Music Broadcast

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Economic Impact of the Recorded Music Industry in India September 2019

Economic impact of the recorded music industry in India September 2019 Economic impact of the recorded music industry in India Contents Foreword by IMI 04 Foreword by Deloitte India 05 Glossary 06 Executive summary 08 Indian recorded music industry: Size and growth 11 Indian music’s place in the world: Punching below its weight 13 An introduction to economic impact: The amplification effect 14 Indian recorded music industry: First order impact 17 “Formal” partner industries: Powered by music 18 TV broadcasting 18 FM radio 20 Live events 21 Films 22 Audio streaming OTT 24 Summary of impact at formal partner industries 25 Informal usage of music: The invisible hand 26 A peek into brass bands 27 Typical brass band structure 28 Revenue model 28 A glimpse into the lives of band members 30 Challenges faced by brass bands 31 Deep connection with music 31 Impact beyond the numbers: Counts, but cannot be counted 32 Challenges faced by the industry: Hurdles to growth 35 Way forward: Laying the foundation for growth 40 Conclusive remarks: Unlocking the amplification effect of music 45 Acknowledgements 48 03 Economic impact of the recorded music industry in India Foreword by IMI CIRCA 2019: the story of the recorded Nusrat Fateh Ali-Khan, Noor Jehan, Abida “I know you may not music industry would be that of David Parveen, Runa Laila, and, of course, the powering Goliath. The supercharged INR iconic Radio Ceylon. Shifts in technology neglect me, but it may 1,068 crore recorded music industry in and outdated legislation have meant be too late by the time India provides high-octane: that the recorded music industries in a. -

Pvt. C&S Tv Channels

[ Lok Sabha Unstarred Question No. 3416 'Annexure‐I' " ] PVT. C&S TV CHANNELS Sl.No. Sl.No. Genre Channel Name all Star Plus Colors Viacom18 Z Zee TV LIFE OK SONY ENTERTAINMENT TV 1 Hindi GEC SONY SAB Star Utsav Sahara One BIG Magic Z Smile 9X Aaj Tak ABP News India TV Zee News India News NDTV India News 24 IBN 7 Samay 2 Hindi News Tez P7 news NEWS EXPRESS Live India 4 REAL NEWS Disha Channel Total TV SHRI NEWS Sudarshan News Janta TV Channel One News KHABRAIN ABHI TAK A2Z News Aryan TV Aap Ki Awaaz Azad News Khoj India Jain TV GNN News Khabar Bharti Lemon TV99 Zee Cinema Star Gold SONY MAX UTV Movies UTV Action Z Classic 3 Hindi Movie FILMY B4U Movies Z Action Z Premier Enter 10 Television Manoranjan TV V UTV Bindass 4 Hindi Music MTV SONY MIX 9X M Mastii B4U Music Z ETC Music Express Z Business CNBC Awaaz CNBC TV 18 5 Business Channel ET Now NDTV Profit Bloomberg UTV POGO CN Cartoon Network 6 Kids Channel NICK SONIC Zoom Zing Food Food Hindi Life Style NDTV Good Times 7 Channel ZEE KHANA KHAZANA Zee Trendz Vision Shiksha Vision TV Aastha Sanskar Divya Bhakti TV 8 Hindi Spiritual Z Jagran Sadhna Aastha Bhajan SANATAN TV KAATYAYANI Jinvani Dilli Aaj Tak Sahara Samay NCR Har Raj Regional News 9 INDIA NEWS HARYANA Delhi TAAZA TV Perls NCR-Har - Raj AXN Z Cafe 10 English GEC BIG CBS LOVE BIG CBS PRIME BBC ENTERTAINMENT NDTV 24X7 CNN/IBN Times Now Headlines Today 11 English News News X NEWS 9 HY TV AYUR LIVING INDIA HBO SONY PIX Movies Now 12 English Movie Z Studio UTV WORLD MOVIES Firangi VH1 13 English Music BIG CBS SPARK Star Jalsha 14 Bangla GEC Z Bangla ETV Bangla Aakash Bangla RUPASHI BANGLA ABP Ananda 24 Ghanta Kolkata TV 15 Bangla News NEWS TIME BANGLA RPLUS Channel 10 S BANGLA 16 Bangla Music Dhoom Music Tara Music 17 Bangla Movie SONY AATH Mahuaa Sobhagya Mithila Hamar TV 18 Bihar GEC TV100 Himalaya Raftaar Maurya TV Pvt. -

