Oil Prices Facts and Stats

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WTI Crude Oil West Texas Intermediate

WTI Crude Oil West Texas Intermediate Alexander Filitz Minh Khoa Nguyen Outline • Crude Oil • Value Chain • Politics • Market • Demand • Facts & Figures • Discussion Crude Oil • Flammable liquid consisting of a complex mixture of hydrocarbons of various molecular weights and other liquid organic compounds • Is recovered mostly through oil drilling • In its strictest sense, petroleum includes only crude oil, but in common usage it includes all liquid, gaseous, and solid hydrocarbons. • An oil well produces predominantly crude oil, with some natural gas dissolved in it Classification • By the geographic location it is produced in • Its API gravity (an oil industry measure of density) • Its sulfur content • Some of the common reference crudes are: • West Texas Intermediate (WTI), a very high-quality, sweet, light oil delivered at Cushing, Oklahoma for North American oil. • Brent Blend, comprising 15 oils from fields in the North Sea. • Dubai-Oman, used as benchmark for Middle East sour crude oil flowing to the Asia-Pacific region • The OPEC Reference Basket, a weighted average of oil blends from various OPEC (The Organization of the Petroleum Exporting Countries) countries West Texas Intermediate • Also known as Texas light sweet, used as a benchmark in oil pricing • API gravity of around 39.6 and specific gravity of 0.827 and 0.24% sulfur • WTI is refined mostly in the Midwest and Gulf Coast regions in the U.S • It is the underlying commodity of New York Mercantile Exchange's (NYMEX) oil futures contracts • Often referenced in news reports -

Monthly Report on Petroleum Developments in the World Markets February 2020

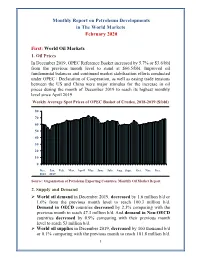

Monthly Report on Petroleum Developments in The World Markets February 2020 First: World Oil Markets 1. Oil Prices In December 2019, OPEC Reference Basket increased by 5.7% or $3.6/bbl from the previous month level to stand at $66.5/bbl. Improved oil fundamental balances and continued market stabilization efforts conducted under OPEC+ Declaration of Cooperation, as well as easing trade tensions between the US and China were major stimulus for the increase in oil prices during the month of December 2019 to reach its highest monthly level since April 2019. Weekly Average Spot Prices of OPEC Basket of Crudes, 2018-2019 ($/bbl) 80 70 60 50 40 30 20 10 0 Dec. Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec. 2018 2019 Source: Organization of Petroleum Exporting Countries, Monthly Oil Market Report. 2. Supply and Demand World oil demand in December 2019, decreased by 1.6 million b/d or 1.6% from the previous month level to reach 100.3 million b/d. Demand in OECD countries decreased by 2.3% comparing with the previous month to reach 47.3 million b/d. And demand in Non-OECD countries decreased by 0.9% comparing with their previous month level to reach 53 million b/d. World oil supplies in December 2019, decreased by 100 thousand b/d or 0.1% comparing with the previous month to reach 101.8 million b/d. 1 Non-OPEC supplies remained stable at the same previous month level of 67.2 million b/d. Whereas preliminary estimates show that OPEC crude oil and NGLs/condensates total supplies decreased by 0.6% comparing with the previous month to reach 34.5 million b/d. -

Price Forecast June 30, 2015 Contents

Resource Evaluation & Advisory Price forecast June 30, 2015 Contents Canadian price forecast 1 International price forecast 5 Global outlook 6 Western Canada royalty comparison 8 Pricing philosophy 11 Glossary 12 Canadian domestic price forecast Forecast commentary Andrew Botterill Senior Manager, Resource Evaluation & Advisory “Everything is in a state of fl ux, including status quo” - Robert Byrne As industry adjusts to the “new normal” we have analyzed This narrowing has been most notable on the heavy oil in our last two forecasts, activities in the energy sector side, where diff erentials have decreased more than 30 per are beginning to demonstrate a cautious, but optimistic cent compared with where they were in summer 2014. view of the future. While not anticipating $100 oil in the With greater than 60 per cent of Canadian production near term, these views show an expectation industry will being from oil sands (CAPP 2015 forecast report) the bring a more focused approach to North American oil narrowing of heavy diff erentials is welcome news to much development within the coming 12 to 18 months. of the sector. In recent weeks, the WTI to heavy diff erential has been narrower than we have seen recently as In recent weeks, Canadian-received oil prices have been production from some projects was shut-in due to wildfi res stronger relative to the beginning of the year, with daily in northern Alberta. The shut-in production has since been WTI settlements hovering around $60/bbl USD and brought back on-stream, which has slowed the narrowing Canadian Light settlements greater than $70/bbl CAD. -

