ 56 x 91 g 25 Unilever Krispy Kernels Hellmann’s Vinaigrette / Dressing Arachides salées Salade de chou crémeuse Salted peanuts ¢ Creamy coleslaw ¢ 108 x 60 g 20 2 x 3,78 L 35 Yum Yum Croustilles / Chips BBQ ¢ 30 x 65 g 20 Lafleur Saucisses fumées, 6” Wieners, 6” 12 / lb ¢ 2 x 3 kg 60 Pour plus d’informations, contactez votre représentant. For more informations, contact your representative. Lassonde Kellogg’s Everfresh Frosted Flakes Jus d’orange concentré, 3 + 1 Céréales en sac Concentrated orange juice, Cereal in bag ¢ 3 + 1 ¢ 6 x 950 g 50 12 x 1 L 50 Dare Tropical Oasis Simple Plaisirs Jus de fraises surgelé Biscuits / Cookies Frozen strawberry juice ¢ 200 x 2 un. ¢ 12 x 960 ml 50 50 Agropur Louis Dreyfus Whole Sun Natrel Jus d’orange surgelé Crème, 10 % / Cream, 10% Frozen orange juice ¢ Portions ¢ 48 x 170 ml 25 200 x 15 ml 30 Canada Dry-Motts Mondelez– Christie Garden Cocktail Biscuits Thé social Cocktail de légumes Social Tea cookies ¢ Vegetable cocktail ¢ 200 x 2 un.