A Study on the Role of Public and Private Sector Radio in Women's

Athens Journal of Mass Media and Communications- Volume 4, Issue 2 – Pages 121-140 A Study on the Role of Public and Private Sector Radio in Women’s Development with Special Reference to India By Afreen Rikzana Abdul Rasheed Neelamalar Maraimalai† Radio plays an important role in the lives of women belonging to all sections of society, but especially for homemakers to relieve them from isolation and help them to lighten their spirit by hearing radio programs. Women today play almost every role in the Radio Industry - as Radio Jockeys, Program Executives, Sound Engineers and so on in both public and private radio broadcasting and also in community radio. All India Radio (AIR) constitutes the public radio broadcasting sector of India, and it has been serving to inform, educate and entertain the masses. In addition, the private radio stations started to emerge in India from 2001. The study focuses on private and public radio stations in Chennai, which is an important metropolitan city in India, and on how they contribute towards the development of women in society. Keywords: All India Radio, private radio station, public broadcasting, radio, women’s development Introduction Women play a vital role in the process of a nation’s change and development. The Indian Constitution provides equal status to men and women. The status of women in India has massively transformed over the past few years in terms of their access to education, politics, media, art and culture, service sectors, science and technology activities etc. (Agarwal, 2008). As a result, though Indian women have the responsibilities of maintaining their family’s welfare, they also enjoy more liberty and opportunities to chase their dreams. -

Audio Production Techniques (206) Unit 1

Audio Production Techniques (206) Unit 1 Characteristics of Audio Medium Digital audio is technology that can be used to record, store, generate, manipulate, and reproduce sound using audio signals that have been encoded in digital form. Following significant advances in digital audio technology during the 1970s, it gradually replaced analog audio technology in many areas of sound production, sound recording (tape systems were replaced with digital recording systems), sound engineering and telecommunications in the 1990s and 2000s. A microphone converts sound (a singer's voice or the sound of an instrument playing) to an analog electrical signal, then an analog-to-digital converter (ADC)—typically using pulse-code modulation—converts the analog signal into a digital signal. This digital signal can then be recorded, edited and modified using digital audio tools. When the sound engineer wishes to listen to the recording on headphones or loudspeakers (or when a consumer wishes to listen to a digital sound file of a song), a digital-to-analog converter performs the reverse process, converting a digital signal back into an analog signal, which analog circuits amplify and send to aloudspeaker. Digital audio systems may include compression, storage, processing and transmission components. Conversion to a digital format allows convenient manipulation, storage, transmission and retrieval of an audio signal. Unlike analog audio, in which making copies of a recording leads to degradation of the signal quality, when using digital audio, an infinite number of copies can be made without any degradation of signal quality. Development and expansion of radio network in India FM broadcasting began on 23 July 1977 in Chennai, then Madras, and was expanded during the 1990s, nearly 50 years after it mushroomed in the US.[1] In the mid-nineties, when India first experimented with private FM broadcasts, the small tourist destination ofGoa was the fifth place in this country of one billion where private players got FM slots. -

SL NO. AGENCY NAME STATE 1 BIG FM Tirupati ANDHRA PRADESH 2 SFM Tirupathi ANDHRA PRADESH 3 SFM Vijaywada ANDHRA PRADESH 4 SFM Ra