The Cost of Pipeline Constraints in Canada by Elmira Aliakbari and Ashley Stedman

FRASER RESEARCH BULLETIN FROM THE CENTRE FOR NATURAL RESOURCE STUDIES May 2018 The Cost of Pipeline Constraints in Canada by Elmira Aliakbari and Ashley Stedman MAIN CONCLUSIONS Despite the steady growth in crude oil From 2013 to 2017, after accounting for available for export, new pipeline proj- quality differences and transportation ects in Canada continue to face delays costs, the depressed price for Canadian related to environmental and regula- heavy crude oil has resulted in CA$20.7 tory impediments as well as political billion in foregone revenues for the Ca- opposition. nadian energy industry. This significant loss is equivalent to almost 1 percent of Canada’s lack of adequate pipeline ca- Canada’s national GDP. pacity has imposed a number of costly constraints on the nation’s energy sec- In 2018, the average price differen- tor including an overdependence on tial (based on the first quarter) was the US market and reliance on more US$26.30 per barrel. If the price differ- costly modes of energy transportation. ential remains at the current level, we These and other factors have resulted estimate that Canada’s pipeline con- in depressed prices for Canadian heavy straints will reduce revenues for Cana- crude (Western Canada Select) relative dian energy firms by roughly CA$15.8 to US crude (West Texas Intermediate) billion in 2018, which is approximately and other international benchmarks. 0.7 percent of Canada’s national GDP. Between 2009 and 2012, the average Insufficient pipeline capacity has re- price differential between Western sulted in substantial lost revenue for Canada Select (WCS) and West Texas the energy industry and thus imposed Intermediate (WTI) was about 13 per- significant costs on the economy as a cent of the WTI price. -

The Price of Oil Risk

The Price of Oil Risk Steven D. Baker,∗ Bryan R. Routledge,y [February 10, 2017] Abstract We solve a Pareto risk-sharing problem for two agents with heterogeneous re- cursive utility over two goods: oil, and a general consumption good. Using the optimal consumption allocation, we derive a pricing kernel and the price of oil and related futures contracts. This gives us insight into the dynamics of prices and risk premia. We compute portfolios that implement the optimal consumption policies, and demonstrate that large and variable open interest is a property of optimal risk-sharing. A numerical example of our model shows that rising open interest and falling oil risk premium are an outcome of the dynamic properties of the optimal risk sharing solution. ∗ McIntire School of Commerce, University of Virginia; [email protected]. y Tepper School of Business, Carnegie Mellon University; [email protected]. 1 Introduction The spot price of crude oil, and commodities in general, experienced a dramatic price increase in the summer of 2008. For oil, the spot price peaked in early July 2008 at $145.31 per barrel (see Figure 1). In real-terms, this price spike exceeded both of the OPEC price shocks of 1970's and has lasted much longer than the price spike at the time of the Iraq invasion of Kuwait in the summer of 1990. The run-up to the July 2008 price of oil begins around 2004. Buyuksahin, Haigh, Harris, Overdahl, and Robe (2011) and Hamilton and Wu (2014) identify a structural change in the behavior of oil prices around 2004. -

The Impact of the U.S Fracking Boom on the Price of Oil and on Arab Oil Producers

The Impact of the U.S Fracking Boom on the Price of Oil and on Arab Oil Producers Lutz Kilian University of Michigan CEPR Background ● Shale oil production became possible because of technological innovation (horizontal drilling, hydraulic fracturing (fracking), microseismic imaging). ● The rapid expansion of U.S. shale oil production was stimulated by the high price of conventional crude oil after 2003, which made this new technology competitive. ● Since then efficiency gains in shale oil production have lowered its cost, allowing continued production at much lower oil prices. ● Because the price of oil has remained low since 2015, shale oil producers are experiencing increased operating losses and financial stress. The Role of Refineries ● Crude oil is being consumed by refineries that turn crude oil into refined products such as gasoline, diesel, heating oil, jet fuel and heavy fuel oil. ● Not all refineries are alike. Their technical configuration determines which type of crude oil they can process. ● Changing an existing configuration is costly. The Refining Industry in Transition A few years ago, the global refining industry expected a growing shortage of light sweet crude oil worldwide: 1. Refiners along the Texas Gulf Coast invested in new technology that allowed them to become the world leader in processing heavier crudes. This allowed them to process lower priced crudes imported from Saudi Arabia, Venezuela and Mexico. 2. Refiners along the East Coast began to shut down existing refineries for light sweet crude oil in anticipation of a growing shortage of light sweet crude oil. The Glut That No One Saw Coming After 2010 shale oil was shipped in ever increasing quantities from the interior of the country to the U.S. -