List of Pvt FM to whom BOC issued advertisement during 2016-17 SL NO. AGENCY NAME STATE 1 BIG FM Tirupati ANDHRA PRADESH 2 SFM Tirupathi ANDHRA PRADESH 3 SFM Vijaywada ANDHRA PRADESH 4 SFM Rajamundri ANDHRA PRADESH 5 Radio Mirchi-Vijaywada ANDHRA PRADESH 6 Radio City Vizag ANDHRA PRADESH 7 Radio Mirchi 98.3, Vishakhapatnam ANDHRA PRADESH 8 Gup-Shup 94.3 FM Guwahati ASSAM 9 BIG FM Guwahati ASSAM 10 Red FM Guwahati ASSAM 11 Radio Mirchi-Patna BIHAR 12 Radio Dhamaal - Muzaffarpur BIHAR 13 My FM - Chandigarh CHANDIGARH 14 Radio Mirchi-Rajkot CHHATTISGARH 15 My FM Bilaspur CHHATTISGARH 16 My Fm 94.3 Raipur CHHATTISGARH 17 Radio Tadka Raipur CHHATTISGARH 18 ISHQ FM - DELHI DELHI 19 Hit 95 FM Delhi DELHI 20 Fever 104 FM Bangalore DELHI 21 BIG FM Vishakhapatnam DELHI 22 Best FM Thrissur DELHI 23 Best FM, Kannur DELHI 24 Radio City Surat DELHI 25 Rangila Raipur DELHI 26 RED FM Cochin DELHI 27 Fever 104- Delhi DELHI 28 Radio City-Nagpur DELHI 29 Radio City-jalgaon DELHI 30 Aamar FM- Kolkatta DELHI 31 Power FM- Kolkatta DELHI 32 Radio One -Delhi DELHI 33 Suryan FM Tirunelveli DELHI 34 Visakha FM Suryan DELHI 35 RADIO MIRCHI, DELHI DELHI 36 SURYAN FM Chennai DELHI 37 RED FM, DELHI DELHI 38 Radio City Delhi DELHI 39 BIG FM Panaji GOA 40 Indigo Panaji GOA 41 My FM 94.3 Ahmedabad GUJARAT 42 Red FM Ahmedabad GUJARAT 43 Radio One 94.3 FM, Ahmedabad GUJARAT 44 BIG FM Rajkot GUJARAT 45 Big FM Baroda GUJARAT 46 RADIO MIRCHI, AHMEDABAD GUJARAT 47 Radio City-Baroda GUJARAT 48 Radio Mirchi Surat GUJARAT 49 Radio Mirchi-Baroda GUJARAT 50 Radio Mirchi-Raipur -

Download Speed >=512 Kbps)

Telecom Regulatory Authority of India The Indian Telecom Services Performance Indicators April - June, 2014 New Delhi, India 7th November, 2014 Mahanagar Doorsanchar Bhawan, Jawahar Lal Nehru Marg, New Delhi-110002 Tel: +91-11- 23230752, Fax: +91-11- 23236650 Website: www.trai.gov.in Disclaimer The Information and Statistics contained in this report are derived from variety of sources, but are mainly reliant on data obtained from Service Providers. This report does not constitute commercial or other advice. No warranty, representation or undertaking of any kind, express or implied, is given in relation to the information and statistics contained in this report. Table of Contents Snapshot ......................................................................................................... i Trends at a Glance .......................................................................................... xi Introduction ................................................................................................. xiii Chapter 1 : ...................................................................................................... 1 Subscription Data ............................................................................................ 1 Section A : Access Service - An Overview .......................................................... 2 Section B : Wireless Service ........................................................................... 11 Section C : Wireline Service .......................................................................... -

Campaign Period : 24Th February'11 to 10Th March'11

PRASAR BHARATI (Broadcasting Corporation of India) DG: Doordarshan Development Communication Division Doordarshan Bh awan New Delhi Media plan –II Campaign Period : 24th February’11 to 10th March’11 A) National-Network & DD-News Channel Telecast Dates Telecast Details 24th Feb.’11 One Spot of 30 sec once after Hindi Samachar in to Morning at 7:15am for 15days. 10th March.’11 One Spot of 30 sec before Hindi Samachar once at 8:15 (15 days) pm for 15days. 24th Feb.’11 Five Spots of 30 sec daily with Women Oriented to Programme & Serials once at 1:00pm, once at 1:30pm, 10th March.’11 once at 2:00pm once at 2:30pm & once at 3:00pm for (13 days) 13 days. National (Monday-Saturday) Network 24th Feb.’11 DD-1 to Once spot of 30 sec daily at 9:30pm for 11 days. 10th March.’11 (Sunday to Thursday) (11 days) (Sunday - Thursday) 25th Feb.’11 & Two Spots of 30 secs with Friday Feature Film once at 4th March.’11 10:00pm & other at 10:3opm for 2 Fridays. (2 Fridays) 26thFeb.’11 & Two Spots of 30 secs with Saturday Feature Film once 5th March’11 at 10:00pm &other at 10: 3o pm for 2 Saturdays. (2 Saturdays) 27thFeb.’11 & Two spots of 30sec in-between Sunday Feature Film 6th March’11 (4:00pm to 6:30pm) r for 2Sundays. Delhi LPT (2 Sundays) 24th Feb.’11 to Five Spots of 30 sec in-between 7:00pm to 10:30pm DD-News 10th March.’11 respectively for 15days. (15 days) B) Regional Kendras Channel Telecast Details Of Telecast Dates Ahmadabad One Spot of 30 Sec daily in between Bhopal Regional News for Bangalore (15 Days.) Bhubaneswar 24th Feb.’11 Chennai to Delhi Lpt 10th March.’11 Guwathi (15 days) Hyderabad Jalandhar Jaipur Kolkata Lucknow Patna Ranchi Raipur Mumbai Srinagar Thiruvananthapuram C) North-East Kendras Kendra Telecast Days Telecast Details Aizwal One spot of 30 sec once before Regional News at 7:00pm for 15days. -