2019 Capital Budget & Operating Plan

2019 Capital Budget & Operating Plan Supplemental Information & Investor Update UPDATED AS OF FEBRUARY 2019 Cautionary Statement The following presentation includes forward-looking statements. These statements relate to future events, such as anticipated revenues, earnings, business strategies, competitive position or other aspects of our operations, operating results or the industries or markets in which we operate or participate in general. Actual outcomes and results may differ materially from what is expressed or forecast in such forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that may prove to be incorrect and are difficult to predict such as operational hazards and drilling risks; potential failure to achieve, and potential delays in achieving expected reserves or production levels from existing and future oil and gas development projects; unsuccessful exploratory activities; difficulties in developing new products and manufacturing processes; unexpected cost increases or technical difficulties in constructing, maintaining or modifying company facilities; international monetary conditions and exchange rate fluctuations; changes in international trade relationships, including the imposition of trade restrictions or tariffs relating to crude oil, bitumen, natural gas, LNG, natural gas liquids and any other materials or products (such as aluminum and steel) used in the operation of our business; our ability to collect payment when due under -

Peak Oil Demand and Long-Run Oil Prices

January 2018 Peak Oil Demand and Long-Run Oil Prices Abstract The prospect that global oil demand will gradually slow and eventually peak has created a cottage industry of executives and commentators trying to predict the point at which demand will peak. In this Energy Insight, we argue that this focus seems misplaced. The date at which oil demand will stop growing is highly uncertain and small changes in assumptions can lead to vastly different estimates. More importantly, there is little reason to believe that once it does peak, that oil demand will fall sharply. The world is likely to demand large quantities of oil for many decades to come. Rather, the significance of peak oil is that it signals a shift in paradigm – from an age of (perceived) scarcity to an age of abundance – and with it is likely to herald a shift to a more competitive market environment. This change in paradigm is also likely to pose material challenges for oil producing economies as they try both to ensure that their oil is produced and consumed, and at the same time diversify their economies fit for a world in which they can no longer rely on oil revenues to provide their main source of revenue for the indefinite future. We argue that the extent and pace of this diversification is likely to have an important bearing on oil prices over the next 20 or 30 years. It seems likely that many low-cost producers will delay the pace at which they adopt a more competitive “higher volume, lower price” strategy until they have made material progress in reforming their economies. -

Welcome to the 11Th Edition of Energy Perspectives! This Is An

Welcome to the 11th edition of Energy Perspectives! This is an independent report that informs Equinor’s strategy and offers a fact-based contribution to the energy transition debate. This year’s edition is an update of the edition from November last year, and with a lot happening on the global arena the last 6 months, there is a lot to consider when looking 30 years ahead. As always, this report and its data and conclusions would be impossible without the excellent work of many of my colleagues, to whom I extend my appreciation and gratitude. You are the best! 1 Covid19 is not over. In a global perspective, we are still dealing with its impact and the enormous effects it has on people, societies, economies, and markets. We are not through it yet. And we might have to live with recurring infection spikes, especially in parts of the world that do not get sufficient access to vaccines. Recurring lockdowns entailed that energy demand, and in particular oil demand due to its use as a transport fuel, was hit hard. Recovery is in the making, and faster than many feared, but oil demand, as an example, is still not back to pre-Covid19-levels. The map shows how the pandemic has affected economies across the globe, with almost all countries pink or red, that is, with negative economic development. Industrialised countries are on their way out of recession while disabling the virus, but the uncertainty is still high in many emerging economies. 2 We are seeing signs of recovery. Thanks to the development and rollout of vaccines and massive public spending to stimulate demand, there are signs that the situation is being brought under control so that we can live with the virus more like we do with normal flus. -