A Look Into How India's Only Music Station Is Raising the Bar for Brand

For Nokia, Mahindra Xylo, Perfetti-Chocoliebe Eclairs Plus, Kurkure, Pantaloons, LIC, Strepsils… A look into how India’s only Music Station is raising the bar for brand solutions on radio. 1 2 INSIDE Contents December 2010 4 Comment Focus on Music Specialists: What is a music station? Why a music station? How Radio One is playing tunes that are music to MUSIC the ears of both their clients and the listeners. WORKS! Today, when every other radio 5 Musical solutions by Radio One station plays the same music and it A showcase of various case studies highlighting has become the innovative ways in which the music station difficult to tell helped the big brands reach their target groups. one station from another, Radio One stands out. With maximum music 10 Case Studies and maximum How 94.3 Radio One created Karaoke magic for choices, the music Mahindra Xylo, the campaign deatails. station helps promote diverse genres of music. A look at how the 12 Interview ‘music speacialists’ work. The brand ambassadors of 94.3 Radio One, SEL - the country’s most loved music band and the kings of heartening melodies and beats are making music work. Some excerpts... ............................................. By Ankit Bhatnagar 14 Interview [email protected] Vineet Singh Hukmani, managing director, Radio One gives a lowdown on how the music station has specialised the trade, even without going niche. afaqs! explores... 16 Interview Music is core to a radio station’s existence. If the music played is the best, popularity of the station is highest thinks Vivek Nayer. Some excerpts on how he thinks radio works. -

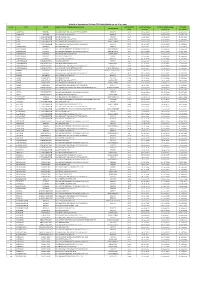

Details of Operational Private FM Radio Station As on 16.07.2021 S

Details of Operational Private FM Radio Station as on 16.07.2021 S. NO. CITY STATE NAME OF THE PERMISSION HOLDER FREQUENCY DATE OF GOPA/ DATE OF OPERATION- LICENSE CHANNEL ID MHz MGOPA ALISATION VALIDITY 1 AGARTALA TRIPURA M/S RELIANCE BROADCAST NETWORK LTD. BIG FM 92.7 05-04-2016 01-04-2017 31-03-2032 2 AGARTALA TRIPURA M/S SOUTH ASIA FM LTD. RED FM 95 20-06-2018 08-06-2019 07-06-2034 3 AGRA UTTAR PRADESH M/S HT MEDIA LTD. FEVER 93.7 11-02-2016 19-08-2016 18-08-2031 4 AGRA UTTAR PRADESH M/S MUSIC BROADCAST LTD. RADIO CITY 91.9 02-02-2017 01-04-2015 31-03-2030 5 AGRA UTTAR PRADESH M/S RAJASTHAN PATRIKA PVT. LTD. RADIO TADKA 94.5 05-04-2016 07-03-2017 06-03-2032 6 AGRA UTTAR PRADESH M/S RELIANCE BROADCAST NETWORK LTD. BIG FM 92.7 19-11-2015 01-04-2015 31-03-2030 7 AHMEDABAD GUJARAT M/S DB CORP LTD. MY FM 94.3 18-11-2015 01-04-2015 31-03-2030 8 AHMEDABAD GUJARAT M/S ENTERTAINMENT NETWORK INDIA LTD. RADIO MIRCHI 98.3 30-09-2015 01-04-2015 31-03-2030 9 AHMEDABAD GUJARAT M/S ENTERTAINMENT NETWORK INDIA LTD. MIRCHI LOVE 104 05-04-2016 05-09-2016 04-09-2031 10 AHMEDABAD GUJARAT M/S MUSIC BROADCAST LTD. RADIO CITY 91.1 10-11-2015 01-04-2015 31-03-2030 11 AHMEDABAD GUJARAT M/S NEXT RADIO LTD. -

Remote Audiences Beyond 2000 : Radio, Everyday Life and Development in South India

Edith Cowan University Research Online Theses: Doctorates and Masters Theses 1-1-2002 Remote audiences beyond 2000 : radio, everyday life and development in South India Thomas J. Yesudhasan Edith Cowan University Follow this and additional works at: https://ro.ecu.edu.au/theses Part of the Radio Commons Recommended Citation Yesudhasan, T. J. (2002). Remote audiences beyond 2000 : radio, everyday life and development in South India. https://ro.ecu.edu.au/theses/729 This Thesis is posted at Research Online. https://ro.ecu.edu.au/theses/729 Edith Cowan University Copyright Warning You may print or download ONE copy of this document for the purpose of your own research or study. The University does not authorize you to copy, communicate or otherwise make available electronically to any other person any copyright material contained on this site. You are reminded of the following: Copyright owners are entitled to take legal action against persons who infringe their copyright. A reproduction of material that is protected by copyright may be a copyright infringement. Where the reproduction of such material is done without attribution of authorship, with false attribution of authorship or the authorship is treated in a derogatory manner, this may be a breach of the author’s moral rights contained in Part IX of the Copyright Act 1968 (Cth). Courts have the power to impose a wide range of civil and criminal sanctions for infringement of copyright, infringement of moral rights and other offences under the Copyright Act 1968 (Cth). Higher penalties may apply, and higher damages may be awarded, for offences and infringements involving the conversion of material into digital or electronic form. -

Media Ecosystems: the Walls Fall Down

Media ecosystems: The walls fall down KPMG in India’s Media and Entertainment report 2018 September 2018 kpmg.com/in Media ecosystems: The walls fall down KPMG in India’s Media and Entertainment report 2018 We would like to thank all those who have contributed and shared their valuable domain insights in helping us put this report together. Image courtesy Makuta VFX Prime Focus Ltd Reliance Animation Sony Pictures Network India Toonz Animation Viacom 18 Media Pvt Ltd Yash Raj Films Zee Entertainment Enterprises Ltd • The information contained in Media ecosystems: The walls fall down report is of a general nature and is not intended to address the circumstances of any particular individual or entity. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. • Although we have attempted to provide correct and timely information, there can be no guarantee that such information is correct as of the date it is received or that it will continue to be correct in the future. • The report contains information obtained from the public domain or external sources which have not been verified for authenticity, accuracy or completeness. • Use of companies’ names in the report is only to exemplify the trends in the industry. We maintain our independence from such entities and no bias is intended towards any of them in the report. • Our report may make reference to ‘KPMG Analysis’; this merely indicates that we have (where specified) undertaken certain analytical activities on the underlying data to arrive at the information presented; we do not accept responsibility for the veracity of the underlying data. -

Fundam Entals of Journalism and Mass Communication

FUNDAM ENTALS OF JOURNALISM AND MASS COMMUNICATION MA [Mass Communication and Journalism] First Year Paper I MANONMANIAM SUN DARANAR UNIVERSITY Directorate of Distance and Continuing Education Abishekapatti, Tirunelveli-627 012 Tamilnadu, lndia Authots Dr Hemant Joshl, Associate Prcfessor cf Hindi Jo.rmalism at llMC, New Delhi Manjarl Joshl, Nannreader, Ddhi Doordarshan Copyright @ Authors, 201 1 All rights res6N€d. No part of this publlcauon whlch is material protoclsd bythis copyright notica may be reproducedortrensmitied or utillzed orstored in anyform or byanymaans now known or her€inaft€r in\Iented, elsctronic, digital or mochanical, including photocopying, scanning, rocording or by any information storage or retrieval s]istem, withoul prior written p€rmission from the Publisher. lnformation contained in thls book has been published by VIKAS@ Publishing House hi. Ltd. and has be6n obtained by ib Authors from Bourcos belie\,€d to be reliable and are conect to the best of thoir knowledge. Howe\Ier, the Publisher and its Authors shall in no e\ent be liabl€ for any errors, omissions or damages arising out of use of this lnformation and specifically disclaim any implied warranties or msrchantability or fitnass for anyparlicular usa. m Vikas@ is the registeed trademark of Vikas@ Publishing Ho.rse Art. Ltd. VKAS@ PUBLISHING HOUSE PVr. LTD. E-28, Sector-8, Ncida - 201301 (UP) Phone: 0120-4078900 e Fax 0'120-4078999 Regd. Office: 576, Masjid Road, Jangpura, New Delhi 110 014 o Website: www.vikaspublishing.con o Email: [email protected] SYLLABI-BOOK MAPPING TABLE Fundamentals of Journalism and Mass Communication Syllabi Mapping in Book Unit 1 Definition of Journalism: Unit 1: Joumalism: Nature, Nature, Scope, Functions, Role of Press in Democracy, Scope and Functions Principles of Journalism, Kinds of Journalism.