U.S.-Canada Cross- Border Petroleum Trade

U.S.-Canada Cross- Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits March 2021 Submitted to: American Petroleum Institute 200 Massachusetts Ave NW Suite 1100, Washington, DC 20001 Submitted by: Kevin DeCorla-Souza ICF Resources L.L.C. 9300 Lee Hwy Fairfax, VA 22031 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits This report was commissioned by the American Petroleum Institute (API) 2 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits Table of Contents I. Executive Summary ...................................................................................................... 4 II. Introduction ................................................................................................................... 6 III. Overview of U.S.-Canada Petroleum Trade ................................................................. 7 U.S.-Canada Petroleum Trade Volumes Have Surged ........................................................... 7 Petroleum Is a Major Component of Total U.S.-Canada Bilateral Trade ................................. 8 IV. North American Oil Production and Refining Markets Integration ...........................10 U.S.-Canada Oil Trade Reduces North American Dependence on Overseas Crude Oil Imports ..................................................................................................................................10 Cross-Border Pipelines Facilitate U.S.-Canada Oil Market Integration...................................14 -

Market Indicators As at End*: August-2020

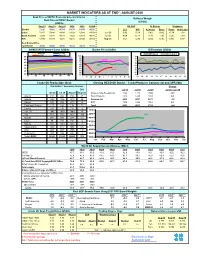

MARKET INDICATORS AS AT END*: AUGUST-2020 Spot Price of OPEC Basket & Selected Crudes Refiners' Margin Real Price of OPEC Basket (US$/b) (US$/b) Aug-18 Aug-19 Aug-20 2018 2019 2020# US Gulf N. Europe Singapore Basket 72.26 59.62 45.19 69.78 64.04 40.50 LLS WTI A. Heavy Brent Oman Arab Light Dubai 72.47 58.88 43.89 69.68 63.48 41.54 Jun-20 3.92 5.19 0.42 0.42 -0.74 1.02 North Sea Dtd 72.64 58.83 44.79 71.22 64.19 40.88 Jul-20 4.64 6.13 -1.86 1.30 1.26 1.99 WTI 67.99 54.84 42.36 65.16 57.02 38.15 Aug-20 3.67 5.30 -2.05 0.16 0.86 0.87 Real Basket Price Jun01=100 46.86 39.02 28.30 35.22 44.73 26.19 NYMEX WTI Forward Curve (US$/b) Basket Price (US$/b) Differentials (US$/b) May-20 Jun-20 WTI-Brent Brent-Dubai Jul-20 Aug-20 50 100 3 90 2 45 2018 80 1 70 40 0 60 35 2019 -1 50 30 40 -2 2020 -3 25 30 20 -4 20 10 -5 1M 3M 5M 7M 9M 11M J F M A M J J A S O N D 03 05 07 11 13 17 19 21 25 27 31 Crude Oil Production (tb/d) Closing OECD Oil Stocks - Crude/Products Commercial and SPR (Mb) Crude Oil Production (Tb/d) Production: Secondary Sources Change Diff. -

The Impact of the Decline in Oil Prices on the Economics, Politics and Oil Industry of Venezuela

THE IMPACT OF THE DECLINE IN OIL PRICES ON THE ECONOMICS, POLITICS AND OIL INDUSTRY OF VENEZUELA By Francisco Monaldi SEPTEMBER 2015 B | CHAPTER NAME ABOUT THE CENTER ON GLOBAL ENERGY POLICY The Center on Global Energy Policy provides independent, balanced, data-driven analysis to help policymakers navigate the complex world of energy. We approach energy as an economic, security, and environmental concern. And we draw on the resources of a world-class institution, faculty with real-world experience, and a location in the world’s finance and media capital. Visit us atenergypolicy. columbia.edu facebook.com/ColumbiaUEnergy twitter.com/ColumbiaUEnergy ABOUT THE SCHOOL OF INTERNATIONAL AND PUBLIC AFFAIRS SIPA’s mission is to empower people to serve the global public interest. Our goal is to foster economic growth, sustainable development, social progress, and democratic governance by educating public policy professionals, producing policy-related research, and conveying the results to the world. Based in New York City, with a student body that is 50 percent international and educational partners in cities around the world, SIPA is the most global of public policy schools. For more information, please visit www.sipa.columbia.edu THE IMPACT OF THE DECLINE IN OIL PRICES ON THE ECONOMICS, POLITICS AND OIL INDUSTRY OF VENEZUELA By Francisco Monaldi* SEPTEMBER 2015 *Francisco Monaldi is Baker Institute Fellow in Latin American Energy Policy and Adjunct Professor of Energy Economics at Rice University, Belfer Center Associate in Geopolitics of Energy at the Harvard Kennedy School, Professor at the Instituto de Estudios Superiores de Administracion (IESA) in Caracas, Venezuela, and Founding Director of IESA’s Center on Energy and the Environment.